- LED & Lighting (Optoelectronics)

- LED Tube Market

LED Tube Market Size, Share, and Growth Forecast, 2026 - 2033

LED Tube Market by Product Type (LED T8, LED T5, LED T10, LED T12), End-Use (Commercial, Industrial, Residential), Sales Channel (Online, Offline), and Regional Analysis for 2026-2033

LED Tube Market Share and Trends Analysis

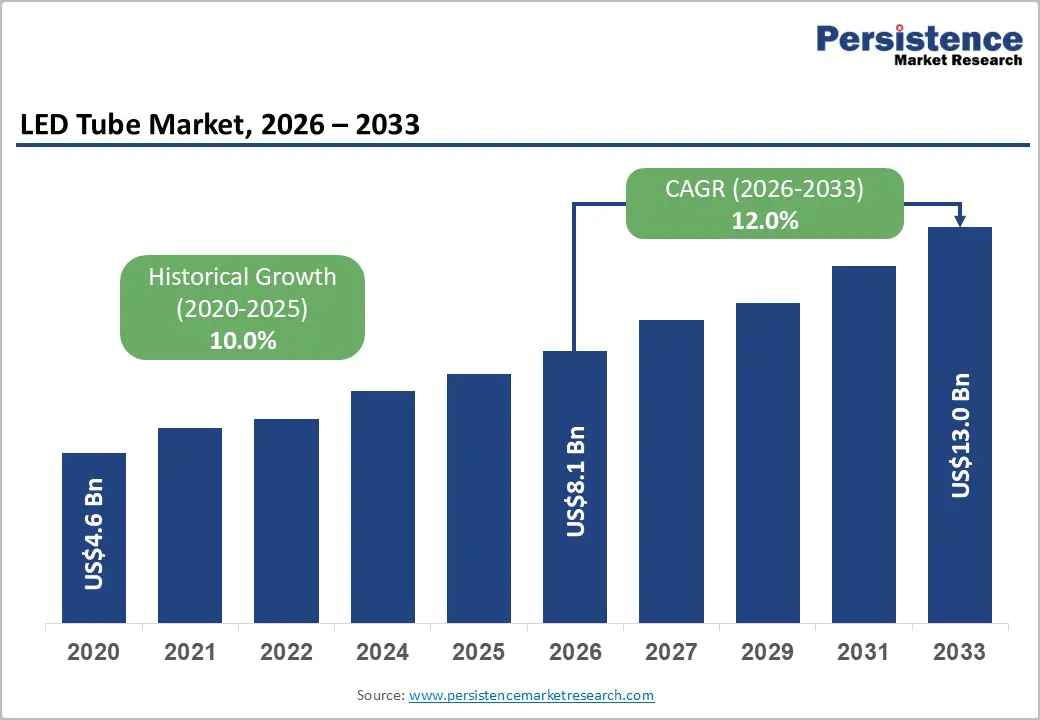

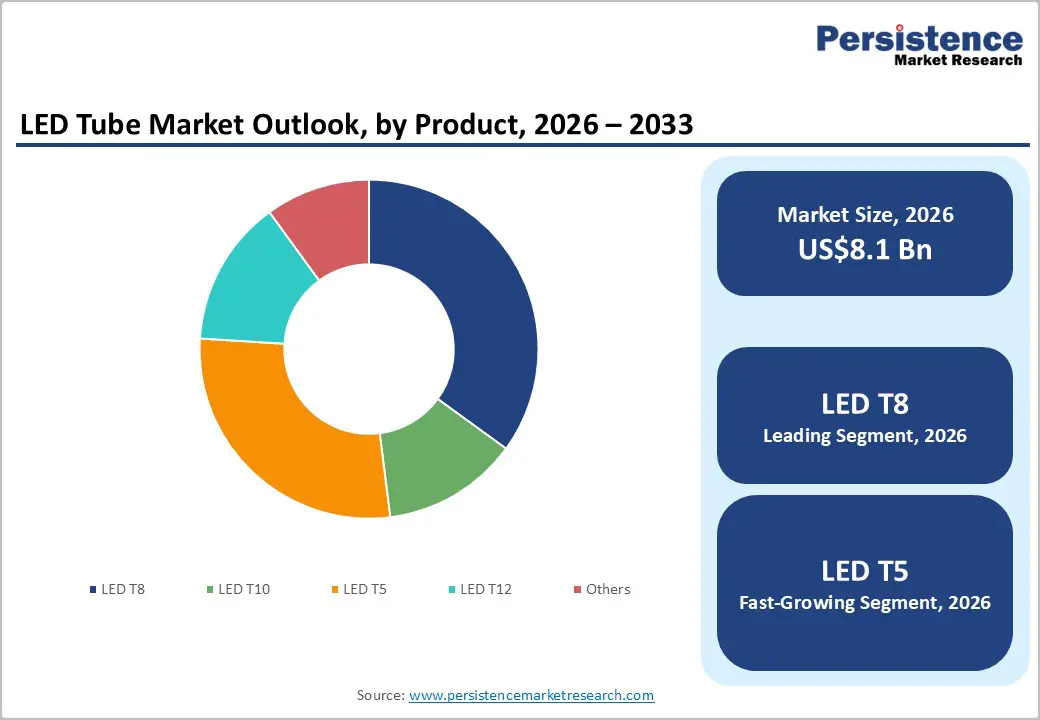

The global LED tube market size is likely to be valued at US$ 8.1 billion in 2026, and is projected to reach US$ 13.0 billion by 2033, growing at a CAGR of 10% during the forecast period 2026−2033. This growth trajectory reflects sustained demand, as organizations increasingly prioritize energy efficiency, regulatory compliance, and long-term cost optimization. Declining light-emitting diode (LED) component prices are improving return on investment, while stricter efficiency standards are encouraging faster replacement of conventional fluorescent lighting. From a strategic perspective, suppliers benefit as buyers shift from pilot installations to large-scale deployments across standardized facilities. Market momentum is strengthening as commercial and industrial end users are actively implementing lighting retrofits to reduce operating expenses and improve asset performance.

Public-sector adoption is also accelerating, as government-backed energy conservation programs continue to support LED tube installations in public infrastructure, educational campuses, and institutional buildings. Over the forecast period, demand is likely to be shaped by integrated sustainability targets, procurement policies favoring efficient technologies, and growing awareness of lifecycle cost advantages. Stakeholders who align product portfolios with regulatory requirements and offer retrofit-friendly solutions will be better positioned to capture incremental demand as replacement cycles shorten globally.

Key Industry Highlights

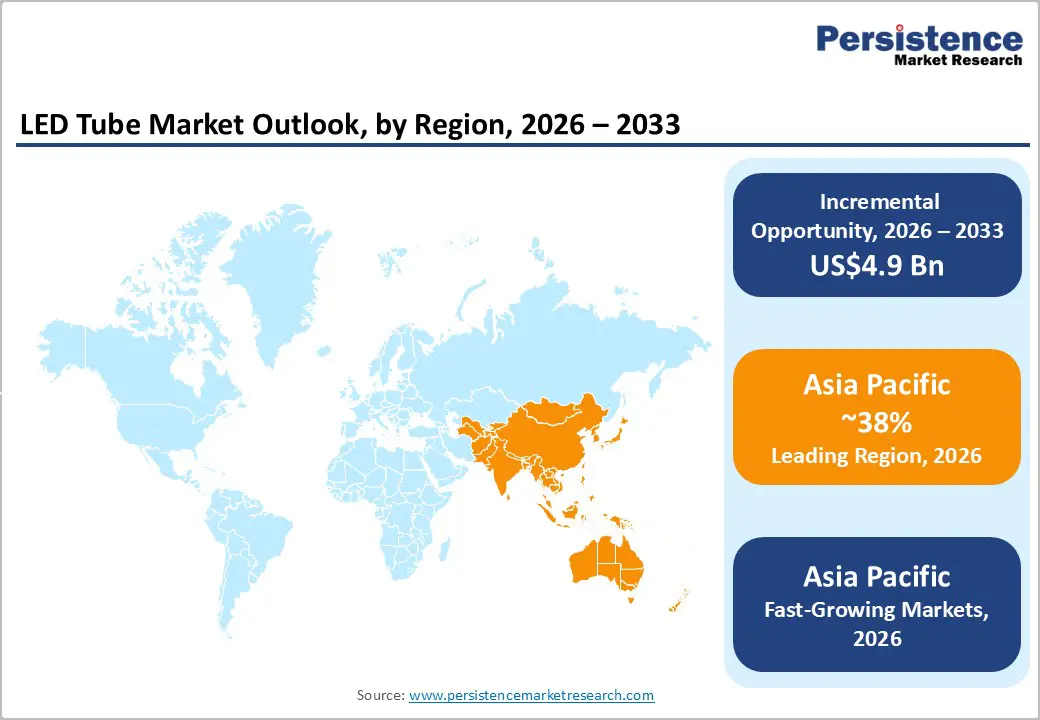

- Regional Dominance: The Asia-Pacific market is likely to be both the leading and fastest-growing, accounting for approximately 38% of the market in 2026, owing to extensive domestic consumption and its role as the primary global electronics manufacturing hub.

- Leading & Fastest-growing Product Type: LED T8 is slated to lead with about 60% of the revenue share in 2026, while LED T5 is likely to be the fastest-growing segment through 2033.

- Dominant & Fastest-growing End-Use: Commercial end use is projected to dominate, accounting for approximately 45% of revenue in 2026, while industrial end use posts the highest 2026-2033 CAGR.

- Market Driver: Stringent global energy-efficiency regulations mandate phase-outs of fluorescent lighting, creating structural replacement demand.

| Key Insights | Details |

|---|---|

| LED Tube Market Size (2026E) | US$ 8.1 Bn |

| Market Value Forecast (2033F) | US$ 13.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10% |

| Historical Market Growth (CAGR 2020 to 2025) | 12% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Energy Efficiency Regulations and Sustainability Mandates

Global energy-efficiency standards are reshaping the lighting industry. LED tubes are the preferred replacement for fluorescent tubes. The U.S. Department of Energy (DOE) establishes regulations that phase out inefficient fluorescent lamps. The European Union (EU) implements the EcoDesign Directive to restrict high-energy lighting products. These measures create mandatory replacement demand across multiple sectors. Organizations upgrade their lighting infrastructure to meet compliance requirements. Governments enforce these standards through clear timelines and penalties for noncompliance. Businesses prioritize the adoption of LED technology to avoid operational disruptions and regulatory fines.

Corporate environmental, social, & governance (ESG) commitments accelerate this transition. Companies pursue carbon neutrality targets through systematic infrastructure upgrades. The commercial, industrial, and institutional segments experience consistent demand growth as a result of this regulatory-corporate convergence. Facility managers select LED tubes as the optimal solution. These tubes are compatible with existing fixtures and exhibit superior energy performance. Procurement teams benefit from predictable replacement cycles that align with long-term sustainability objectives. Strategic suppliers capture this sustained market expansion. They offer comprehensive retrofit solutions and performance guarantees.

Supply Chain Complexity and Component Price Volatility

LED tube manufacturing relies on complex global supply chains. These supply chains face risks from geopolitical tensions, semiconductor shortages, and fluctuations in raw material prices. The industry relies on specialized components, including LED chips, driver electronics, and aluminum housings. Manufacturers source these materials from concentrated supplier bases, primarily in Asia. Recent semiconductor constraints expose sector vulnerabilities to component disruptions. Supply chain managers implement diversification strategies to mitigate risks associated with single-source dependencies. Procurement teams establish alternative supplier relationships to ensure production continuity during market disruptions.

Rare earth element price volatility affects phosphors essential for color rendering. This volatility creates margin pressure for manufacturers. Trade policy uncertainties, including tariff regimes for electronics imports, generate price volatility. These factors complicate long-term project planning for capital-intensive retrofit initiatives. Low-cost manufacturers introduce substandard products. These products challenge quality assurance efforts. Customers develop skepticism toward new entrants. Procurement teams extend sales cycles through rigorous verification protocols. Strategic manufacturers can differentiate through verified quality certifications and transparent supply chain practices, building customer trust through consistent performance guarantees and established reliability records.

Infrastructure Development and Urbanization in Developing Economies

The unprecedented scale, extent, and pace of urbanization across Asia Pacific, Latin America, and Africa generate substantial LED tube demand. New commercial construction and infrastructure modernization accelerate this growth. Governments launch ambitious urban development programs such as India's Smart Cities Mission. The initiative mandates energy-efficient lighting for new urban infrastructure. China's Belt and Road Initiative channels infrastructure investments across multiple countries. Project guidelines specify energy-efficient lighting solutions. Emerging markets adopt LED technology directly. They bypass legacy fluorescent infrastructure and avoid retrofit barriers. Urban planners prioritize modern lighting standards from project inception. Infrastructure developers integrate LED tubes into original design specifications.

Government procurement practices evolve in these regions. Officials prioritize lifecycle costs over initial capital expenditure. LED solutions demonstrate superior total cost of ownership despite higher upfront costs. Municipal authorities establish energy efficiency requirements for public projects. Commercial real estate developers respond to tenant demands for modern lighting infrastructure. Facility managers seek solutions that minimize long-term operational expenses. Strategic suppliers position themselves as preferred partners for large-scale urban projects. They offer comprehensive lifecycle support, including installation, maintenance, and performance guarantees. Local governments create procurement frameworks that favor verified energy-efficient solutions. This approach supports sustainable urban development objectives while optimizing public expenditure.

Category-wise Analysis

Product Type Insights

LED T8 is poised to dominate the product type segment, commanding approximately 60% of the LED tube market revenue share in 2026, owing to its direct compatibility with existing T8 fluorescent fixture infrastructure installed across millions of commercial and industrial facilities worldwide. Facility managers are achieving measurable cost savings because installations require minimal electrical modifications and limited downtime. By retaining existing fixtures, organizations are preserving prior capital investments while realizing immediate reductions in energy consumption and maintenance costs. Upgrade programs are therefore proceeding without disrupting daily operations, enabling productivity continuity while lighting systems are transitioning to higher-efficiency standards.

LED T5 tubes are expected to be the fastest-growing product segment from 2026 to 2033, driven by demand for high-performance lighting in precision-oriented environments. Their compact form factor delivers superior luminous efficacy and a controlled beam distribution, supporting applications such as retail displays, architectural lighting, task workstations, and hospitality interiors. These solutions are performing strongly where focused illumination is required, including visual merchandising zones and premium public spaces. Adoption of T5 configurations in new construction projects is accelerating, as modern recessed fixture designs increasingly incorporate them. Higher pricing is reflecting specialized use cases, tighter performance tolerances, and increased manufacturing precision, positioning T5 products as value-driven solutions rather than volume-led replacements.

End-Use Insights

The commercial segment is poised to capture approximately 45% of the LED tube market revenue in 2026, supported by strong adoption across office buildings, retail spaces, and hospitality properties, where lighting quality directly influences productivity and customer experience. Commercial real estate operators are demonstrating clear financial incentives, as energy expenditure represents a significant share of operating costs in office environments. Facility managers are therefore prioritizing LED tube solutions that are delivering immediate and quantifiable reductions in electricity consumption and maintenance spending. Corporate sustainability reporting requirements are further accelerating portfolio-wide upgrades, while tenant expectations for modern and energy-efficient workspaces are reinforcing the shift toward standardized LED infrastructure across commercial assets.

The industrial segment is expected to be the fastest-growing application area between 2026 and 2033, driven by manufacturing capacity expansion and the rapid development of warehousing and logistics facilities, particularly in emerging economies. Industrial operations are maintaining continuous lighting cycles, which is amplifying the energy savings potential of LED tube conversions over extended operating hours. These solutions also demonstrate high reliability in demanding environments, withstanding temperature fluctuations, vibration, and heavy dust exposure without compromising performance. In contrast, conventional fluorescent systems are experiencing premature failure under similar conditions, leading to frequent maintenance interruptions. As a result, industrial operators are increasingly favoring LED tubes to support operational continuity, safety compliance, and long-term cost efficiency.

Sales Channel Insights

The offline distribution channel is expected to account for approximately 55% of the LED tube market share in 2026, as specialty lighting stores, electrical wholesalers, and brick-and-mortar retail outlets continue to play a central role in purchasing decisions. These channels are enabling buyers to examine products directly, compare alternatives side by side, and assess build quality before finalizing procurement. Access to trained sales and technical personnel further supports adoption, as customers receive application-specific guidance tailored to operating conditions and performance requirements. Offline channels are remaining particularly critical for commercial and industrial buyers, who require customized configurations, detailed project quotations, and on-site technical support to ensure correct specification, installation accuracy, and sustained system performance.

The online channel is forecast to deliver the highest CAGR from 2026 to 2033, driven by the rapid expansion of e-commerce platforms and evolving buyer behavior. Digital marketplaces offer broad product portfolios from multiple manufacturers, enabling customers to evaluate options efficiently. Detailed specifications, performance data sheets, and installation documentation are instantly accessible, reducing information asymmetry during decision-making. Verified customer reviews provide practical insights into real-world performance across diverse use cases, while transparent price comparisons improve value discovery. As e-commerce aggregators increasingly integrate digital sourcing into purchasing workflows, online channels are set to strengthen their role in both small-scale replacements and standardized bulk purchases.

Regional Insights

Asia Pacific LED Tube Market Trends

Asia-Pacific is likely to be the leading and fastest-growing regional market for LED tubes in 2026, accounting for approximately 38% of the market. China leads regional demand through extensive domestic consumption and its role as the primary global manufacturing hub. Japan, India, and ASEAN countries contribute substantial volume through new construction projects, infrastructure upgrades, and industrial expansion. Asian manufacturers maintain cost leadership advantages. Vertical integration spans LED chip production through finished goods assembly. Established supply chain ecosystems support efficient component sourcing and logistics. Government initiatives across China, India, and Southeast Asia mandate or incentivize LED adoption. Procurement policies, utility rebate programs, and updated building codes drive institutional demand.

Rapid urbanization accelerates infrastructure lighting requirements across India and the ASEAN bloc. Commercial office developments, manufacturing facilities, and retail centres create sustained demand for modern lighting solutions. Price sensitivity influences procurement decisions in developing markets. Buyers often prioritize initial capital costs over lifecycle economics considerations. Japanese and South Korean markets emphasize advanced specifications. Smart lighting integration and human-centric illumination are priorities for premium customers. International manufacturers face intense competition from regional suppliers in Southeast Asian and South Asian markets. Strategic positioning requires balancing cost competitiveness with quality differentiation and localized service capabilities.

Europe LED Tube Market Trends

Europe commands a substantial presence in the global market for LED tubes. Germany, the United Kingdom, France, and Spain drive regional demand through ambitious carbon-reduction commitments. The European Green Deal establishes comprehensive climate action frameworks. National plans require deep energy-efficiency improvements across the existing building stock. The EU has been aggressively implementing the Energy Performance of Buildings Directive to accelerate its transition to a net-zero economy. This directive mandates near-zero energy standards for new construction projects. Building specifications inherently favor LED lighting technology from the design phase. Public sector procurement prioritizes verified performance characteristics and environmental certifications.

Regulatory harmonization creates consistent market conditions across the EU. EcoDesign requirements establish quality baselines that eliminate substandard products. Energy labeling standards support informed purchasing decisions. The circular economy emphasis requires manufacturers to demonstrate product recyclability and component recovery capabilities. Extended producer responsibility regulations generate compliance costs. Manufacturers gain competitive advantages through comprehensive take-back and refurbishment programs. European markets prefer high-quality, long-lifespan products over low-cost alternatives.

North America LED Tube Market Trends

North America is anticipated to maintain a strong position in the market for LED tubes through 2033, with the United States accounting for the majority of regional demand due to stringent DOE efficiency standards. Aging fluorescent lighting infrastructure across commercial buildings requires systematic replacement, which is reinforcing consistent retrofit activity. State-level regulations, including California’s Title 24 building energy efficiency standards, are mandating compliance-driven upgrades regardless of short-term economic cycles. Facility managers are therefore executing planned replacement programs to meet regulatory deadlines and avoid financial penalties. Commercial property operators are increasingly standardizing LED specifications across portfolios to simplify compliance management, control operating costs, and ensure uniform performance across assets.

The regional market is also benefiting from a mature innovation ecosystem that is supporting advanced product development and value-added adoption. Leading manufacturers are investing in smart lighting systems and human-centric lighting applications to meet evolving performance expectations. High concentrations of corporate headquarters are driving demand for premium, specification-driven solutions aligned with Leadership in Energy and Environmental Design (LEED) and WELL Building Standard certification requirements. As market maturity is increasing, incremental growth is shifting toward industrial applications such as cold storage warehouses and data centers that require specialized high-bay LED configurations. Competitive intensity remains high, with global players operating alongside domestic suppliers serving niche requirements. Well-developed distribution networks are enabling end-to-end retrofit execution through electrical wholesalers and integrated facility services providers, while investment activity is increasingly favoring technology acquisitions and the expansion of LED-as-a-service financing models.

Competitive Landscape

The global LED tube market exhibits a moderately fragmented structure, with leading players including Signify, Acuity Brands, Panasonic Corporation, Toshiba Lighting & Technology Corporation, and Cree Lighting. Collectively, these companies are accounting for approximately 40% to 45% of total market revenue, reflecting a balance between global scale leaders and a broad base of regional and specialized manufacturers. Market competition remains dynamic, as established firms defend their market share through brand strength, extensive distribution networks, and long-standing relationships with commercial and industrial customers. From a consumer standpoint, these dynamics enable and ensure product availability and price competition while maintaining acceptable quality and compliance standards.

Competitive differentiation is increasingly being driven by continuous technological advancement and sustained investment in innovation. Leading manufacturers are allocating significant resources to research and development activities that deliver higher energy efficiency, improved lumen output, and longer operational lifespans. Product development is increasingly integrating capabilities such as smart lighting controls, wireless connectivity, and advanced thermal management systems to enhance reliability and system intelligence. In parallel, key players are forming strategic partnerships to accelerate the adoption of new technologies, while mergers and acquisitions are expanding product portfolios and strengthening regional distribution. These initiatives reinforce competitive positioning and enable market leaders to maintain relevance across diverse geographies, regulatory environments, and end-user segments.

Key Industry Developments

- In November 2025, EarthTronics launched a 4’ T8 LED Linear Lamp delivering 1700 lumens at 10.5W, with 4000K/5000K options, CRI 82, 50,000-hour life, and direct-wire installation without ballast. It features a 300° beam angle, glass construction for even light, UL/DLC listed, damp/dry rated, and a 5-year warranty, ideal for retrofits in schools, offices, and retail.

- In November 2025, Nanlite unveiled the PavoTube II 6CP, an upgraded compact 10-inch RGB LED tube light weighing 267g, featuring 10% brighter output, a 3200mAh battery for 30% longer runtime, and an extended 2400-12,000K CCT range with ±150 green/magenta adjustment via the new Nebula C4 engine.

- In June 2025, Evluma and LED Roadway Lighting announced a collaboration combining products, technology, and engineering expertise to advance outdoor LED lighting innovation. The partnership leverages complementary strengths for smarter, sustainable street and area lighting solutions, expanding market reach without disrupting operations.

Companies Covered in LED Tube Market

- Koninklijke Philips N.V.

- Acuity Brands, Inc.

- IDEAL INDUSTRIES, INC.

- Eaton Corporation

- SAVANT TECHNOLOGIES LLC.

- OSRAM Gmbh

- Seoul Semiconductor

- Zumtobel Group

- Bajaj Electricals

- Wipro Ltd

- NEPTUN lights Inc.

- Havells

- Syska

- Foshan Electrical and Lighting Co., Ltd

- LED Tube Lighting Pty. Ltd.

- Panasonic Corporation

- Opple Lighting Co., Ltd.

- Crompton Greaves Consumer Electricals Limited.

- HPL Electric & Power Ltd

- Toshiba Ltd

Frequently Asked Questions

The global LED tube market is projected to reach US$ 8.1 billion in 2026.

Stringent energy efficiency regulations, declining manufacturing costs, and continuous technological improvements are propelling market expansion.

The market is poised to witness a CAGR of 10% from 2026 to 2033.

Smart lighting integration, emerging market infrastructure development, and ESG-driven corporate procurement are creating substantial growth potential.

Signify N.V., Acuity Brands, Inc., Panasonic Corporation, Toshiba Lighting & Technology Corporation and Cree Lighting are some of the key players in the market.