- Healthcare Services

- Meditation Management Apps Market

Meditation Management Apps Market Size, Share, and Growth Forecast 2026 - 2033

Meditation Management Apps Market by Platform (Android, iOS, Others), Application (Stress & Anxiety Management, Sleep Improvement, Mental Health Support, Focus & Productivity, Spiritual Wellness), Deployment (Cloud-based, On-premise), End-user (Individual Consumers, Corporate / Employee Wellness Programs, Healthcare & Wellness Providers), and Regional Analysis, 2026 - 2033

Meditation Management Apps Market Share and Trends Analysis

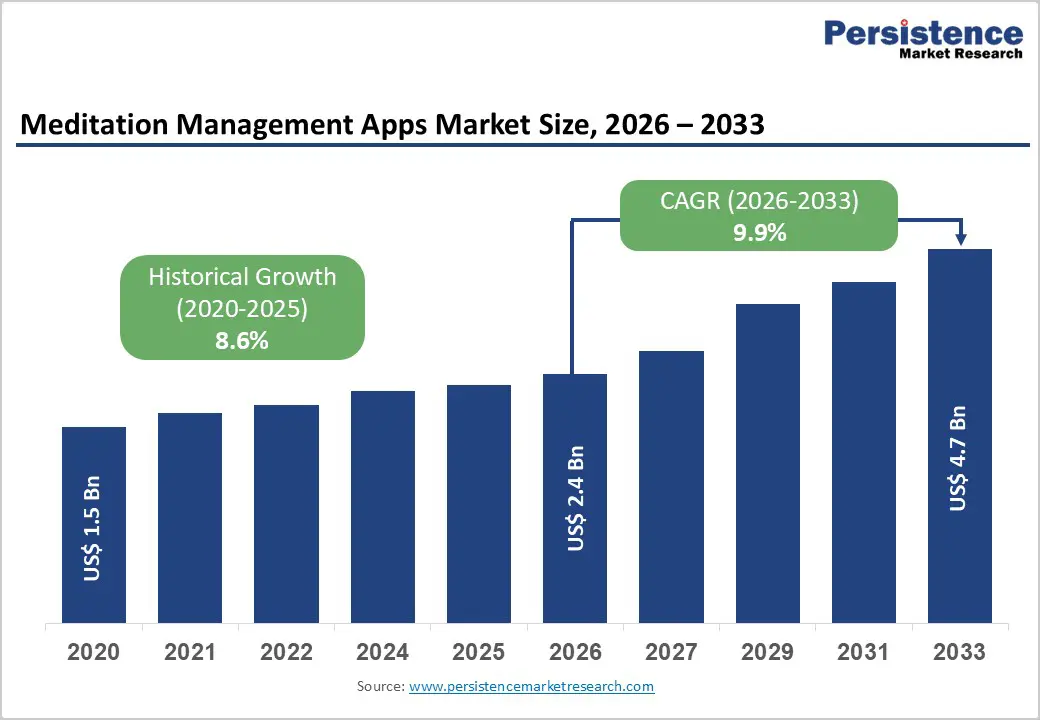

The global meditation management apps market size is expected to be valued at US$ 2.4 billion in 2026 and projected to reach US$ 4.7 billion by 2033, growing at a CAGR of 9.9% between 2026 and 2033.

This robust expansion reflects the convergence of rising mental health burdens, widespread smartphone adoption, and growing acceptance of app-based mindfulness as part of everyday self-care. As consumers, employers, and healthcare providers increasingly turn to digital tools for stress reduction, sleep support, and emotional resilience, meditation management apps have become a mainstream component of the broader digital mental health ecosystem. The market’s trajectory is further reinforced by continuous innovation in personalization, analytics, and integration with wearables and telehealth platforms.

Key Industry Highlights:

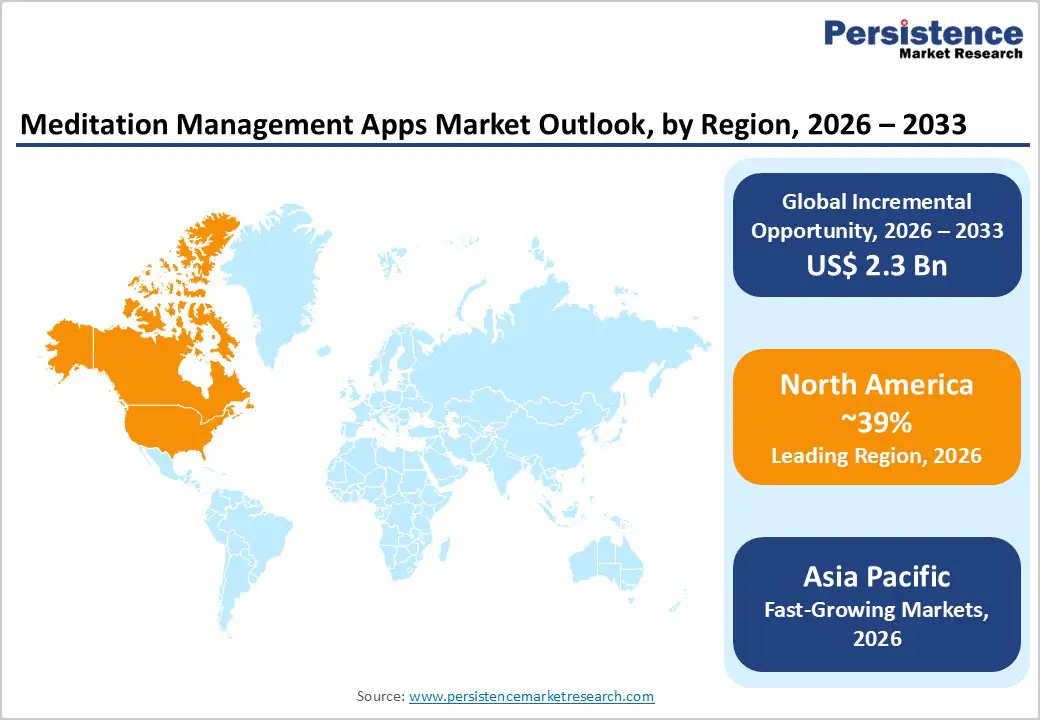

- Leading Region: North America is expected to remain the largest regional market for Meditation Management Apps through 2033, supported by high mental health awareness, strong consumer spending power, advanced digital health infrastructure, and expanding partnerships between meditation platforms, employers, and health insurers that embed app-based mindfulness into everyday care pathways.

- Fastest Growing Region: Asia Pacific is projected to register the fastest growth between 2026 and 2033, driven by rapid smartphone adoption, government-backed digital mental health initiatives in China, India, Japan, and Australia, and a young, urban population increasingly willing to use app-based tools for stress relief, meditation, and sleep support.

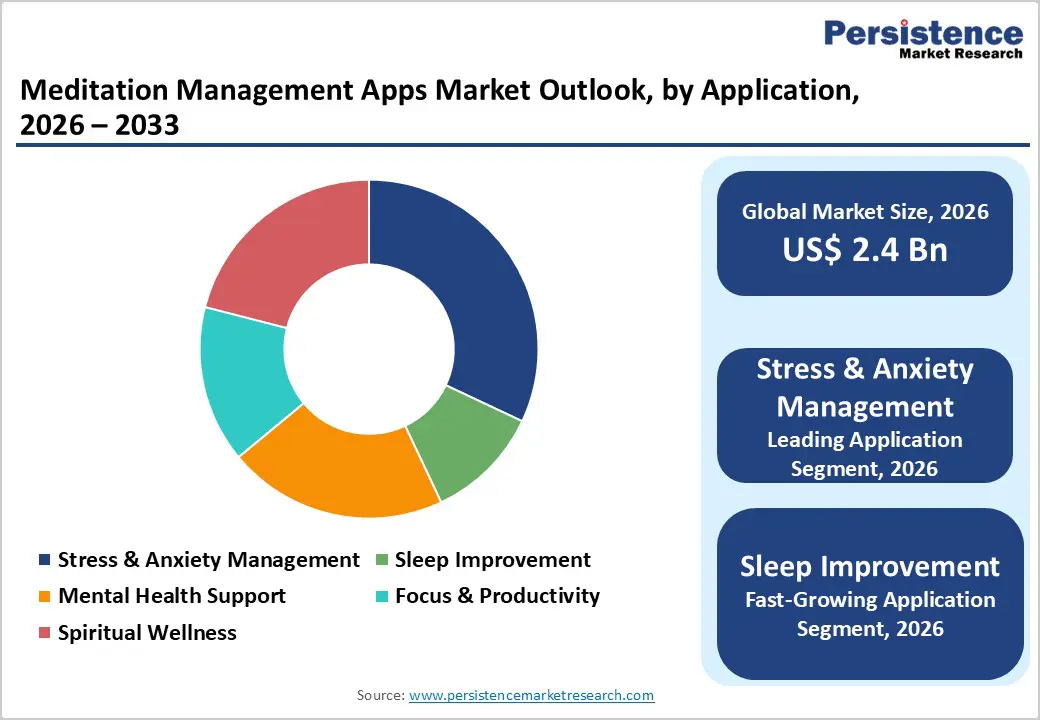

- Dominant Application: Within applications, stress & anxiety management growth is estimated at 32% share in 2025. It is expected to remain the dominant segment as individuals, employers, and educators prioritize accessible tools to cope with everyday stressors, workplace burnout, and elevated anxiety levels documented across major regions.

- Fastest Growing Application: Sleep improvement focused meditation content is anticipated to be among the fastest-growing segments, as a rising share of users seek digital solutions for insomnia and poor sleep quality; the popularity of sleep stories, soundscapes, and structured bedtime routines in leading apps is driving high engagement and premium subscription upgrades.

- Key Opportunity: A key opportunity lies in scaling cloud-based, enterprise-grade meditation platforms that integrate with corporate wellness programs, insurer networks, and telehealth services, enabling vendors to reach large covered populations, demonstrate measurable clinical and productivity benefits, and diversify revenue beyond direct-to-consumer subscriptions.

| Key Insights | Details |

|---|---|

| Meditation Management Apps Size (2026E) | US$ 2.4 billion |

| Market Value Forecast (2033F) | US$ 4.7 billion |

| Projected Growth CAGR (2026 - 2033) | 9.9% |

| Historical Market Growth (2020 - 2025) | 8.6% |

Market Dynamics

Drivers - Surging Smartphone Penetration and Normalization of Mindfulness Apps

Another major driver is the ubiquity of smartphones and the normalization of mindfulness and wellness apps as part of daily digital routines. Globally, there are more than 5 billion smartphone users, with recent mobile operating system statistics showing Android holding around 70-72% of smartphone OS market share and iOS about 27-30%, together accounting for over 99% of active smartphones. This enormous installed base has fueled rapid growth in downloads and engagement: in 2019, the top 10 meditation apps were downloaded roughly 52 million times, and Google search interest in mindfulness and meditation apps surged by more than 60% during the early pandemic period. Leading brands such as Calm and Headspace Health dominate the mindfulness category in app stores, with millions of paying subscribers and tens of millions of downloads. As users become accustomed to using smartphones for health tracking, fitness, and sleep, meditation apps integrate seamlessly into daily self-care habits, underpinning recurring subscription revenues and long-term market expansion.

Restraints - Evidence, Quality, and Engagement Gaps in Mental Health Apps

Despite strong growth, quality and engagement issues pose meaningful restraints for the Meditation Management Apps market. Academic reviews estimate that there are more than 10,000 mental health-related smartphone apps available, but only a small fraction are grounded in robust clinical evidence or developed with mental health professionals. In one detailed assessment of more than 350 mental health apps, only about 11% clearly cited scientific evidence, while over 15% lacked transparent data-sharing policies. Real-world usage patterns show high churn: studies suggest that fewer than 5-6% of users persist with mental health apps long enough to complete multi-week programs, even when initial downloads number in the tens of thousands. For meditation management app providers, such evidence and engagement gaps can erode user trust, limit clinical acceptance, and increase scrutiny from regulators and healthcare partners, ultimately tempering the pace at which apps are integrated into formal care pathways.

Regulatory, Privacy, and Reimbursement Barriers

Evolving but fragmented regulatory and reimbursement frameworks present another important restraint. Meditation apps that move beyond general wellness to offer targeted support for anxiety, depression, or sleep disorders increasingly intersect with digital health and medical device regulations. In the European Union, stringent data protection rules under GDPR and the medical device framework demand high standards of security, consent, and clinical validation. In the United Kingdom, the National Health Service (NHS) operates assessment processes for apps listed in its libraries, and only those meeting strict criteria are recommended. In the United States, policy analysis by organizations such as the Kaiser Family Foundation (KFF) highlights concerns around data privacy, algorithmic transparency, and how app-based services should be reimbursed by insurers and employer plans. Compliance with diverse national rules can increase development and operating costs, slow time-to-market, and discourage smaller innovators, constraining overall market expansion until clearer, harmonized frameworks emerge.

Opportunities - Expansion into Sleep, Holistic Wellness, and Multi-Modal Journeys

A significant opportunity lies in the rapid expansion of meditation apps into adjacent wellness domains such as sleep, emotional resilience, and holistic wellbeing. Sleep disruption has become a pervasive concern, with large-scale surveys reporting that around 30-40% of adults in many countries experience insomnia symptoms or poor sleep quality. Leading meditation platforms including Calm, Headspace Health, and Insight Timer have successfully incorporated sleep stories, soundscapes, and bedtime routines alongside breathing and mindfulness exercises, which has boosted user engagement and improved conversion to premium tiers. Industry analyses of meditation and mental wellness apps suggest that the broader category could surpass US$ 7 billion in value by the late 2020s, driven substantially by demand for sleep and holistic wellness content rather than meditation alone. Combined with emerging technologies such as virtual reality relaxation experiences forecast to generate several billion US$ in annual revenues across digital therapeutics and wellness providers that position meditation as the core of an integrated wellness journey can unlock higher lifetime value and cross-selling opportunities.

Corporate, Payer, and Healthcare Integration via Cloud-based Platforms

Another high-potential opportunity is deeper integration with enterprise buyers employers, health plans, and healthcare systems through scalable cloud-based platforms. Corporate wellbeing has become nearly universal in many large markets: workplace wellness research indicates that about 80-90% of mid-to-large employers in North America and Europe now operate structured wellness programs, with mental health and stress-management components present in around 60-75% of these offerings. Surveys by the American Psychological Association (APA) show that mindfulness and stress reduction initiatives can lower reported employee stress levels by approximately 25-30%, strengthen engagement, and reduce burnout.

Meditation app leaders are leveraging these trends: Headspace Health partners with thousands of employers and health plans worldwide, serving tens of millions of eligible members, while Calm has developed the Calm Business and Calm Health offerings tailored to enterprises and clinical partners. Cloud-native architectures enable secure, multi-tenant deployments, real-time analytics, integration with human resources systems, and alignment with telehealth and electronic health record workflows. Vendors that can demonstrate measurable improvements in absenteeism, productivity, and clinical outcomes stand to capture fast-growing, recurring revenue streams from corporate and healthcare clients.

Category-wise Analysis

Platform Insights

Platform choice is central to reach and monetization in the Meditation Management Apps market, with Android currently emerging as the leading platform segment by user base. Global mobile OS data show Android accounting for roughly 70-72% of smartphone market share, compared with about 27-30% for iOS, together representing more than 99% of active smartphones worldwide. This dominance translates into a broad installed base for Android meditation apps, particularly in cost-sensitive markets across Asia, Latin America, and Africa, where affordable Android handsets are available. As a result, the Android segment is estimated to command a share in the high-60% range of global meditation app users in 2025, making it the clear volume leader. At the same time, iOS is often viewed as the fastest-growing segment in terms of revenue per user, as iOS users typically show higher in-app spending and subscription uptake. This dynamic encourages leading vendors to optimize user experience and pricing for both ecosystems, but Android’s massive installed base ensures that it remains the anchor platform for scale.

Application Insights

By application, stress & anxiety management is the dominant segment, accounting for about 32% of the meditation management apps market in 2025. This leadership reflects the pervasive nature of stress and anxiety in modern life. The World Health Organization (WHO) estimates that anxiety disorders affect approximately 4-5% of the global population, while a significant share of adults report frequent stress related to work, finances, and family responsibilities. In several high-income countries, surveys show that nearly 50% of young adults feel anxious or stressed “most of the time” during the year.

Meditation apps directly address these needs with guided breathing exercises, body scans, mindfulness-based stress reduction modules, and cognitive reframing practices. Within app libraries, stress and anxiety programs frequently rank among the most searched and most completed courses. While Sleep Improvement is identified as the fastest-growing application segment as more users seek help for insomnia and circadian disruption, Stress & Anxiety Management is expected to remain the largest category due to the broad base of users struggling with everyday psychological stressors.

Deployment Insights

From a deployment standpoint, Cloud-based solutions clearly lead the Meditation Management Apps market and are also the fastest-growing model. Most consumer meditation apps rely on cloud infrastructures to deliver continuously updated content libraries, AI-driven personalization, and real-time performance tracking without requiring users to manage local installations. Reviews of digital mental health ecosystems highlight that the vast majority of the more than 10,000 mental health apps available globally depend on cloud-hosted back ends for scalability and security. On the enterprise side, corporate wellbeing and healthcare customers increasingly demand web dashboards, secure APIs, and integration with existing HR or clinical systems, all of which are more efficiently delivered via cloud. Workplace wellbeing analyses indicate that around 85-90% of organizations deploying wellness platforms now use cloud-hosted solutions. On-premise deployments remain limited to institutions with stringent data residency or internal control requirements, such as certain government agencies or highly regulated clinical environments, but their overall share is comparatively small.

Regional Insights

North America Meditation Management Apps Market Trends and Insights

North America is the leading regional market for meditation management apps, accounting for an estimated 39% share of global revenues in 2025. The region’s leadership reflects both high mental health need and a mature digital infrastructure. In the United States, opinion polls indicate that around 90% of adults view the country as being in a mental health crisis, and roughly one in five adults experience a mental health condition each year. At the same time, workforce surveys show significant burnout: close to 60% of employees report negative impacts of stress on their work, underpinning demand for scalable, app-based coping tools. High smartphone penetration, strong willingness to pay for digital services, and the presence of leading app developers create a favorable environment for premium meditation subscriptions and bundled wellness offerings.

Regulatory and innovation ecosystems in North America further support digital mental health adoption. Federal and state policies have expanded coverage for telehealth and remote behavioral health services, creating opportunities for meditation apps to integrate into hybrid care models. Major insurers and employers increasingly partner with platforms like Headspace Health and Calm to offer meditation, mindfulness, and sleep content as part of benefit packages, in some cases extending eligibility to millions of covered members. Venture investment and corporate partnerships continue to flow into mental health and wellness technologies, reinforcing North America’s role as a test bed for innovative content formats, AI-driven personalization, and outcome-based contracts.

Asia Pacific Meditation Management Apps Market Trends and Insights

Asia Pacific is the fastest-growing regional market for Meditation Management Apps, supported by large populations, rising mental health awareness, and rapid smartphone penetration. The region leads the world in mobile data consumption, with smartphone adoption rates exceeding 80% in markets such as China and South Korea and growing quickly in India and ASEAN countries. Android holds close to 80% smartphone OS share in many Asia Pacific markets, providing a vast base for affordable meditation and wellbeing apps targeted at younger, tech-savvy users. Mental health burden is substantial: studies from global health agencies estimate that hundreds of millions of people in Asia live with anxiety and depressive disorders, while economic analyses project cumulative productivity losses running into hundreds of billion US$ over multi-decade horizons if treatment gaps persist.

Governments and public health initiatives increasingly recognize digital mental health as part of the solution. The Australian Government Department of Health supports a nationally coordinated ecosystem of digital mental health services, including online programmes and apps for anxiety, depression, and wellbeing, guided by national safety and quality standards. In China, systematic reviews have identified hundreds of mobile mental health apps, many incorporating meditation, relaxation, and mindfulness elements as core techniques. India, Japan, and ASEAN countries are seeing a rapid rise in local startups offering meditation content in regional languages, often combining traditional practices with modern app design. Regional research points to double-digit compound annual growth in mental health app revenues across Asia Pacific as consumers adopt these culturally tailored, low-stigma tools. Together, these dynamics underline Asia Pacific’s status as the fastest-growing region for meditation management apps over 2026 - 2033.

Competitive Landscape

The meditation management apps market is highly competitive and fragmented, dominated by global players offering a wide range of guided meditations, sleep aids, and mental wellness features. Leading companies like Calm, Headspace, Insight Timer, and Simple Habit focus on user engagement, subscription models, and personalized content to retain customers. New entrants differentiate through niche offerings such as sleep improvement, focus enhancement, or spiritual wellness. Continuous innovation, strategic partnerships with healthcare providers, and expansion into corporate wellness programs are key strategies.

Key Developments:

- In October 2025, Cairns Health, a leading provider of digital health solutions for seniors and individuals with chronic conditions, acquired Together by Renee, an award-winning AI-powered healthcare app from SixD Inc. This strategic acquisition strengthened Cairns' commitment to simplifying healthcare through technology that empowered patients and their caregivers.

Companies Covered in Meditation Management Apps Market

- Calm, Headspace Health

- Insight Timer

- Simple Habit

- Breethe

- Aura Health

- Ten Percent Happier

- Meditopia

- Inner Explorer

- Meditation Moments

- Smiling Mind

- Meditation Studio

- MyLife Meditation

- Balance

- Sanvello

Frequently Asked Questions

The global Meditation Management Apps market is expected to reach around US$ 2.4 billion in 2026, driven by rising mental health awareness, expanding smartphone penetration, and increasing acceptance of app-based mindfulness, sleep, and stress-management solutions across key regions.

Key demand drivers include the growing global burden of anxiety and depression, limited access to traditional mental health services, and near-universal smartphone adoption. Consumers, employers, and healthcare providers are turning to meditation apps as convenient, low-stigma tools for managing stress, anxiety, and insomnia, while corporate wellness and digital health initiatives further accelerate adoption.

North America currently leads the global Meditation Management Apps market, contributing an estimated high-thirty-percent share of revenues, supported by strong consumer in-app spending, widespread corporate wellness programs, an advanced innovation ecosystem, and expanding partnerships between meditation app providers, employers, and health insurers.

One of the most attractive opportunity areas is the development of cloud-based, enterprise-ready meditation platforms integrated with corporate wellness, insurer networks, and telehealth services, enabling vendors to serve large populations, demonstrate tangible clinical and productivity gains, and diversify revenue beyond direct-to-consumer subscriptions.

Key players include Calm, Headspace Health, Insight Timer, Simple Habit, Breethe, Aura Health, Ten Percent Happier, Meditopia, Inner Explorer, Meditation Moments, Smiling Mind, Meditation Studio, MyLife Meditation, Balance, and Sanvello, alongside numerous regional and niche meditation app providers.