- Pharmaceuticals

- Esketamine Nasal Spray Market

Esketamine Nasal Spray Market Size, Share, and Growth Forecast, 2026 - 2033

Esketamine Nasal Spray Market by Indication Type (Treatment-Resistant Depression (TRD), Acute Suicidal Ideation, General Anaesthetics), Age Group (Pediatric, Adult, Geriatric), End-User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers (ASCs)), and Regional Analysis for 2026-2033

Esketamine Nasal Spray Market Share and Trends Analysis

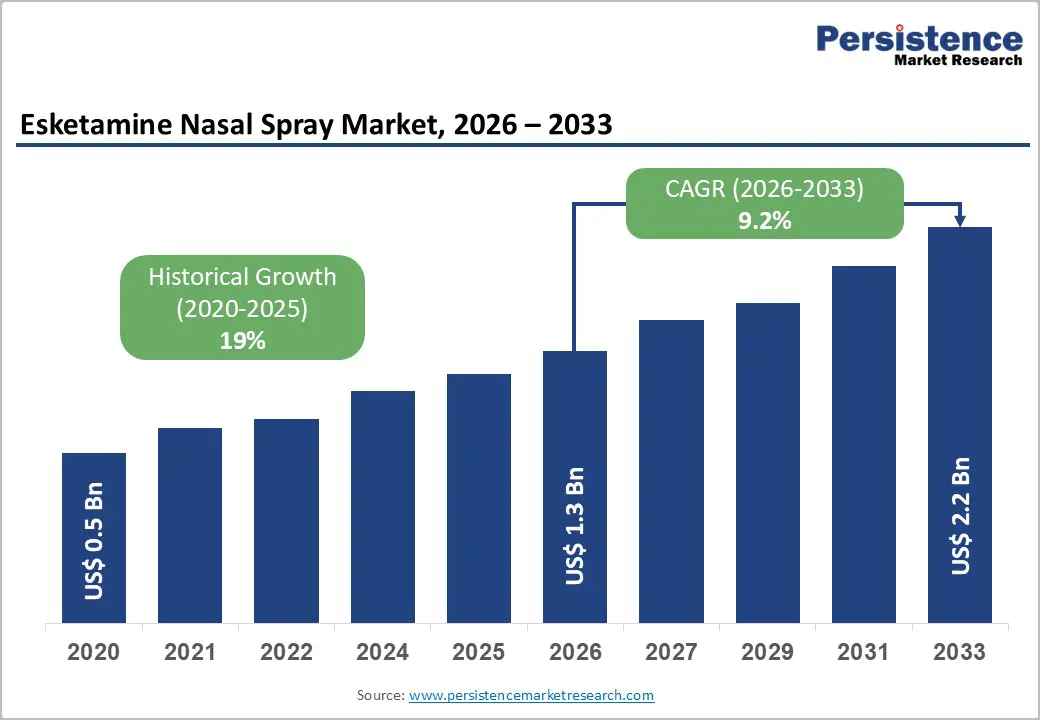

The global esketamine nasal spray market size is likely to be valued at US$ 1.3 billion in 2026, and is projected to reach US$ 2.2 billion by 2033, growing at a CAGR of 9.2% during the forecast period 2026−2033. Market growth is accelerating as healthcare systems are recognizing the rising burden of treatment-resistant depression (TRD), a severe subtype of major depressive disorder (MDD) that does not respond adequately to conventional pharmacological interventions. A growing proportion of adult patients is experiencing persistent depressive symptoms despite multiple treatment attempts, which is increasing the demand for innovative therapeutic modalities. Pharmaceutical manufacturers and healthcare providers are prioritizing advanced neuropsychiatric therapies, and regulatory agencies are continuing to support novel drug approvals that address high unmet clinical needs.

Esketamine nasal spray is gaining clinical acceptance as it provides rapid antidepressant effects through N-methyl-D-aspartate (NMDA) receptor modulation, which differs mechanistically from traditional selective serotonin reuptake inhibitors (SSRIs) and serotonin and norepinephrine reuptake inhibitors (SNRIs). Patients are experiencing symptom improvement within hours, while conventional antidepressants are typically requiring several weeks to achieve therapeutic outcomes. This rapid onset is improving patient adherence, reducing hospitalization risk, and enhancing overall treatment pathways, particularly in acute care settings such as psychiatric clinics and specialized mental health centers.

Key Industry Highlights

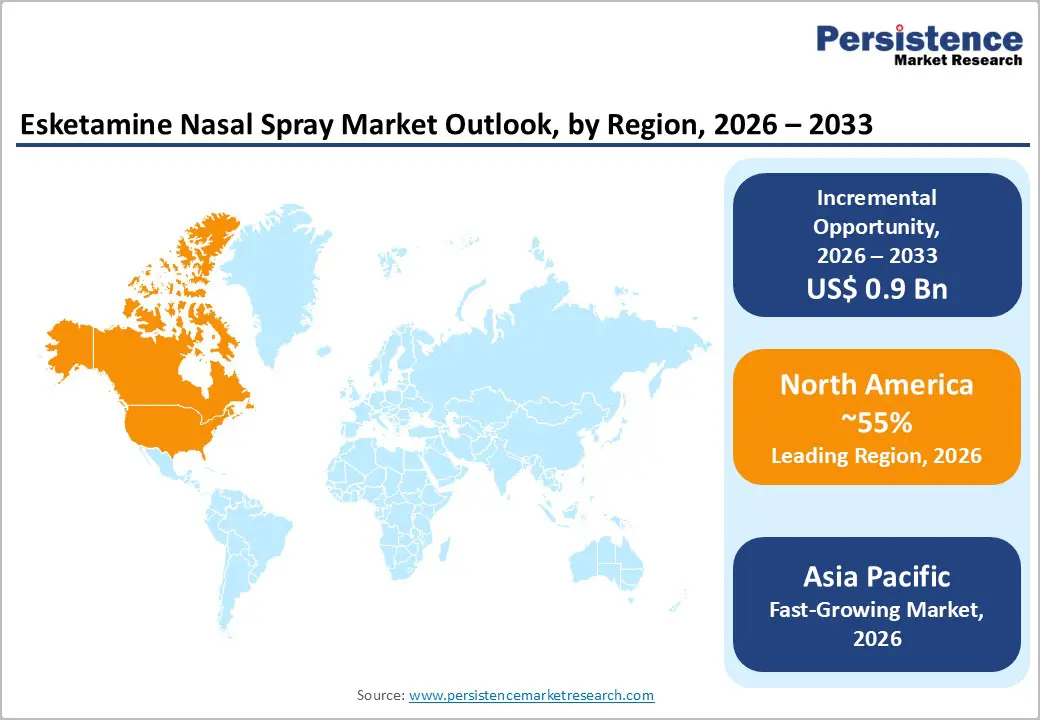

- Dominant Region: North America is expected to command about 55% market share in 2026, supported by regulatory approvals and a robust research & development (R&D) ecosystem.

- Fastest-growing Market: The Asia Pacific market is slated to be the fastest-growing during the 2026-2033 forecast period, due to widening awareness about mental health.

- Leading & Fastest-growing Indication Types: TRD is likely to command approximately 75% of total market revenue, while acute suicidal ideation is set to be the fastest-growing segment during the 2026-2033 forecast period.

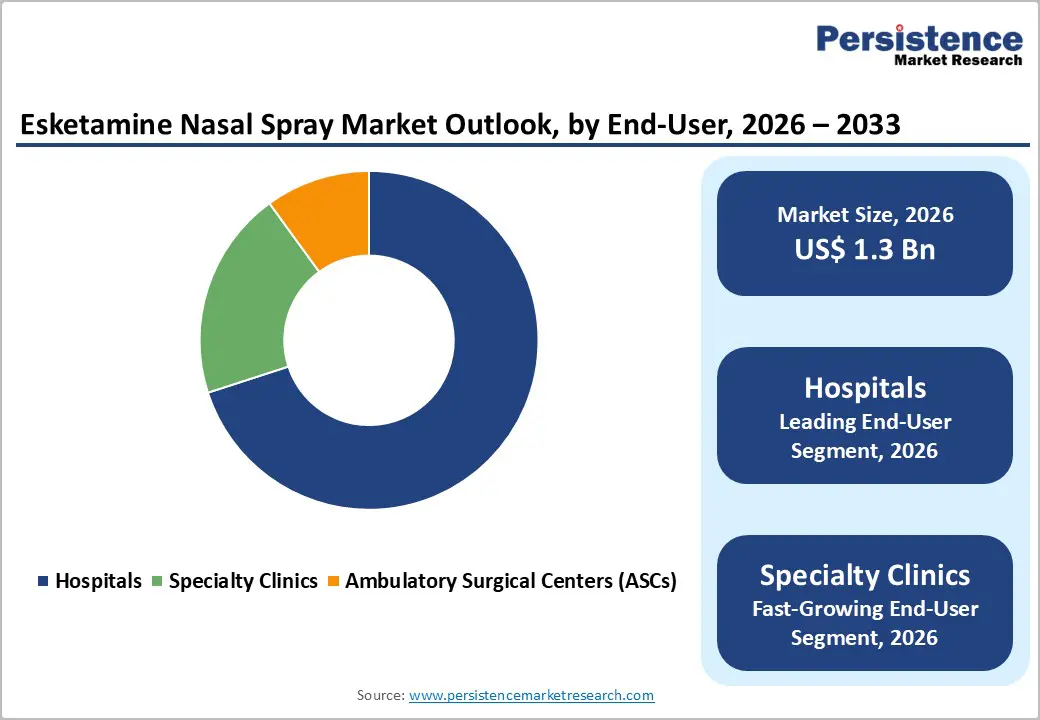

- Leading & Fastest-growing End-User: Hospitals are poised to lead with an approximate 70% market share in 2026, whereas specialty clinics are projected to be the fastest-growing segment through 2033.

| Key Insights | Details |

|---|---|

| Esketamine Nasal Spray Market Size (2026E) | US$ 1.3 Bn |

| Market Value Forecast (2033F) | US$ 2.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 19% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Treatment-Resistant Depression

The growing burden of TRD is driving market expansion as a central catalyst. Epidemiological evidence indicates that a substantial proportion of patients with MDD does not achieve adequate response after multiple antidepressant regimens, which is creating persistent clinical gaps. Healthcare providers are recognizing TRD as a complex psychiatric condition that conventional pharmacotherapies cannot sufficiently address, which is increasing the urgency for advanced interventions. This unmet need is strengthening demand for esketamine nasal spray, a therapy that is delivering rapid symptom relief compared with traditional antidepressants. The World Health Organization (WHO) identifies depression as the leading cause of disability worldwide, and prevalence rates are continuing to rise, which is reinforcing the importance of scalable and effective treatment solutions.

Patients and clinicians are increasingly adopting esketamine because it is addressing critical therapeutic limitations within mental health management. Conventional treatment pathways often require several weeks before measurable improvement occurs, whereas esketamine is producing faster clinical responses that are improving functional recovery and patient outcomes. The economic burden associated with TRD, including elevated healthcare expenditures, reduced workplace productivity, and long-term disability risks, is motivating healthcare systems to invest in more effective modalities. Pharmaceutical manufacturers are expanding accessibility through regulatory approvals, physician education programs, and awareness initiatives, which will have strengthened market penetration by the time emerging markets reach maturity. This transition is supporting improved depression management globally and is reinforcing sustained adoption of next-generation neuropsychiatric therapies.

Favorable Regulatory Approvals and Clinical Validation

Regulatory approvals from major health authorities are accelerating the penetration of esketamine nasal spray across global markets. For example, the U.S. Food and Drug Administration (FDA) has granted breakthrough therapy designation and approved esketamine under the brand formulation as a novel antidepressant with a differentiated mechanism of action. Other regulatory bodies, such as the European Medicines Agency (EMA), are also recognizing its role as a monotherapy option for treatment-resistant depression, which is eliminating the earlier requirement for combination use with oral antidepressants and simplifying treatment protocols. Clinical trial data are demonstrating significant improvements in standardized depression rating scales compared with placebo, reinforcing the therapy’s clinical credibility and supporting physician confidence.

Healthcare providers are increasing prescription adoption because regulatory validation is reducing uncertainty regarding safety, efficacy, and treatment positioning. Insurance providers and reimbursement agencies are expanding coverage decisions in response to these endorsements, which is improving patient affordability and access. Pharmaceutical companies are continuing to submit regulatory applications across emerging markets, and global authorities will have further aligned approval frameworks by the time the market reaches maturity. This regulatory progress is encouraging innovation in rapid-acting neuropsychiatric treatments and is strengthening stakeholder trust throughout the healthcare ecosystem.

High Treatment Costs and Limited Reimbursement

The high cost associated with esketamine therapy is creating a significant barrier to broader market adoption. The therapy is priced at premium levels per dose, and patients are receiving treatment under supervised conditions in certified healthcare facilities, which is increasing operational and administrative expenses. During the initial induction phase, healthcare providers are scheduling frequent treatment sessions, which is further elevating cumulative costs for patients and payers. Insurance reimbursement remains inconsistent across public and private coverage programs, which is limiting affordability and restricting access for economically vulnerable populations. Lower-income patient groups are facing the greatest constraints on account of substantial out-of-pocket expenses without financial assistance mechanisms.

Payers and regulatory authorities are scrutinizing pricing structures, which is intensifying discussions around healthcare equity and cost-effectiveness. Pharmaceutical companies are exploring value-based pricing frameworks, patient assistance programs, and alternative reimbursement agreements to address affordability concerns while maintaining innovation incentives. Patient advocacy organizations are advocating for expanded coverage policies to ensure equitable treatment access across socioeconomic groups. Companies need to introduce flexible payment models and strategic collaborations that may include partnerships with generic drug producers to reduce long-term costs. Governments are also implementing pricing oversight measures in response to public pressure, which is balancing innovation sustainability with accessibility goals. This evolving environment is supporting more inclusive mental healthcare delivery while enabling steady market development.

Strict Administration Requirements and Safety Concerns

Esketamine therapy operates under a Risk Evaluation and Mitigation Strategy (REMS) framework that imposes strict operational requirements and limiting scalability. The U.S. FDA mandates administration exclusively within certified healthcare settings, where providers are continuously monitoring patients for at least two hours following each dose. Clinical teams are actively managing risks such as sedation, dissociation, respiratory depression, and potential misuse, which is increasing procedural complexity and delivery costs. These restrictions are reducing accessibility in rural and underserved regions that lack certified facilities and trained personnel, which is slowing treatment expansion. Patients are also known to experience adverse effects such as nausea, dizziness, elevated blood pressure, and perceptual disturbances, which is influencing acceptance rates.

Clinicians are excluding individuals with contraindicated conditions such as aneurysmal vascular disease, arteriovenous malformations, or prior intracerebral hemorrhage to minimize safety risks. Esketamine is classified as a Schedule III controlled substance due to the historical recreational misuse associated with ketamine, which is prompting heightened concerns regarding diversion and dependency potential. Healthcare organizations are enforcing strict monitoring and documentation protocols, while pharmaceutical companies are investing in provider training initiatives and facility certification programs to reduce implementation barriers. Regulatory authorities are progressively refining guidance to balance patient safety with broader treatment access, and advocacy groups are encouraging eligibility expansion to reach more individuals with unmet clinical needs.

Expansion into Emerging Markets and Label Extensions

High-growth emerging economies are creating huge opportunities for market participants. Asia Pacific, for instance, is experiencing increasing mental health awareness alongside modernization of healthcare infrastructure, which is strengthening the environment for advanced neuropsychiatric therapies. China, India, and Japan are reporting rising depression prevalence while a growing middle-income population is gaining the financial capacity to access premium treatment options. Pharmaceutical companies are entering these markets through strategic local partnerships, regulatory submissions, and distribution agreements that are improving commercialization pathways. Governments are also investing in national mental health programs and public awareness campaigns, which are increasing diagnosis rates and generating higher treatment demand.

Clinical development initiatives are also diversifying therapeutic applications beyond TRD, which is expanding long-term revenue potential. Researchers are evaluating esketamine for indications such as MDD with acute suicidal ideation, chronic pain syndromes, and post-traumatic stress disorder (PTSD), broadening clinical relevance. The U.S. FDA is supporting label expansions for depressive symptoms in adults with urgent psychiatric needs, and each additional approval is enlarging the eligible patient population while strengthening commercial prospects. Pharmaceutical firms are collaborating with biotechnology partners to accelerate clinical trials and secure multinational regulatory endorsements, which will have enhanced market penetration across diverse care settings. This strategic evolution is driving patient volume growth and positioning esketamine as a versatile therapeutic platform that addresses complex mental health challenges globally.

Development of Alternative Delivery Systems and Combination Therapies

Ongoing innovation in drug delivery technologies and therapeutic formulations is creating strong growth pathways for esketamine-based treatments. Researchers are developing alternative modalities such as oral formulations, subcutaneous injections, and extended-release preparations that are aiming to improve pharmacokinetic stability and patient convenience. These advancements are expected to reduce dependence on REMS program requirements, thereby expanding accessibility to a broader patient population. Pharmaceutical companies are actively investigating injectable variants to simplify dosing procedures and optimize clinical workflows, while healthcare providers are recognizing the potential to minimize infrastructure constraints and accelerate treatment delivery timelines. Continuous investment in formulation science is enhancing bioavailability, tolerability, and adherence potential, which is strengthening competitive differentiation and long-term market positioning.

Therapeutic integration strategies are further expanding clinical utility through combination approaches that pair esketamine with supportive interventions such as psychotherapy, neuromodulation technologies including transcranial magnetic stimulation (TMS), and emerging pharmacological agents. This multidisciplinary framework is improving treatment outcomes and increasing applicability across diverse mental health conditions. Companies are also collaborating with digital health platforms to enable remote patient monitoring, data analytics, and coordinated care management, which is enhancing treatment continuity and clinical oversight. Telemedicine infrastructure is supporting supervised treatment models in geographically remote areas, and regulatory authorities are encouraging these hybrid care approaches to balance safety requirements with equitable access.

Category-wise Analysis

Indication Type Insights

Treatment-resistant depression is anticipated to account for approximately 75% of the esketamine nasal spray market revenue share in 2026. This leadership position reflects the primary regulatory approval granted by the U.S. FDA and the large patient population that is requiring alternative therapeutic strategies after inadequate response to multiple antidepressant regimens. Physicians are increasingly prescribing esketamine because clinical evidence is demonstrating superior efficacy in individuals who have not achieved remission through conventional pharmacological approaches. The general anesthesia application, although historically associated with ketamine-based compounds, is representing a comparatively small share within the market due to formulation-specific administration constraints and limited procedural adoption.

Acute suicidal ideation is projected to be the fastest-growing segment from 2026 to 2033. The U.S. FDA approval granted in 2020 for depressive symptoms in adults with suicidal thoughts or behaviors is addressing a critical psychiatric emergency that requires immediate intervention. Esketamine is providing rapid symptom reduction within 24 hours, which is offering emergency departments and psychiatric crisis centers an effective therapeutic option during high-risk clinical scenarios. Market expansion within this segment is supported by increasing investments in mental health crisis response infrastructure, expanding clinical evidence in acute care environments, and rising awareness among emergency medicine specialists.

End-User Insights

Hospitals are set to lead with an estimated 70% of the esketamine nasal spray market share in 2026. The REMS framework mandates supervised administration within certified healthcare environments, which is concentrating treatment delivery across hospital-affiliated centers and specialized psychiatric units. These institutional settings are maintaining the infrastructure necessary for continuous patient monitoring, emergency intervention readiness, and multidisciplinary psychiatric coordination that supports safe esketamine administration. Large academic medical centers and integrated health systems are establishing dedicated treatment programs that are improving protocol standardization and patient access pathways. Hospital procurement frameworks and volume-based purchasing agreements with pharmaceutical manufacturers are further strengthening the dominance of this channel by optimizing supply consistency and cost management.

Specialty clinics are projected to be the fastest-growing end users through 2033, as they offer focused psychiatric expertise and operational efficiency. Purpose-built esketamine treatment centers, operated by psychiatric practice networks and mental health service providers, are delivering streamlined patient experiences through optimized scheduling, dedicated observation areas, and staff training centered specifically on therapy management. This care model is attracting patients who are seeking specialized treatment outside conventional hospital environments while maintaining clinical oversight standards. Ambulatory surgical centers (ASCs) are representing a smaller yet gradually expanding segment, particularly in cases where esketamine is integrated with complementary therapeutic procedures. Future development of alternative formulations such as oral preparations could significantly reshape distribution dynamics over time.

Regional Insights

North America Esketamine Nasal Spray Market Trends

North America is expected to hold approximately 55% of the esketamine nasal spray market value in 2026, supported by early regulatory approvals and highly developed clinical infrastructure. The U.S. is generating the majority of regional revenue through established mental health systems, certified treatment centers, and strong institutional adoption across academic hospitals and urban healthcare networks. Providers are concentrating specialized facilities within major metropolitan areas and research institutions, which is accelerating therapy uptake for TRD. High patient demand driven by the substantial prevalence of TRD is creating sustained clinical urgency, while favorable reimbursement decisions from commercial insurers and Medicare Part D (Part D) prescription drug plans are improving patient access despite premium pricing structures. Pharmaceutical companies are leveraging this mature healthcare ecosystem to expand treatment penetration and strengthen provider engagement initiatives.

Regional innovation capacity is further reinforcing market leadership through ongoing research into label expansions, therapeutic combinations, and next-generation formulations. The FDA is enabling the introduction of novel psychiatric therapies through expedited regulatory pathways, which is encouraging continued investment in neuroscience development programs. Strategic acquisitions and portfolio expansions are signaling strong industry confidence, while leading manufacturers are maintaining competitive positioning ahead of potential generic entry following patent expirations. This environment is positioning North America as a global reference point for commercialization strategies that balance therapeutic innovation with equitable mental healthcare delivery.

Europe Esketamine Nasal Spray Market Trends

Europe stands as the second-largest regional market for esketamine nasal spray, fueled by robust pharmaceutical infrastructure and comprehensive public healthcare systems. Germany, the U.K., France, Spain, and Italy exhibit distinct adoption patterns that reflect differences in reimbursement mechanisms, psychiatric care delivery models, and national health priorities. Healthcare providers are integrating advanced neuropsychiatric therapies into structured treatment pathways, which is supporting consistent clinical uptake across the region. Governments are prioritizing mental health through policy reforms, funding programs, and national awareness initiatives that are increasing diagnosis rates and encouraging the use of innovative interventions for TRD. This coordinated policy environment is strengthening long-term market sustainability while improving patient access to specialized therapies.

Germany is spearheading regional penetration due to well-integrated mental health services within its statutory health insurance framework and strong academic research collaboration that is facilitating clinical adoption. The U.K.’s National Health Service (NHS) is evaluating esketamine through health technology assessment processes and is granting targeted access for eligible TRD patients who meet defined clinical criteria. France and Spain are advancing utilization through national initiatives that are addressing the socioeconomic burden of depression and productivity losses associated with untreated psychiatric conditions. The EMA is harmonizing regulatory standards to support cross-border commercialization; however, individual member states are maintaining independent reimbursement policies, which is creating heterogeneous market conditions across the region. Investments are focusing on expanding certified treatment centers into secondary cities and integrating esketamine therapy within broader mental health strategies.

Asia Pacific Esketamine Nasal Spray Market Trends

Asia Pacific is projected to become the fastest-growing market for esketamine nasal spray, on the back of rising healthcare investments, expanding mental health awareness, and progressive infrastructure development. Japan, China, India, South Korea, and the ASEAN bloc are progressing at different stages of regulatory approval and commercialization readiness, which is creating diverse growth trajectories across the region. Japan is demonstrating the highest level of market maturity as the Pharmaceuticals and Medical Devices Agency (PMDA) has approved esketamine and national insurance systems are covering eligible patients. Governments are increasing healthcare expenditure and strengthening psychiatric care capacity, which is accelerating therapy adoption and improving treatment accessibility. Pharmaceutical companies are implementing localized market entry strategies that account for country-specific regulatory frameworks, reimbursement environments, and cultural considerations, while healthcare providers are adapting treatment protocols to align with regional clinical practices.

China is attracting strong commercial interest due to its large patient population and expanding middle-income demographic, although the National Medical Products Administration (NMPA) is still evaluating therapy submissions. India is gaining momentum through increasing public awareness of mental health conditions, rising healthcare spending, and the presence of medical tourism centers that are offering advanced psychiatric interventions. Regional manufacturing capabilities are improving production efficiency and reducing costs through local supply chains, which is enhancing affordability and availability. Companies are forming partnerships with regional distributors, investing in clinician education programs, and expanding certified treatment infrastructure to address these barriers, while regulatory authorities are gradually refining policies to improve equitable access across populations.

Competitive Landscape

The global esketamine nasal spray market structure is moderately concentrated, dominated by Johnson & Johnson, Pfizer, Merck, Eli Lilly, and AbbVie in terms of revenue share. This strong market positioning is reflecting early mover advantages that have resulted from pioneering regulatory approvals from the U.S. FDA, extensive clinical development investments, and comprehensive intellectual property protection supported by patent portfolios that are extending into the 2030s. Leading companies are leveraging established commercialization networks, physician engagement programs, and research collaborations to sustain competitive advantages and expand treatment adoption. The current competitive environment is remaining relatively consolidated because barriers to entry are high, particularly due to regulatory complexity, safety monitoring requirements, and specialized administration protocols.

However, the market landscape is expected to evolve gradually as new market entrants are preparing to challenge incumbent dominance. Generic pharmaceutical manufacturers are positioning for future participation following patent expirations, while alternative ketamine-based formulations offered through compounding pharmacies are creating indirect competitive pressure in certain regions. In parallel, pharmaceutical innovators are advancing next-generation rapid-acting antidepressants with novel mechanisms of action, which are aiming to capture segments of the treatment-resistant depression population. Strategic partnerships, acquisitions, and pipeline diversification initiatives are continuing to shape competitive dynamics, and companies will have intensified research investments to maintain differentiation by the time market maturity occurs.

Key Industry Developments

- In October 2025, a five-year real-world analysis of more than 1.48 million treatment sessions by Janssen Scientific Affairs LLC reported that esketamine nasal spray demonstrates a safety profile consistent with clinical trials and product labeling. Serious adverse events occurred in less than 0.2% of sessions and suicide rates remaining at or below expected levels for TRD populations.

- In September 2025, the U.S. FDA approved esketamine nasal spray (Spravato) as a monotherapy for adults with TRD, based on phase 4 trials showing rapid symptom improvement versus placebo as early as 24 hours and sustained benefits at 4 weeks.

- In May 2025, esketamine nasal spray (Spravato) was subsidized in Australia for eligible patients with TRD, significantly reducing out-of-pocket costs under the Pharmaceutical Benefits Scheme (PBS), although treatment still requires supervised clinical administration due to safety protocols.

Companies Covered in Esketamine Nasal Spray Market

- Johnson & Johnson

- Pfizer Inc.

- Merck & Co., Inc. (MSD)

- Eli Lilly and Company

- AbbVie Inc.

- Novartis International AG

- Otsuka Pharmaceutical Co., Ltd.

- Endo International plc

- Bausch Health Companies Inc.

- Biogen Inc.

- Sage Therapeutics, Inc.

- MedKoo Biosciences, Inc.

- H. Lundbeck A/S

- Intra-Cellular Therapies, Inc.

- Bristol Myers Squibb Company

Frequently Asked Questions

The global esketamine nasal spray market is projected to reach US$ 1.3 billion in 2026.

The market is driven by growing incidence of TRD, high demand for rapid-acting minimally invasive therapies, regulatory approvals, and increasing mental health awareness.

The market is poised to witness a CAGR of 9.2% from 2026 to 2033.

Major opportunities lie in expansion into new indications (for example, suicidality), telemedicine integration, prioritization of advanced neuropsychiatric therapies by pharmaceutical companies, and supportive regulations for novel drugs.

Johnson & Johnson, Pfizer Inc., Merck & Co., Inc., Eli Lilly and Company, and AbbVie Inc. are some of the key players in the market.