- Medical Devices

- Leadless Pacing System Market

Leadless Pacing System Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Leadless Pacing System Market by Product (Single-chamber leadless pacemakers, Dual-chamber leadless pacemakers, Leadless cardiac resynchronization therapy (CRT) systems, Others), Indication (Atrial Fibrillation, Sinus Node Dysfunction, Atrioventricular Block, Others), End-user (Hospitals, Ambulatory surgical centers, Others), and Regional Analysis from 2026 - 2033

Leadless Pacing System Market Share and Trends Analysis

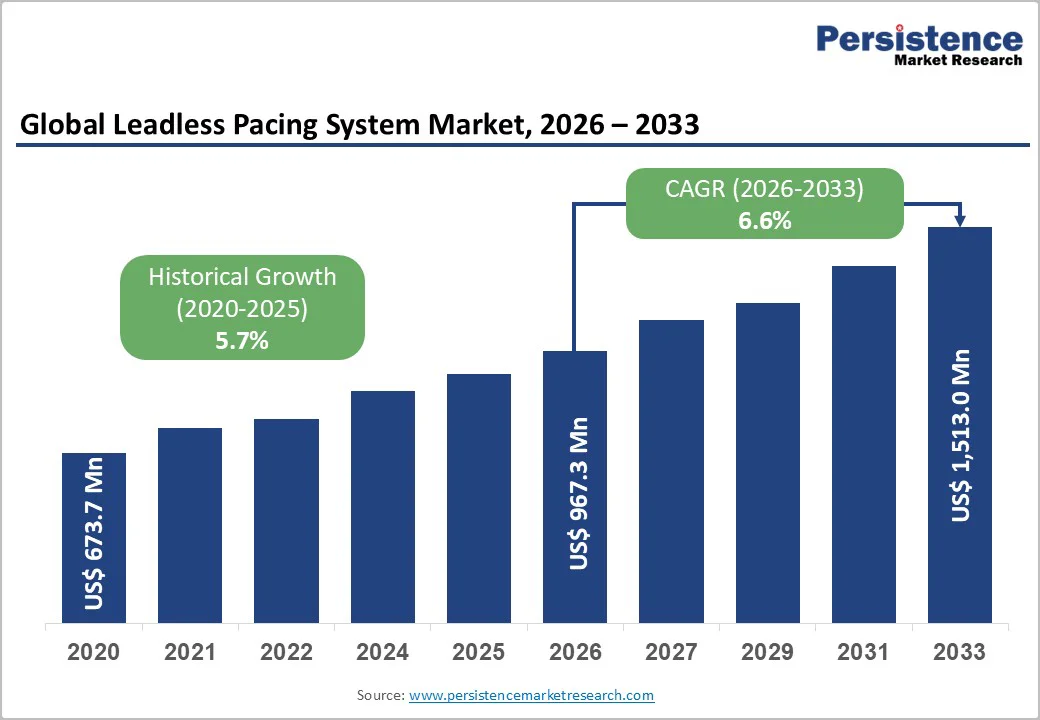

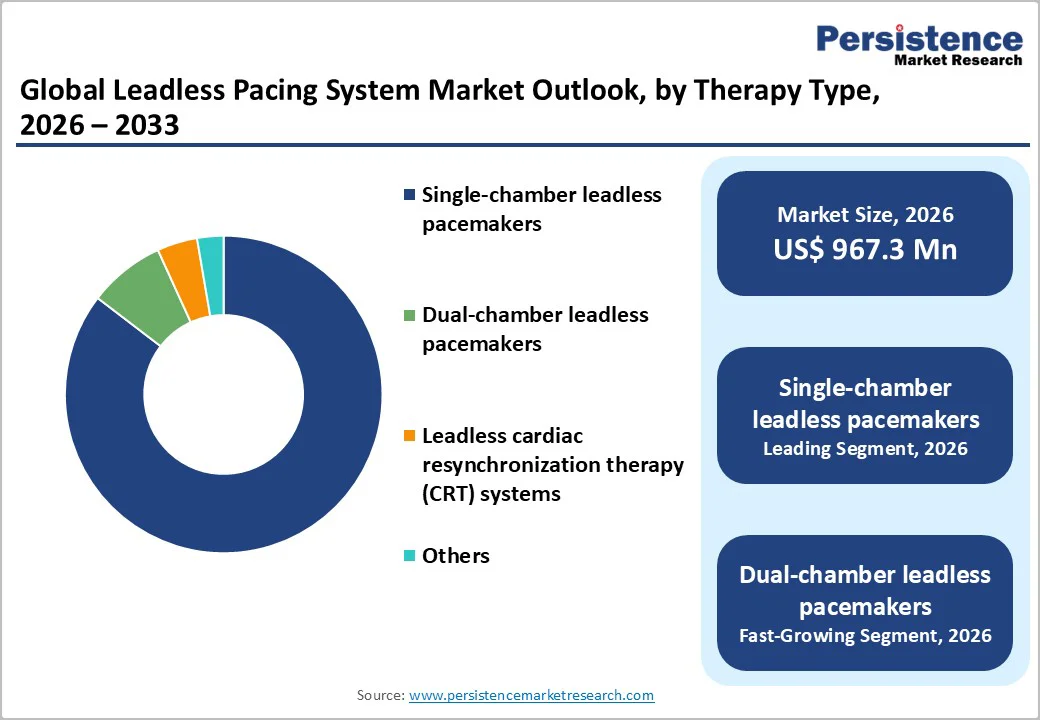

The global leadless pacing system market is projected to be valued at US$967.3 million in 2026 and to reach US$1,513.0 million by 2033, growing at a CAGR of 6.6% from 2026 to 2033.

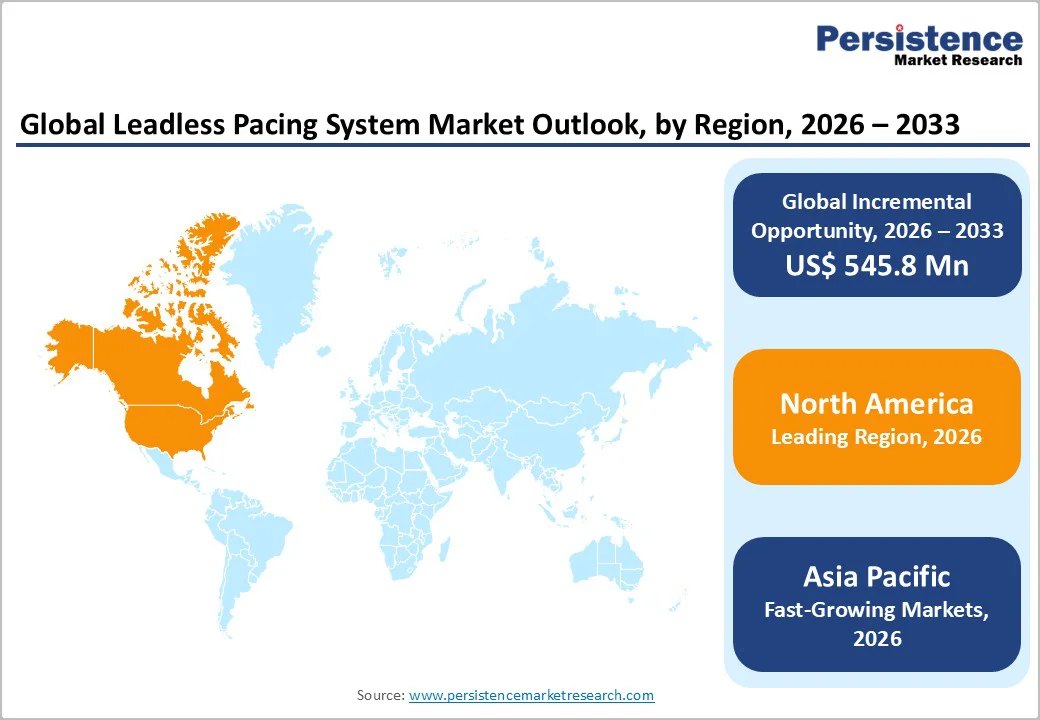

The leadless pacing system industry is expanding rapidly, driven by rising cases of bradycardia, demand for minimally invasive cardiac therapies, and reduced lead-related complications. North America leads due to high device adoption, strong reimbursement, and advanced electrophysiology centers. The Asia-Pacific region is the fastest-growing, driven by increasing cardiac procedure volumes, improved healthcare access, and expanding adoption of next-generation leadless devices.

Key Industry Highlights:

- Dominant Segment: Single-chamber leadless pacemakers dominate the 2025 market, accounting for 85.4% share, supported by proven safety, broad clinical acceptance, simpler implantation, and strong reimbursement. Dual-chamber leadless systems are the fastest-growing due to expanded indications and physiologic pacing benefits, while leadless CRT remains niche but promising for complex cardiac cases.

- Dominant Region: North America leads with a 42.3% share driven by advanced electrophysiology labs, strong reimbursement, early adoption of dual-chamber devices, and high bradycardia procedure volumes. Europe follows with robust cardiology networks, while Asia-Pacific is the fastest-growing region due to rising cardiac cases, expanding EP labs, and increasing access to next-generation leadless pacemakers.

- Growth Indicator: Growth is fueled by rising prevalence of bradycardia, increasing preference for minimally invasive, lead-free pacing, reduced infection and lead-related complications, technological advances in device longevity and atrial-ventricular synchrony, a growing elderly population, and expanding adoption of dual-chamber and MRI-compatible leadless systems in EP practices.

- Market Opportunity: Key opportunities include rapid expansion of dual-chamber and future multi-chamber leadless systems, wireless cardiac resynchronization innovations, miniaturized longer-life batteries, remote monitoring integration, value-tier devices for emerging markets, and partnerships with cardiology centers to penetrate high-growth indications such as AV block, sick sinus syndrome, and post-TAVR pacing.

| Key Insights | Details |

|---|---|

|

Leadless Pacing System Market Size (2026E) |

US$ 967.3 Mn |

|

Market Value Forecast (2033F) |

US$ 1,513.0 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

6.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.7% |

Market Dynamics

Driver - Rising prevalence of bradycardia and conduction disorders

Heart-rhythm and conduction disorders are increasingly prevalent, driving demand for leadless pacing systems. Studies indicate that overall conduction disorders affect approximately 15–27% of adults, with new cases occurring at around 0.6% per year. Among adults aged 65–73 years, about 4.8% have rhythm abnormalities, with age-related bradyarrhythmias and atrioventricular conduction blocks being particularly common. Globally, bradycardia prevalence, including sinus-node dysfunction and AV blocks, is estimated between 0.5% and 2%, though underdiagnosis suggests the true burden is higher.

Aging populations, coupled with increasing comorbidities such as hypertension, diabetes, and heart disease, further elevate the risk of conduction disorders, expanding the pool of patients requiring cardiac pacing. Leadless pacemakers offer a minimally invasive, lead-free solution that reduces risks associated with traditional transvenous devices, including infections and lead fractures. As awareness grows and more patients are diagnosed, the rising prevalence of bradycardia and conduction disorders is a major driver for the adoption and growth of the leadless pacing system market.

Restraints - Limited clinical experience and adoption

Although over 150,000 leadless pacemakers have been implanted globally, they represent only a small fraction of total pacemaker procedures, reflecting limited clinical experience and adoption. Surveys of electrophysiology centers indicate that 31% do not implant leadless devices at all, and 59% perform fewer than 20 leadless pacemaker implants annually. Key barriers include high device costs, limited atrial pacing capability in many systems, and limited tools for device retrieval or replacement. Most published data on leadless pacemakers come from trials and small cohort studies involving around 2,500 patients, with relatively short follow-up periods.

Long-term outcomes, including device retrieval, generator replacement, and complication rates over decades, remain under-documented. Consequently, many cardiologists and hospitals continue to rely on conventional transvenous pacemakers due to familiarity and established protocols. This limited clinical experience and cautious adoption by physicians acts as a significant restraint, slowing broader market penetration and adoption of leadless pacing systems despite their clinical advantages.

Opportunity - Expansion of dual-chamber and multi-chamber leadless devices

The advent of dual-chamber leadless pacemakers has transformed leadless pacing from a niche to a mainstream approach. In a recent study of the novel system, with two wireless leadless devices implanted in the right atrium and right ventricle, the implantation success rate was 98.3% among 300 patients, with atrioventricular (AV) synchrony achieved in 97.3%. Procedural safety and pacing performance exceeded predefined goals, showing that dual-chamber leadless pacing can safely and effectively reproduce physiological pacing.

Given that traditionally around 30–40% of pacemaker patients require dual-chamber pacing (rather than single-chamber), this new capability dramatically expands the eligible patient pool. Moreover, by eliminating leads and generator pockets, leadless multi-chamber systems retain the infection and lead-related complication benefits of single-chamber LPMs. Together, these advances open a substantial growth pathway as more patients, previously excluded from leadless pacing, become eligible.

Category-wise Analysis

By Product, Single-chamber leadless pacemakers Dominates the Leadless Pacing System Market

Single-chamber leadless pacemakers accounts for 85.4% share of the global market in 2025, because most pacing indications, such as atrioventricular block and ventricular bradycardia, require only ventricular pacing. Approximately 68% of new pacemaker implants are single-chamber devices, while around 30% are dual-chamber. Leadless technology initially targeted single-chamber patients, capturing the largest eligible population. These devices are compact, simpler to implant, and eliminate leads and pocket-related complications, reducing procedural risks and recovery time. Additionally, many patients do not require atrial pacing, making single-chamber systems sufficient for effective therapy. The combination of broad clinical applicability, procedural ease, and safety advantages ensures that single-chamber leadless pacemakers retain the largest market share compared with dual-chamber and multi-chamber systems, solidifying their dominance in current global adoption.

By End-user, Hospitals is gaining traction due to advanced infrastructure, monitoring, specialized staff, and procedural safety

Hospitals dominate the leadless pacing system market with 72.7% share in 2025, because they provide the comprehensive cardiac infrastructure, electrophysiology labs, advanced imaging support, and 24/7 monitoring required for safe implantation and post-procedure care. Data from recent years show that nearly 98% of leadless pacemaker implants occur in hospital settings, with only about 2% performed outside hospitals. Additionally, by 2023, roughly 7% of all pacemaker implantations, including traditional devices, were performed in ambulatory surgical centers, while the majority were conducted in hospital inpatient or outpatient departments. The specialized nature of leadless systems, along with the need for immediate management of potential complications, makes hospitals the preferred and dominant end-user segment, ensuring safety, procedural efficiency, and optimal patient outcomes.

Regional Insights

North America Leadless Pacing System Market Trends

North America dominates the leadless pacing system market with 42.3% share in 2025, because of its well-established cardiac infrastructure, high pacemaker implantation rates and rapid uptake of new pacing technologies. In the U.S., over 200,000 pacemaker implants are performed annually, representing more than one-quarter of global implants. A substantial share of these are increasingly switching to leadless systems as hospitals adopt advanced cardiac rhythm-management devices.

In 2024, North America held roughly 50% of the global leadless pacemaker market share, reflecting early adoption, favorable reimbursement frameworks, and widespread access to cardiac care. With an aging population and high prevalence of conduction disorders, demand remains strong, making North America the predominant region for leadless pacemaker use.

Europe Leadless Pacing System Market Trends

Europe is an important region in the leadless pacing system market due to its high baseline demand for pacemakers and increasing adoption of advanced technologies. In Western European countries, pacemaker implantation rates exceed 100 per 100,000 population annually, reflecting a substantial patient pool. Leadless pacemaker use is rising rapidly, with some countries reporting an 18% year-on-year increase in implants. Surveys of electrophysiology centers indicate that approximately 86% of hospitals have experience with leadless devices, demonstrating broad clinical readiness and familiarity. Combined with strong healthcare infrastructure, favorable reimbursement policies, and growing awareness of leadless system benefits, Europe represents a critical market for expansion and innovation in leadless pacing, offering both stable demand and high potential for adoption of new technology.

Asia-Pacific Leadless Pacing System Market Trends

The Asia-Pacific region is the fastest-growing for the leadless pacing system market due to its rapidly rising cardiovascular disease burden and expanding healthcare infrastructure. By 2050, the number of individuals affected by cardiovascular disease in Asia is projected to reach nearly 730 million, more than double the 2025 figures. Heart failure and arrhythmia prevalence is also high, with age-standardized rates ranging from approximately 212 to over 1,030 per 100,000 across the region. Pacemaker implantation is rising, particularly in Japan, China, and India, reflecting growing adoption of cardiac rhythm management therapies. Coupled with an aging population, increasing arrhythmia incidence, and improving access to advanced cardiac care, demand for leadless pacemakers in the Asia-Pacific region is accelerating, making it the fastest-growing regional market globally.

Competitive Landscape

Leading companies in the leadless pacing system market focus on innovative, minimally invasive devices, reliability, and safety. They invest in single- and dual-chamber technologies, improve battery life and device performance, and collaborate with hospitals. R&D emphasizes procedural simplicity, patient safety, and cost-effectiveness, supporting broader adoption across AV block, sinus node dysfunction, and bradyarrhythmia treatments globally.

Key Industry Developments:

- In October 2025, Healthcare major Abbott launched its dual-chamber leadless pacemaker system, marking a significant advancement in cardiac rhythm management. The new system enables atrioventricular synchronized pacing without traditional leads, reducing procedural complications and improving patient outcomes.

- In May 2024, The MODULAR ATP study of the mCRM™ System successfully met its primary safety and efficacy endpoints, demonstrating the system’s reliable performance in clinical use. The results confirmed that the device provides effective antitachycardia pacing while maintaining a strong safety profile, supporting its potential adoption in managing patients with cardiac arrhythmias.

- In January 2024, Medtronic received CE Mark approval for its next-generation Micra leadless pacing systems, allowing the devices to be marketed across Europe. The new systems offer enhanced features, improved battery life, and advanced pacing capabilities, strengthening Medtronic’s position in the leadless pacemaker market and expanding treatment options for patients with bradycardia and conduction disorders.

Companies Covered in Leadless Pacing System Market

- Medtronic plc

- Abbott Laboratories

- Boston Scientific Corporation

- EBR Systems, Inc.

- Biotronik SE & Co. KG

- Osypka AG / Osypka Medical GmbH

- Shree Pacetronix Ltd.

- Others

Frequently Asked Questions

The global leadless pacing system market is projected to value at US$ 967.3 Mn in 2026.

Rising bradycardia prevalence, aging populations, minimally invasive procedures, reduced complications, technological advancements, and increasing awareness drive market growth globally.

The global leadless pacing system market is poised to witness a CAGR of 6.6% between 2026 and 2033.

Expansion of dual and multi-chamber devices, emerging Asia-Pacific markets, outpatient adoption, AI integration, cost reduction, and post-market service enhancements offer growth opportunities.

Medtronic plc, Abbott Laboratories, Boston Scientific Corporation, EBR Systems, Inc., Biotronik SE & Co. KG, OSYPKA MEDICAL.