- LED & Lighting (Optoelectronics)

- Laser Processing Market

Laser Processing Market Size, Share, and Growth Forecast, 2026 - 2033

Laser Processing Market by Product Type (Gas Lasers, Solid-state Lasers, Fiber Lasers and Others), by Process type (Material Processing, Marking and Engraving and Micro-Processing), by End-use (Automotive, Aerospace, Machine Tools, Electronics and Microelectronics, Medical, and Packaging), and Regional Analysis for 2026 - 2033

Laser Processing Market Size and Trends Analysis

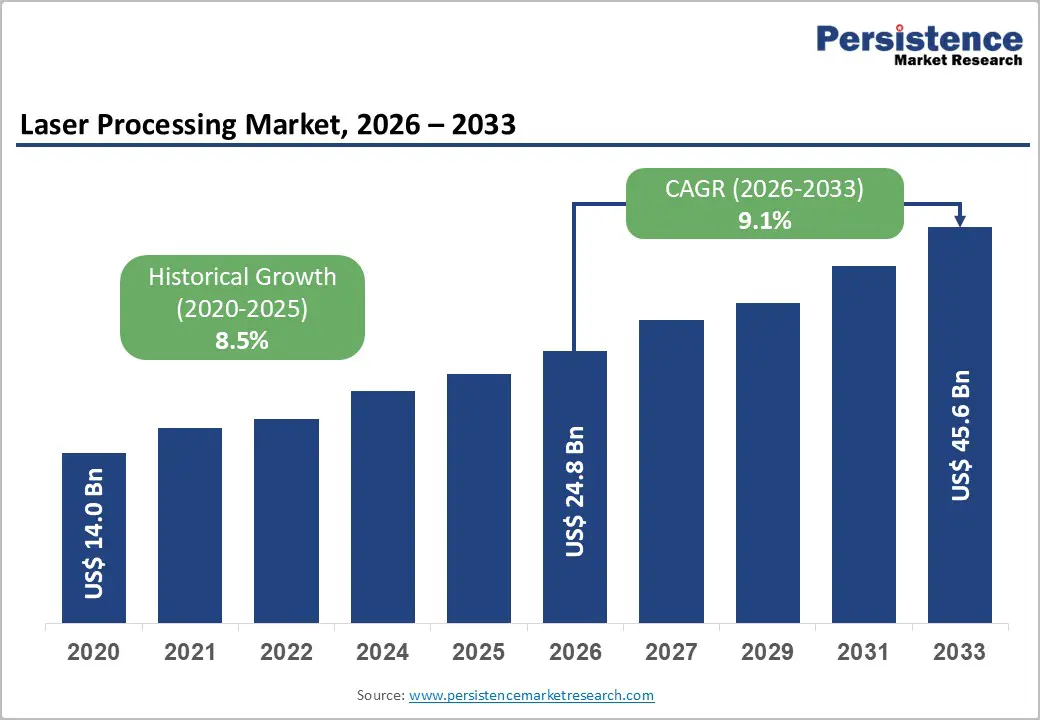

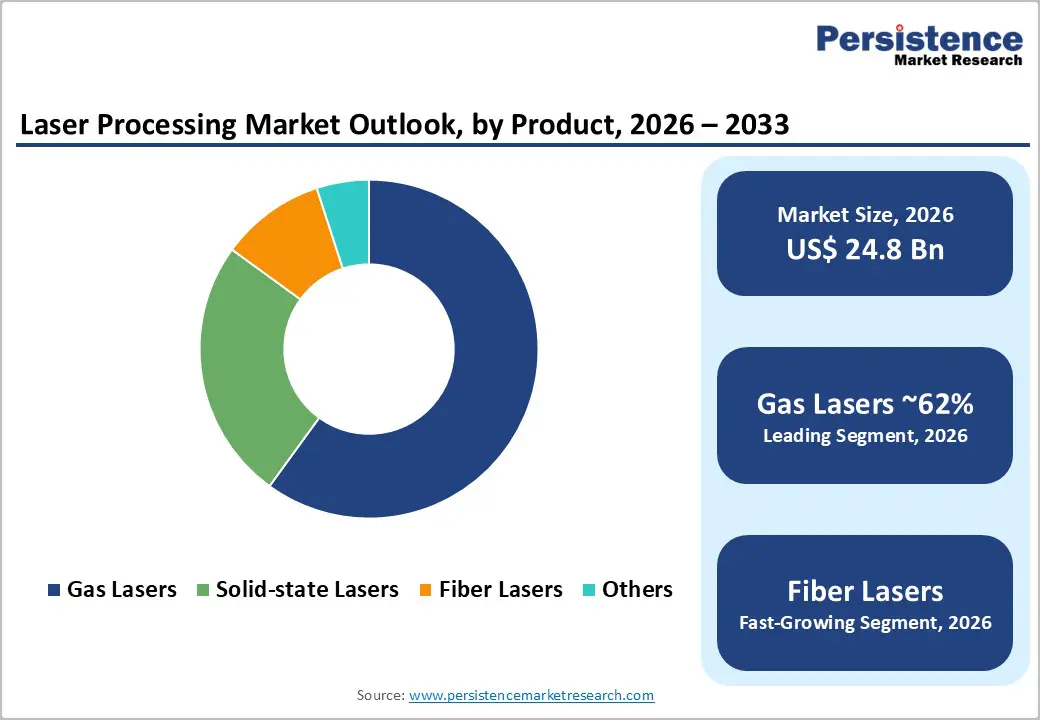

The global laser processing market size is likely to be valued at US$ 24.8 billion in 2026 and is projected to reach US$ 45.6 billion by 2033, growing at a CAGR of 9.1% between 2026 and 2033.

The market is driven by stringent quality requirements in automotive and aerospace manufacturing, the adoption of Industry 4.0 technologies, and the growth of applications in electronics and microelectronics processing.

Key Industry Highlights:

- Leading Product Type: Gas lasers dominate with 62% market share, driven by established infrastructure and cost advantages, while Fiber lasers are the fastest-growing segment at a 10.8% CAGR, driven by efficiency improvements and micro-processing applications in semiconductor and electronics manufacturing.

- Primary Process Type: Material processing holds a 46.1% share through cutting, welding, and forming applications, while Micro-processing is the fastest-growing segment at a 12% CAGR, driven by electronics miniaturization and the expansion of semiconductor manufacturing.

- Leading End-use Application: Machine tools command 32.3% market share reflecting precision manufacturing requirements, while Electronics and Microelectronics represent the fastest-growing segment at 13% CAGR, driven by semiconductor expansion and electric vehicle battery manufacturing.

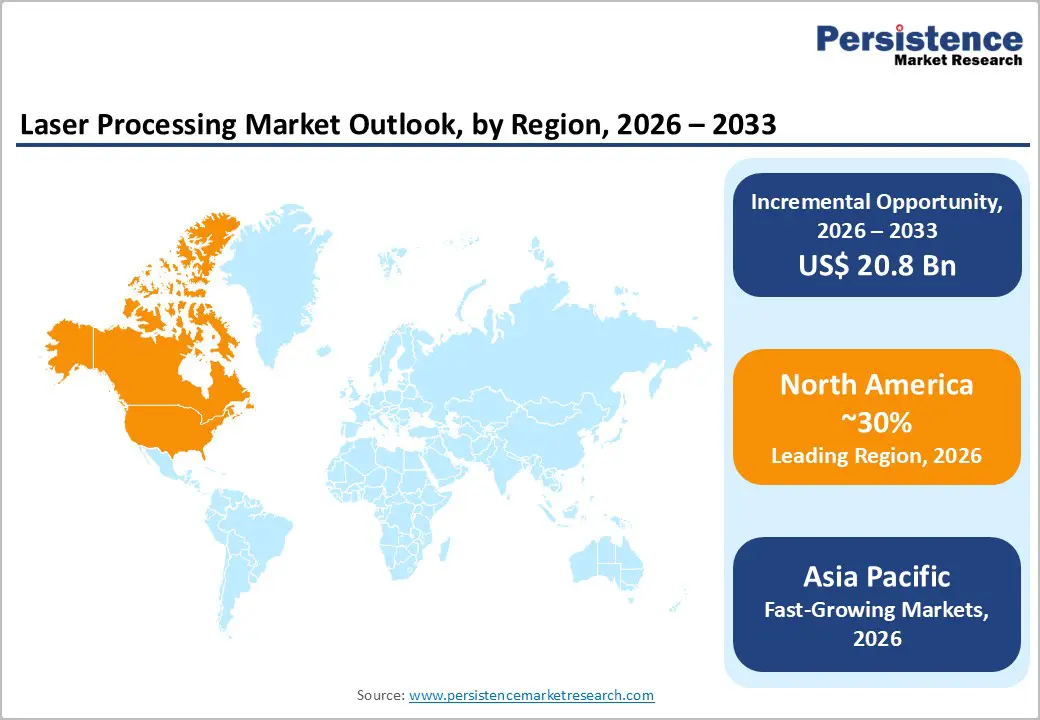

- Regional Market Leadership: North America maintains 30% global market share driven by aerospace manufacturing and semiconductor technology leadership; Europe commands 26% share with regulatory harmonization; Asia Pacific demonstrates fastest regional growth at 12% CAGR, expanding from 36% current share to 45% by 2033.

- Technology Innovation Acceleration: AI-driven autonomous laser systems enabling 92% defect detection superior to manual inspection; Fiber laser efficiency improvements achieving 40-50% electrical conversion versus CO2 at 10%; Predictive maintenance platforms reducing unplanned downtime by 30%.

- Market Consolidation: Top 8 suppliers control 55% global market share, with TRUMPF, Coherent, and IPG Photonics maintaining technology and relationship dominance; Chinese manufacturers establishing competitive positioning through cost advantages and emerging market penetration.

| Key Insights | Details |

|---|---|

| Laser Processing Market Size (2026E) | US$ 24.8 Bn |

| Market Value Forecast (2033F) | US$ 45.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.1% |

| Historical Market Growth (CAGR 2020 to 2024) | 8.5% |

Market Dynamics

Drivers - Accelerating Industrial Automation and Industry 4.0 Digital Transformation

The global manufacturing sector is undergoing a systematic digital transformation, with approximately 75% of large industrial facilities implementing or planning to implement Industry 4.0 technologies by 2028. Laser processing systems, integrated with IoT sensors, artificial intelligence algorithms, and real-time process monitoring, enable predictive maintenance and autonomous operation, reducing downtime by 20%. Demand for precision manufacturing in the automotive sector, with production volumes exceeding 80 million units annually, drives the adoption of laser systems for welding, cutting, and marking applications.

Manufacturing efficiency gains, with laser-based processes reducing material waste by 15-25% and production cycle times by 20-35% compared to conventional methods, establish compelling ROI justifications. Government industrial modernization programs, including Germany's Industry 4.0 initiative, China's Made in China 2025 strategy, which allocates US$ 300+ billion, and India's National Manufacturing Policy, collectively establish sustained technology investment.

Rapidly Expanding Electronics and Microelectronics Manufacturing Demand

Global semiconductor and microelectronics production, representing a US$ 500+ billion market, increasingly depends on laser processing for micro-drilling, marking, and precision cutting applications. The fiber laser market, driven by micro-processing applications in consumer electronics, semiconductor packaging, and printed circuit board manufacturing, is expanding at a 10.8-15.2% CAGR, substantially exceeding overall laser processing growth. Smartphone production, exceeding 1.2 billion units annually, requires laser-based precision processing for component assembly and internal circuit marking.

Advanced semiconductor manufacturing, including sub-7nm chip production at facilities in Taiwan, South Korea, and the United States, necessitates ultra-precision laser systems achieving sub-micron accuracy. Battery manufacturing for electric vehicles, with annual capacity reaching 500+ GWh globally, requires laser processing for component marking, welding, and quality verification.

Restraints - High Capital Equipment Costs and Technical Expertise Requirements

Laser processing system acquisition costs, ranging from US$ 50,000 to US$500,000+ per unit, depending on power, type, and automation level, create significant capital barriers for small and mid-sized manufacturers. System integration complexity, requiring specialized electrical infrastructure, environmental conditioning, and safety containment, adds 30-50% to total installation costs increasing total deployment expense. Operator certification and training requirements, with skilled laser technician development requiring 6-12 months of intensive training programs, create workforce development barriers, particularly in developing economies.

Maintenance and consumable costs, including laser tube replacement (CO2 systems) requiring US$ 5,000-15,000 per replacement every 3-5 years, create ongoing operational expenses. Technology obsolescence risk, with laser system capabilities advancing 15-20% annually through improvements in power, beam quality, and control systems, constrains equipment lifecycle economics.

Safety Regulations and Laser Hazard Management Compliance Complexity

Occupational Safety and Health Administration (OSHA) regulations, European Machinery Directive, and ISO 21500 laser safety standards establish stringent operational requirements, including Class 3B and Class 4 laser containment systems. Environmental regulations regarding laser exhaust fume management, hazardous material disposition from cutting operations, and wastewater treatment create operational compliance complexity and cost.

Personnel exposure limitations, with ANSI Z136.1 standards restricting operator exposure to nominal ocular hazard areas, requiring extensive facility engineering controls. Supply chain traceability for raw material sourcing, including conflict mineral documentation and environmental impact assessments, establishes an administrative burden particularly for manufacturers serving defense and aerospace customers. Regulatory approval timelines for new laser system designs, requiring third-party testing and certification before commercial deployment, extend new product development cycles by 12-18 months.

Opportunity - Advanced Materials Processing and Additive Manufacturing Integration

Laser-based additive manufacturing (3D printing), including selective laser melting (SLM) and laser sintering technologies, represents a distinct market opportunity with an estimated US$8 billion valuation by 2033. The metal additive manufacturing market, currently valued at US$3 billion and expanding at 15% CAGR, depends critically on high-power fiber laser technology for melting and fusing metal powders. Aerospace component manufacturing utilizing additive technologies demonstrates 30-50% material waste reduction and 20% weight reduction benefits, justifying premium processing costs.

Medical device manufacturing, including customized implants and surgical instruments, benefits from laser-based additive capabilities, enabling patient-specific design customization. Government investments in additive manufacturing infrastructure, including US$ 400+ million National Institute of Standards and Technology (NIST) research programs and €150+ million European manufacturing initiatives, establish sustained technology development support.

Emerging Market Manufacturing Expansion and Localization

Asia-Pacific manufacturing sectors, particularly in India, Vietnam, and Indonesia, offer expansion opportunities, with structural demand growth driven by labor cost arbitrage and government incentives. India's manufacturing export initiatives, including the Production Linked Incentive (PLI) scheme, which allocates US$ 30+ billion, provide direct funding for the deployment of laser processing systems. The relocation of electronics manufacturing from China, driven by geopolitical concerns and supply chain diversification imperatives, creates new market demand in Southeast Asia and South Asia.

Automotive manufacturing expansion in India and ASEAN nations, with combined vehicle production projected to exceed 12-15 million units by 2033, creates proportionate demand for laser processing systems. Government skilled workforce development programs, including India's National Skill Development Corporation and Vietnam's manufacturing training initiatives, address technical expertise barriers, enabling faster technology adoption.

Category-wise Analysis

Product Type Insights

Gas lasers hold 62% market share due to their technological maturity, long-standing manufacturing infrastructure, and broad use in cutting, engraving, and welding applications. CO2 lasers dominate this category, accounting for nearly 90% of gas laser usage, supported by cost advantages that make them 30% cheaper than comparable fiber systems. Their compatibility with existing factory setups and decades of trained workforce adoption further strengthen their position.

In contrast, fiber lasers are the fastest-growing segment, projected to grow at 10.8% CAGR through 2033. They offer superior energy efficiency, excellent beam quality, and minimal maintenance needs, making them ideal for semiconductor micromachining and precision cutting. Their lightweight, portable design and lower lifecycle costs continue to accelerate industry-wide adoption.

Process Type Insights

Material processing accounts for 46.1% of the laser processing market due to its essential role in cutting, welding, and shaping metals, plastics, ceramics, and composites. Laser cutting remains the largest application, delivering high precision for automotive, aerospace, and industrial manufacturing. Laser welding offers superior joint strength and minimal distortion, while laser cleaning is gaining traction as a chemical-free surface preparation method. These systems provide strong flexibility, as one laser can handle multiple materials by adjusting parameters, improving production efficiency by reducing waste 15% and cycle times 25%.

Micro-processing is the fastest-growing segment, expanding at 12% CAGR, driven by rising miniaturization in electronics and semiconductors. Fiber lasers enable micro-drilling, micro-marking, and precision cutting with minimal thermal damage. Falling system costs and superior beam quality are accelerating widespread adoption.

End-user Insights

Machine tools manufacturing accounts for 32.3% of the laser processing market due to its reliance on high-precision cutting, shaping, and component fabrication. Laser systems are widely used for producing tungsten carbide cutting tools, complex geometries, and precision machine components such as spindles, collets, and bearings. Leading OEMs including TRUMPF, Bystronic, and Amada have deeply integrated laser technologies into their equipment portfolios, creating strong market concentration and high switching costs.

Electronics and microelectronics represent the fastest-growing end-use segment, expanding at 13% CAGR through 2033. Semiconductor manufacturing, fueled by global capacity expansions and government incentives, is driving strong equipment demand. Consumer electronics and PCB production require extensive laser drilling, cutting, and marking. Rapid growth in EV battery manufacturing further boosts adoption. By 2033, this segment is expected to reach US$ 10 billion.

Regional Market Insights

North America Market Analysis

North America commands approximately 30% of global laser processing market share, valued at approximately US$ 6.9 billion in 2026 with projections approaching US$ 12 billion by 2033. The United States represents the dominant regional market contributor, accounting for 85-90% of North American market value, driven by aerospace manufacturing leadership, automotive innovation ecosystem, and semiconductor technology advancement. The North American market reflects technology leadership dominance by established laser manufacturers, including Coherent (US), TRUMPF (US operations), and IPG Photonics (US), complemented by machine tool integrators such as Bystronic and the Trumpf machine tool divisions.

Europe Laser Processing Market Analysis

Europe represents approximately 22% of the global laser processing market share, valued at approximately US$ 5.6 billion in 2026. Germany, United Kingdom, France, and Spain collectively represent 82% of the European market value, reflecting manufacturing concentration and advanced industrial base European investments concentrate on additive manufacturing laser systems and advanced fiber laser development, with manufacturers allocating €1.5-2.5 billion collectively through 2030 for capability advancement.

Asia Pacific Laser Processing Market Trends

Asia Pacific dominates global laser processing market expansion, commanding approximately 25% market share with projections increasing to 35% by 2033. The region valued at approximately US$ 6.4 billion in 2026 is anticipated to reach US$ 16 billion by 2033, representing the fastest-growing regional market with an estimated CAGR of 12%.

Manufacturing scale represents the primary regional differentiator, with China producing 30+ million vehicles annually, electronics manufacturing exceeding 20% of global output, and semiconductor manufacturing capacity accelerating. Government manufacturing modernization initiatives, including China's Made in China 2025 strategy, India's PLI scheme, and ASEAN manufacturing hubs development, establish binding technology investment mandates.

Competitive Landscape

The market players are investing heavily in research and development for new and efficient products. Companies are also focusing on product launches to augment their market positions. The key players in the market include Avalanche Technology Inc., Crocus Nano Electronics LLC, Everspin Technologies Inc., Honeywell International Inc., Infineon Technologies AG, Intel Corporation, NVE Corporation, Qualcomm Incorporated, Samsung Electronics Co. Ltd., Toshiba Corporation, Tower Semiconductor Ltd.

Key Industry Developments

- In January 2024, Coherent unveiled the OBIS 640 XT, a new red laser module that offers high output power, low noise, and excellent beam quality. This module complements their existing blue and green laser offerings, collectively enhancing the performance of high-performance SRM systems. The introduction of this product signifies Coherent's commitment to advancing laser technology for various applications.

- In January 2024, Novanta Inc. acquired Motion Solutions, which is expected to facilitate the development of innovative intelligent subsystems by leveraging their combined technological capabilities. This acquisition aims to enhance their product offerings and create unique solutions tailored to customer needs. The integration of both companies' technologies presents exciting opportunities for future advancements in their respective markets.

Companies Covered in Laser Processing Market

- Altec GmbH

- Alpha Nov laser

- Amada Co., Ltd.

- Bystronic Laser AG

- Coherent Inc.

- Epilog Laser, Inc.

- Eurolaser GmbH

- IPG Photonics Corporation

- Coherent Inc.

- IPG Photonics Corporation

- Newport Corporation

- Trumpf GmbH + Co. KG

- Universal Laser Systems, Inc.

- Others Key Players

Frequently Asked Questions

The Laser Processing market is estimated to be valued at US$ 24.8 Bn in 2026.

The primary demand driver for the laser processing market is the rising need for high-precision, flexible, and efficient manufacturing across industries. As sectors such as automotive, electronics, aerospace, medical devices, and semiconductors shift toward miniaturization, automation, and high-quality production.

In 2026, the North America region will dominate the market with an exceeding 30% revenue share in the global Laser Processing market.

Among the End- use, Machine Tools holds the highest preference, capturing beyond 32.3% of the market revenue share in 2026, surpassing other End- use type.

The key players in Laser Processing are Altec GmbH, Alpha Nov laser, Amada Co., Ltd., Bystronic Laser AG and Coherent Inc.