- Pharmaceuticals

- Nasal Allergy Treatment Market

Nasal Allergy Treatment Market Size, Share and Growth Forecast, 2026 - 2033

Nasal Allergy Treatment Market by Treatment (Immunotherapy, Others), Disease (Seasonal Allergic Rhinitis, Others), Route of Administration (Oral, Nasal, Intraocular, Intravenous), and Regional Analysis for 2026 - 2033

Nasal Allergy Treatment Market Share and Trends Analysis

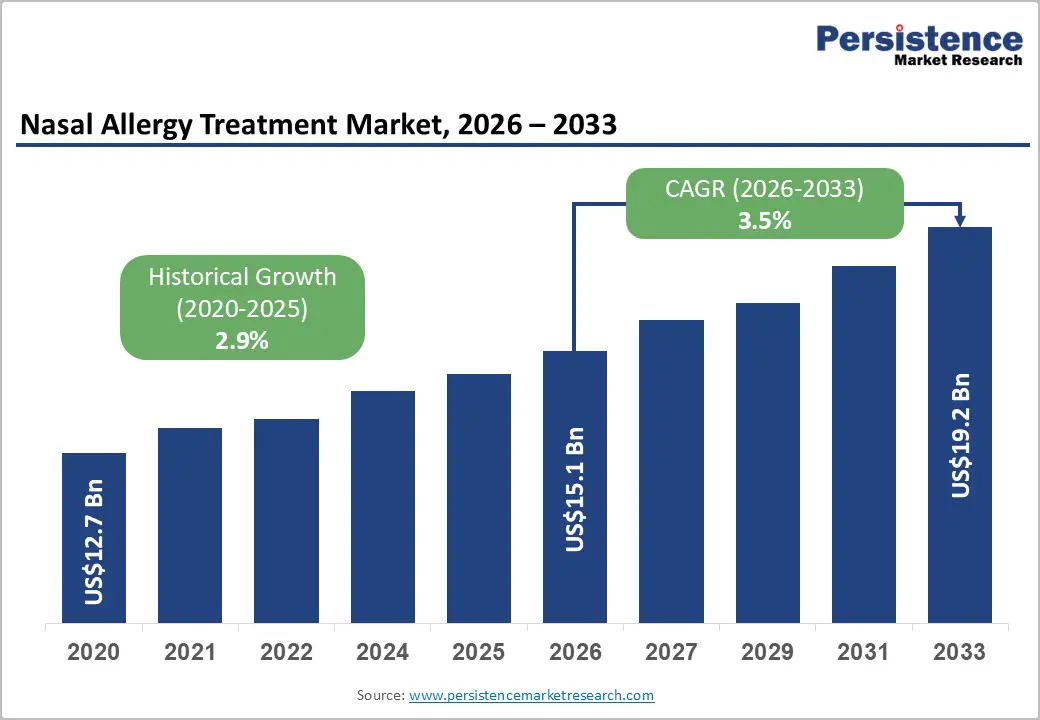

The global nasal allergy treatment market size is likely to be valued at US$ 15.1 billion in 2026 and is projected to reach US$ 19.2 billion by 2033, growing at a CAGR of 3.5% during the forecast period from 2026 to 2033, driven by the rising prevalence of allergic rhinitis affecting nearly 400 million people globally, increasing urban pollution exposure, and higher diagnosis rates supported by updated ARIA (Allergic Rhinitis and its Impact on Asthma) guidelines.

Growth is further reinforced by improved access to over-the-counter therapies and combination drug regimens. Demand is also rising due to seasonal variability and occupational allergen exposure in industrialized economies.

Key Industry Highlights:

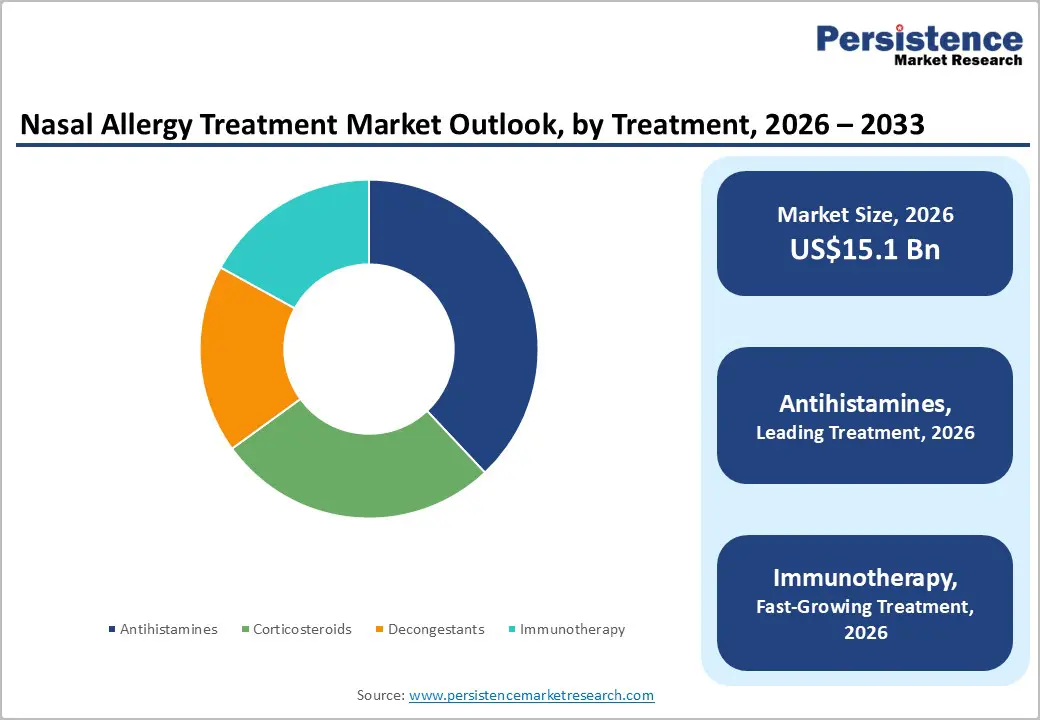

- Dominant Treatment Segment: Antihistamines are expected to lead the nasal allergy treatment market with 38% share in 2026, while immunotherapy is projected to be the fastest growing at 3.8% CAGR through 2033, supported by disease-modifying benefits and rising EAACI guideline adoption.

- Leading Disease Type: Seasonal allergic rhinitis is likely to dominate with 44% share in 2026, while occupational allergic rhinitis is expected to grow fastest at 3.6% CAGR through 2033, driven by rising workplace allergen exposure and improved occupational health reporting.

- Dominant Route of Administration: Oral route is expected to lead with 52% share in 2026, while nasal route is projected to be the fastest growing at 4.1% CAGR through 2033, driven by targeted delivery and improved corticosteroid nasal sprays.

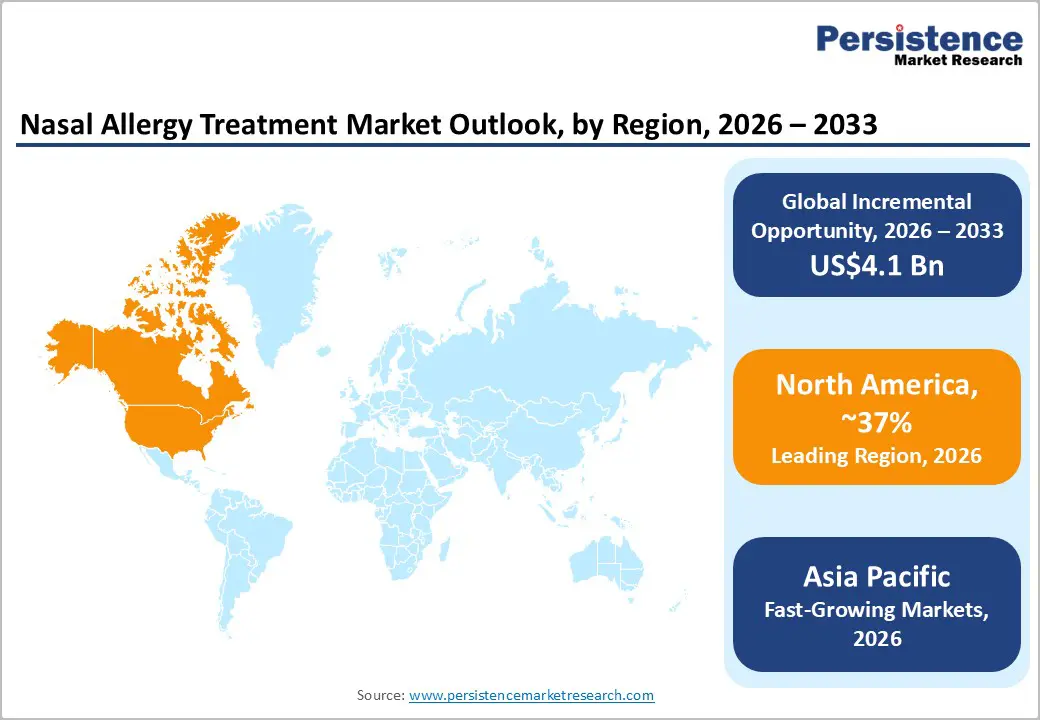

- Regional Leadership: North America is set to dominate with 37% share in 2026, while Asia Pacific is expected to grow fastest at 4.2% CAGR through 2033, driven by pollution, urbanization, and expanding healthcare access.

- Competitive Environment: Market competition is moderately fragmented, with growth driven by OTC antihistamines, nasal spray innovation, immunotherapy expansion, and rising focus on AI-enabled diagnostics and precision allergy treatment.

DRO Analysis

Driver - Rising Global Prevalence of Allergic Rhinitis and Environmental Triggers

The strongest driver of the allergic rhinitis treatment market is the rising prevalence of allergic disorders driven by pollution, climate change, and urbanization. According to the World Health Organization (WHO), allergic rhinitis affects 10-30% of the global population, with increasing incidence in urban regions due to PM2.5 exposure exceeding WHO air quality limits.

Industrial emissions and vehicle pollution in Asia and Europe have intensified allergen sensitivity. This has increased outpatient visits for nasal allergy treatments by over 20-25% in major healthcare systems. The market impact is significant as demand rises for antihistamines, corticosteroids, and immunotherapy solutions, particularly in densely populated regions, driving sustained pharmaceutical consumption and prescription growth globally.

Restraint - High Treatment Non-Adherence and Side Effects Limiting Long-Term Use

A key restraint in the nasal allergy treatment market is poor patient adherence due to chronic therapy requirements and side effects associated with long-term drug usage. Studies from the U.S. Centers for Disease Control and Prevention (CDC) and European respiratory health surveys show that nearly 40-50% of allergic rhinitis patients discontinue prescribed corticosteroids or antihistamines within six months.

Sedation, nasal irritation, and reduced perceived efficacy contribute to treatment drop-offs. Additionally, immunotherapy requires long-term administration cycles spanning 3-5 years, limiting patient compliance. This reduces sustained pharmaceutical revenue potential and increases relapse rates, leading to a higher healthcare burden. The restraint impacts market growth by slowing conversion from symptomatic treatment to long-term disease management solutions.

Opportunity - Expansion of Immunotherapy and Personalized Allergy Treatment Solutions

A major opportunity in the nasal allergy treatment market lies in the expansion of allergen-specific immunotherapy (AIT) and precision medicine approaches. Immunotherapy is emerging as a rapidly growing segment, with increasing clinical adoption across Europe and North America. The European Academy of Allergy and Clinical Immunology (EAACI) recognizes AIT as the only disease-modifying treatment for allergic rhinitis. Growth is being driven by sublingual and injectable formulations, supported by stronger guideline integration and physician preference for long-term disease control.

Advances in biomarker-based allergy profiling and digital diagnostics are enabling more accurate patient stratification and personalized treatment pathways. This is accelerating the shift from symptomatic relief to targeted immunological intervention, improving treatment durability and reducing recurrence frequency across seasonal and perennial allergic rhinitis populations.

Category-wise Analysis

Treatment Insights

Antihistamines are expected to dominate the nasal allergy treatment market, accounting for around 38% share in 2026, supported by rapid symptom relief, strong OTC availability, and their continued positioning as first-line therapy. Second-generation formulations with lower sedation profiles are likely to improve patient compliance, sustaining steady prescription and retail demand. Seasonal allergy peaks and expanding OTC approvals in major markets such as the U.S. and Europe are expected to further reinforce their leadership.

Immunotherapy is projected to be the fastest-growing segment at a 3.8% CAGR through 2033, driven by its disease-modifying potential compared to conventional symptomatic treatments. Increasing clinical endorsement under EAACI guidelines and rising adoption of sublingual immunotherapy (SLIT) in North America and Europe are expected to accelerate uptake. Improvements in allergen standardization and simplified dosing formats are likely to enhance adherence. Expansion of allergy specialty clinics and precision medicine programs is expected to further support long-term integration.

Disease Insights

Seasonal allergic rhinitis is expected to lead the segment with around 44% share in 2026, driven by predictable pollen exposure cycles and high prevalence across temperate regions. Recurring seasonal triggers are expected to sustain consistent demand for antihistamines and nasal sprays during peak allergy periods. Rising pollen intensity linked to climate variability and improving diagnostic rates in developed regions are likely to further support market growth.

Occupational allergic rhinitis is expected to be the fastest-growing segment at a 3.6% CAGR through 2033, driven by increasing exposure to industrial and chemical allergens. Strengthening regulatory oversight under OSHA and EU occupational safety frameworks is expected to improve detection and reporting rates. Expanding workplace screening programs in the manufacturing and healthcare sectors is likely to support early diagnosis. Increasing adoption of occupational health monitoring systems is expected to further drive treatment uptake.

Route of Administration Insights

The oral route is expected to dominate the market with around 52% share in 2026, supported by ease of administration, high patient compliance, and widespread availability of antihistamines and decongestants. Oral therapies are expected to remain first-line treatment across global clinical guidelines due to strong OTC penetration and accessibility. Expanding self-care adoption and pharmacy distribution channels are likely to further reinforce segment leadership.

The nasal route is projected to be the fastest-growing segment at a 4.1% CAGR through 2033, driven by targeted drug delivery and faster onset of symptom relief. Corticosteroid nasal sprays are expected to gain wider clinical preference for localized inflammation control. Advancements in metered-dose delivery systems and combination therapies are likely to improve precision and outcomes. Increasing physician preference for localized treatment approaches is expected to further accelerate adoption globally.

Regional Analysis

North America Nasal Allergy Treatment Market Trends

North America is projected to remain the dominant region in the nasal allergy treatment market with 37% share in 2026, underpinned by a high burden of allergic rhinitis, advanced care delivery systems, and strong consumer reliance on OTC antihistamines and nasal sprays. Increasing exposure to urban pollutants and longer allergy seasons are sustaining treatment demand. The presence of a strong U.S. FDA-led regulatory ecosystem is also accelerating approvals for next-generation therapies, including combination nasal formulations and biologics, reinforcing continuous product innovation.

U.S. Nasal Allergy Treatment Market Trends

The U.S. is expected to contribute 72% of regional demand in 2026, driven by widespread allergy prevalence, strong insurance coverage, and high self-medication behavior. Growth is further supported by a mature pharmaceutical innovation base and rapid integration of digital healthcare platforms. Recent momentum includes the expansion of virtual allergy clinics and the growing use of AI-supported diagnostic tools that help refine treatment selection and improve patient monitoring.

Canada Nasal Allergy Treatment Market Trends

Canada is likely to account for 38% of the regional market in 2026, supported by universal healthcare access and increasing awareness of environmental and seasonal allergies. Rising pollen variability across provinces such as Ontario and British Columbia is contributing to higher diagnosis rates. Recent developments include broader pharmacist-led prescribing models and the gradual adoption of intranasal steroid therapies as first-line care in primary settings.

Europe Nasal Allergy Treatment Market Trends

Europe is estimated to hold 28% share of the global nasal allergy treatment market in 2026, supported by strong clinical awareness, standardized treatment pathways, and well-established public healthcare systems. The region benefits from structured regulatory oversight through EMA frameworks, while EAACI guidelines continue to shape early diagnosis and immunotherapy adoption. Shifting pollen patterns and increasing urban air pollution are gradually expanding the patient base, particularly in densely populated metropolitan areas.

Germany Nasal Allergy Treatment Market Trends

Germany is expected to capture 32% of the regional market in 2026, supported by a strong physician-led diagnosis culture and high acceptance of allergen immunotherapy. Insurance-backed healthcare access ensures sustained treatment adherence and early intervention. Recent developments include the scaling of sublingual immunotherapy programs and the expansion of specialized allergy diagnostic centers integrated into hospital networks, improving long-term disease management.

U.K. Nasal Allergy Treatment Market Trends

The U.K. is projected to hold 18% of the regional market, driven by high seasonal allergy burden and strong reliance on OTC antihistamines. NHS-backed primary care pathways continue to support early-stage treatment adoption. Recent trends include wider rollout of digital prescribing platforms and increasing preference for fixed-dose combination nasal sprays, improving treatment convenience and patient compliance.

Asia Pacific Nasal Allergy Treatment Market Trends

Asia Pacific is expected to emerge as the fastest-expanding region, holding 25% share of the global nasal allergy treatment market in 2026, supported by rapid urbanization, worsening air quality, and rising awareness of respiratory allergies. The region is also benefiting from expanding pharmaceutical manufacturing capacity, strong generic drug ecosystems, and government-led air pollution control initiatives that are improving diagnosis rates and treatment penetration across both urban and semi-urban populations.

China Nasal Allergy Treatment Market Trends

China is projected to account for 40% of the regional market in 2026, driven by high industrial pollution exposure and a steadily rising prevalence of allergic rhinitis in urban centers. Expanding healthcare infrastructure and improved medication accessibility are reinforcing demand. Recent developments include strengthened national respiratory surveillance programs and rapid scaling of online pharmacy ecosystems, which are improving drug availability and patient reach beyond major cities.

India Nasal Allergy Treatment Market Trends

India is expected to contribute 18% of the regional market in 2026, supported by increasing urban pollution, growing awareness of allergy conditions, and expanding OTC drug penetration. Healthcare access is improving in tier-1 and tier-2 cities, enabling earlier diagnosis and treatment initiation. Recent developments include the rapid expansion of organized retail pharmacy chains and government-led respiratory health initiatives focused on early detection and broader public awareness.

Competitive Landscape

The global nasal allergy treatment market is moderately consolidated, with key players such as GlaxoSmithKline, Sanofi, Johnson & Johnson, Bayer, and AstraZeneca holding strong combined influence. These companies dominate through established OTC brands, wide distribution networks, and continuous innovation in antihistamines and corticosteroid nasal sprays. Their leadership is reinforced by strong physician trust and sustained R&D in fast-acting and non-drowsy formulations. Strong marketing capabilities and global reach further consolidate their market positions.

Specialty players such as ALK-Abelló and Stallergenes Greer are strengthening their presence through allergen immunotherapy and disease-modifying therapies. Entry barriers remain moderate to high due to regulatory requirements for prescription drugs and immunotherapy products in key markets. However, rising e-pharmacy adoption and telehealth integration are enabling improved access for smaller players. The market is expected to gradually consolidate further, supported by partnerships between pharmaceutical firms and digital health platforms.

Key Industry Developments:

- In February 2026, Dupixent was approved in the U.S. for allergic fungal rhinosinusitis (AFRS), expanding its role in nasal inflammation treatment. This strengthens its position as a leading biologic therapy for severe sinus and allergic airway diseases.

- In 2025, Stallergenes Greer expanded its allergen immunotherapy portfolio through acquisitions and broader vaccine offerings in North America. This reinforced its leadership in disease-modifying allergy treatments and strengthened its global immunotherapy presence.

Companies Covered in Nasal Allergy Treatment Market

- GlaxoSmithKline plc

- Sanofi S.A.

- Johnson & Johnson

- Bayer AG

- AstraZeneca plc

- Merck & Co., Inc.

- Pfizer Inc.

- Novartis AG

- Teva Pharmaceutical Industries

- Sun Pharmaceutical Industries

- Cipla Ltd.

- ALK-Abelló A/S

- Stallergenes Greer

- Roche Holding AG

Frequently Asked Questions

The global nasal allergy treatment market is projected to reach US$ 15.1 billion in 2026.

Rising allergic rhinitis prevalence, increasing pollution exposure, and growing OTC drug adoption drive the market.

The nasal allergy treatment market is expected to grow at a CAGR of 3.5% from 2026 to 2033.

Expansion of immunotherapy, precision medicine adoption, and digital allergy diagnostics create major growth opportunities.

GlaxoSmithKline, Sanofi, Johnson & Johnson, Bayer, AstraZeneca, and ALK-Abelló are key players in the market.