- Renewable Energy

- String Inverter Market

String Inverter Market Size, Share, and Growth Forecast, 2026 - 2033

String Inverter Market by Type of System (On-grid, Off-grid), Phase Type (Single-phase, Three-phase), Application (Residential, Commercial, Industrial), and Regional Analysis for 2026 – 2033

String Inverter Market Size and Trends Analysis

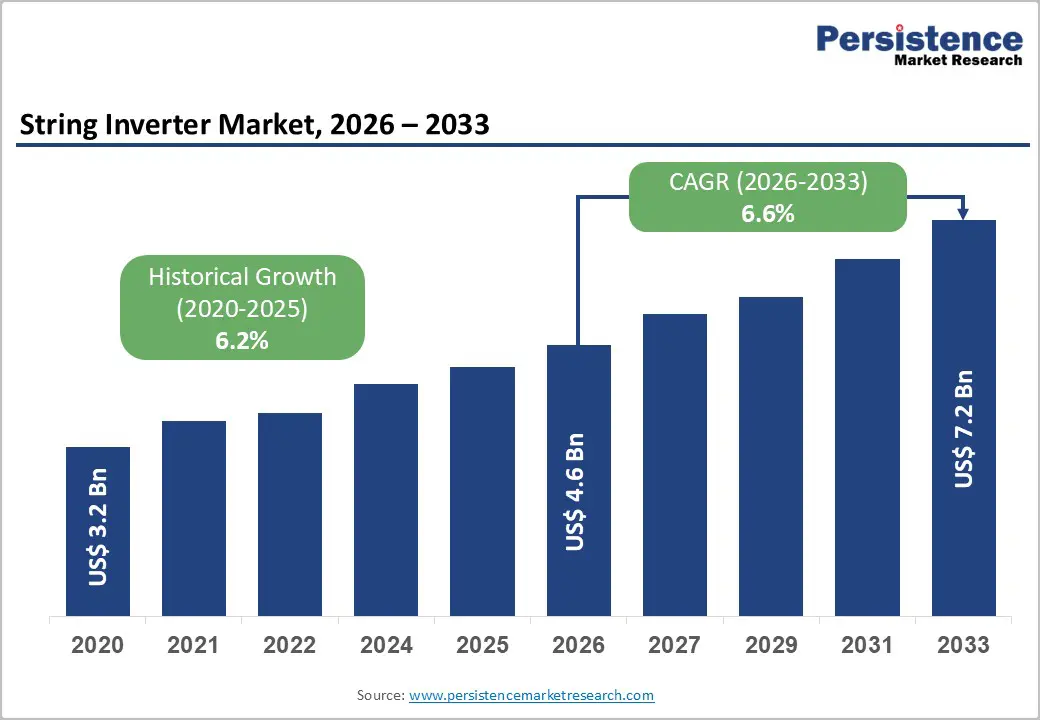

The global string inverter market size is likely to be valued at US$4.6 billion in 2026, and is expected to reach US$7.2 billion by 2033, growing at a CAGR of 6.6% during the forecast period from 2026 to 2033, driven by the increasing prevalence of solar photovoltaic installations, rising demand for cost-effective string-level MPPT solutions, and growing adoption of grid-tied residential and commercial solar systems.

Growing demand for high-efficiency, reliable string inverters, especially on-grid three-phase models for commercial and industrial applications, is accelerating adoption across end-use sectors. Advances in smart monitoring, MPPT optimization, and lightweight designs are further boosting uptake by offering better energy yield and lower installation costs. Increasing recognition of string inverters as critical for scalable, decentralized solar power generation in emerging renewable markets remains a major driver of market growth.

Key Industry Highlights:

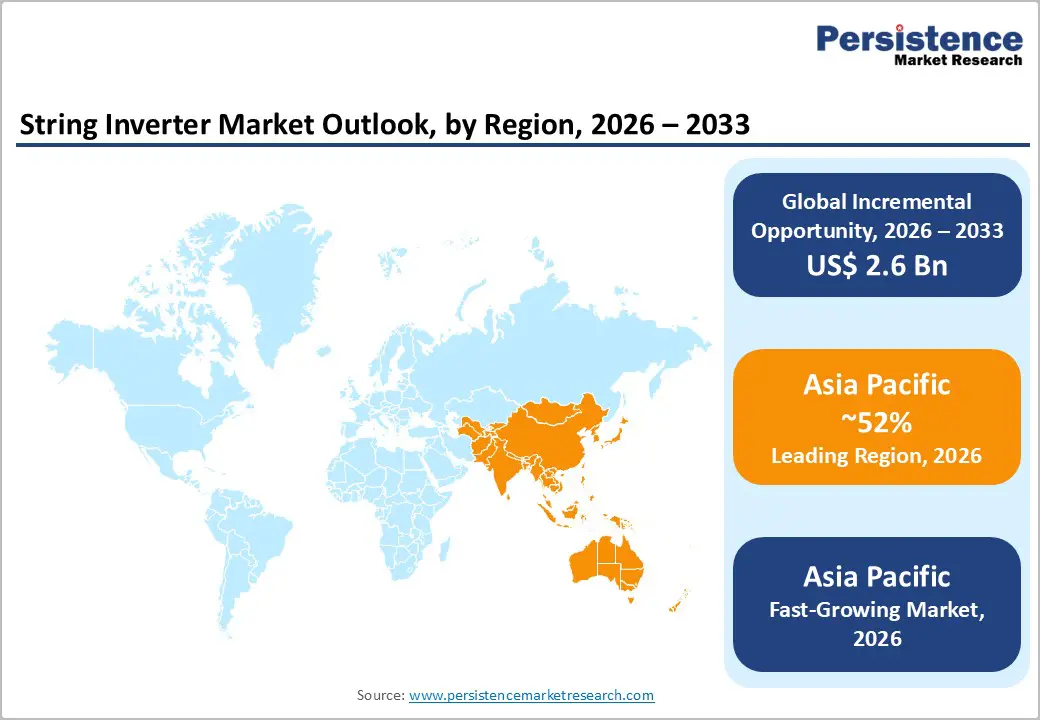

- Leading Region: Asia Pacific, anticipated to account for a 52% market share in 2026, driven by dominant solar PV capacity additions, strong government subsidies, and high demand in China and India.

- Fastest-growing Region: Asia Pacific, fueled by rapid residential rooftop solar growth, expanding utility-scale projects, and growing investments in inverter manufacturing.

- Leading Phase Type: Three-phase, to contribute nearly 68% of the market revenue, due to dominance in commercial and industrial installations.

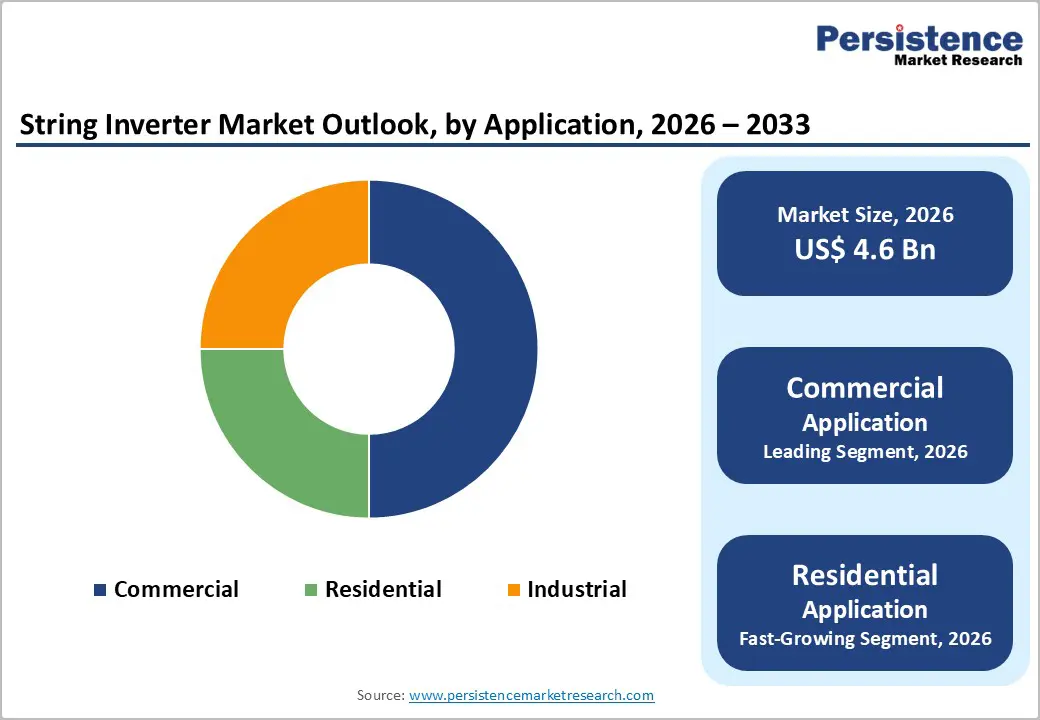

- Leading Application: Commercial, to account for over 45% of the market revenue, due to large-scale rooftop and ground-mounted systems.

| Key Insights | Details |

|---|---|

| String Inverter Market Size (2026E) | US$4.6 Bn |

| Market Value Forecast (2033F) | US$7.2 Bn |

| Projected Growth CAGR (2026-2033) | 6.6% |

| Historical Market Growth (2020-2025) | 6.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Rising Solar PV Installations and Cost-Effective String-Level MPPT Solutions

The rise in solar photovoltaic (PV) installations worldwide has increased the focus on maximizing the efficiency and reliability of power conversion systems. As more residential, commercial, and utility-scale solar projects come online, operators are seeking solutions to maximize the energy yield of each array. One key challenge in large and complex PV systems is mismatch loss, where shading, soiling, or module performance differences cause some panels to operate below optimal power. Traditional central inverters with a single maximum power point tracking (MPPT) algorithm can struggle to optimize energy harvest under these non-uniform conditions. Solar installations continue to expand strongly into 2025, with early figures indicating hundreds of gigawatts were added in the first half of the year as deployment accelerates in key markets such as China, India, and the U.S.

This has led to the growing adoption of string-level MPPT solutions, which allow each string or subgroup of solar modules to be tracked independently. By adjusting operating points for individual strings, string-level MPPT can substantially increase energy capture, particularly in installations with shading or orientation variations. Because these solutions can be implemented with more cost-effective power electronics than multiple microinverters, they offer a favorable balance of performance and affordability.

Increasing Decentralized Solar Adoption and Smart Monitoring Integration

The rise in decentralized solar adoption and integration of smart monitoring technologies is reshaping how solar PV systems are deployed and managed. Decentralized solar, including rooftop, residential, and small commercial installations, enables users to generate electricity close to where it’s consumed, reducing reliance on centralized grids and minimizing transmission losses. Distributed solar deployments now account for a significant share of global PV capacity additions, representing about 44% of new solar PV capacity added in 2023, highlighting strong momentum toward localized generation.

Smart monitoring systems, including IoT-enabled sensors, cloud-based analytics, and digital energy management platforms, are increasingly being integrated into decentralized PV systems. Around 62% of solar users now employ smart technologies to enhance performance, enable real-time monitoring, and reduce energy waste. These tools not only enable system owners to remotely track energy production but also support predictive maintenance and automated optimization, improving reliability and system efficiency.

Barrier Analysis – High Competition from Microinverters and Central Inverters

Competition among solar power electronics is intensifying as microinverters, string inverters, and central inverters target different segments of the PV market. Central inverters are preferred for large-scale solar farms because they efficiently handle high power capacity, minimizing the cost per kilowatt. They are less effective in managing performance variations caused by shading or mismatched panels. Microinverters, in contrast, optimize each solar panel individually, improving energy harvest in residential and small commercial systems, but come with higher upfront costs.

String inverters with multiple MPPT channels aim to balance the two, offering cost-effective modular solutions with improved performance in partially shaded or uneven arrays. The presence of these competing technologies creates a market where solar developers must carefully choose solutions based on system size, budget, and site conditions. For context, in residential systems, microinverters can increase energy yield by 5–15% in shaded or irregular installations, while central inverters remain more cost-effective for large, uniform utility projects.

Supply Chain Volatility and Component Shortages

Supply chain volatility and component shortages have become significant challenges for the solar PV industry, affecting system availability, costs, and deployment timelines. The solar value chain relies on a global network of suppliers for modules, inverters, mounting structures, wiring, and semiconductors. Disruptions, whether caused by geopolitical tensions, trade policy shifts, logistics bottlenecks, or factory closures, can restrict access to critical parts and raw materials. When an essential component, such as power electronics, specialized semiconductor chips, or PV junction boxes, becomes scarce, manufacturers are forced to delay shipments, adjust production schedules, or source alternative parts, which increases lead times.

Price fluctuations are another consequence: shortages of key inputs like silicon wafers, copper, or electronic components can raise procurement costs and squeeze profit margins. For installers and project developers, extended lead times translate into delayed project commissioning and financing challenges, particularly when incentives are tied to completion deadlines. Volatility also pressures inventory management. Companies may hold larger inventories to hedge against shortages, tying up capital and raising storage costs.

Opportunity Analysis – Expansion of Smart and Hybrid String Inverter Platforms

The expansion of smart and hybrid string inverter platforms is reshaping how solar PV systems are designed, operated, and maintained. Traditional string inverters convert DC power from multiple solar panel strings into AC power for the grid or load, but smart and hybrid platforms go a step further by integrating advanced control, monitoring, and energy management features directly into the inverter architecture.

Smart string inverters are equipped with real-time data analytics, remote monitoring, and adaptive control capabilities that enable system owners to optimize energy production and quickly identify performance issues. These inverters can communicate with energy management systems, battery storage, and load controllers, improving overall system efficiency and resilience. Hybrid string inverters take this further by integrating PV power conversion with energy storage, enabling systems to balance solar generation with battery charging and discharging without requiring separate dedicated hardware.

Growth in Residential and C&I Rooftop Solar with Value-Added Services

Growth in residential and commercial & industrial (C&I) rooftop solar is increasingly driven by the addition of value-added services that enhance performance, reliability, and customer experience. Homeowners and businesses are no longer buying solar panels alone; they are investing in complete energy solutions that include performance monitoring, maintenance plans, financing packages, and integration with storage or smart load management systems.

In the residential segment, value-added offerings such as real-time performance dashboards, remote troubleshooting, and automated system health alerts give consumers greater visibility and control over their energy production. Financing innovations such as solar leases, power purchase agreements (PPAs), and low-interest loans have also lowered entry barriers, attracting a broader customer base. Similarly, many installers now bundle roof assessments, preventive maintenance, and warranty extensions to improve long-term system reliability and peace of mind. Commercial and industrial users benefit from tailored services that align solar power with energy cost management goals, such as demand-charge reduction strategies and on-site energy storage optimization. These services help businesses lower operating costs while maximizing return on investment.

Category-wise Analysis

Phase Type Insights

Three-phase systems are projected to lead the market, accounting for nearly 68% of revenue in 2026, as they are the preferred choice for medium to large commercial, industrial, and utility-scale installations. Unlike single-phase systems, three-phase inverters distribute electrical loads more evenly, improve power quality, and support higher capacity outputs, making them more efficient for large arrays. They also reduce electrical losses and better handle fluctuations in generation, which enhances system reliability and performance. SMA Solar Technology AG’s Sunny Highpower three-phase inverters are designed for 1500 V PV systems and are widely used in commercial and utility projects to boost power density and lower overall system costs, highlighting the market's preference for three-phase solutions in larger solar applications.

Single-phase is expected to be the fastest-growing phase type, fueled by the increasing adoption in residential and small commercial systems, where simplicity, affordability, and ease of installation are key priorities. As rooftop solar expands among homeowners and small businesses, single-phase inverters offer a cost-effective solution that efficiently handles the lower power requirements typical of these installations. Their lighter weight and smaller footprint simplify permitting and installation, while smart features and improved efficiency further boost appeal. Sungrow Power Supply Co., Ltd., which introduced its SG 5.0RS-L residential single-phase hybrid inverter, catering to homeowners who want both solar and battery integration in a compact unit. This highlights the trend toward more powerful and versatile single-phase solutions for household solar installations.

Application Insights

The commercial segment is expected to dominate the market, contributing nearly 45% of revenue in 2026, as businesses and institutions are rapidly adopting solar to reduce energy costs and meet sustainability goals. Commercial installations, such as factories, offices, shopping centers, and schools, typically require larger systems than residential roofs, creating higher overall revenue per project. These systems also often leverage value-added solutions such as energy storage, demand-charge management, and smart monitoring, which increase system complexity and cost and thus market value. Walmart Inc. is one of the largest corporate adopters of rooftop solar in the United States. As reported by the Solar Energy Industries Association (SEIA), Walmart has deployed solar photovoltaic systems on hundreds of its store rooftops and facilities, placing it among the top corporate users of commercial solar capacity nationwide.

The residential segment is expected to represent the fastest-growing application, driven by homeowners who are investing in rooftop systems to cut electricity costs, increase energy independence, and benefit from renewable incentives. Falling installation costs, easier financing options, and simpler permitting processes have made residential solar accessible to a broader range of consumers. The rise of home battery storage and smart energy management systems has increased the appeal of residential PV as part of an integrated home energy solution. Sunrun Inc., a leading U.S. residential solar company, became the first clean energy provider to surpass 1 million residential solar customers, roughly one in every five U.S. home solar systems installed, demonstrating rapid adoption of rooftop solar at the household level. This milestone reflects strong consumer interest in home solar power for energy independence, cost savings, and grid resilience.

Regional Insights

North America String Inverter Market Trends

In North America, growth is driven by the region’s advanced solar deployment, strong research and development capabilities, and high public awareness of distributed generation benefits. Installation systems in the U.S. and Canada provide extensive support for string inverter programs, ensuring wide accessibility across on-grid, three-phase, and commercial populations. Increasing demand for smart, convenient, and easy-to-install forms is further accelerating adoption, as these formats improve energy yield and reduce barriers associated with central inverters.

Innovation in string inverter technology, including stable multi-MPPT, improved smart monitoring, and targeted residential enhancement, is attracting significant investment from both public and private sectors. Government initiatives and ITC campaigns continue to promote the use of against grid risks, installation costs, and emerging distributed solar threats, creating sustained market demand. The growing focus on commercial grades and specialty uses, particularly for residential and other uses, is expanding the target applications for string inverters.

Europe String Inverter Market Trends

Europe is supported by increasing awareness of distributed solar benefits, strong regulatory systems, and government-led renewable programs. Countries such as Germany, Spain, Italy, and the Netherlands have well-established solar frameworks that support routine string inverter use and encourage adoption of innovative inverter delivery methods, including string inverters. These high-efficiency formulations are particularly appealing for commercial populations, regulation-conscious installers, and residential users, improving yield and coverage rates.

Technological advancements in string inverter development, such as enhanced multi-MPPT, application-targeted delivery, and improved smart grades, are further boosting market potential. European authorities are increasingly supporting research and trials for inverters against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, grid-support options is aligned with the region’s focus on preventive renewable integration and reducing curtailment. Public awareness campaigns and promotion drives are expanding reach in both urban and rural areas, while suppliers are investing in monitoring and novel variants to increase efficacy.

Asia Pacific String Inverter Market Trends

Asia Pacific is projected to dominate and be the fastest-growing market, capturing 52% revenue in 2026, propelled by rising solar awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Japan, and Australia are actively promoting inverter campaigns to address solar growth and emerging distributed generation needs. String inverters are particularly attractive in these regions due to their cost-effective administration, ease of installation, and suitability for large-scale rooftop and C&I drives in both urban and rural populations.

Technological advancements are supporting the development of stable, effective, and easy-to-deploy string inverters, which can withstand challenging climatic conditions and minimize downtime dependence. These innovations are critical for reaching domestic installers and improving overall solar coverage. Growing demand for on-grid, three-phase, and commercial applications is contributing to market expansion. Public-private partnerships, increased renewable expenditure, and rising investment in inverter research and manufacturing capacity are further accelerating growth. The convenience of inverter delivery, combined with improved efficiency and reduced risk of failure, positions string inverters as a preferred choice.

Competitive Landscape

The global string inverter market features competition between established power electronics leaders and emerging digital inverter suppliers. In North America and Europe, SMA Technologies AG and SolarEdge Technologies Ltd lead through strong R&D, distribution networks, and installer ties, bolstered by innovative multi-MPPT and smart monitoring programs.

In Asia Pacific, Huawei Technologies Co. Ltd. and Growatt New Energy Technology Co. Ltd. advance with cost-competitive solutions, enhancing accessibility. Smart monitoring delivery boosts yield, cuts O&M risks, and enables mass integrations across projects. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. High-efficiency formulations solve yield issues, aiding penetration in residential and C&I segments.

Key Industry Developments:

- In October 2025, GoodWe Technologies Co., Ltd. launched the 50 kW SDT G3 inverter for the European corporate and industrial (C&I) solar market. This low-noise, lightweight string inverter, part of the SDT series, was designed for small- to medium-scale C&I solar installations, addressing demand for quieter operation and easier installation, especially for commercial rooftops and distributed solar projects across Europe.

- In January 2023, SolaX unveiled its new single-phase residential on-grid inverter, the X1-MINI G4 (0.6–3.3 kW). Weighing just 5.2 kg and measuring 290×206×120 mm, it delivered an efficiency of 98% (96–97% for the European version). The compact design and high performance made it ideal for homeowners seeking reliable and efficient on-grid solar solutions.

Companies Covered in String Inverter Market

- Chint Group Corp.

- Delta Electronics Inc.

- Growatt New Energy Technology Co., Ltd.

- Siemens AGSMA Technologies AG

- Fimer S.p.A.

- SolarEdge Technologies Ltd.

- Ginlong Technologies Co.

- SolarMax Energy Pvt. Ltd.

- Huawei Technologies Co., Ltd.

- ABB Ltd.

- KACO New Energy GmbH

- Ningbo Ginlong Technologies Co., Ltd.

Frequently Asked Questions

The global string inverter market is projected to reach US$4.6 billion in 2026.

Rising solar PV installations and demand for cost-effective string-level MPPT solutions are the key drivers.

The string inverter market is poised to witness a CAGR of 6.6% from 2026 to 2033.

Smart and hybrid string inverter platforms and value-added services in residential and C&I rooftop solar are key opportunities.

SMA Technologies AG, SolarEdge Technologies Ltd., Huawei Technologies Co. Ltd., Growatt New Energy Technology Co. Ltd., and ABB Ltd. are the key players.