- Sporting Goods & Equipment

- Yoga and Meditation Products Market

Yoga and Meditation Products Market Size, Share, and Growth Forecast 2026 - 2033

Yoga and Meditation Products Market by Product Type (Clothing & Accessories, Yoga Mats & Props, Meditation Cushions & Benches, Weighted Blankets, Wearables, Devices, and Others), End-user (Individual Consumers/Households, Corporate and Educational Institutions, Fitness & Yoga Centers / Studios, Healthcare & Rehabilitation Centers, and Others), Distribution Channel (Online Channels and Offline Channels), and Regional Analysis 2026 - 2033

Yoga and Meditation Products Market Size and Share Analysis

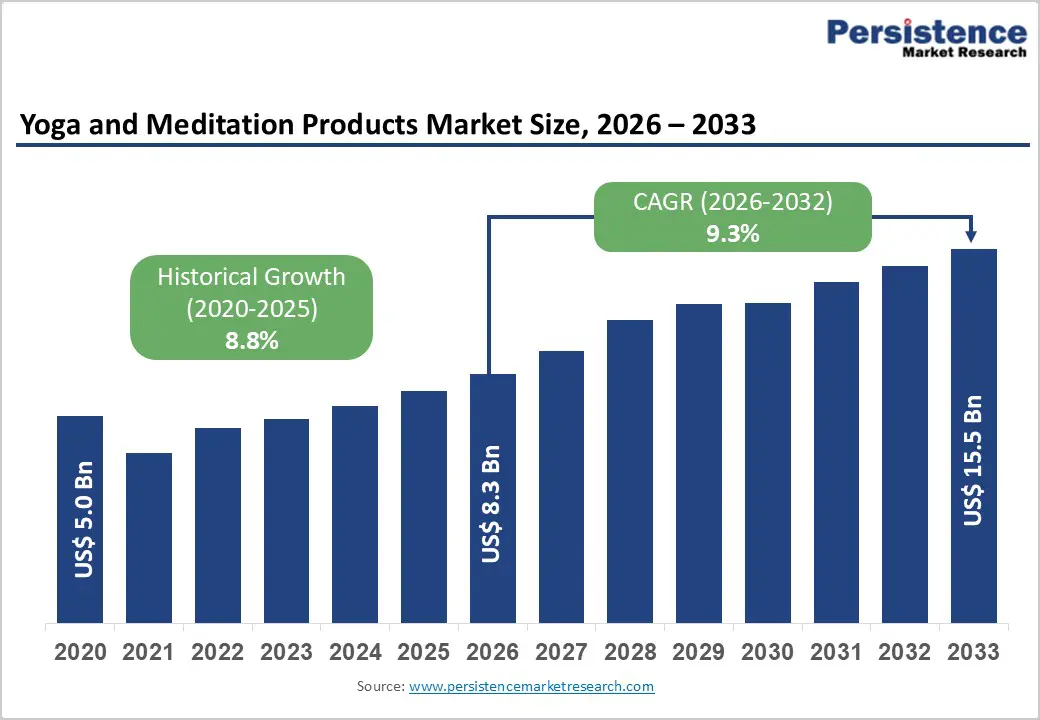

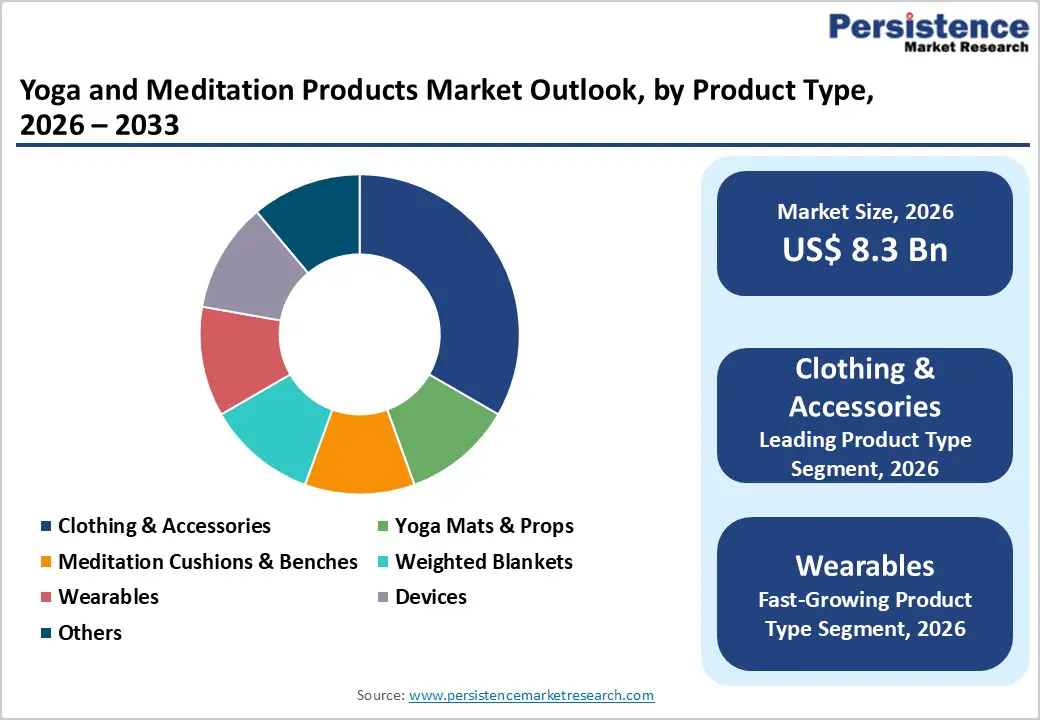

The global yoga meditation products market size is likely to be valued at US$ 8.3 billion in 2026 and is projected to reach US$ 15.5 billion by 2033, growing at a CAGR of 9.3% between 2026 and 2033.

The market is primarily driven by the surging prevalence of stress-related disorders, a global shift towards holistic preventive healthcare, and the rapid digitalization of fitness, exemplified by the proliferation of AI-enabled yoga apps and smart wearables. The World Health Organization reports that anxiety and depression increased by 25% globally in recent years, resulting in the adoption of yoga and meditation as accessible therapeutic interventions.

Key Industry Highlights:

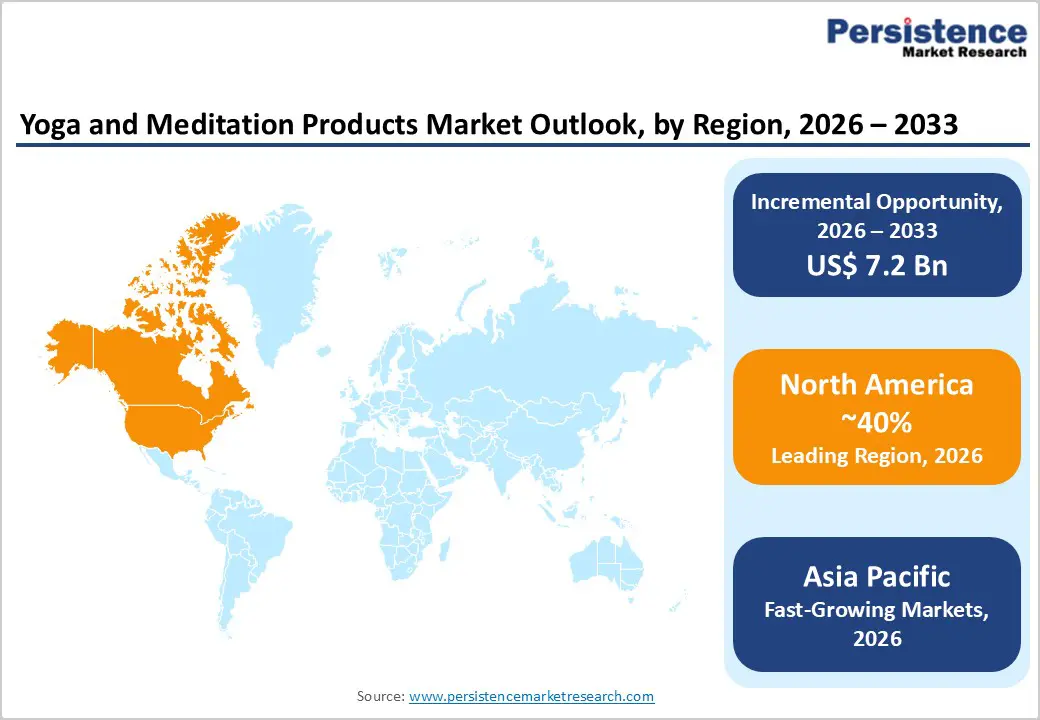

- Leading Region: North America commands the 40% revenue share, supported by high discretionary spending on wellness products, widespread adoption of premium athleisure, and a mature digital ecosystem that accelerates subscriptions and DTC sales.

- Fastest-Growing Region: Asia Pacific is the fastest-expanding regional market, with a 10.2% CAGR, driven by India's deep-rooted yoga heritage

- and rising luxury wellness consumption among urban consumers in China.

- Dominant Product Type: Clothing & Accessories remains the highest-revenue-generating Product Type, fueled by the global athleisure movement, which positions yoga wear as both functional fitness gear and everyday lifestyle fashion.

- Fastest Growing Distribution Channel: Online Channels are outpacing brick-and-mortar retail, driven by direct-to-consumer (DTC) brand strategies, wider product availability, and the seamless bundling of physical products with digital meditation and yoga subscriptions.

- Key Market Opportunity: The development of male-focused yoga products and programs represents a largely untapped, high-growth opportunity as men's participation rises and demand grows for performance- and recovery-oriented yoga solutions.

| Key Insights | Details |

|---|---|

|

Global Yoga and Meditation Products Market Size (2026E) |

US$ 8.3 Bn |

|

Market Value Forecast (2033F) |

US$ 15.5 Bn |

|

Projected Growth CAGR(2026-2033) |

9.3% |

|

Historical Market Growth (2020-2025) |

8.8% |

Market Dynamics

Drivers - Rising Integration of Yoga and Meditation into Corporate Wellness Programs

The increasing incorporation of yoga and meditation into corporate wellness programs has emerged as a major growth driver for the global yoga and meditation products market. Industry surveys indicate that over 80% of large employers in North America now offer formal wellness benefits, with mind–body practices ranking among the most frequently adopted interventions due to their low implementation cost and measurable impact on stress reduction, employee engagement, and productivity. According to workplace health studies, organizations implementing regular mindfulness or yoga initiatives report 20–30% reductions in employee stress levels and lower absenteeism rates, strengthening employer return on investment.

Large corporations are increasingly partnering with digital wellness platforms to scale these initiatives. For example, Cigna Healthcare has partnered with Headspace to provide guided meditation and mindfulness content to millions of employees globally. This institutional adoption drives bulk procurement of yoga accessories and meditation products, creating a stable B2B revenue stream for manufacturers and platform providers. More importantly, corporate endorsement normalizes yoga and meditation as daily productivity and mental health tools rather than niche lifestyle practices, significantly expanding the total addressable market beyond individual consumers to enterprises, co-working spaces, and wellness service providers.

Technological Advancements in Smart Yoga Accessories Driving Premiumization and Higher Per-User Spend

The integration of digital technology into traditional yoga and meditation practices is accelerating market growth through product innovation and premium pricing. The emergence of smart yoga mats, posture-sensing cushions, and connected meditation devices equipped with embedded sensors enables real-time feedback on alignment, balance, and breathing patterns. These products often connect to companion mobile applications, allowing users to track performance metrics such as session duration, posture accuracy, heart rate variability, and mindfulness minutes.

Innovations that integrate with wearables such as the Apple Watch and Fitbit further enhance user engagement by linking yoga and meditation sessions to broader health dashboards. This data-driven and gamified approach resonates strongly with millennial and Gen Z consumers, over 60% of whom actively use fitness or wellness tracking applications. As a result, consumers are increasingly willing to pay a premium for smart, connected yoga products that deliver measurable progress and personalized insights.

Restraints - Lack of Standardization and Quality Variability Undermines Consumer Trust and Repeat Purchases

The lack of industry-wide standards for yoga and meditation products is a notable market restraint, leading to significant variability in product quality, safety, and performance. Consumers frequently encounter inconsistencies in material durability, grip, cushioning, and ergonomic support across different brands and price points, particularly in online purchases where physical inspection is not possible. This variability can result in negative user experiences, especially for beginners, reducing trust in branded products and discouraging repeat purchases.

The influx of low-quality imports and counterfeit products further exacerbates this challenge by diluting brand credibility and confusing consumers. For institutional buyers such as yoga studios, wellness centers, and corporate programs, the lack of standardized quality benchmarks complicates procurement decisions and increases perceived risk. Consequently, this restraint can slow brand loyalty formation and limit long-term market value creation despite increasing participation in yoga and meditation practices.

Opportunity - Expansion into Healthcare and Rehabilitation Sectors Unlocks Access to Non-Discretionary Spending

The integration of yoga and meditation products into healthcare and rehabilitation ecosystems presents a high-value growth opportunity for market participants. A growing body of clinical evidence supports the effectiveness of yoga-based interventions in managing chronic conditions such as lower back pain, arthritis, cardiovascular disorders, anxiety, and post-surgical rehabilitation. As healthcare systems increasingly shift toward preventive and non-pharmacological therapies, yoga and meditation are gaining recognition as complementary treatment modalities rather than purely lifestyle practices.

Manufacturers and solution providers can collaborate with hospitals, rehabilitation centers, physiotherapy clinics, and insurance providers to position specific yoga props, therapeutic cushions, and guided programs as clinically validated therapeutic aids. Rehabilitation centers are already incorporating yoga therapy into structured recovery protocols for mobility restoration and pain management. The development of medically certified products, ergonomically designed for patients with limited mobility, or evidence-based digital therapeutics creates a pathway to tap into the significantly larger and more stable healthcare spending pool. This transition enables vendors to move beyond discretionary consumer wellness spending and into institutional, reimbursable healthcare budgets, supporting long-term revenue scalability.

Rising Acceptance of Yoga Among Men Creates an Untapped Opportunity for Male-Centric Product Innovation

The global yoga and meditation products market also presents a significant opportunity through deeper penetration of the male consumer segment, which has historically been underrepresented due to gender-biased marketing and cultural perceptions. This dynamic is rapidly changing as stigma surrounding male participation in yoga diminishes, driven by endorsements from professional athletes and trainers across high-performance sports leagues such as the NBA and NFL. Yoga is increasingly seen as a tool for strength, recovery, injury prevention, and mental resilience, rather than just flexibility.

Despite rising male participation, the market currently offers limited product differentiation tailored to men’s physiological needs. There is a clear gap in yoga apparel designed for male body structures, as well as mats and props engineered for larger frames, higher impact, and strength-focused practices. Companies that introduce male-specific product lines, supported by targeted messaging around functional fitness and athletic recovery, can capture a fast-growing and relatively underserved segment. Brands such as Alo Yoga have already begun increasing male representation in marketing campaigns, signaling a broader industry shift that other players can strategically leverage.

Category-wise Analysis

Product Type Insights

The Clothing & Accessories represents the largest share of the global yoga and meditation products market, accounting for approximately 45% of total revenue. This dominance is primarily driven by the continued rise of the athleisure trend, in which yoga apparel is worn not only during practice but also as everyday lifestyle clothing. Unlike yoga mats and accessories, which are durable goods with longer replacement cycles, apparel benefits from high purchase frequency, seasonal refreshes, and fashion-driven consumption.

Advancements in fabric technology, including moisture-wicking materials, compression support, four-way stretch, and sustainable inputs such as recycled polyester, further enhance consumer appeal and encourage repeat purchases. Yoga apparel increasingly serves a social signaling function, particularly within urban and digitally connected consumer segments. Premium positioning and strong brand identity from players such as Alo Yoga reinforce aspirational value, driving both volume and pricing power.

End-user Insights

The Individual Consumers / Households segment holds the largest share of the global yoga and meditation products market, accounting for an estimated 68% of total demand. This leadership is underpinned by the structural shift toward home-based fitness and wellness routines, a trend accelerated during the pandemic and sustained by the widespread adoption of hybrid and remote work models. For many practitioners, the home has become the primary venue for yoga and meditation practice.

Consumers are increasingly investing in personalized “home sanctuaries”, purchasing mats, blocks, bolsters, apparel, and complementary digital subscriptions to replicate studio-like experiences. While institutional adoption across corporate, healthcare, and educational settings is expanding, the sheer scale and frequency of individual purchases continue to anchor market revenues. High engagement levels are further supported by on-demand digital platforms such as Peloton, which maintain consistent household participation and reinforce repeat consumption of physical and digital yoga-related products.

Distribution Channel Insights

Online channels have emerged as the fastest-growing and increasingly dominant distribution channel in the global yoga and meditation products market, accounting for approximately 55% of total sales. The shift toward e-commerce is driven by the expansion of direct-to-consumer (DTC) strategies, which enable brands to achieve higher margins, maintain pricing control, and build deeper customer relationships through data-driven engagement.

The inherently digital nature of meditation apps, virtual classes, and hybrid product ecosystems further strengthens the role of online platforms. E-commerce channels also offer significantly broader product assortments, including niche and specialty items such as eco-friendly cork mats and sustainable accessories that may not be widely available through physical retail. Added benefits such as doorstep delivery, flexible return policies, and access to peer reviews enhance purchase confidence, making online platforms the preferred channel for modern, wellness-focused consumers.

Regional Insights

North America Yoga and Meditation Products Trends

North America continues to lead the global yoga and meditation products market with over 40% share in 2026, supported by high disposable incomes and a deeply embedded wellness-oriented lifestyle culture. The United States accounts for the majority of regional demand and serves as a global innovation hub, hosting the headquarters of major industry players such as Peloton and CorePower Yoga. Consumers in the region demonstrate strong willingness to pay for premium apparel, smart fitness devices, and subscription-based digital wellness services, reinforcing higher average revenue per user compared to other regions.

Innovation remains a defining trend, with a robust startup ecosystem focused on AI-driven mental health and meditation applications, personalized wellness analytics, and connected fitness ecosystems. The regulatory environment is increasingly supportive, with growing recognition of mental health parity in insurance coverage across the U.S. This evolving policy landscape indirectly boosts spending on meditation programs and mindfulness tools, strengthening both consumer and institutional demand. As a result, North America remains the most mature and monetized regional market.

Europe Yoga and Meditation Products Trends

Europe is experiencing steady and structurally driven growth, particularly across Germany, the United Kingdom, and France. Unlike the fashion- and trend-driven dynamics seen in North America, the European market is heavily influenced by sustainability, ethical sourcing, and regulatory alignment. Consumers show a strong preference for eco-friendly yoga products, including biodegradable mats made from natural rubber, cork-based accessories, and yoga apparel produced from organic or recycled materials.

Government support for mental well-being further distinguishes the region. In the UK, the expansion of social prescribing frameworks, which formally recognize mindfulness and meditation courses as legitimate health interventions, is driving institutional adoption across healthcare providers, schools, and community programs. This policy-backed demand creates a stable and recurring revenue base that is less susceptible to fashion cycles. Overall, Europe’s yoga and meditation products market is characterized by privacy-conscious consumers, sustainability-led purchasing decisions, and long-term institutional support.

Asia Pacific Yoga and Meditation Products Trends

Asia Pacific is projected to be the fastest-growing regional market with 10.2% CAGR through 2033, led by rapid expansion in India and China. As the birthplace of yoga, India is witnessing a strong revival and modernization of the practice, supported by public initiatives such as the International Day of Yoga, which has significantly increased awareness and participation across urban and semi-urban populations. Rising disposable incomes and digital access are translating this cultural momentum into growing demand for branded yoga and meditation products.

China, meanwhile, represents a high-potential premium and luxury wellness market, where affluent urban consumers increasingly view international yoga brands and studio memberships as status symbols. The region also benefits from substantial manufacturing advantages, serving as a global hub for textile production, yoga mats, and accessories. This proximity to manufacturing reduces costs for local and regional brands, enabling competitive pricing and faster innovation cycles. The rapid expansion of the middle class across ASEAN countries is accelerating a shift from unorganized, generic products toward branded wellness offerings, reinforcing long-term market growth across the Asia Pacific.

Competitive Landscape

The yoga meditation products market is moderately fragmented, featuring a dichotomy between large, diversified athletic brands and specialized, niche wellness companies. Market concentration is higher in the digital segment, where players like Headspace and Calm (competitor) hold significant sway, whereas the physical product market is more distributed among numerous manufacturers.

Key differentiators for market leaders include ecosystem integration, combining hardware (mats/bikes) with software (subscriptions), and community building. Emerging business models are increasingly focusing on "hybrid wellness," offering memberships that grant access to both physical studios and digital libraries, a strategy aggressively pursued by chains like Core Power Yoga and Equinox.

Key Market Developments

- In November 2025, Cigna Healthcare announced a strategic collaboration with Headspace to offer digital mental health tools to over 7 million members. This partnership integrates Headspace's mindfulness content directly into Cigna's employer behavioral health offerings, significantly expanding its B2B user base.

- In December 2025, Peloton Digital expanded its content library by launching a new series of Disney-themed fitness classes and specialized Yin Yoga sessions. This development aims to attract families and users seeking lower-intensity recovery workouts, broadening the Product Type's appeal beyond high-intensity cycling.

- In August 2025, Manduka released its new "Deep Verve" collection for the PRO™ Yoga Mat series. The launch emphasizes the company's commitment to durability and lifetime guarantees, targeting serious practitioners who require high-performance, sustainable equipment for daily practice.

Companies Covered in Yoga and Meditation Products Market

- Lululemon Athletica

- Alo Yoga

- Manduka LLC

- Gaiam (Fit For Life LLC)

- JadeYoga

- Hugger Mugger Yoga Products

- Liforme Ltd.

- PrAna (Columbia Sportswear Company)

- Yoga Design Lab

- BalanceFrom

- Nike Inc.

- Decathlon S.A.

- Adidas AG

- EcoYoga Ltd.

- Barefoot Yoga Co.

Frequently Asked Questions

The market size is estimated to be US$ 8.3 billion in 2026, and is expected to reach US$ 15.5 billion in 2033, with a projected CAGR of 9.3% from 2026 to 2033.

Key drivers include the rising global prevalence of stress and anxiety, increased adoption of corporate wellness programs, and the digitization of fitness through smart apps and wearables.

The Apparel segment generates the most revenue, accounting for roughly 45% of the market, driven by the popularity of athleisure wear.

North America leads the market, supported by high disposable incomes, strong digital infrastructure, and the presence of key industry players like Peloton and Headspace.

A major opportunity lies in the healthcare sector, specifically in integrating yoga therapy into rehabilitation programs and insurance-covered medical interventions.