- Electric Mobility

- Traction Inverter Market

Traction Inverter Market Size, Share, and Growth Forecast, 2026 - 2033

Traction Inverter Market by Propulsion Type (BEV, HEV and PHEV), by Output Power Type (200V, 201 to 900V and above 901V), by Materials Type (Gallium Nitride (GaN), Silicon (Si) and Silicon Nitride (SiC), by Technology Type (IGBT and MOSFET), by Vehicle Type (Two-wheeler, Passenger Car, Commercial Vehicle and Train) and Regional Analysis for 2026 - 2033

Traction Inverter Market Size and Trends Analysis

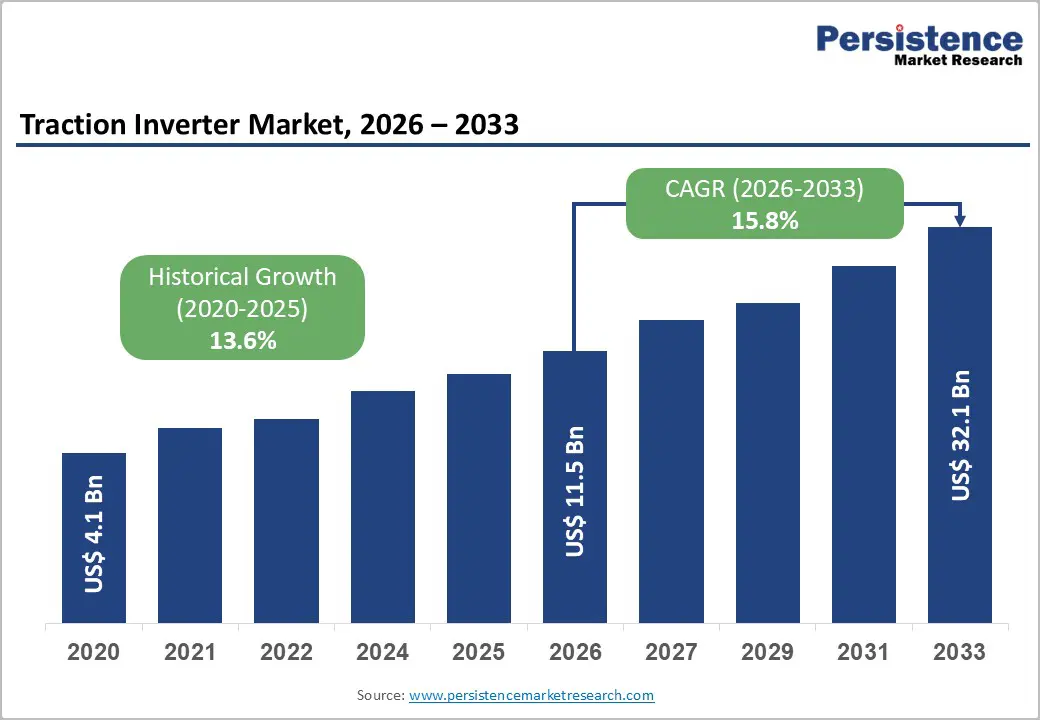

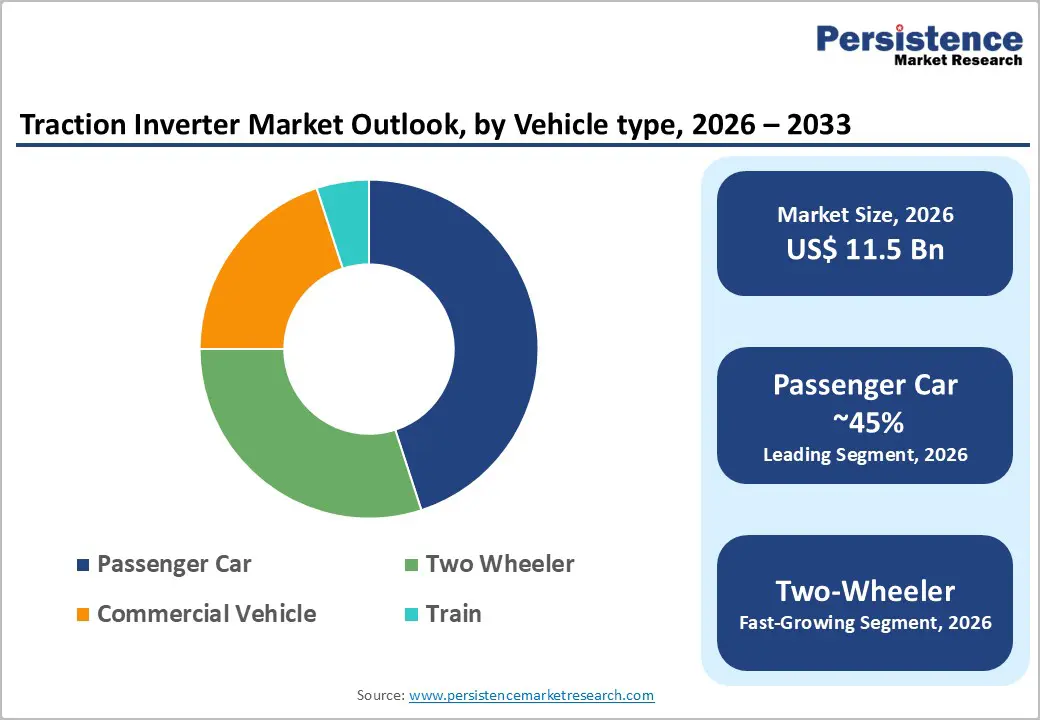

The global Traction Inverter Market size was valued at US$ 11.5 billion in 2026 and is projected to reach US$ 32.1 billion by 2033, growing at a CAGR of 15.8% between 2026 and 2033.

Market expansion is fundamentally driven by accelerating global electric vehicle adoption, rising government mandates for vehicle electrification, and advancing semiconductor technologies including silicon carbide and gallium nitride integration. The transition toward high voltage battery architectures supporting rapid charging capabilities, coupled with increasing commercial vehicle electrification including buses and trucks, establishes substantial demand drivers for advanced traction inverter solutions.

Key Industry Highlights:

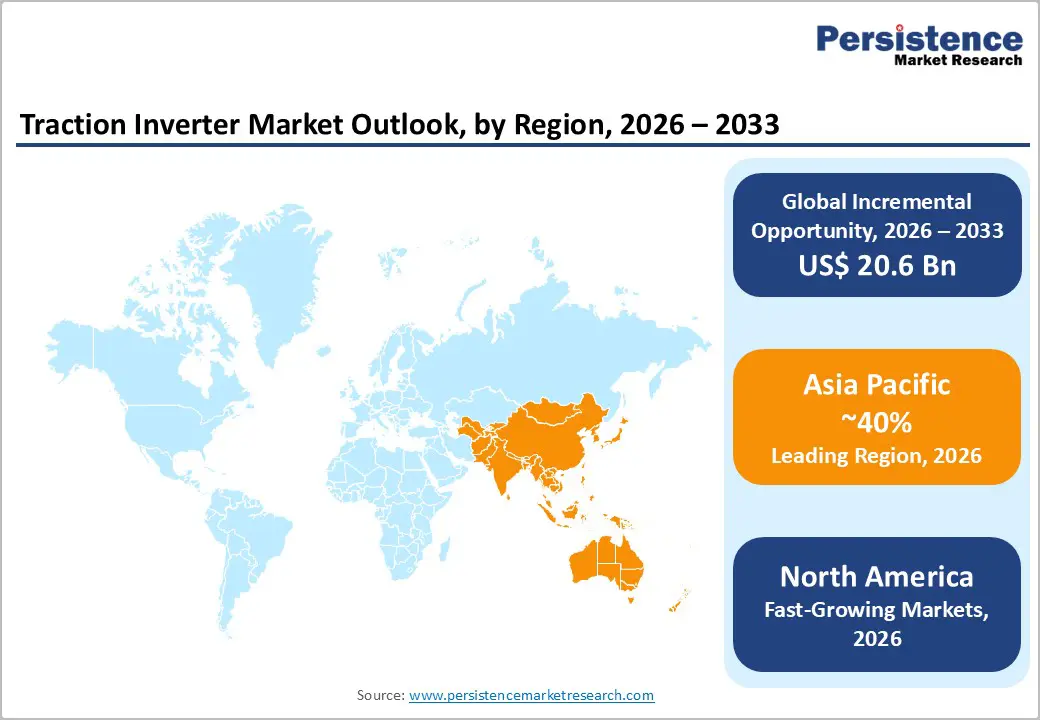

- Asia Pacific Regional Dominance: Asia Pacific commanding 40% global market share with 17% CAGR growth led by China (19.8% CAGR) and India (18.4% CAGR) establishing region as primary growth and manufacturing center globally.

- BEV Segment Leadership with HEV Growth: Battery Electric Vehicle segment commanding 74% market share while Hybrid Electric Vehicle segment growing fastest at 15% CAGR reflecting transition market dynamics across emerging and developed economies.

- two Wheeler Fastest Growing Vehicle Category: Two and three-wheeler segment expanding at 30% CAGR driven by India's FAME II program supporting 2.5 million annual electric two wheeler sales by 2027 establishing high volume emerging market opportunity.

- Silicon Carbide Technology Penetration: SiC semiconductor adoption increasing from 28% BEV market penetration in 2023 to projected 50% by 2028 driven by efficiency advantages supporting 0.5gram per kilometre vehicle range improvement justifying premium pricing.

- Commercial Vehicle Electrification Opportunity: Commercial vehicle segment growing at 22% CAGR through 2033 capturing USD 8 billion cumulative traction inverter market opportunity as global electric bus and truck adoption accelerates.

- In-house OEM Development Acceleration: Major automotive manufacturers including Volkswagen, Tesla, BYD, and emerging competitors investing USD 15 billion cumulatively in proprietary inverter development reflecting strategic supply chain security and intellectual property control priorities.

| Key Insights | Details |

|---|---|

|

Traction Inverter Market Size (2026E) |

US$ 11.5 Bn |

|

Market Value Forecast (2033F) |

US$ 32.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

15.8% |

|

Historical Market Growth (CAGR 2020 to 2024) |

13.6% |

Market Dynamics

Growth Drivers

Rapid Global Electric Vehicle Adoption and Production Scaling

Global electric vehicle sales expanding at unprecedented rates, with BEV market share exceeding 14 million units annually in 2025 and projected growth to 35 million units by 2030, establishes primary demand for traction inverter deployment. European BEV market registrations surging 34% in first half of 2025, driven by regulatory mandates including EU internal combustion engine phaseout targets by 2035, create sustained demand across passenger and commercial vehicle segments. China's EV market expanding at 19.8% CAGR through 2033, supported by government subsidies, manufacturing incentives, and domestic OEM production scaling exceeding 15 million vehicles annually, establishes largest regional market opportunity. India's electric vehicle market growth at 18.4% CAGR, driven by FAME II program allocating USD 1.4 billion for electric two and three wheeler manufacturing incentives, creates high volume emerging market opportunity.

Advanced Semiconductor Technology Integration and Efficiency Improvements

Silicon carbide and gallium nitride semiconductor adoption enabling 25% efficiency improvements and 20% energy consumption reduction in EV drivetrains establishes critical differentiator for automotive original equipment manufacturers seeking competitive advantage. Sic based inverters capturing 28% of BEV market in 2023 and projected to exceed 50% penetration by 2028, driven by superior thermal performance, reduced power losses, and improved driving range capabilities motivating widespread adoption across OEM platforms. GaN semiconductor technology adoption accelerating for onboard chargers and DCDC converters, with potential penetration in traction inverter applications by 20272028 as manufacturing maturity improves and costs decline. 800volt battery architecture adoption by premium and mass market automotive manufacturers, requiring high performance semiconductor solutions enabling rapid charging with 1080% battery capacity in under 20 minutes, drives substantial inverter technology advancement requirements. Thermal management system integration with advanced power electronics supporting compact modular inverter designs, reducing weight by 15% and enhancing vehicle packaging efficiency further accelerates technology driven market growth.

Government Electrification Mandates and Infrastructure Investment

Global government commitments supporting vehicle electrification including net zero emission targets mandating ICE phaseout across developed markets by 20352040 establish regulatory framework ensuring sustained demand. European Union automotive regulations require average fleet CO2 emissions reduction to 49.5 g/km by 2030, with enforcement mechanisms including substantial manufacturer penalties exceeding USD 95 per vehicle per g/km excess, drive accelerated EV adoption across all vehicle categories. U.S. Infrastructure Investment and Jobs Act allocating USD 7.5 billion for EV charging infrastructure deployment combined with federal tax credits supporting consumer EV purchase incentives accelerate market adoption in North America. India's government targeting 70% commercial vehicle fleet electrification by 2030 and China's domestic EV market development strategies prioritizing battery and inverter technology advancement establish structural demand foundations supporting regional market expansion through 2033.

Market Restraints

High Component Costs and Supply Chain Vulnerabilities

Advanced traction inverter system costs ranging from USD 1,500 to USD 4,000 per vehicle depending on semiconductor technology and voltage architecture, creating 815% contribution to total vehicle manufacturing cost limiting adoption in price sensitive emerging markets. Silicon carbide and gallium nitride semiconductor supply constraints with global production capacity insufficient to meet 20252026 demand projections by estimated 2025% threaten scaling timelines for OEMs. Raw material cost volatility including rare earth elements and semiconductor precursor materials creating ±1015% cost uncertainty in annual inverter procurement constrains manufacturer margin planning. Geopolitical trade restrictions and supply chain concentration in China and Taiwan representing 60%+ of global semiconductor manufacturing capacity create procurement vulnerability for Western automotive manufacturers.

Technical Integration Challenges and Thermal Management Complexity

Advanced semiconductor integration requires sophisticated thermal management systems to maintain junction temperatures below 150175°C under full load operating conditions and increases design and engineering complexity. Reliability and durability validation requirements for high power semiconductor devices demanding 2–3year qualification cycles before mass production authorization delay TimeTarget for emerging technology solutions. Integration challenges combining inverters, motors, and transmissions into unified eaxle modules requiring new manufacturing processes and assembly procedures limit production flexibility among existing automotive suppliers.

Market Opportunities

Commercial Vehicle and Heavy Duty Electrification Expansion

Commercial vehicle electrification segment emerging as fastestgrowing application category with projected 22% CAGR through 2033 driven by government mandates including EU heavyduty vehicle CO2 reduction targets and China's commercial fleet electrification programs. Electric bus and truck market expanding at 28% CAGR globally, with China deploying over 500,000 electric buses cumulatively by 2025 and India planning similar scale expansion establishing USD 8 billion cumulative traction inverter opportunity through 2033.

Last mile delivery vehicle electrification supporting ecommerce logistics expansion across emerging markets creates USD 23 billion opportunity for integrated invertermotor solutions. Public transportation system electrification initiatives including electric train and light rail deployment across Asia Pacific and Europe represent specialized high power inverter applications capturing USD 4 billion market opportunity.

Two Wheeler and Three Wheeler Emerging Market Growth

Two and three wheeler electrification representing fastestgrowing vehicle segment globally with projected 32% CAGR through 2033 driven by India's FAME II program supporting 2.5 million electric two wheeler sales annually by 2027 and China's mature e bike and e scooter market supporting 50 million annual unit sales. Cost effective inverter solutions required to create mass market opportunity for simplified semiconductor architectures using standard silicon based designs capturing USD 35 billion cumulative market opportunity through 2033.

Fleet operator cost sensitivity driving demand for extended battery life and operational efficiency optimization incentivizes advanced inverter development supporting reduced energy consumption and maintenance requirements. Government subsidies and deployment incentives across India, Southeast Asia, and Africa supporting electric two wheeler adoption as primary last mile transportation solution establish sustainable demand foundations supporting emerging supplier commercialization.

Segmentation Analysis

Propulsion Type Analysis

Battery Electric Vehicle (BEV) segment commanding 74% market share establishes dominant propulsion category, driven by superior efficiency, zero operational emissions, and regulatory policy support across developed and emerging markets. BEV inverter requirements emphasize high efficiency semiconductor technology and compact thermal management design supporting extended driving range and rapid charging capabilities reinforcing technology leadership positioning. BEV market growth accelerated at 25% CAGR supported by expanding charging infrastructure, declining battery costs, and increasing model variety across price segments.

Hybrid Electric Vehicle (HEV) segment growing fastest at 18% CAGR, driven by transition market positioning in emerging economies with limited charging infrastructure and premium market segments leveraging hybrid technology for performance optimization. HEV inverter designs emphasizing cost optimization and simplified semiconductor architectures supporting mass market adoption across price sensitive consumer segments.

Semiconductor Material Technology Analysis

Silicon carbide material commanding dominant positioning in premium and performance vehicle segments with 28% penetration in BEV market in 2023 and projected growth to 50% by 2028 reflecting superior thermal performance, efficiency advantages, and reliability characteristics preferred by premium OEMs. SiC technology enabling 0.51 gram per kilometer range improvement per vehicle justifying USD 500 per vehicle cost premium in premium segments.

Gallium Nitride material emerging as fastestgrowing semiconductor category with projected 35% CAGR through 2033 driven by advancing substrate technology, vertical device development, and cost reduction supporting 400600V application expansion. Traditional silicon technology maintaining significant positioning in cost optimized platforms and emerging market applications capturing 3540% market share through 2033 where cost considerations outweigh efficiency optimization priorities.

Vehicle Type Analysis

Passenger car segment commanding 45% market share establishing dominant application category driven by global vehicle production exceeding 80 million units annually with increasing EV penetration from 15% in 2024 to projected 40% by 2030. Passenger car inverter demand emphasizing compact design, cost optimization, and multiplatform scalability supporting efficient OEM manufacturing across diverse model lineups. Two wheeler segment emerging as fastestgrowing vehicle category with projected 32% CAGR through 2033 driven by India's electric two wheeler market expansion from 2.5 million units in 2024 to 810 million units by 2030.

Commercial vehicle segment growing at 22% CAGR supported by electric bus and truck adoption across China, Europe, and emerging markets requiring high power inverter solutions supporting sustained operational performance. Train and rail vehicle segment represents specialized high power application category with growing adoption of electric locomotives and light rail systems establishing USD 12 billion niche market opportunity.

Regional Market Insights

North America Traction Inverter Market Trends

North America commanding estimated 20% global market share with growth rate of 14% CAGR driven by U.S. government EV incentive programs, charging infrastructure investment, and major automotive manufacturer EV platform expansion. United States market dominated by Tesla's proprietary inverter technology and expanding production capacity exceeding 2 million vehicles annually, coupled with traditional OEM investments including Ford, General Motors, and Stellantis expanding domestic EV manufacturing facilities. Infrastructure Investment and Jobs Act allocating USD 7.5 billion for EV charging deployment establishing regulatory foundation supporting sustained EV adoption and traction inverter demand through 2033. Federal EV tax credits providing USD 7,500 consumer incentives reducing vehicle purchase barriers and accelerating adoption across diverse consumer segments.

Automotive supplier ecosystem supporting advanced semiconductor integration with established partnerships between traditional inverter suppliers including Bosch, Continental, and emerging technology leaders developing next generation solutions. Research and development investments across North American universities and technology centers supporting innovation in thermal management, semiconductor design, and integrated powertrain architectures strengthening competitive positioning.

Europe Traction Inverter Market Trends

Europe represents estimated 22% global market share with highest regional growth at 16% CAGR driven by EU regulatory mandates, green energy transition commitments, and automotive manufacturer concentration supporting EV platform development. German market leadership reflecting 35% European market share through automotive OEM presence including Volkswagen, BMW, Mercedes Benz, and established supplier ecosystem including Siemens, Infineon, and Bosch. European Union fleet CO2 emission regulations requiring 49.5 g/km average by 2030 with manufacturer penalty structure exceeding USD 95 per vehicle per gram excess establishing structural demand driver ensuring sustained EV investment through regulatory compliance. United Kingdom market growth at 14% CAGR supported by ICE phaseout targets and government charging infrastructure investment.

France and Spain emerging as secondary growth markets with government EV incentive programs and automotive manufacturing capability supporting regional supply chain development. European semiconductor manufacturers including Infineon, ST Microelectronics, and power.one expanding SiC and GaN manufacturing capacity supporting regional supply chain resilience and technology advancement. Battery manufacturing ecosystem development including Gigafactory operations across multiple countries creating integrated value chain supporting OEM efficiency and supply security.

Asia Pacific Traction Inverter Market Trends

Asia Pacific dominating global market commanding 40% market share with strongest regional growth projection at 17% CAGR driven by massive EV production concentration, government electrification mandates, and emerging technology manufacturing leadership. China maintaining dominant regional position with estimated 45% Asia Pacific market share reflecting world's largest EV production supporting 14 million annual unit output with BEV market share exceeding 70% of global production. China's "Made in China 2025" strategy and 14th Five Year Plan prioritizing battery and inverter technology advancement establishing government backed development programs supporting domestic supplier capability building. China's traction inverter market growth at 19.8% CAGR driven by government EV production targets, domestic OEM expansion, and technology partnerships between Chinese automakers and international semiconductor suppliers. India's electric vehicle market growth at 18.4% CAGR representing fastestgrowing national market globally, supported by FAME II program allocating USD 1.4 billion for electric two and three wheeler incentives. India's electric two wheeler market expanding from 2.5 million units in 2024 to projected 8 million units by 2030 creating massive emerging market opportunity for cost effective inverter solutions. Japan's specialized positioning emphasizing precision manufacturing and advanced technology integration with Nissan, Toyota, and Honda driving hybrid and EV innovation. Southeast Asian manufacturing expansion including Vietnam and Thailand supporting regional supply chain development and emerging market penetration.

Traction Inverter Market Competitive Landscape

The traction inverter market demonstrates moderate consolidation with leading global suppliers including Bosch, Continental, Siemens, DENSO, and Hitachi collectively commanding estimated 35% global market share. Bosch established market leadership position through advanced SiC inverter technology and major OEM supply partnerships supporting 15% estimated global market share. Chinese manufacturers including BYD, SAIC, and specialized suppliers competing through cost effective positioning and domestic OEM integration advantages capturing 20% market share in Asian markets.

Market structure reflects substantial engineering expertise requirements, automotive qualification complexity, and integrated supply chain capabilities creating barriers protecting established manufacturers. Emerging technology suppliers including power semiconductor specialists and automotive electronics innovators penetrating market through specialized technology differentiation and OEM partnership development supporting competitive dynamics evolution.

Key Industry Developments

- In November 2024, Hillcrest Energy Technologies announced its Zero Voltage Switching (ZVS) traction inverter prototype aimed at improving cost efficiency for EV manufacturers. The prototype boasts a die area of just 3 mm²/kW, which is below the industry target for future models. This innovation is expected to reduce production costs while enhancing performance significantly.

- In September 2024, STMicroelectronics announced the launch of its fourth generation STPOWER silicon carbide (SiC) MOSFET technology, specifically designed for next generation EV traction inverters. This new technology aims to enhance power efficiency and density, making it suitable for a broader range of electric vehicles, including midsize and compact models.

Companies Covered in Traction Inverter Market

- Siemens AG

- Infineon Technologies AG

- Continental AG

- Robert Bosch GmbH

- Delphi Technologies

- Hitachi Automotive Systems

- Mitsubishi Electric Corporation

- Toshiba Corporation

- Texas Instruments Incorporated

- ABB Ltd

- Others Key Players

Frequently Asked Questions

The Traction Inverter market is estimated to be valued at US$ 11.5 Bn in 2026.

The key demand driver for the Traction Inverter market is the rapid and sustained growth in electric vehicle (EV) adoption worldwide, driven by environmental regulations, government incentives, and shifting consumer preferences toward sustainable and efficient transportation.

In 2026, the Asia Pacific region will dominate the market with an exceeding 40% revenue share in the global Traction Inverter market.

Among the Vehicle Type, Passenger Car hold the highest preference, capturing beyond 45% of the market revenue share in 2026, surpassing other Vehicle Type.

The key players in Traction Inverter are Siemens AG, Infineon Technologies AG, Continental AG, Robert Bosch GmbH and Delphi Technologies.