Marketing Automation Software Market Size, Share, and Growth Forecast, 2026 – 2033

Marketing Automation Software Market by Deployment (Cloud-based, On-premises), Channel Type (Email, Social Media, Mobile App/Messaging, Others), Application Type (Email Marketing, Lead Nurturing & Scoring, Others), and Regional Analysis 2026 – 2033

Marketing Automation Software Market Size and Trends Analysis

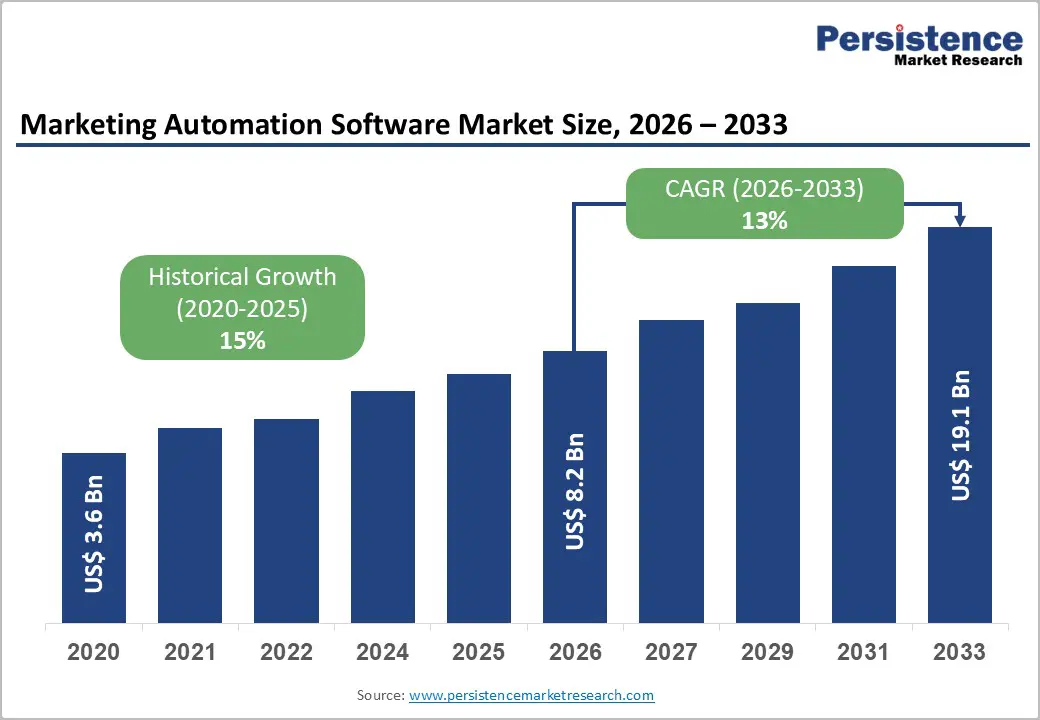

The global marketing automation software market size is likely to be valued at US$8.2 billion in 2026 and is expected to reach US$19.1 billion by 2033, growing at a CAGR of 13% during the forecast period from 2026 to 2033, driven by the rising demand for personalized customer engagement amid digital transformation.

The market is currently experiencing a transformative phase driven by the integration of Generative AI (GenAI) and machine learning, which are shifting platforms from simple task schedulers to predictive decision engines. Organizations are increasingly prioritizing data-driven customer journey mapping, using unified platforms to bridge the gap between sales and marketing teams, thereby accelerating revenue cycles and improving customer retention rates without relying on hyperbole.

Key Industry Highlights:

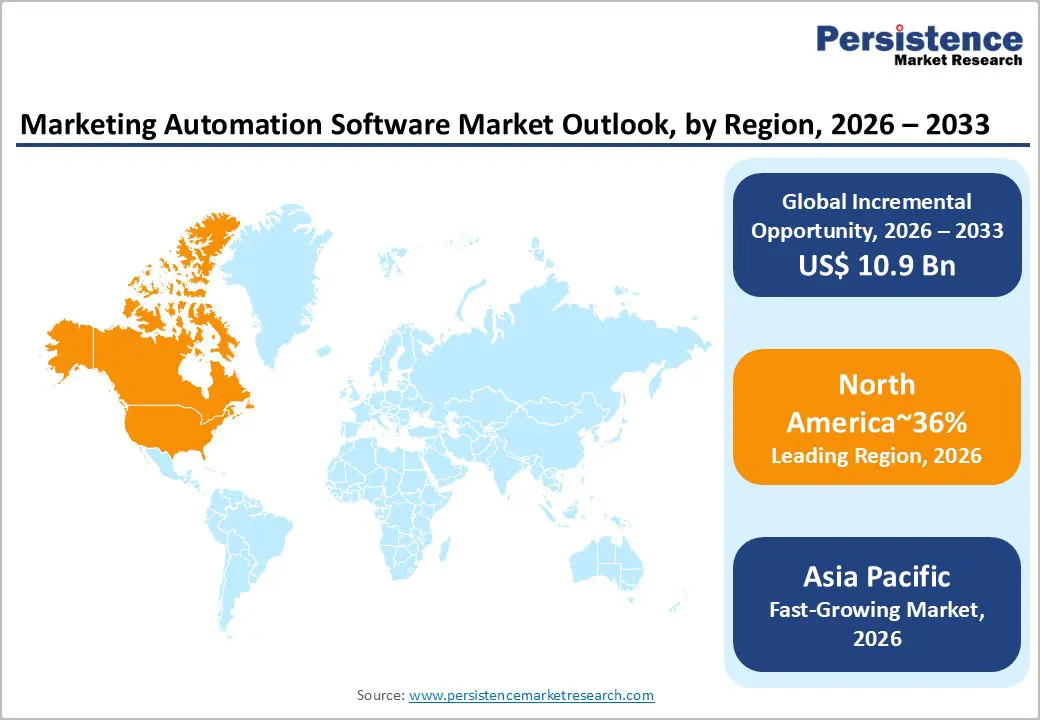

- Leading Region: North America is expected to lead with approximately 36% share, supported by high enterprise software penetration, early adoption of Generative AI-driven marketing workflows, and strong demand for privacy-compliant, first-party data activation platforms.

- Leading Deployment: Cloud-based deployment is anticipated to remain the leading deployment model, holding around 74% share, as enterprises and SMEs prioritize scalability, lower upfront infrastructure costs, rapid implementation, and seamless integration with CRM, CDP, and cloud-native analytics ecosystems.

- Leading Channel Type: Email is expected to remain the leading channel type, accounting for approximately 35% share, as email continues to deliver measurable ROI, mature automation workflows, and deep integration with customer lifecycle management across B2B and B2C marketing operations.

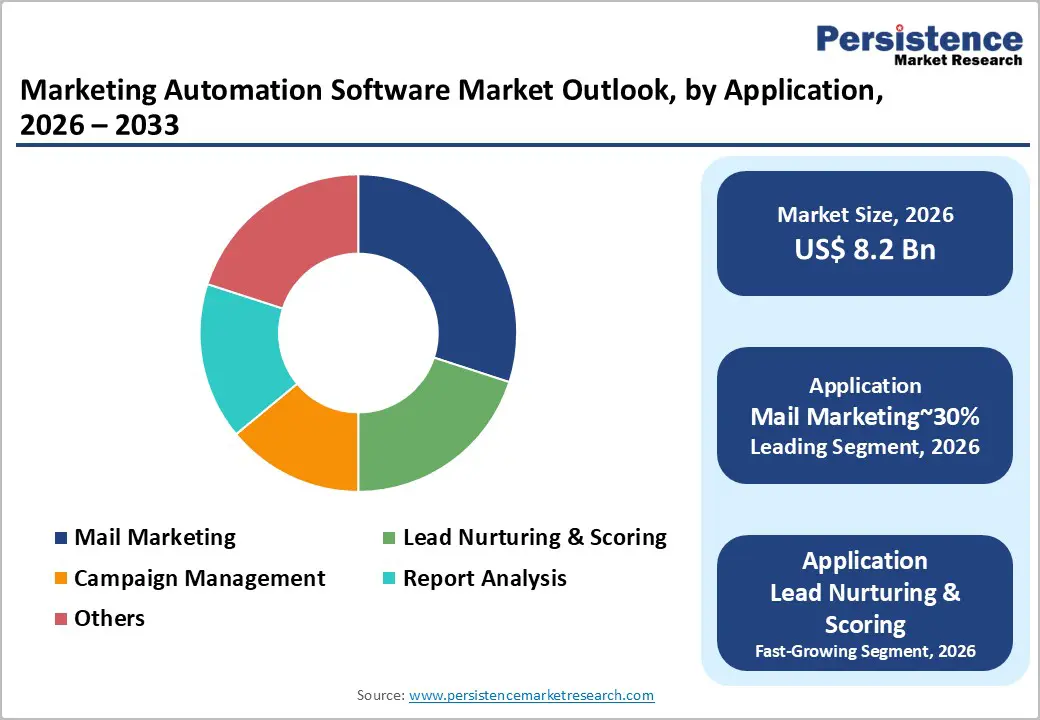

- Leading Application: Email marketing is anticipated to remain the leading application, holding around 30% share, driven by its central role in omnichannel campaign execution, lead nurturing workflows, and performance attribution within marketing automation platforms.

| Key Insights | Details |

|---|---|

| Marketing Automation Software Market Size (2026E) | US$8.2 Bn |

| Market Value Forecast (2033F) | US$19.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 13% |

| Historical Market Growth (CAGR 2020 to 2025) | 15% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis: Integration of Artificial Intelligence and Generative AI

The integration of AI and Generative AI is transforming marketing automation, shifting platforms from rule-based systems to predictive, self-optimizing solutions. AI-enabled workflows enhance hyper-segmentation, behavioral modeling, and predictive lead scoring, allowing marketers to prioritize high-intent prospects with precision. Generative AI furthers this by automating content ideation, copy variation, creative testing, and personalized messaging at scale, reducing bottlenecks in campaign lifecycles. This shift is turning marketing automation from a campaign management tool into a revenue intelligence layer embedded in CRM and customer data platforms.

From an operational perspective, AI-driven orchestration enables real-time optimization across channels, adjusting send timing, creative variants, and channel mix based on user responses and historical engagement patterns. This directly addresses efficiency, performance attribution, and ROI concerns as customer acquisition costs rise and privacy constraints limit targeting. For vendors, AI-native architectures offer defensible differentiation, while enterprises gain higher conversion efficiency, reduced manual workload, and faster campaign iterations. As AI governance improves, its integration will remain a key driver in platform selection and competitive positioning. For instance, Adobe Marketo Engage's 2025 launch of GenAI-powered email tools exemplifies these advancements, enhancing personalization and lead generation.

Surge in SME Adoption of SaaS Solutions

The rapid adoption of cloud-based SaaS marketing automation by small and medium enterprises (SMEs) is reshaping the market, expanding beyond its traditional enterprise focus. Historically limited by high licensing fees and integration complexity, SMEs now benefit from subscription models that eliminate upfront costs and simplify deployment. Modular, "light" platform editions with easy onboarding, preconfigured workflows, and template-driven campaigns lower barriers to entry, enabling quicker time-to-value for resource-strapped teams. This shift opens new growth opportunities for vendors, particularly in underpenetrated regional and vertical SME markets.

From a competitive standpoint, the rise of SME adoption is influencing product roadmaps, pushing vendors toward more user-friendly, low-code solutions and automated core functions such as email nurturing, social publishing, and CRM integration. These tools help SMEs streamline marketing processes and improve efficiency without needing to scale up headcount. As SME adoption accelerates faster than enterprise uptake, vendors are prioritizing tiered pricing, self-service setups, and integrations with e-commerce and lightweight CRM systems. This shift diversifies revenue streams, reduces reliance on long enterprise sales cycles, and drives recurring SaaS subscription growth. For example, ActiveCampaign’s April 2025 update to its AI Campaign Builder allows marketers to fine-tune AI-generated content, enhancing campaign relevance and ROI.

Barrier Analysis: Integration Complexity and Data Silos

Integration complexity within fragmented MarTech stacks remains a significant barrier to marketing automation adoption and value realization, especially for organizations with diverse CRM, e-commerce, analytics, and legacy IT systems. Disparate data schemas, proprietary APIs, and inconsistent identity resolution prevent the creation of a unified customer profile, undermining key use cases such as omnichannel orchestration, real-time personalization, and closed-loop attribution. As a result, automated campaigns often operate on incomplete or delayed data, risking inconsistent messaging, poor segmentation, and misaligned customer journeys. This fragmentation weakens the effectiveness of AI-enabled automation, as predictive models and personalization engines rely on high-quality, integrated data pipelines.

From a cost and execution standpoint, integration challenges erode ROI by extending deployment timelines and increasing the total cost of ownership. Organizations invest heavily in custom middleware, connectors, and ongoing maintenance to bridge system gaps, leading to technical debt and operational fragility. This dependence on bespoke integrations raises switching costs, locking enterprises into suboptimal vendor ecosystems and limiting platform flexibility. For SMEs with limited IT resources, these integration hurdles are even more pronounced, often resulting in underutilized automation features and a disconnect between platform capabilities and outcomes. Together, integration friction and data silos hinder market penetration, scalability, and the full potential of AI-driven marketing automation.

Market Opportunities: Hyper-Personalization via Predictive Analytics

Hyper-personalization is emerging as a key growth driver in marketing automation, as enterprises transition from campaign-centric models to customer-level orchestration powered by predictive analytics. With growing audience fatigue from generic messaging, platforms that enable 1:1 engagement at scale gain a competitive edge. The core opportunity lies in unifying structured behavioral data with unstructured signals, such as social sentiment, web interactions, call-center transcripts, and support ticket histories, to infer intent and determine the "next best action." This shifts marketing automation from rules-based sequencing to probabilistic decision-making, optimizing content, channel, and timing in real-time across the customer lifecycle, from acquisition to reactivation.

Commercially, personalization engines embedded within automation stacks are poised for accelerated value capture as enterprises focus on churn reduction, customer lifetime value expansion, and cross-sell efficiency in a more cost-constrained acquisition environment. Buyers increasingly seek platforms that natively embed predictive models, reduce reliance on external customer data platforms (CDPs), and demonstrate measurable improvements in engagement, conversion, and retention. Vendors that re-architect solutions toward anticipatory engagement platforms can command premium contracts, especially in sectors with high switching costs and complex customer journeys, such as financial services, e-commerce, and B2B SaaS. Strategic differentiation will hinge on data fusion capabilities, model explainability, privacy-safe inference, and real-time decision orchestration, positioning hyper-personalization as a defensible, monetizable layer in the marketing automation ecosystem. For example, Klaviyo's September 2025 launch of its AI Agent within the Customer Hub exemplifies this shift, offering 24/7 customer support, personalized recommendations, and enhanced retention with in-stack predictive personalization.

AI–5G Convergence

The convergence of Artificial Intelligence, 5G connectivity, and edge computing is set to drive significant growth in marketing automation entering 2026, enabling real-time decisioning, high-bandwidth content delivery, and low-latency customer interactions at scale. Ultra-low latency networks allow AI-driven personalization engines to infer intent and deliver context-aware content synchronously with user behavior, enhancing engagement and conversion. Edge intelligence moves inference closer to the user, reducing latency, improving privacy via localized processing, and supporting mobile use cases where cloud dependency previously limited responsiveness. Simultaneously, 5G unlocks immersive ad formats such as AR/VR and interactive 3D experiences within automated journeys, expanding creative possibilities for performance marketing. Hyper-local targeting further extends automation into proximity-based activation, enabling real-time offer orchestration tied to precise location signals.

Strategically, the AI–5G convergence transforms marketing automation from workflow execution to autonomous revenue orchestration. Continuous data streams enable systems to dynamically adjust bids, budgets, creatives, and channel mixes in near real-time based on performance telemetry. Conversational interfaces evolve into low-latency voice and video agents, supporting commerce and service flows. Programmatic advertising moves toward second-by-second optimization, continuously adapting targeting and creatives to streaming data. Vendors embracing edge-native AI, privacy-preserving inference, and immersive content will capture early enterprise demand, especially in retail, mobility, travel, and on-demand services.

Category–wise Analysis

Channel Type Insights

Email is expected to lead the market, accounting for approximately 35% share, driven by its high ROI, deep integration capabilities, and role as the foundation of omnichannel orchestration. Platforms, including Active-Campaign, Salesforce, and HubSpot, leverage predictive analytics, customer behavior signals, and AI-powered automation to optimize lifecycle campaigns, while advanced features such as hyper-personalization, interactive AMP emails, and BIMI-enhanced brand recognition reinforce engagement. The continued emphasis on intelligent ecosystems and first-party data collection ensures email remains indispensable for lead generation, automated follow-ups, and coordinated campaigns across SMS and social channels. Its technical reliability and familiarity among enterprise and SMB marketers further solidify its dominant market position.

Mobile app automation is expected to be the fastest-growing segment, driven by its ability to deliver real-time, context-aware messaging and deep user engagement. Platforms, including Braze, Airship, and CleverTap, leverage agentic AI for predictive push notifications, in-app personalization engines, and Zero-UI interactions on wearables to maximize retention and conversion. SDK consolidation, app clips, instant apps, and edge-side automation allow campaigns to trigger without latency, while biometric and location-based data provide granular behavioral insights. The expansion of 5G networks, rich media capabilities, and AI-driven churn prevention strategies is accelerating adoption, making mobile apps the primary growth engine for innovative marketing automation solutions.

Application Insights

Email marketing automation is expected to lead, accounting for approximately 30% share, driven by its unparalleled ROI, first-party data ownership, and central role in omnichannel engagement. Platforms such as Salesforce Einstein 1, HubSpot Breeze, and Klaviyo leverage Agentic AI to autonomously orchestrate content, timing, and frequency based on real-time user behavior, while innovations such as AMP for Email 2.0 and BIMI enhance conversion and brand trust. Hyper-personalization at scale, AI-generated visuals, and zero-party data integration ensure that email remains the primary engine for both B2B and B2C conversions, making it the backbone of modern marketing strategies and a critical touchpoint for high-value customer journeys.

Lead nurturing & scoring is expected to be the fastest-growing segment, driven by its ability to optimize conversion efficiency and manage complex B2B buying journeys. Platforms, including 6sense, HubSpot, and Adobe Marketo, use AI-powered intent scoring, predictive churn analysis, and hyper-personalized nurture paths to identify sales-ready leads and reduce wasted ad spend. Real-time alerts to sales teams, conversational chat-based nurturing, and zero-party data integration allow every prospect to receive uniquely tailored engagement, while graph database insights map inter-company connections for precise targeting. These innovations accelerate revenue impact and make automated lead nurturing an indispensable growth driver.

Regional Insights

North America Marketing Automation Software Market Trends

North America is projected to dominate the global demand for data-driven customer engagement solutions, capturing around 36% of the total market share. This is attributed to a mature digital commerce ecosystem, high enterprise technology spending, and early adoption of AI-driven architectures. The region benefits from a large concentration of enterprises with complex omnichannel marketing needs, robust cloud infrastructure, and a culture deeply rooted in performance marketing, especially in sectors such as retail, BFSI, healthcare, and B2B tech.

The demand is expected to remain strong due to sustained investments in AI-native platforms, real-time personalization, and the operational need to integrate CRM, CDP, and marketing automation into unified stacks. Regulatory pressures, particularly around privacy and data protection, will further shape platform capabilities, with an emphasis on privacy-by-design, consent management, and first-party data activation.

The U.S. will remain a leader, driven by its extensive digital advertising market and high SaaS adoption. Canada is anticipated to see growth in platform deployments, supported by cloud migration and increasing cross-border digital commerce with the U.S. The region’s growth is also fueled by the shift toward zero-party and first-party data strategies, AI-powered analytics, edge computing for real-time marketing, and consolidation of customer data into integrated growth platforms.

Europe Marketing Automation Software Market Trends

Europe is set to remain a key player in the market, holding around 27% of the total market share. This is driven by regulatory rigor, particularly GDPR compliance, and a focus on ethical AI. The region’s growth is underpinned by widespread adoption of GDPR-compliant platforms and AI frameworks aligned with the EU AI Act, prioritizing transparency and conversion efficiency over lead volume. High digital literacy, strong cloud infrastructure, and broad use of omnichannel engagement (email, messaging apps, social media) further bolster demand.

Regulatory enforcement, especially privacy-by-design and server-side tracking, incentivizes compliance, resulting in higher customer retention and stable subscription revenues for vendors. The rapid adoption of hyper-localized AI content, Green MarTech preferences, and EU-driven interoperability standards favor platforms that integrate with open APIs across diverse enterprise ecosystems. Germany and the U.K. drive European performance, with significant contributions from the DACH region and the U.K. & Ireland.

Leading players such as SAP Emarsys, Microsoft Dynamics 365, Salesforce, HubSpot, Adobe (Marketo), and Brevo emphasize multilingual support, explainable AI, and privacy-preserving features. The region’s focus on zero-party data collection, Edge AI for localized processing, and automation solutions for sectors such as industrial, BFSI, and public services further strengthens its market stability. Europe’s regulatory-driven approach sets the global benchmark for high-value, compliant marketing automation.

Asia Pacific Marketing Automation Software Market Trends

Asia Pacific is the fastest-growing region, driven by mobile-first digital adoption, rapid urbanization, and a surge in e-commerce and digital payments. The region’s growth is anchored in the proliferation of Super-Apps such as WeChat, KakaoTalk, and Line, which integrate messaging, payments, and commerce into a single ecosystem, allowing automation to reach consumers directly where they interact most. Hyper-local cloud clusters launched in Mumbai, Seoul, and Jakarta reduce latency, enabling real-time AI-powered personalization, while SMEs are leapfrogging legacy CRM systems to adopt AI-first, mobile-centric automation. The youthful, tech-savvy demographic, combined with extensive 5G rollout across China, India, and Vietnam, supports high-volume, hyper-personalized engagement.

The major key industrial trends include Conversational Commerce through messaging apps, vernacular NLP for multi-language automated campaigns, voice-based outreach in rural populations, and short-form video automation on TikTok/Douyin/Reels. Regulatory reforms such as India’s DPDP Act and China’s PIPL are accelerating permission-based marketing and local data storage. Leading players include Alibaba, Tencent, Baidu, Netcore Cloud, WebEngage, CleverTap, Line Corp, Braze, and HubSpot, with India emerging as a global R&D hub exporting advanced MarTech solutions. Offline-to-online automation, low-code/no-code journey builders, and 5G-enabled personalization underscore APAC’s position as the growth engine of the global market.

Competitive Landscape

The global marketing automation software market demonstrates moderate consolidation driven by technical and ecosystem complexity. Incumbents such as Salesforce, Adobe, and HubSpot leverage scale, platform control, and validated expertise to secure enterprise clients, collectively holding around 40-50% of the market. Mid-tier and specialized vendors, including Klaviyo and ActiveCampaign, compete through vertical-specific functionality, usability, and price differentiation. Innovation adoption is widespread, particularly in ecosystem integration, where seamless connectivity with other business tools drives incremental competitive advantage. Competitive behaviour balances defending premium enterprise segments while pursuing growth via niche or regional opportunities.

Even in this moderately consolidated market, gradual evolution toward tech-enabled solutions is evident, with vendors increasingly emphasizing plug-and-play integrations and specialized automation features. Sustainability is emerging indirectly through efficient workflow automation that reduces operational overhead and resource consumption. This signals ongoing pressure to differentiate beyond pricing alone, encouraging both incumbents and smaller vendors to invest in platform interoperability, user-centric design, and continuous feature innovation to maintain relevance and capture growth across fragmented segments.

Key Industry Highlights

- In December 2025, HubSpot released updates for smarter segmentation, Segment Analytics, and tighter AI controls. These provide performance insights and data governance, minimizing manual efforts and optimizing marketing automation precision.

- In November 2025, Consensus launched an AI-Powered Demo Automation Platform. It streamlines video demo creation and tailoring for campaigns, saving time and improving marketing content relevance.

- In February 2025, Klaviyo introduced Automated SMS conversations and Spin-to-win gamified forms. These features drive higher engagement through interactive messaging and incentives, improving conversion rates and customer interaction in automated campaigns.

Companies Covered in Market

- Oracle

- Microsoft

- SAP

- Braze

- Klaviyo

- ActiveCampaign

- Intuit (Mailchimp)

- Constant Contact

- CleverTap

- Salesforce Inc.

- Adobe Inc.

- HubSpot

- Keap

- Genesys

- Zoho Corporation

- Thryv

- Ontraport

Frequently Asked Questions

The global marketing automation software market is projected to be valued at US$8.2 billion in 2026 and is expected to reach US$19.1 billion by 2033, driven by the integration of AI and the rising demand for personalized, data-driven customer engagement.

The integration of AI and Generative AI is revolutionizing platforms, transforming them from basic schedulers into predictive decision engines. This shift enables hyper-personalization, automated content creation, real-time optimization, and enhanced ROI, positioning automation as a key revenue intelligence layer in modern marketing.

The marketing automation software market is forecast to grow at a CAGR of 13.0% from 2026 to 2033, reflecting accelerated adoption across enterprises and SMEs.

Asia Pacific is the fastest-growing regional market, fueled by mobile-first digital adoption, the proliferation of Super-Apps, rapid e-commerce growth, and extensive 5G rollout, which enable hyper-localized, real-time AI-powered engagement.

The market is moderately consolidated, with key players including Salesforce Inc., Adobe Inc., HubSpot, Oracle, and Microsoft. These incumbents leverage scale and platform ecosystems, while specialists, including Klaviyo, Braze, and ActiveCampaign, compete on vertical expertise and usability.