- Metals & Minerals

- Lead Sulphide Market

Lead Sulphide Market Size, Share, and Growth Forecast 2026 – 2033

Global Lead Sulphide Market by Purity (82% Purity, 90% Purity, and 99% Purity), Application (Spectroscopic Study, Photo Optic, Slip Property Modifier, Infrared Detectors, and Semiconductor), and Regional Analysis

Lead Sulphide Market Size and Share Analysis

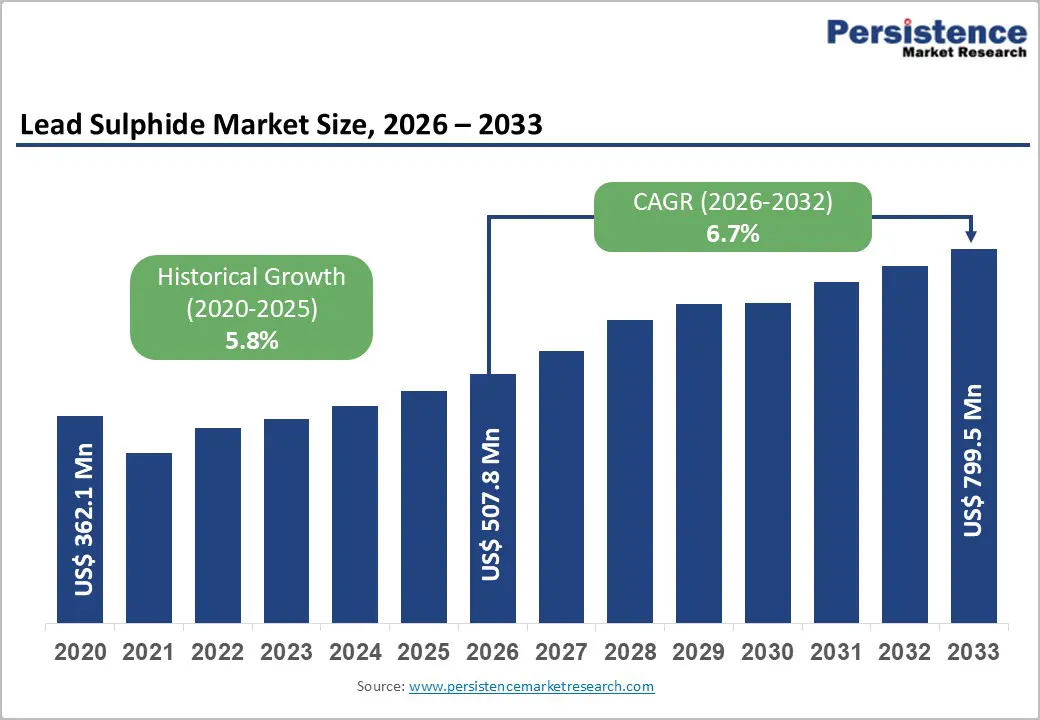

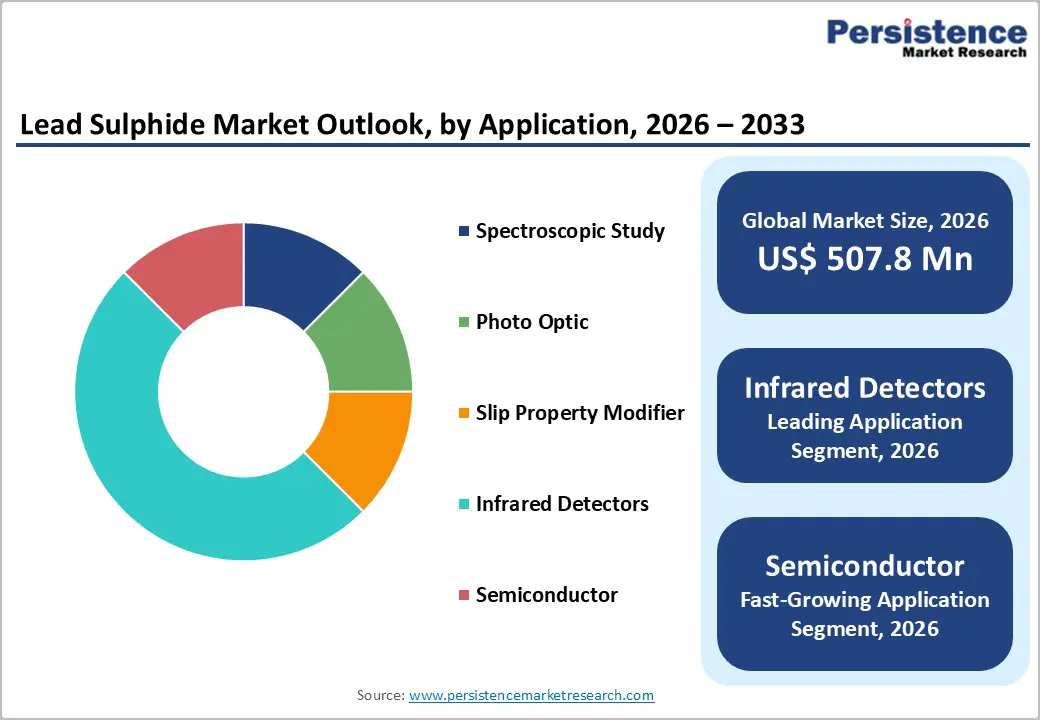

The global lead sulphide (PbS) market size was valued at US$ 507.8 Mn in 2026 and is projected to reach US$ 799.5 Mn by 2033, growing at a CAGR of 6.7% between 2026 and 2033. The market expansion is driven by exponential growth in infrared detector applications across defense, security, automotive, and scientific research sectors requiring advanced thermal imaging and night vision capabilities, accelerating research into quantum dot technology and nanomaterial development leveraging lead sulphide's tunable band gap and strong infrared absorption properties, and increasing adoption of sophisticated sensor systems across aerospace, industrial monitoring, and medical diagnostic applications.

Key Market Highlights

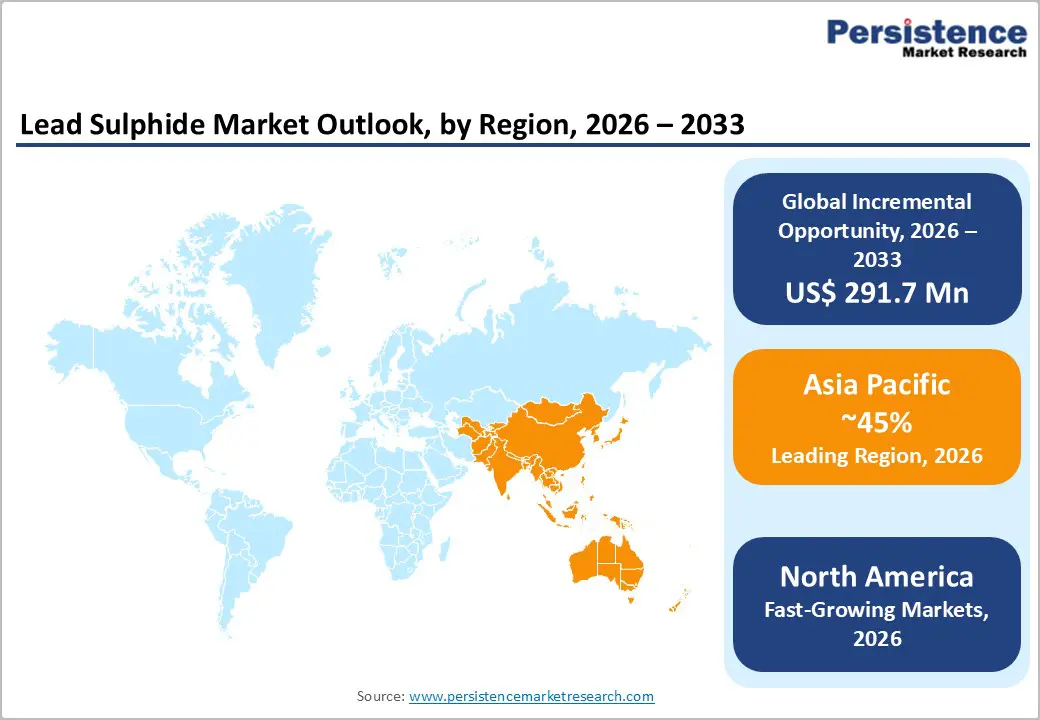

- Leading Region: Asia Pacific dominates the global lead sulphide market with commanding 45% market share, anchored by China's semiconductor manufacturing dominance, Japanese precision electronics expertise, and India's expanding research sector, establishing the region as primary demand driver for lead sulphide materials and applications.

- Fastest Growing Country: China and emerging Asia Pacific nations experience fastest growth within the region at 8.8% CAGR through 2033, propelled by government renewable energy policies, quantum dot research expansion, photovoltaic technology advancement, and rising industrial infrastructure development supporting sustained regional demand acceleration.

- Dominant Purity: 90% purity lead sulphide dominates the product category, commanding approximately 55% market share, driven by optimal cost-performance balance supporting broad-based commercial applications, established production infrastructure, and proven quality assurance protocols enabling widespread industrial adoption.

- Growing Application: Semiconductor and photovoltaic applications represent the fastest-growing segment, experiencing 7.8% CAGR through 2033, propelled by quantum dot technology advancement, solar cell efficiency improvement research, emerging wearable electronics applications, and government renewable energy development support.

- Key Market Opportunity: Quantum dot technology commercialization and photovoltaic solar cell development represent exceptional growth opportunities, with emerging manufacturing scale-up initiatives, research partnership acceleration, and government renewable energy incentives establishing substantial demand potential for specialized lead sulphide quantum dot materials.

| Report Attribute | Details |

|---|---|

|

Global Lead Sulphide Market Size (2026E) |

US$ 507.8 Mn |

|

Market Value Forecast (2033F) |

US$ 799.5 Mn |

|

Projected Growth CAGR(2026-2033) |

6.7% |

|

Historical Market Growth (2020-2025) |

5.8% |

Market Dynamics

Market Growth Drivers

Accelerating Infrared Detector Demand Across Defense, Security, and Thermal Imaging Applications

Infrared detector technology represents the dominant application segment for lead sulphide, commanding approximately 40-45% of total market consumption, driven by exponential growth in defense and security applications requiring advanced thermal imaging and night vision capabilities. Global infrared detector market expansion at 7.1% CAGR through 2035 is establishing substantial demand drivers for specialized photon detector materials including lead sulphide, which demonstrates superior performance characteristics for mid-infrared detection between 1-3 micrometer wavelengths. Military and aerospace applications including night vision systems, thermal imaging equipment, and tactical surveillance platforms extensively utilize lead sulphide-based infrared detectors for superior sensitivity and room-temperature operational capability.

Automotive advanced driver assistance systems (ADAS) and motion sensing applications are experiencing exceptional growth, with manufacturers standardizing infrared detector integration for pedestrian detection, collision avoidance, and safety feature enhancement. Security and surveillance sector expansion across government installations, commercial facilities, airports, and critical infrastructure is generating sustained demand for infrared detectors incorporating lead sulphide technology. The compound's exceptional mid-infrared sensitivity and compact design create competitive advantages supporting continued market dominance throughout the forecast period.

Advanced Semiconductor and Quantum Dot Technology Development Expansion

Emerging research into semiconductor applications including quantum dot technology and photovoltaic cell development is establishing substantial growth opportunities for lead sulphide-based materials, driven by the compound's tunable band gap enabling electronic property control through nanoparticle size manipulation. Lead sulphide quantum dots demonstrate exceptional absorption coefficients and size-dependent optical properties, with emission wavelengths ranging from 900-1600 nanometers covering significant portions of the near-infrared spectrum valuable for photovoltaic applications. Academic and commercial research institutions are systematically investigating lead sulphide nanoparticle synthesis methodologies enabling precise control of morphologies and electronic characteristics for solar cell efficiency improvement and photodetection sensitivity enhancement.

Published research demonstrates that lead sulphide quantum dot size variation between 2.5-8 nanometers enables targeted modification of energy band gaps accommodating diverse application requirements. The strong absorption properties across the infrared spectrum position lead sulphide as valuable material for next-generation photovoltaic systems targeting far-infrared radiation absorption capability. Ongoing research advancement combined with commercialization pathways for quantum dot-based devices establishes sustained momentum supporting market expansion beyond traditional detector applications.

Market Restraints

Lead Toxicity Concerns and Environmental Regulation Constraints

Lead sulphide materials inherently contain toxic lead elements creating substantial regulatory compliance challenges and environmental disposal constraints limiting market penetration in certain application segments. Stringent environmental regulations governing lead-containing materials impose manufacturing restrictions, handling protocols, and waste disposal requirements increasing production costs and operational complexity compared to alternative detector technologies.

Health and safety regulations across developed markets require specialized handling procedures, worker protection measures, and decontamination protocols for lead sulphide manufacturing facilities, creating significant capital and operational expense burdens. International regulations including Basel Convention restrictions governing lead-containing material transportation and disposal are constraining supply chain logistics and manufacturing location flexibility. Environmental consciousness among end-user industries is driving adoption of alternative photon detector technologies including indium gallium arsenide (InGaAs) and mercury cadmium telluride (MCT) which avoid lead-related regulatory complications.

Competition from Alternative Infrared Detector Technologies and Material Substitution

Competing infrared detector technologies including InGaAs, mercury cadmium telluride (MCT), quantum well-infrared photodetectors (QWIP), and microbolometer designs are capturing increasing market share through superior performance characteristics, reduced regulatory constraints, and continuous cost reductions from manufacturing scale. Thermal microbolometer detectors are experiencing exceptional market growth through superior cost-effectiveness, integration compatibility, and uncooled operation capability reducing system complexity compared to cooled detector systems.

Alternative photon detectors are demonstrating improved spectral coverage, sensitivity levels, and temperature stability characteristics potentially displacing traditional lead sulphide applications in emerging application segments. Research and development investments directed toward competitor technologies are reducing technology maturity gaps and enabling performance parity achievement reducing lead sulphide's competitive advantages.

Market Opportunities

Quantum Dot Advancement and Next-Generation Photovoltaic Development

Quantum dot technology represents an exceptional growth opportunity for lead sulphide materials, driven by research demonstrating exceptional promise for solar cell efficiency improvement and photovoltaic device performance enhancement. Size-tunable band gap engineering through nanoparticle morphology control enables development of customized electronic properties optimizing performance across diverse photovoltaic applications. Lead sulphide quantum dots with tunable band gaps ranging from 2.15 to 3.11 electron volts demonstrate exceptional versatility for colloidal quantum dot solar cell development.

Research institutions and commercial enterprises are establishing quantum dot manufacturing partnerships and collaborative development initiatives accelerating commercialization timelines for quantum dot-based devices. Government incentives supporting renewable energy development are creating favorable market conditions for photovoltaic technology advancement where lead sulphide quantum dots offer tunable optical absorption and strong infrared sensitivity. Emerging markets for wearable electronics, portable imaging systems, and flexible electronics represent expanding application domains where compact quantum dot-based detectors deliver measurable performance advantages.

Photocatalytic Applications and Environmental Remediation Market Expansion

Lead sulphide nanoparticles are demonstrating exceptional potential for photocatalytic environmental remediation applications, with published research confirming photocatalytic efficiencies ranging from 28.3% to 60.0% for organic pollutant degradation in contaminated wastewater. Hexadecylamine-capped lead sulphide nanoparticles have demonstrated capability to catalyze methylene blue dye degradation under ultraviolet irradiation, establishing proof-of-concept for wastewater treatment and industrial effluent cleanup applications. Global wastewater treatment market expansion driven by stringent environmental regulations and expanding municipal infrastructure requirements is generating incremental demand for specialized photocatalytic materials.

Emerging markets in Asia Pacific experiencing rapid industrialization and requiring enhanced environmental protection technologies present substantial demand growth opportunities for advanced photocatalytic materials including lead sulphide. Custom synthesis and functionalization capabilities enabling targeted photocatalytic performance optimization are establishing high-margin specialty chemical business opportunities for suppliers possessing advanced materials science expertise. Government policies emphasizing sustainable industrial practices and circular economy principles are accelerating adoption of advanced catalytic technologies addressing environmental contamination challenges.

Category-wise Insights

Purity Analysis

The 90% purity segment commands market leadership, accounting for approximately 55% of total lead sulphide market share, driven by optimal balance between cost-effectiveness and performance characteristics supporting broad-based application deployment across commercial sectors. Standard-grade 90% purity materials demonstrate exceptional performance adequacy for the predominant infrared detector applications where ultimate electronic property perfection is unnecessary. Manufacturing economics favor 90% purity production through simplified purification methodologies reducing production costs significantly compared to high-purity 99% alternatives, enabling competitive market pricing supporting volume-based demand expansion.

Quality assurance protocols and regulatory compliance pathways are well-established for 90% purity standards, enabling rapid product qualification and commercialization. Established supply chain relationships and production infrastructure optimization around the 90% purity segment create competitive advantages for established suppliers. Research applications and commercial product development consistently utilize 90% purity materials, establishing baseline demand supporting sustained segment growth.

Application Analysis

Infrared detector applications command market dominance, accounting for approximately 45% of total lead sulphide consumption, driven by irreplaceable functional requirements for mid-infrared radiation detection and thermal imaging applications. Military and defense sector applications including night vision systems, thermal surveillance equipment, and tactical imaging platforms represent primary volume drivers utilizing lead sulphide's exceptional mid-infrared sensitivity and compact design. Automotive security and advanced driver assistance systems (ADAS) are experiencing rapid adoption expansion, with manufacturers integrating infrared detectors for pedestrian detection, collision avoidance, and advanced safety features. Aerospace applications including aircraft thermal management monitoring and environmental sensing extend infrared detector applications across high-reliability domains.

Semiconductor applications represent the fastest-growing lead sulphide segment, experiencing growth rates exceeding 7.8% CAGR through 2033, driven by accelerating quantum dot research and emerging photovoltaic device commercialization. Lead sulphide nanoparticles and quantum dots are demonstrating exceptional promise for solar cell efficiency enhancement, with research confirming tunable band gap characteristics enabling optimized electronic properties for photovoltaic applications. Quantum dot-based solar cells leverage lead sulphide's strong infrared absorption capability enabling higher energy density harvesting compared to conventional silicon photovoltaic materials. Commercial development initiatives are establishing manufacturing scale-up pathways for quantum dot production, positioning segment for exponential growth during 2025-2033 forecast period.

Regional Insights

North America Lead Sulphide Trends

North America represents a significant lead sulphide market, commanding approximately 25-30% of global demand, with the United States maintaining market leadership through world-class research institutions, military and defense sector requirements, and established aerospace industry presence. U.S. government military and defense applications generate substantial sustained demand for infrared detection systems incorporating lead sulphide technology, with classified defense programs driving confidential procurement of specialized detector components. American research institutions at MIT, Stanford, and CalTech are conducting advanced research into quantum dot technology and photovoltaic applications, establishing intellectual property foundations supporting domestic materials supplier competitive positioning.

Aerospace applications across commercial aviation, military aircraft, and space programs require sophisticated thermal imaging and infrared sensing equipment standardizing lead sulphide incorporation in critical system designs. Automotive manufacturers are rapidly expanding infrared detector integration across ADAS and safety system platforms, generating incremental lead sulphide consumption growth.

Europe Lead Sulphide Trends

Europe represents a significant lead sulphide market, commanding approximately 25% of global demand, with Germany maintaining technology and materials science leadership through renowned research institutions and world-class semiconductor manufacturing. European research organizations and specialized equipment manufacturers are investigating advanced infrared detector applications and quantum dot technology development establishing innovation centers for next-generation device development.

Regulatory environment harmonization across European Union member states regarding lead-containing materials management is creating standardized compliance frameworks supporting manufacturing operations. Security and surveillance sector expansion across European cities and critical infrastructure is driving infrared detector adoption for smart city initiatives and public safety applications. Aerospace and defense applications across NATO member states maintain sustained demand for specialized infrared detector systems incorporating lead sulphide technology.

Asia Pacific Lead Sulphide Trends

Asia Pacific represents the fastest-growing regional market for lead sulphide, experiencing growth rates substantially exceeding developed market expansion, with 45% of global lead sulphide demand and projected CAGR exceeding 7% through 2033. China dominates regional manufacturing and consumption, leveraging extensive semiconductor production infrastructure and quantum dot research capabilities positioning the nation as global technology innovation center. Japanese precision manufacturing excellence maintains steady demand for high-purity lead sulphide materials supporting advanced electronic and photovoltaic applications.

India's emerging semiconductor and research sectors are establishing growing consumption of lead sulphide materials for scientific research and technology development initiatives. Southeast Asian nations are experiencing accelerating industrial expansion and infrastructure development, creating incremental demand for infrared sensing and surveillance technologies. Government policies supporting renewable energy development and photovoltaic technology advancement across Asia Pacific are establishing favorable market conditions for quantum dot-based solar cell commercialization.

Competitive Landscape for the Lead Sulphide Market

The lead sulphide market exhibits a moderately consolidated competitive structure dominated by established specialty chemical manufacturers and global life science suppliers with comprehensive distribution capabilities and technical support. Tier 1 companies including MilliporeSigma (Merck), American Elements, and Otto Chemie collectively command approximately 50-60% market share through established brand recognition, extensive product portfolios, and global customer relationships. MilliporeSigma/Merck, the market leader with 26.1% click share prominence, maintains dominance through comprehensive chemical catalog, technical literature support, and quality assurance certifications.

American Elements and Xi'an Function Material Group manage approximately 17.4% click share each, differentiating through specialized production capabilities and cost competitiveness. Emerging suppliers including Ereztech, Alfa Chemistry, and Stanford Advanced Materials are establishing competitive positions through focused technology development and emerging application specialization. Vertical integration strategies linking suppliers to research institutions and manufacturing partners are establishing long-term collaboration relationships supporting market expansion.

Key Market Development

- In 2024, Research institutions published comprehensive findings on single-source precursor synthesis pathways enabling controlled morphology lead sulphide nanoparticle production, establishing manufacturing foundations for scalable quantum dot commercialization. The research confirms feasibility of size-tunable band gap engineering supporting customized photovoltaic application development.

- In 2024, Research and development partnerships between materials suppliers and photovoltaic manufacturers announced manufacturing scale-up initiatives for lead sulphide quantum dot-based solar cells, establishing commercialization pathways for next-generation photovoltaic devices.

- In 2023, Academic publications documented lead sulphide nanoparticle photocatalytic efficacy achieving 60% degradation efficiency for organic pollutants in wastewater, establishing proof-of-concept for environmental cleanup applications. The findings position lead sulphide as viable material for emerging photocatalytic technology market expansion.

Companies Covered in Lead Sulphide Market

- Chem Service HUSHI

- American Elements

- Chem Service

- Strem Chemicals Inc.

- CHEM-IMPEX

- ProChem Inc

- APOLLO

- Aladdin

- Achemica

- OKA

- Sigma-Aldrich

- Stanford Advanced Materials

- BeanTown Chemical

- Noah Technologies Corporation

- ESPI Metals

Frequently Asked Questions

The global Lead Sulphide Market is projected to reach US$ 799.5 million by 2033, expanding from US$ 507.8 million in 2025 at a CAGR of 6.7%, driven by infrared detector demand growth, quantum dot technology advancement, semiconductor application expansion, and emerging photovoltaic cell development supporting sustained market growth through the forecast period.

Market demand growth is driven by multiple converging factors including exponential growth in infrared detector applications across defense, security, and automotive sectors; accelerating quantum dot research for photovoltaic applications; semiconductor advancement requiring specialized materials; global infrared detector market expansion; and emerging photocatalytic applications for environmental remediation supporting diverse demand pathways.

Infrared detector applications represent the dominant segment, commanding approximately 45% market share, driven by critical functionality requirements for mid-infrared radiation detection in 1-3 micrometer wavelengths, military and defense applications, automotive ADAS systems, and aerospace thermal imaging requirements where lead sulphide demonstrates superior performance.

Asia Pacific commands market leadership with approximately 45% global lead sulphide demand, anchored by China's semiconductor manufacturing dominance, Japanese precision electronics expertise, India's expanding research sector, and emerging Southeast Asian industrial expansion establishing the region as primary demand driver.

Major market opportunities include quantum dot technology commercialization for solar cell applications; photovoltaic device development leveraging tunable band gap engineering; photocatalytic environmental remediation achieving 60% degradation efficiency; emerging wearable electronics applications; and government renewable energy incentives supporting quantum dot-based solar cell market expansion.

Leading market players include MilliporeSigma/Merck KGaA commanding global market leadership through comprehensive product portfolios and technical support; American Elements offering specialized high-purity materials and global manufacturing presence; Otto Chemie Pvt. Ltd. leveraging cost-effective production and regional market expertise; Xi'an Function Material Group and Stanford Advanced Materials providing specialized capabilities supporting diverse application requirements.