- Pharmaceuticals

- Nasal Antiseptic Market

Nasal Antiseptic Market Size, Share, and Growth Forecast 2026 - 2033

Nasal Antiseptic Market by Antiseptic Type (Iodine-based, Others), Formulation (Sprays, Swabs, Ointments), Distribution Channel (Hospital Pharmacies, Others), Application (Infection Control, Others), and Regional Analysis 2026 - 2033

Nasal Antiseptic Market Share, Size, and Trends Analysis

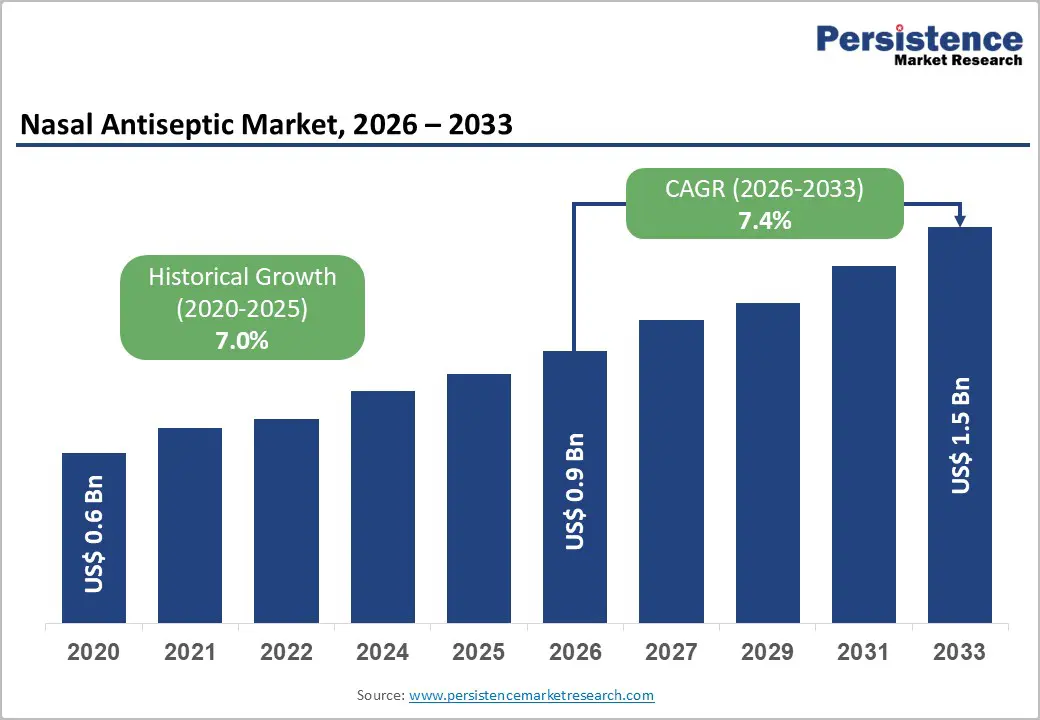

The global nasal antiseptic market size is likely to be valued at US$0.9 billion in 2026 and is projected to reach US$1.5 billion by 2033, growing at a CAGR of 7.4% during the forecast period between 2026 and 2033, driven by the critical need to reduce Healthcare-Associated Infections (HAIs), specifically Surgical Site Infections (SSIs) caused by Staphylococcus aureus.

Growth is further bolstered by the widespread implementation of preoperative decolonization protocols in developed healthcare systems, which favor nasal antiseptics over antibiotic prophylaxis to mitigate antimicrobial resistance (AMR).

Key Industry Highlights

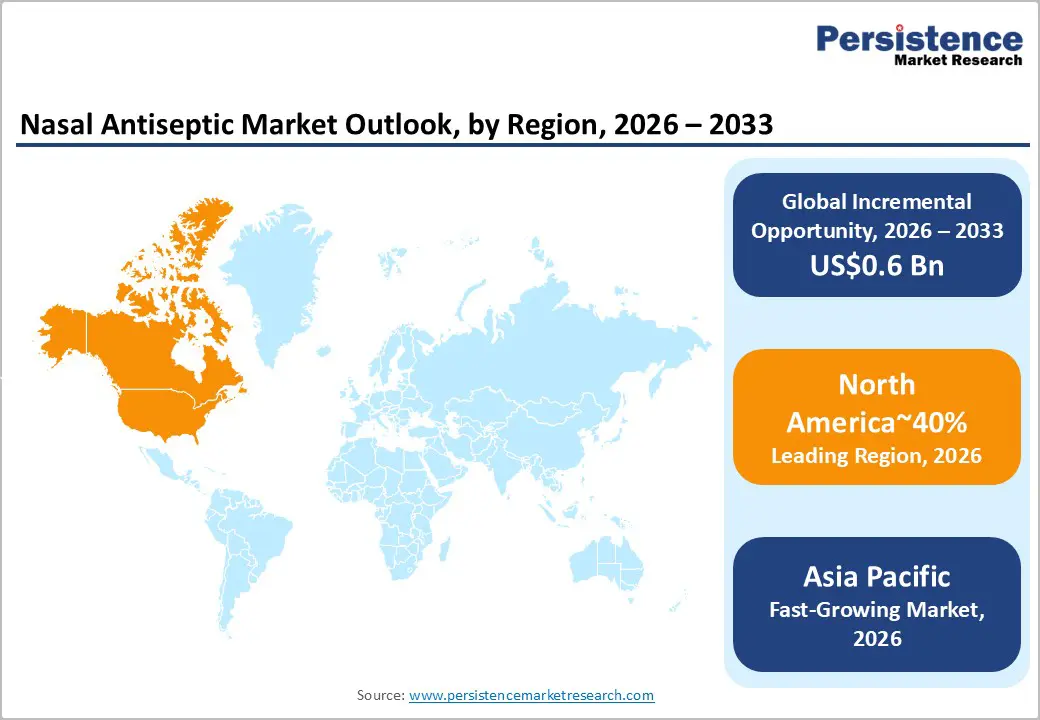

- Leading Region: North America is projected to lead the market with a 40% share in 2026, driven by high surgical volumes, advanced hospital infrastructure, strict FDA compliance, and widespread use of prophylactic nasal antiseptics in infection control.

- Fastest-growing Region: Asia-Pacific is likely to be the fastest-growing region, driven by expanding hospital infrastructure, increased healthcare access, medical tourism, government efforts to reduce hospital-acquired infections, and rising hygiene awareness and disposable incomes in urban and Tier-2 cities.

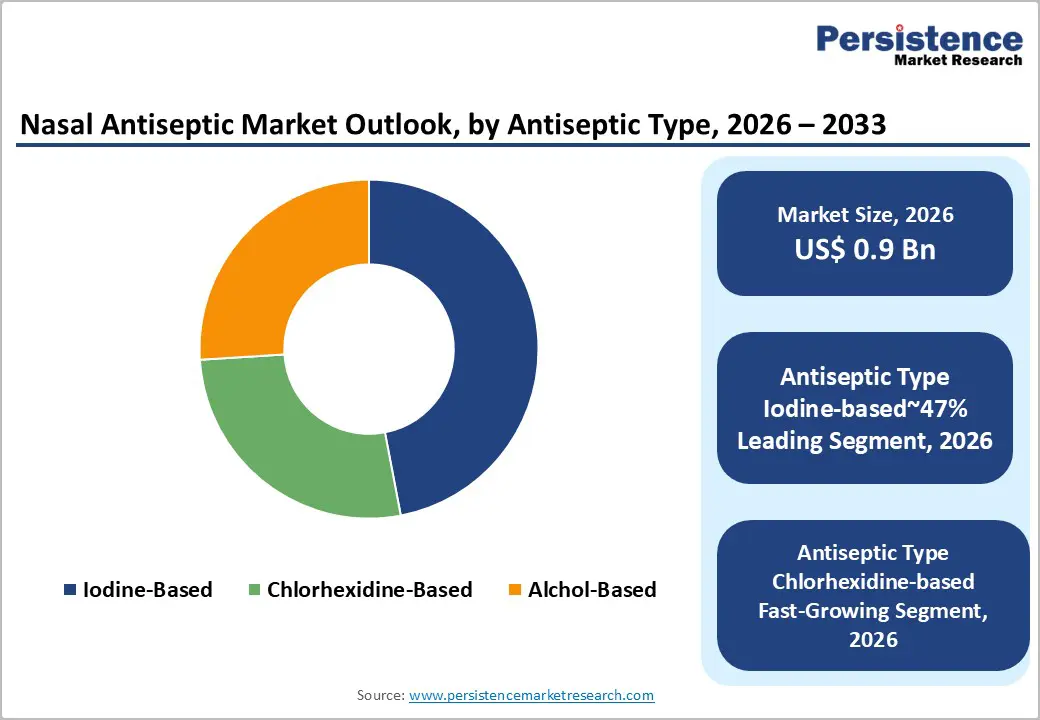

- Leading Antiseptic Type: Iodine-based antiseptics are expected to lead, with an approximately 47% share in 2026, benefiting from broad-spectrum antimicrobial efficacy, clinical trust, and cost efficiency across emerging and developed markets.

- Leading Distribution Channel: Hospital pharmacies are expected to remain the largest channel, with a 50% market share in 2026, owing to clinical protocols, centralized procurement, and high-stakes surgical applications.

- Key Industry Development: In December 2024, Ondine Biomedical launched the LANTERN Phase 3 trial for its light-activated antimicrobial nasal decolonization technology, in partnership with HCA Healthcare. This innovative approach provides strong evidence for rapid, resistance-free decolonization, with trial results showing up to a 50% reduction in healthcare-associated infections (HAIs). It offers hospitals a powerful tool to improve patient safety and enhance operational efficiency.

| Key Insights | Details |

|---|---|

| Nasal Antiseptic Market Size (2026E) | US$0.9 Bn |

| Market Value Forecast (2033F) | US$1.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.0% |

Market Dynamics - Driver, Barrier, and Opportunity Analysis

Surge in Respiratory Virus Prophylaxis Awareness

The post-pandemic normalization of respiratory risk management has structurally expanded demand for preventive nasal solutions positioned as frontline barriers against airborne pathogens. Consumer behavior has shifted from episodic, illness-driven usage toward routine prophylactic adoption in high-exposure environments such as air travel, mass transit, schools, and dense workplaces. This has repositioned nasal antiseptic sprays from niche clinical adjuncts to everyday consumer health products, accelerating penetration across retail pharmacies and direct-to-consumer digital channels. The concept of “chemical masks” resonates strongly with populations seeking protection without the social or physical constraints of traditional face coverings.

This behavioral shift is reinforced by a growing body of clinical evidence supporting the antiviral efficacy of nitric oxide and iodine-based nasal formulations in reducing nasal viral load and limiting early-stage transmission. Unlike systemic interventions, these sprays align with consumer preferences for localized, noninvasive prevention strategies that provide immediate perceived benefit. As a result, spray-based formulations have emerged as the dominant delivery format, capturing a significant share of total demand due to ease of use, portability, and suitability for frequent application. The convergence of heightened health vigilance, clinical validation, and consumer-friendly delivery formats continues to drive sustained growth in this segment.

Mucosal Irritation and Patient Compliance Constraints

A persistent restraint in the nasal antiseptic spray market is the tolerability limitation associated with potent antimicrobial formulations. Alcohol-based carriers and high-strength iodine or oxidative agents can disrupt the nasal mucosa, causing stinging, dryness, and irritation during repeated use. Over time, these effects may impair mucociliary function, which is critical for natural airway defense. For users seeking preventive or routine protection, even mild discomfort can deter use, narrowing the practical window for frequent application outside acute-use scenarios.

This tolerability gap directly undermines patient compliance, particularly in chronic or preventive regimens where consistent daily use is required to achieve efficacy. From a manufacturer's perspective, formulation development is constrained by the need to preserve antimicrobial potency while minimizing epithelial toxicity and sensory discomfort. This balance slows innovation cycles and limits the scalability of more potent active ingredients in the over-the-counter consumer segment. As a result, adoption favors milder formulations, even when more aggressive antiseptics could offer superior viral or bacterial suppression, creating a structural trade-off between efficacy and sustained user adherence.

Innovation in Next-Generation Formulations

Innovation in next-generation nasal antiseptic formulations presents a structurally attractive opportunity for market participants seeking differentiation beyond traditional chemistries. Emerging actives such as nitric oxide, xylitol, and hypochlorous acid enable broad-spectrum antimicrobial performance while maintaining mucosal compatibility during repeated use. Unlike iodine- or alcohol-based sprays, these compounds are compatible with the physiological nasal environment, reducing the risk of irritation and supporting longer treatment durations. This shifts product positioning from short-term prophylaxis toward sustained therapeutic and preventive use.

The opportunity is especially significant in sinusitis and chronic rhinitis, where patients require consistent, non-irritating daily treatments. Comfort-focused efficacy enables manufacturers to overcome compliance challenges associated with existing products, thereby promoting long-term use rather than episodic demand. From a market perspective, these formulations support premium pricing, foster stronger brand loyalty, and offer the potential for physician endorsement in long-term management strategies. In November 2024, Ondine Biomedical secured US$14 million in funding to accelerate its pivotal U.S. Phase 3 trial of Steriwave nasal photo-disinfection technology, advancing R&D for non-antibiotic decolonization. This could lead to FDA approval and widespread adoption in surgical settings, helping address antimicrobial resistance (AMR) and reduce the risk of surgical site infections (SSI) cost-effectively.

Category-wise Analysis

Antiseptic Type Insights

Iodine-based nasal antiseptics are expected to maintain their leadership in the global market, holding approximately 47% share, supported by broad-spectrum antimicrobial efficacy and cost-efficiency in emerging markets. Products such as Betadine (J&J/Purdue) and Halodine are widely used across hospitals and community settings, benefiting from established clinical trust and versatility against viruses, including SARS-CoV-2. Their dominance is reinforced by routine adoption in general hygiene and preventive care, while structured guidance from health authorities and standards for surgical preparation continue to favor iodine formulations in high-volume applications. Ongoing product innovations, such as reduced-iodine nasal sprays for sensitive mucosa, and distribution in both consumer and clinical channels, are most likely to sustain the segment’s structural advantage, ensuring consistent market share and long-term reliability across diverse geographies.

Chlorhexidine (CHG)-based nasal antiseptics are anticipated to be the fastest-growing segment, driven by superior persistent antimicrobial activity and clinical preference for preventing surgical site infections. Leading products such as ChloraPrep (BD) and Soluprep (3M) leverage alcohol blends and pre-filled applicators to deliver precise, single-use dosing that aligns with universal decolonization practices. Rising adoption is supported by increasing emphasis on antimicrobial stewardship, post-pandemic hygiene awareness, and consumer demand for biodegradable, easy-to-use formulations. Market participants, including 3M, BD, and Aptar Pharma, are expected to expand reach through film-forming applicators and Unidose delivery systems, making CHG antiseptics a strategic growth driver across hospitals, outpatient clinics, and at-home preventive care. The growth is also supported by their compatibility with long-term use and skin-sensitive applications.

Distribution Channel Insights

Hospital Pharmacies are expected to remain the largest distribution channel globally, holding an estimated 50% share of clinical-grade nasal antiseptic procurement. Their leadership is anchored in high-stakes environments such as surgical procedures and preoperative decolonization, where standardized protocols favor institutional sourcing of Chlorhexidine (CHG) and Povidone-Iodine (PVP-I) products. Automation in dispensing, including AI-driven inventory systems, is likely to enhance stock management and reduce waste, while centralized procurement networks are anticipated to strengthen bargaining power for high-volume antiseptics. Hospital pharmacies benefit from prescriber-led trust, where products initiated in inpatient settings often continue through outpatient care, creating a ripple effect in brand adoption. Expanding roles in antimicrobial stewardship further positions these pharmacies as critical gatekeepers, ensuring effective use while minimizing the risk of resistance. Leading suppliers such as BD, 3M, Medline, and Cardinal Health are expected to maintain strong institutional penetration through specialized applicators, swabs, and pre-packaged kits.

Online Pharmacies are anticipated to be the fastest-growing distribution channel, supported by a global shift toward digital healthcare and self-directed treatment. Growth is likely to be driven by high product accessibility, discreet purchasing, and competitive pricing models, enabling consumers to obtain specialized nasal antiseptics conveniently. Quick-commerce integration and direct-to-consumer portals are expected to accelerate adoption, while AI-driven personalization helps anticipate refill needs and improve adherence. Online channels are increasingly leveraged for home-use clinical products, including self-administered antiseptics, bridging retail and healthcare applications. Leading global players such as CVS Health, Walgreens Boots Alliance, and Amazon Pharmacy, alongside regional leaders in India such as Apollo 24|7, Tata 1mg, PharmEasy, and Medplus, are expected to expand market presence by offering comprehensive, digitally enabled solutions.

Regional Insights

North America Nasal Antiseptic Market Trends

North America is expected to dominate the global market, accounting for approximately 40% of the total share, supported by high procedural intensity and institutional healthcare maturity. The U.S. anchors regional leadership through high surgical volumes and a stringent regulatory environment enforced by the FDA, which actively shapes compliance-driven adoption. Healthcare systems across the region align closely with the Agency for Healthcare Research and Quality guidelines, reinforcing standardized surgical safety practices. This regulatory discipline, combined with advanced hospital infrastructure, positions North America ahead of Europe and Asia Pacific in market maturity and risk-managed deployment.

The region is likely to remain a mature yet evolving market as investment priorities shift toward innovation-led infection control strategies. Pharmaceutical and medical technology R&D hubs across the U.S. drive sustained demand, particularly for non-antibiotic solutions addressing antimicrobial resistance and superbug exposure. Public and private stakeholders actively support next-generation infection prevention technologies, balancing patient safety, litigation risk, and reimbursement efficiency.

Europe Nasal Antiseptic Market Trends

Market growth in Europe is supported by harmonized EMA regulations that enable compliant product introductions in Germany and the U.K., while France and Spain exhibit growth driven by high allergy prevalence. The region benefits from structured healthcare systems and regulatory alignment through the Medical Device Regulation, which enforces safety standards while moderating new entry speed. Rising surgical volumes, particularly in orthopedics and cardiovascular care, drive the adoption of pre-surgical antiseptics, reinforcing Europe’s measured yet steady market expansion relative to other mature regions.

The region is likely to remain mature yet evolving as healthcare providers increasingly implement standardized safety protocols and infection prevention strategies. Investment in hospital infrastructure, aligned with regulatory oversight and public health initiatives, supports the adoption of preservative-free and natural formulations. These structural and regulatory factors are expected to sustain Europe’s strategic positioning, balancing compliance-driven constraints with incremental penetration across mature and emerging national markets.

Asia Pacific Antiseptic Market Trends

Asia-Pacific is expected to be the fastest-growing region due to the rapid expansion of hospital infrastructure and increased healthcare accessibility. The region benefits from high population density, increasing urbanization, and government initiatives to reduce hospital-acquired infections, collectively driving the adoption of pre-surgical antiseptics. The growing awareness of hygiene following the COVID-19 pandemic has reinforced demand across public and private healthcare facilities. Structural factors such as expanding medical tourism, improving regulatory frameworks, and investments in standardized infection control protocols are expected to sustain market acceleration, positioning Asia Pacific ahead of mature regions in growth potential.

The region is likely to remain highly dynamic, as countries such as China continue to expand hospital infrastructure and strengthen public health initiatives. Rising disposable incomes and healthcare expenditure increase patient access to preventive care solutions, while local manufacturing advantages for generic antiseptic formulations reduce supply constraints and improve distribution efficiency. These structural and policy-oriented drivers are expected to maintain Asia Pacific’s leadership in market growth, supporting deeper penetration in both urban centers and emerging Tier-2 cities, and enabling long-term adoption of standardized infection prevention practices.

Competitive Landscape

The global nasal antiseptic market is moderately consolidated, with the top five players GSK, Novartis, Johnson & Johnson, 3M, and Pfizer holding approximately 45-50% of the total market share. Hospital-grade products are dominated by a few multinational corporations, leveraging established relationships with healthcare organizations and group purchasing agreements to maintain a strong foothold. In contrast, the OTC and retail segments remain fragmented, with regional manufacturers and startups introducing innovative spray formulations. Competitive positioning emphasizes clinical efficacy, regulatory approvals, and comprehensive infection control portfolios, with differentiation achieved through advanced product features rather than standalone offerings.

Market concentration is higher in North America and Europe, whereas Asia exhibits greater fragmentation, as local players target niche hygiene and antiviral applications. SaNOtize launched its NOWONDER nitric oxide spray in the U.S., enhancing OTC hygiene offerings with viral neutralization technology. Paratek acquired Optinose, integrating XHANCE for the treatment of chronic rhinosinusitis and nasal polyps, thereby creating synergies. Marinomed sold its Carragelose antiviral portfolio to Unither, validating bio-antiviral formulations and expanding product pipelines. These moves highlight a strategic focus on innovation, portfolio expansion, and regional market penetration, particularly in retail and specialty hospital applications.

Key Industry Developments

- In August 2025, Firebrick Pharma secured European patent protection for Nasodine’s use in reducing SARS-CoV-2 viral load and for prophylactic applications. This safeguarded its intellectual property, facilitated entry into the EU market, and strengthened its competitive position against viral threats, with potential for post-COVID applications.

- In June 2025, Firebrick Pharma published peer-reviewed results in Frontiers in Medicine, demonstrating Nasodine’s efficacy against common cold viruses. This built scientific credibility, paved the way for expanded indications and marketing claims, and helped grow consumer trust and market share.

- In May 2025, Mölnlycke Health Care partnered with Ondine Biomedical to distribute Steriwave across the U.K., the EU, and the Middle East, beginning in Q4 2024 in the U.K. The partnership leveraged Mölnlycke’s network to provide broader access to innovative decolonization technologies and to support global efforts to reduce HAIs and promote antibiotic stewardship.

Companies Covered in Nasal Antiseptic Market

- 3M Company

- GlaxoSmithKline plc

- Novartis AG

- Johnson & Johnson

- Pfizer Inc.

- Cipla Limited

- Becton, Dickinson and Company

- Merck & Co.

- Reckitt Benckiser Group

- AstraZeneca

- Global Life Technologies

- PDI Healthcare

- Glenmark Pharmaceuticals

- Haleon plc

- SaNOtize Research & Development Corp.

- Firebrick Pharma

- Viatris Inc.

Frequently Asked Questions

The global nasal antiseptic market is projected to be valued at US$0.9 billion in 2026 and is forecast to reach US$1.5 billion by 2033, driven by the critical need to reduce surgical site infections and the rising adoption of preventive nasal hygiene protocols.

Growth is primarily driven by heightened awareness of respiratory virus prophylaxis post-pandemic, the widespread implementation of preoperative decolonization protocols in hospitals to combat antimicrobial resistance (AMR), and increasing consumer adoption of nasal sprays as routine preventive health measures.

The nasal antiseptic market is expected to grow at a CAGR of 7.4% between 2026 and 2033, reflecting sustained demand from both clinical and consumer health segments.

The Asia Pacific region is the fastest-growing market, fueled by expanding hospital infrastructure, rising healthcare accessibility, government initiatives to reduce hospital-acquired infections, and increased post-pandemic hygiene awareness.

Key players include GSK, Novartis, Johnson & Johnson, 3M, Pfizer, Cipla, Becton, Dickinson and Company, Haleon, SaNOtize, and Firebrick Pharma.