- Technology

- Multi-Touch Market

Multi-Touch Marketing Attribution Software Market Size, Share, and Growth Forecast 2026 - 2033

Multi-Touch Marketing Attribution Software Market by Component (Solutions, Services including Integration and Implementation Services, Advisory Services, Support and Maintenance Services), by Deployment Model (On-premise, Cloud), by Organization Size, by Industry, by Regional Analysis, 2026 - 2033

Multi-Touch Marketing Attribution Software Market Size and Trend Analysis

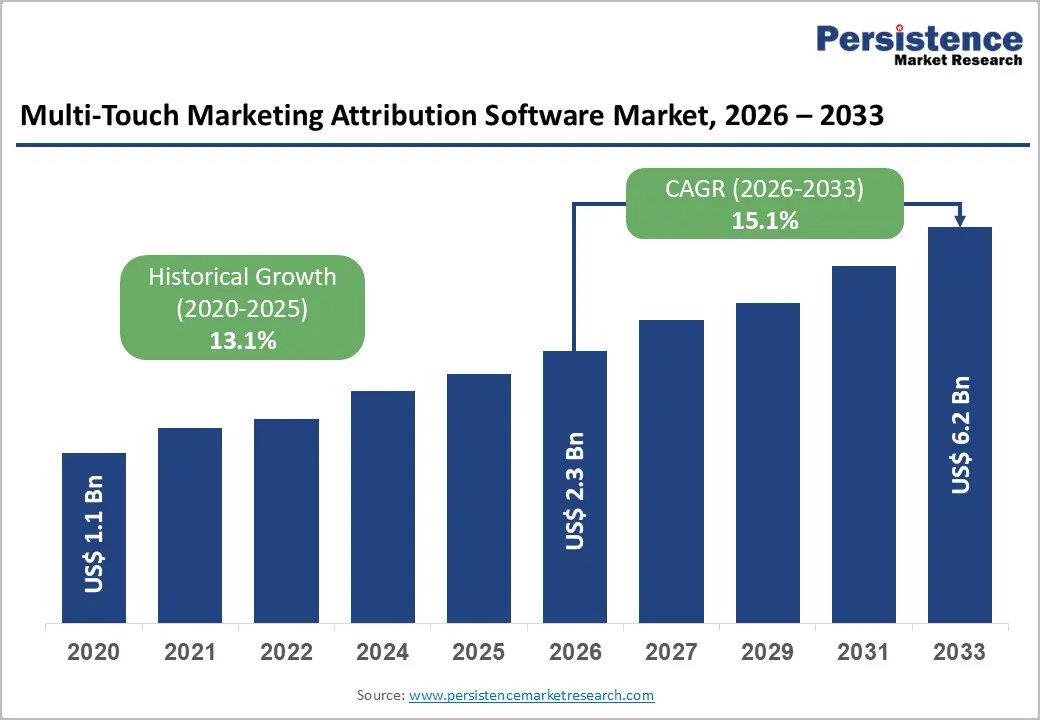

The global multi-touch marketing attribution software market size is projected to reach US$ 2.3 billion in 2026 and expand to US$ 6.2 billion by 2033, growing at a CAGR of 15.1% from 2026 to 2033.

This growth is driven by enterprises’ increasing need for enhanced marketing ROI visibility and the adoption of AI and ML technologies. As customers interact across multiple digital and offline touchpoints, organizations require sophisticated attribution solutions to identify the channels and campaigns that truly influence conversions. The rising focus on omnichannel marketing and integration with customer data platforms (CDPs) is further fueling demand for unified, comprehensive measurement tools.

Key Market Highlights

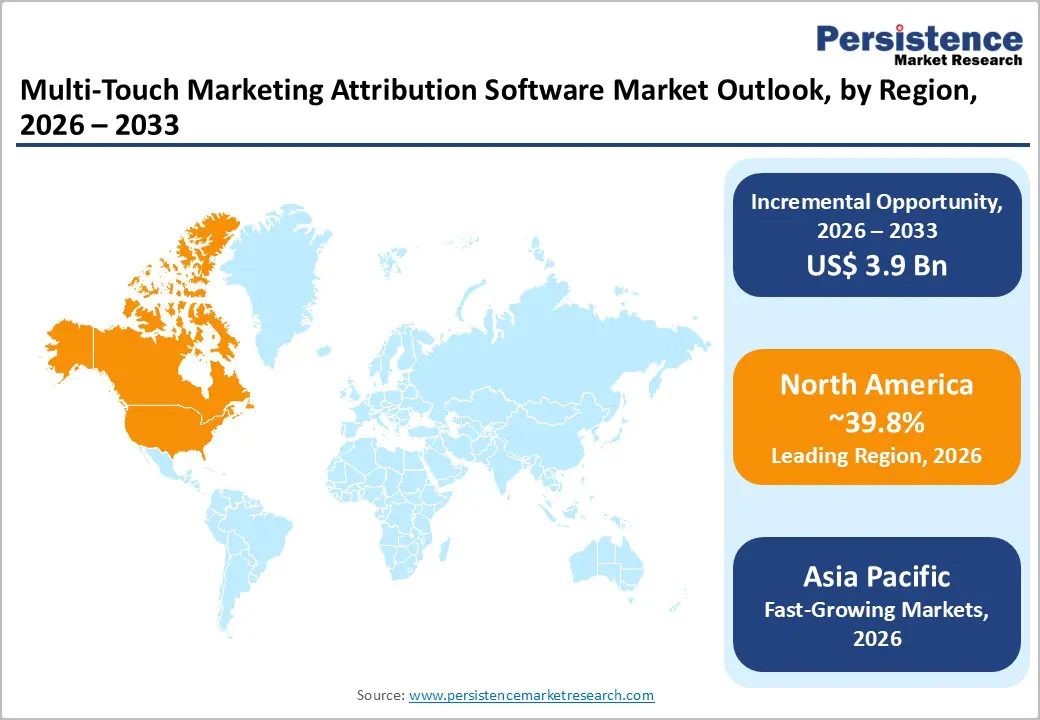

- Leading Region: North America leads the market with a 39.8% share, supported by a strong enterprise base, high martech spending, and mature digital marketing ecosystems.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, holding 32% market share, driven by rapid e-commerce growth, digital infrastructure expansion, and mobile-first adoption.

- Dominant Segment: The solutions component dominates the market with a 65.7% share, reflecting strong demand for core attribution platforms and analytics capabilities.

- Fastest-Growing Segment: Cloud-based deployment, accounting for 67.5% share, is expanding rapidly due to scalability, cost efficiency, and seamless SaaS integration.

- Key Market Opportunity: AI-driven, privacy-first attribution solutions present a major opportunity as enterprises increasingly invest in AI to enhance accuracy while complying with GDPR and CCPA.

| Key Insights | Details |

|---|---|

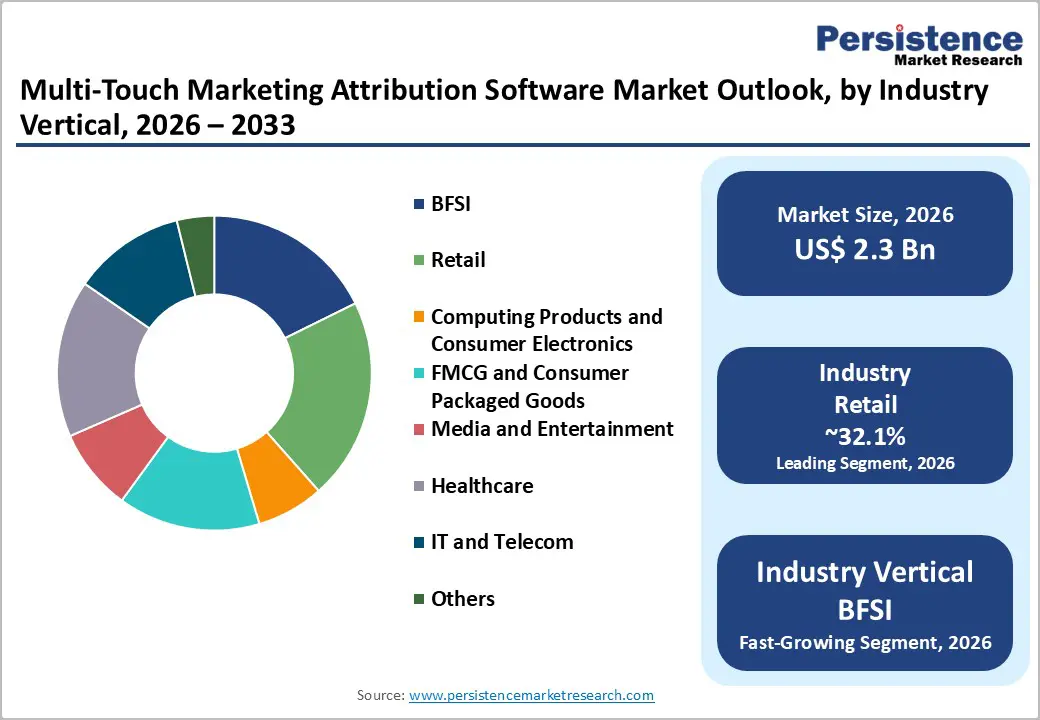

| Multi-Touch Marketing Attribution Software Market Size (2026E) | US$ 2.3 Billion |

| Market Value Forecast (2033F) | US$ 6.2 Billion |

| Projected Growth CAGR (2026 - 2033) | 15.1% |

| Historical Market Growth (2020 - 2025) | 13.1% |

Market Dynamics

Drivers - Rising Demand for Enhanced Marketing ROI Visibility Through Accurate Attribution

The modern digital marketing landscape has grown increasingly complex, with customer journeys spanning multiple touchpoints across search, social media, email, display advertising, and offline channels. Marketing teams are under growing pressure to demonstrate the effectiveness of every marketing dollar spent. Traditional single-touch attribution models fail to capture the intricacies of multi-step buyer journeys, driving the adoption of multi-touch attribution (MTA) solutions that accurately measure each touchpoint’s contribution to conversions and revenue.

Organizations are increasingly prioritizing advanced attribution tools to track customer journeys effectively. Precise attribution empowers marketers to optimize budgets, refine campaigns, and improve overall marketing effectiveness. By understanding which channels genuinely drive conversions, enterprises can achieve a sustainable competitive advantage and enhance operational efficiency in an increasingly data-driven marketing environment.

Accelerated Digital Transformation and E-Commerce Expansion Driving Attribution Software Adoption

The global shift toward digital-first business models has transformed how organizations engage customers, with the pandemic accelerating digital transformation across industries. Businesses now rely heavily on online presence and data-driven marketing strategies, including e-commerce, subscription models, and self-service channels. Companies leveraging multiple digital touchpoints need robust attribution tools to understand customer behavior and optimize marketing investments effectively.

With the Asia Pacific region accounting for around 45% of global digital marketing spend, led by China and India, the demand for multi-touch attribution software has surged. The ability to track and attribute customer actions across mobile apps, websites, and social platforms is essential for businesses competing in fragmented digital markets and seeking to maximize returns on growing digital marketing budgets.

Restraints - Challenges in Data Integration and Compliance with Privacy Regulations Impeding Adoption

Implementing multi-touch attribution solutions requires seamless integration across diverse marketing technology systems, customer data sources, and analytics platforms. Enterprises often struggle with consolidating fragmented data, maintaining quality, and ensuring consistency across platforms. Additionally, stringent privacy regulations, including GDPR, CCPA, and the emerging AI Act, create compliance burdens. Restrictions on third-party cookies, with Google Chrome phasing them out by 2025, add further technical complexity.

Organizations must navigate these compliance requirements while maintaining accurate attribution, increasing implementation costs, and timelines. The shift away from traditional tracking methods necessitates alternative attribution approaches, creating technical challenges that particularly affect smaller enterprises with limited data governance capabilities, thereby restraining broader adoption of multi-touch attribution software.

High Implementation and Operational Costs as a Barrier to Adoption

Deploying comprehensive multi-touch attribution solutions requires substantial upfront capital investment and ongoing operational expenses, which pose significant adoption barriers, especially for small and medium-sized enterprises. Integration with marketing technology stacks, data warehouses, and CRM systems often demands specialized technical expertise and professional services.

Organizations may need additional cloud infrastructure, data engineering resources, and analytics talent to operationalize attribution tools fully. Extended implementation timelines and reliance on consultants increase the total cost of ownership. For businesses with constrained marketing budgets, these financial and resource demands delay or prevent adoption, despite recognizing the strategic importance of multi-touch attribution for optimizing marketing performance.

Opportunity - AI-Powered Predictive Attribution and Privacy-First Solutions Driving Market Opportunities

The convergence of artificial intelligence advancements and stringent privacy regulations presents significant opportunities for next-generation attribution solutions. AI and machine learning algorithms excel at uncovering patterns in complex datasets and making predictions even with limited data, addressing challenges in cookieless environments. Nearly 70% of enterprises are investing in AI to enhance personalization and predictive marketing insights.

Algorithmic and data-driven attribution models, which hold 34.8% market share and grow at 14.3% CAGR, outperform traditional rule-based approaches. Leveraging vast datasets, these solutions help marketers understand true customer journeys, optimize campaigns based on evidence, and combine accuracy with privacy-first methodologies like first-party data and consent-based tracking, enabling vendors to differentiate their offerings and capture significant market share.

Expansion of Attribution Solutions into Regulated Industries and Emerging Markets

While retail and e-commerce have historically dominated adoption, regulated industries such as banking, financial services (BFSI), and healthcare now present significant growth opportunities. Long sales cycles, complex compliance requirements, and omnichannel customer journeys in these sectors create demand for sophisticated attribution capabilities that optimize marketing spend and improve conversion outcomes.

Simultaneously, emerging markets in Asia Pacific are experiencing rapid e-commerce growth, government digital initiatives like India’s Digital India campaign, and increasing mobile-first consumer behavior. The region’s digitally native audience and expanding infrastructure allow companies to adopt modern cloud-native attribution solutions directly, bypassing legacy constraints. This combination of vertical and geographic expansion represents a substantial opportunity for attribution software providers.

Category-wise Analysis

Component Insights

The solutions segment dominates the multi-touch attribution software market, accounting for approximately 65.7% of the total component category. Solutions include the core attribution platform, algorithmic models, analytics dashboards, and integration frameworks that enable accurate marketing measurement and optimization. This dominance reflects the critical role of core technology in providing visibility into marketing ROI, helping organizations understand how each channel contributes to conversions and revenue.

The services segment, encompassing integration and implementation, advisory, and support services, represents the fastest-growing category. Organizations increasingly seek bundled offerings combining software and professional services, which accelerate time-to-value, reduce implementation complexity, and provide ongoing optimization support. While services generate lower revenue per customer than solutions, they are high-margin opportunities that enhance operational excellence and maximize the value derived from attribution software deployments.

Deployment Model Insights

Cloud-based deployment is the leading model in the multi-touch attribution software market, commanding approximately 67.5% market share. Cloud solutions offer superior scalability, cost efficiency, and ease of integration compared to on-premise systems. They enable real-time marketing attribution, faster deployment, automatic updates, and lower IT overhead, driving their dominance across enterprises of all sizes seeking agile and scalable solutions.

The on-premise model represents the fastest-growing deployment category. Organizations increasingly adopt hybrid approaches or selective on-premise solutions to maintain control over sensitive data, meet compliance requirements, or integrate with existing IT infrastructure. Cloud adoption remains preferred for its operational advantages, but on-premise offerings continue to grow as organizations balance flexibility, security, and governance needs.

Organization Size Insights

Large enterprises lead the organization size segment, accounting for approximately 66% market share. These organizations implement complex omnichannel marketing strategies involving multiple digital and traditional channels, including display advertising, influencer campaigns, print, TV, and in-person events. Large-scale attribution solutions integrate data from disparate sources, unify insights across organizational silos, and optimize marketing spend by reallocating budgets to high-performing channels.

Small and medium-sized enterprises (SMEs) are the fastest-growing segment. SMEs are increasingly adopting marketing automation platforms and integrated CRM tools, enabling attribution capabilities within existing workflows. Cloud-based solutions make attribution accessible to smaller organizations, allowing them to optimize marketing spend, improve customer acquisition efficiency, and compete effectively with larger enterprises in digital-first environments.

Industry Insights

The retail and e-commerce sector remains the largest and most mature vertical, holding approximately 32.1% of the industry category. Its dominance is driven by direct transaction traceability, intense competition, and diverse marketing touchpoints such as search, social media, email campaigns, and affiliate networks. Attribution is critical for optimizing customer acquisition strategies, mapping omnichannel journeys, and improving return on advertising spend (ROAS).

Emerging verticals such as BFSI, healthcare, FMCG, IT & telecom, and consumer electronics represent the fastest-growing segments. These industries are increasingly investing in digital marketing, recognizing the value of attribution software in understanding omnichannel customer behavior, optimizing campaign performance, and driving strategic marketing decisions in competitive markets.

Regional Insights

North America Multi-Touch Marketing Attribution Software Trends

North America holds the largest market share, accounting for approximately 39.8%. A high concentration of multinational enterprises drives growth, mature digital marketing ecosystems, and technology hubs such as Silicon Valley that foster continuous product innovation. U.S. organizations deploy attribution software to optimize spend across retail, e-commerce, financial services, and technology sectors, tracking customer journeys through search, social, email, and programmatic display advertising.

Regulatory frameworks, including the California Consumer Privacy Act (CCPA) and state-level privacy laws, encourage privacy-compliant solutions. Enterprises also demonstrate strong adoption of AI-driven models and cloud-based deployment, integrating attribution with customer data platforms and analytics infrastructure. The combination of mature digital ecosystems and regulatory compliance drives North America’s leadership position.

Europe Multi-Touch Marketing Attribution Software Trends

Europe represents the second-largest regional market, with growth driven by stringent regulations such as GDPR and the emerging AI Act, along with significant digital transformation investments. Countries like Germany, the U.K., France, and Spain demonstrate mature adoption among enterprises running complex omnichannel campaigns. Privacy-by-design and consent-based tracking have become key differentiators for European solutions.

The market is expanding steadily with a CAGR of 14.6%, supported by the adoption of first-party data strategies, server-side tracking, and digital marketing investments across retail, financial services, and technology sectors. Enterprises increasingly integrate attribution software to optimize marketing spend while remaining compliant with privacy regulations.

Asia Pacific Multi-Touch Marketing Attribution Software Trends

Asia Pacific is the fastest-growing regional market, accounting for approximately 32% of the global market share. Growth is fueled by rapid digital transformation, e-commerce expansion, and government initiatives such as India’s Digital India campaign. China and India lead the region, with mobile-first consumer behavior and rising social commerce adoption creating strong demand for attribution solutions.

Enterprises, particularly SMEs, are adopting cloud-based SaaS attribution platforms with flexible pricing and fast deployment. Rising digital maturity, increasing marketing spend, and competitive pressures drive widespread adoption. The region’s combination of a digitally native consumer base and strong infrastructure development makes it a key growth area for multi-touch attribution software.

Competitive Landscape

The multi-touch marketing attribution software market shows moderate consolidation, led by large enterprise platform providers that embed attribution within broader marketing, analytics, and data ecosystems. These players benefit from established enterprise relationships, wide platform adoption, and strong integration capabilities. Alongside them, mid-sized vendors focus on specialized attribution expertise, advanced analytics, and service-driven differentiation to address complex customer journey measurement needs.

Market competition is increasingly shaped by AI-driven attribution models, omnichannel measurement, and privacy-compliant tracking approaches. Consolidation continues as larger platforms absorb niche specialists to strengthen analytics depth. Emerging differentiation centers on revenue attribution for B2B cycles, account-based measurement, and industry-specific attribution frameworks tailored to regulated sectors and complex buying environments.

Key Market Developments

- In November 2024, AppsFlyer Ltd. unveiled new AI marketing cloud products designed to drive growth measurement, data collaboration, and advanced measurement capabilities, positioning the company at forefront of AI-powered attribution innovation.

- In September 2024, Adobe, Inc. and Microsoft announced significant partnership expansion, integrating sophisticated agentic AI capabilities into familiar marketing tools, enabling more data-driven decision-making and representing significant advancement in marketing technology integration.

- In August 2024, Oracle Corporation surpassed SAP SE as the number one ERP applications vendor in 2024, with Oracle capturing $8.7 billion in ERP revenue and 6.63% market share, demonstrating competitive strength that extends to integrated attribution and marketing analytics capabilities within enterprise platforms.

Companies Covered in Multi-Touch Market

- Adobe, Inc.

- SAP SE

- Oracle Corporation

- Neustar, Inc.

- Visual IQ / NielsenIQ

- LeadsRx, Inc.

- LeanData, Inc.

- Merkle, Inc.

- C3 Metrics, Inc.

- AppsFlyer Ltd.

- Adjust GmbH

- HubSpot, Inc.

- Conversion Logic, Inc.

- Engagio / Demandbase

- CaliberMind, Inc.

- Google LLC

- Full Circle Insights

- Rockerbox

- Singular

Frequently Asked Questions

The market is valued at US$ 2.3 billion in 2026 and is projected to reach US$ 6.2 billion by 2033, growing at a 15.1% CAGR.

Rising demand for marketing ROI visibility, rapid digital transformation, e-commerce growth, and omnichannel marketing adoption are accelerating enterprise adoption.

The solutions segment dominates with a 65.7% share, driven by demand for core attribution platforms, analytics dashboards, and algorithmic measurement capabilities.

North America leads with a 39.8% market share, supported by mature digital ecosystems, high martech investment, and strong enterprise adoption.

AI-driven, privacy-first attribution solutions represent the key opportunity as enterprises invest in AI while complying with GDPR and CCPA.

Adobe, Inc., SAP SE, Oracle Corporation, Neustar, Inc., and Visual IQ (Nielsen IQ) represent market-leading enterprises with integrated attribution capabilities.