- Industrial Machinery

- Laser Gas Analyzer Market

Laser Gas Analyzer Market Size, Share, and Growth Forecast, 2025 - 2032

Laser Gas Analyzer Market Material Type (Stainless Steel Housings, Advanced Alloys), Product Type (In-Situ Laser Gas Analyzers, Extractive Laser Gas Analyzers), End-user, and Regional Analysis for 2025 - 2032

Laser Gas Analyzer Market Size and Trends Analysis

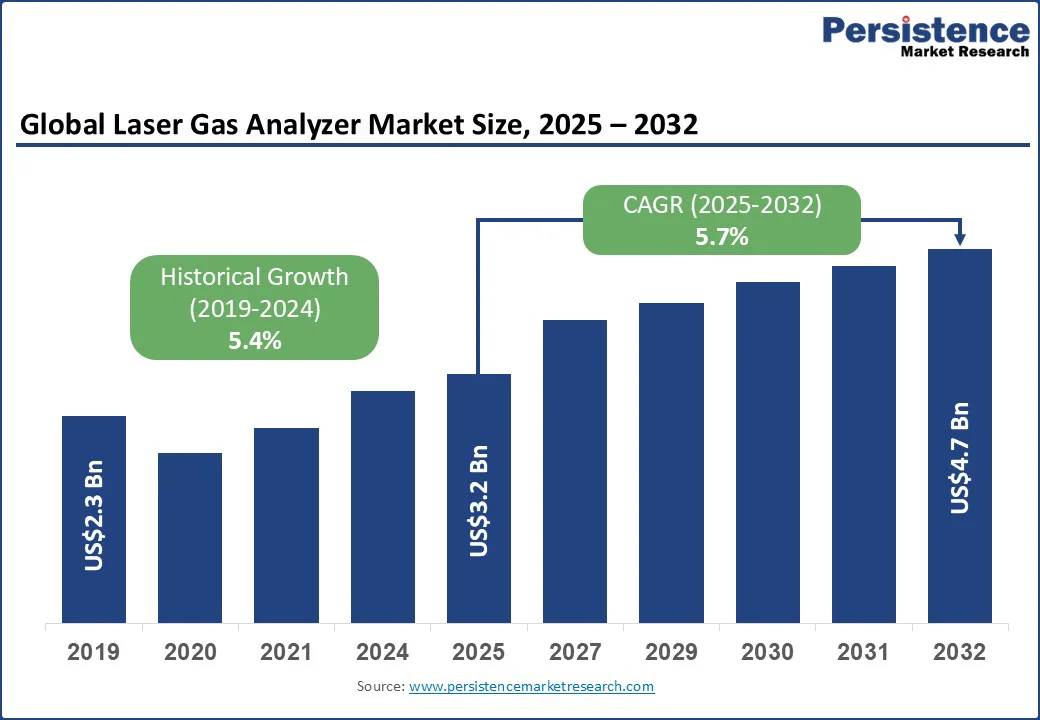

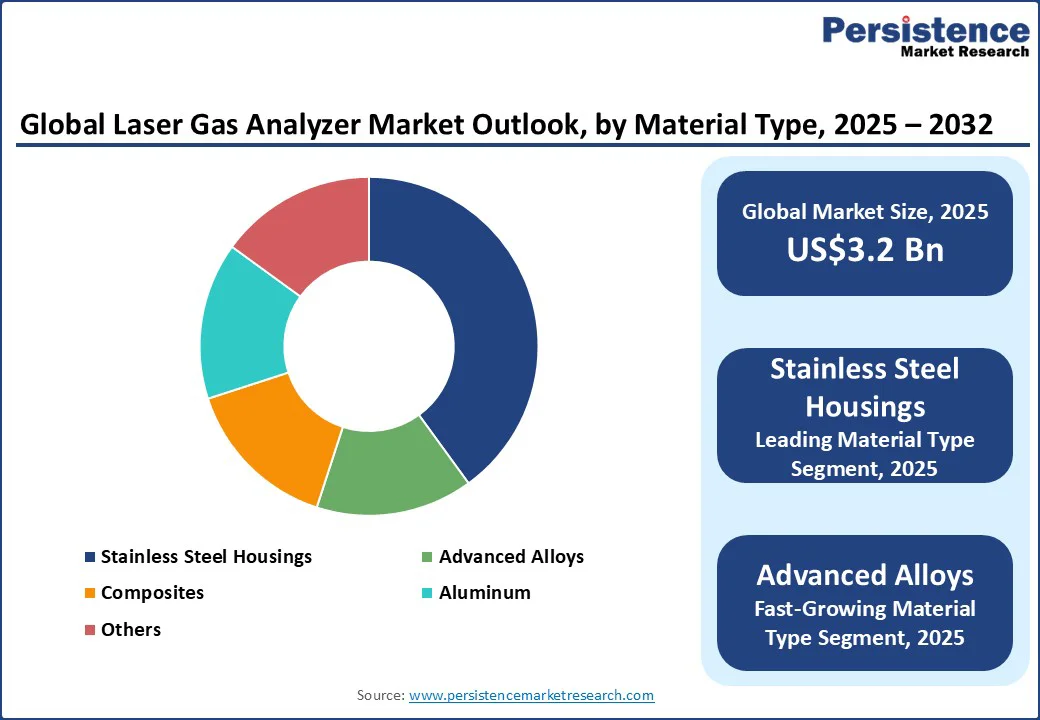

The global laser gas analyzer market size is likely to be valued at US$3.2 Bn in 2025 and is expected to reach US$4.7 Bn by 2032, growing at a CAGR of 5.7% during the forecast period from 2025 to 2032, due to the rising demand for real-time emissions monitoring, stricter environmental regulations, and the shift toward high-precision analytical instruments in industrial applications.

Key Industry Highlights

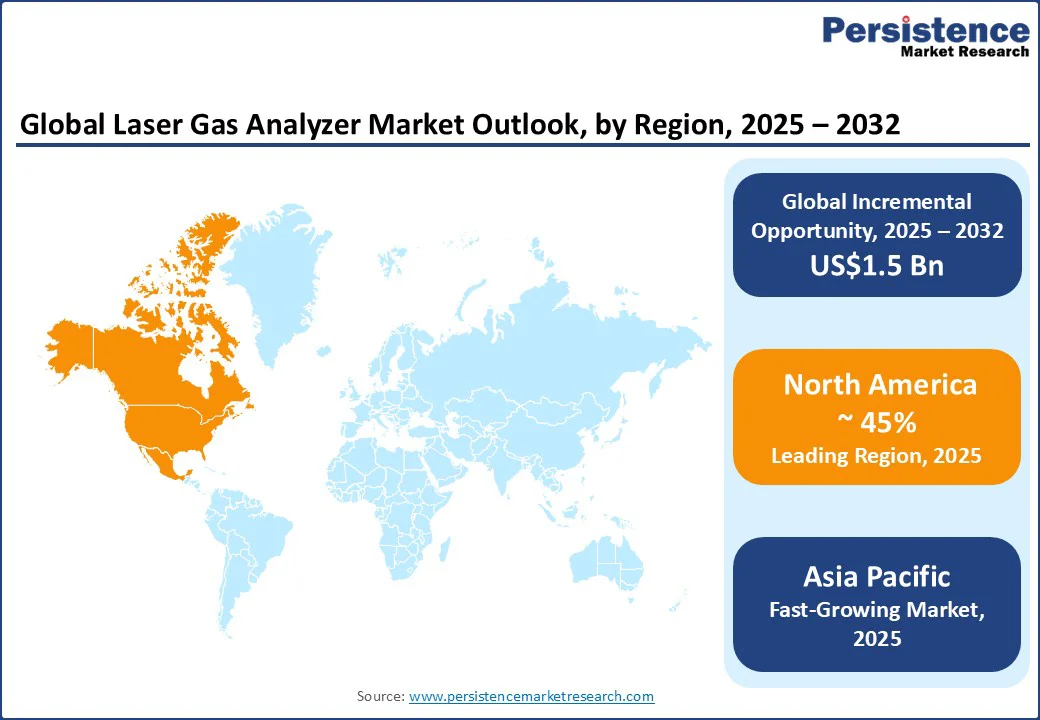

- Leading Region: North America, accounting for 36% of global market share in 2025, driven by stringent EPA compliance requirements and strong adoption in oil & gas and power sectors.

- Fastest-growing Region: Asia Pacific, supported by rapid industrialization, clean air regulations, and hydrogen economy investments in China and India.

- Investment Plans: Global investments in hydrogen infrastructure and carbon capture projects are expected to exceed US$500 Bn by 2030, boosting demand for high-precision analyzers in renewable and clean energy sectors.

- Dominant Material Type: Stainless steel housings, accounting for over 40% of the market share in 2025, driven by corrosion resistance, durability, and compliance with safety standards in oil & gas, chemicals, and power generation industries.

- Leading Product Type: In-situ analyzers, holding over 50% market share in 2025, owing to real-time monitoring and high suitability for high-temperature industrial environments.

| Key Insights | Details |

|---|---|

| Laser Gas Analyzer Market Size (2025E) | US$3.2 Bn |

| Market Value Forecast (2032F) | US$4.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Real-Time Process Optimization and Stricter Environmental Regulations

Governments worldwide are imposing strict mandates to curb industrial emissions. For instance, the U.S. Environmental Protection Agency (EPA) and the European Union Industrial Emissions Directive (IED) require industries to adopt precise monitoring solutions to ensure compliance.

Laser gas analyzers provide continuous emissions monitoring systems (CEMS) that measure pollutants such as CO2, NOx, and SO2 with superior accuracy compared to traditional systems. The compliance-driven adoption is anticipated to increase, particularly in high-emission sectors such as cement, steel, and oil refining, leading to a steady revenue growth through 2032.

Industries such as petrochemicals and power generation increasingly rely on real-time gas analysis to optimize combustion efficiency, reduce fuel costs, and prevent unplanned downtime. According to the International Energy Agency (IEA), industrial energy efficiency improvements could reduce global energy demand by nearly 15% by 2030.

Laser gas analyzers enable inline, non-contact monitoring that facilitates these gains. Their ability to operate in harsh environments with minimal maintenance positions them as a cost-effective solution, fostering wider market penetration.

Progress in tunable diode laser spectroscopy (TDLS), cavity ring-down spectroscopy (CRDS), and quantum cascade lasers (QCL) is improving detection sensitivity and broadening the spectrum of measurable gases. This allows industries to monitor trace-level contaminants critical for safety and quality assurance.

For example, semiconductor manufacturing requires ultra-low concentration detection of moisture and oxygen in process gases. The innovation-driven expansion of application areas enhances the total addressable market for laser gas analyzers, creating opportunities for premium, high-margin product segments.

High Capital Installation Costs and Skilled Workforce Requirements

Laser gas analyzers require a substantial upfront investment, covering not just the equipment itself but also the costs of calibration, integration, and ongoing maintenance.

For small and medium-sized enterprises (SMEs), these financial demands can be a major barrier, especially when compared to more affordable, conventional systems. In regions with less stringent environmental regulations, the high cost-to-benefit ratio further limits adoption, reducing market penetration and hindering short-term growth.

Operating and interpreting data from laser-based analyzers requires skilled technicians. In many developing markets, there is a noticeable shortage of trained professionals, which often forces companies to rely on outsourced expertise.

This dependence significantly raises operational costs. Without adequate investments in technical education and workforce training, this skill gap may continue to slow down the adoption of laser gas analyzers and act as a constraint on overall market growth.

Integration with IIoT Platforms and Renewable Energy Applications

The convergence of laser gas analyzers with Industrial Internet of Things (IIoT) platforms offers predictive maintenance, automated compliance reporting, and advanced data analytics. This integration reduces operational downtime while enabling remote monitoring. Markets adopting smart factories and Industry 4.0 frameworks are projected to accelerate demand, with value-added services creating recurring revenue streams for manufacturers.

Laser gas analyzers are increasingly utilized in hydrogen production plants, bioenergy facilities, and carbon capture projects. Accurate detection of H2 purity and monitoring of CO2 capture processes are vital for safety and efficiency. With global investments in hydrogen infrastructure expected to exceed US$500 Bn by 2030 (Hydrogen Council), the application scope for analyzers in renewable energy markets is set to expand significantly.

Category-wise Analysis

Material Type Insights

Laser gas analyzers with stainless steel housings dominate due to durability, corrosion resistance, and suitability for harsh environments such as oil rigs and chemical plants. They account for the majority share, estimated at over 40% of the market in 2025, owing to compliance with safety regulations and robust lifecycle performance.

Advanced alloys and composite materials are expected to grow at the fastest CAGR between 2025 and 2032. Lightweight structures reduce installation costs and expand deployment flexibility. These materials also support miniaturization trends in portable gas analyzers, enabling wider adoption in mobile and remote applications.

Product Type Insights

In-situ analyzers, which measure gases directly in the process stream, hold the largest market share. Their dominance stems from real-time monitoring capabilities, minimal sample conditioning, and suitability for high-temperature industrial applications. In 2025, they are projected to account for over 50% of total revenues.

Portable analyzers are anticipated to witness the highest CAGR through 2032. The demand arises from mobile inspections, emergency response, and field applications where flexibility and rapid setup are essential. Industries such as mining and environmental monitoring increasingly prefer compact devices, driving accelerated adoption.

Regional Insights

North America Laser Gas Analyzer Market Trends - Regulatory Frameworks, and CCS Projects Fuel Market Leadership

North America is anticipated to dominate, accounting for 36% of the market share in 2025. Growth in this region is largely driven by stringent environmental regulations enforced by agencies such as the U.S. Environmental Protection Agency (EPA).

Regulations such as the Clean Air Act, along with specific mandates under 40 CFR Part 60 and Part 75, require industrial facilities and power plants to implement Continuous Emissions Monitoring Systems (CEMS) for pollutants such as sulfur dioxide, nitrogen oxides, carbon dioxide, and particulate matter. These rules ensure consistent demand for high-precision analyzers and related instrumentation.

The U.S. accounts for over 45% of the regional share in 2025. The shale gas boom in states, including Texas, North Dakota, and Pennsylvania, has further intensified the need for emissions monitoring in upstream oil and gas operations. With increased drilling and natural gas processing comes heightened scrutiny of methane and volatile organic compound (VOC) emissions.

The modernization of the power sector, especially the transition from coal to natural gas, has also led to widespread retrofitting of emissions monitoring systems in combined-cycle plants. Moreover, the growing number of carbon capture and storage (CCS) projects across the U.S. is contributing to demand for sophisticated analyzers that can monitor CO2 capture efficiency and detect leaks in storage infrastructure. Notable projects such as Project Tundra in North Dakota and Petra Nova in Texas exemplify this trend.

Europe Laser Gas Analyzer Market Trends - Climate Policy and Technological Innovation Drive Demand

Europe continues to lead globally in emissions control and environmental sustainability, supported by robust regulatory frameworks such as the European Green Deal, the Industrial Emissions Directive (IED), and the Ambient Air Quality Directives.

The region’s commitment to achieving net-zero carbon emissions by 2050 is reshaping industrial practices and driving investments in advanced monitoring technologies. Countries including Germany and the U.K. are at the forefront of emissions monitoring system adoption, backed by stringent compliance frameworks, active policy enforcement, and large industrial bases.

Germany, for instance, is a central hub for environmental engineering and home to global innovators such as Siemens, SICK AG, and Testo SE. These companies have played a key role in advancing miniaturized and portable analyzers that cater to both heavy industries and research institutions.

The country’s long-standing Energiewende (energy transition) policy aims to phase out fossil fuels, which demands precise, continuous emissions monitoring across the power and manufacturing sectors.

Hydrogen infrastructure is emerging as one of the strongest growth drivers for the laser gas analyzer market in Europe. The EU aims to become a global leader in hydrogen production, distribution, and use by 2030, requiring monitoring equipment that can detect emissions or leakage across the hydrogen value chain.

The emphasis on energy efficiency in manufacturing is another driver, as policies such as the Ecodesign Directive and the Carbon Border Adjustment Mechanism push industries toward cleaner production and comprehensive emissions tracking.

Europe has become a global hub for research and innovation in sensor miniaturization and portable air quality analyzers, which are increasingly used by SMEs, mobile labs, and academic institutions.

Asia Pacific Laser Gas Analyzer Market Trends - Industrial Growth and Policy Mandates Spur Rapid Adoption

Asia Pacific is expected to be the fastest-growing market for emissions monitoring systems through 2030, propelled by rapid industrialization, population growth, and increasing environmental regulation. Countries, including China and India, are leading this surge in adoption due to worsening air quality, growing energy demand, and large-scale government mandates.

China’s 14th Five-Year Plan, for example, places heavy emphasis on environmental protection, requiring industries such as steel, cement, and power generation to install real-time emissions monitoring systems. National initiatives such as the “Blue Sky Protection Campaign” further reinforce this trend, with centralized digital platforms monitoring industrial emissions across the country.

India, meanwhile, has implemented mandatory CEMS installation in 17 categories of highly polluting industries, including coal-fired thermal power plants.

The government’s National Clean Air Programme (NCAP) and market-based efficiency initiatives such as the Perform, Achieve, and Trade (PAT) scheme are incentivizing the adoption of emissions monitoring technology. Local manufacturers such as Aimil Ltd. and partnerships with institutions such as CSIR-NEERI are helping accelerate deployment by offering cost-effective, domestically-produced analyzers.

Competitive Landscape

The global laser gas analyzer market is moderately consolidated, with leading global players holding approximately 45% market share. Competition is characterized by technology leadership, regulatory certifications, and strong regional distribution networks.

Medium-sized firms focus on niche applications and portable device innovation. Market leaders prioritize innovation in spectroscopy technologies, cost leadership through modular designs, and geographic expansion into Asia Pacific. Service-based business models, including cloud-linked monitoring, are emerging as differentiators.

Key Industry Developments:

- In May 2024, Honeywell and Weatherford International announced a collaboration integrating Honeywell’s emissions management software with Weatherford’s SCADA platform. The partnership enables oil & gas producers to achieve near real-time emissions tracking and compliance reporting.

- In June 2025, ABB Ltd. showcased its upgraded ACF5000 laser-based gas analyzer at ENVEX 2025 in South Korea. The system can detect up to 15 gases at ultra-low concentrations and is designed for future regulatory upgrades, strengthening ABB’s leadership in compliance-driven markets.

Companies Covered in Laser Gas Analyzer Market

- ABB Ltd.

- Siemens AG

- Yokogawa Electric Corporation

- Emerson Electric Co.

- Servomex Group Ltd.

- AMETEK Inc.

- Mettler-Toledo International Inc.

- Fuji Electric Co., Ltd.

- Teledyne Technologies Incorporated

- Sick AG

- HORIBA Ltd.

- Endress+Hauser Group

- Nova Analytical Systems

- Honeywell International Inc.

- Opsis AB

- Gasmet Technologies Oy

- Unisearch Associates Inc.

- Neo Monitors AS

- Siemens Process Analytics

- Environnement S.A (ENVEA Group)

Frequently Asked Questions

The laser gas analyzer market size is estimated at US$3.2 Bn in 2025.

By 2032, the laser gas analyzer market is projected to reach US$4.7 Bn, reflecting steady growth through the forecast period.

Key trends include the enforcement of stricter emission regulations, the adoption of real-time process optimization systems, advancements in laser spectroscopy technologies (TDLS, CRDS, QCL), and integration with Industrial IoT platforms. Growing applications in hydrogen production and carbon capture are also shaping market expansion.

By product type, in-situ analyzers dominate with over 50% market share in 2025.

The laser gas analyzer market is projected to grow at a CAGR of 5.7% between 2025 and 2032.

Leading players include ABB Ltd., Siemens AG, Yokogawa Electric Corporation, Emerson Electric Co., and Servomex Group Ltd.