- Smart Packaging

- Insulated Cup Sleeves Market

Insulated Cup Sleeves Market Size, Share, and Growth Forecast, 2026 - 2033

Insulated Cup Sleeves Market by Material (Kraft Paper, Coated Paper, Others), Product Type (Disposable, Reusable, Others), End-user, and Regional Analysis for 2026 - 2033

Insulated Cup Sleeves Market Size and Trends Analysis

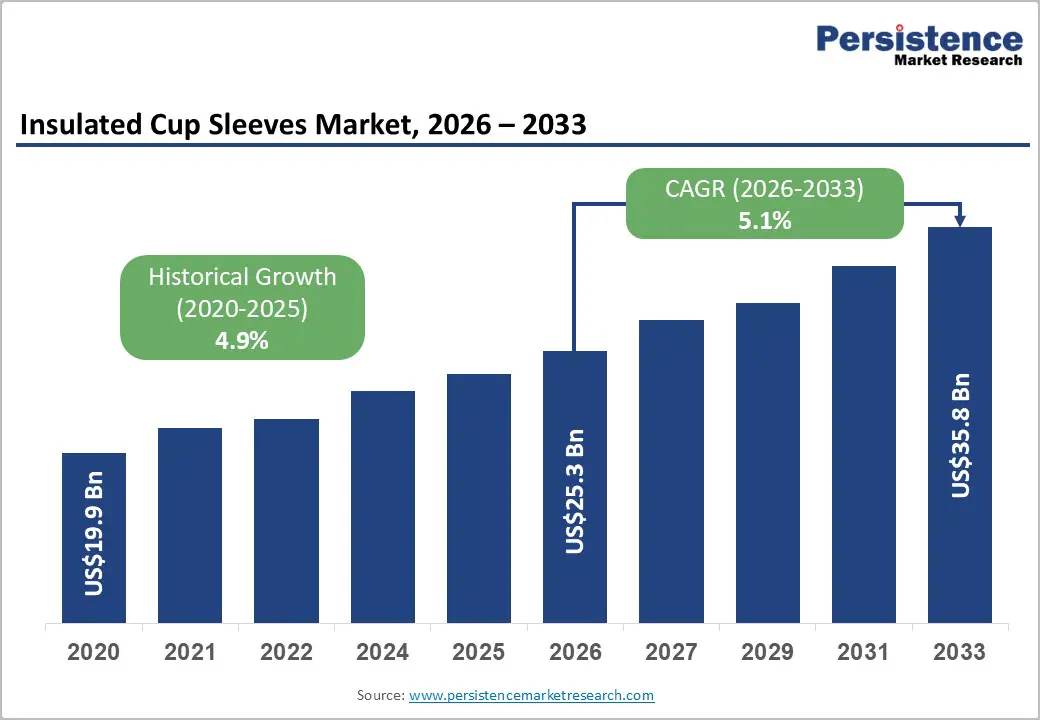

The global insulated cup sleeves market is projected to reach US$25.3 billion in 2026 and expand to US$35.8 billion by 2033, growing at a CAGR of 5.1% during the forecast period, driven by the rapid expansion of on-the-go beverage consumption, increasing adoption of recyclable and reusable packaging, and rising demand for premium, brand-customized sleeve solutions.

Supply-side enhancements in manufacturing efficiency, particularly in the Asia Pacific, and innovations in multi-wall, reusable, and silicone sleeves further support volume growth. Regulatory and corporate sustainability initiatives are fostering the adoption of eco-friendly materials, reinforcing long-term structural demand.

Key Industry Highlights

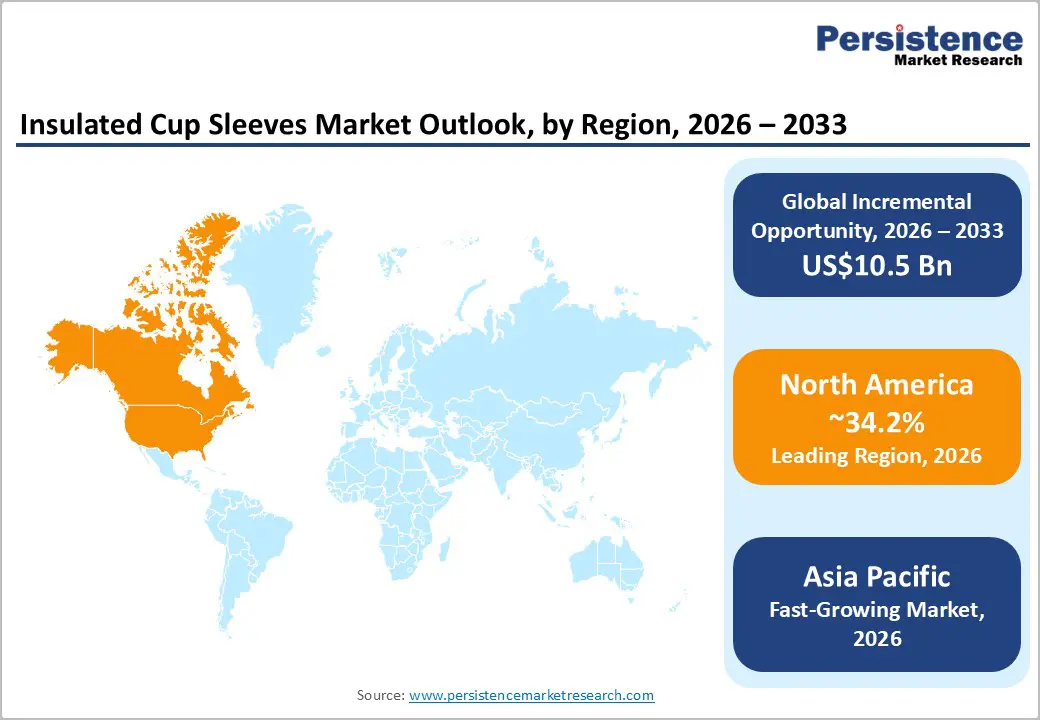

- Leading Region: North America is projected to hold 34.2% market share, driven by high per-capita coffee consumption, dense QSR networks, and large-scale procurement by chains such as Starbucks and Dunkin’, alongside expanding recyclable and reusable sleeve initiatives.

- Fastest-growing Region: Asia Pacific, projected to register the highest CAGR through 2033, supported by rapid café chain expansion in China and India, rising disposable incomes, and strengthening packaging sustainability regulations.

- Investment Plans: Industry participants are investing in recyclable water-based coatings, FSC-certified kraft sourcing, advanced digital printing systems, and vertically integrated supply chains to support branding customization and circular packaging compliance across North America and Europe.

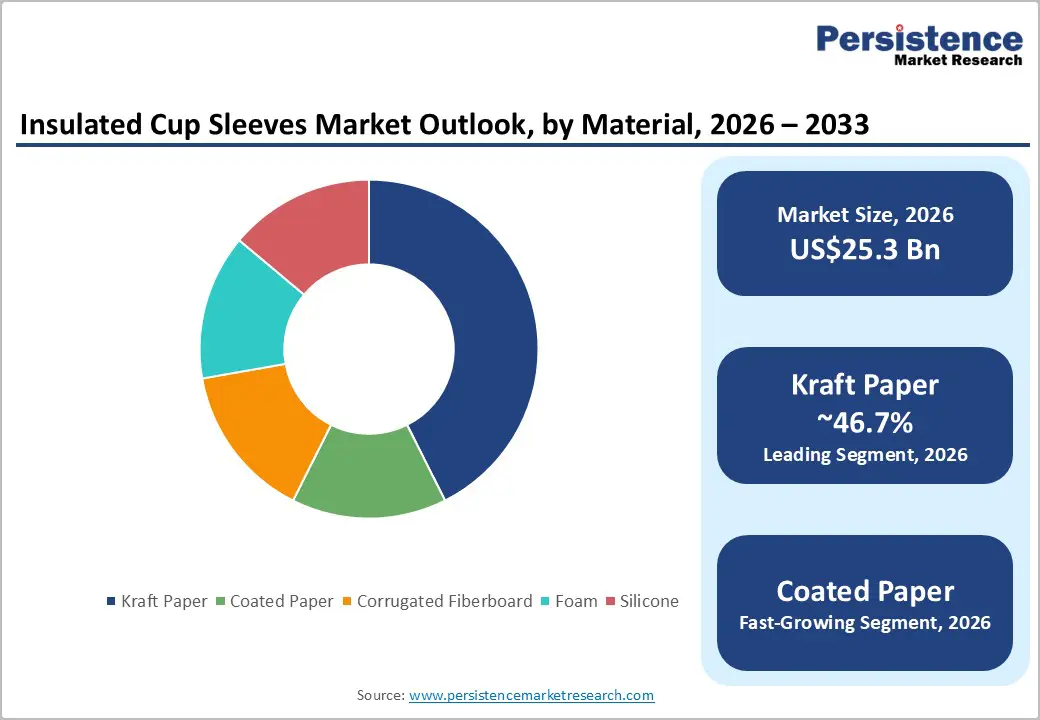

- Dominant Material: Kraft paper is anticipated to hold 46.7% of the market share, favored for cost efficiency, scalability, printability, and strong eco-friendly perception among global coffee chains and QSR operators.

- Leading Product Type: Disposable sleeves are anticipated to account for 63.8% of market share, supported by operational convenience, low per-unit cost, and compatibility with single-use takeaway beverage formats across high-footfall urban markets.

| Key Insights | Details |

|---|---|

| Insulated Cup Sleeves Market Size (2026E) | US$25.3 Bn |

| Market Value Forecast (2033F) | US$35.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of On-The-Go Beverage Consumption

The global coffee and takeaway beverage market has grown sharply due to urbanization, evolving work patterns, and the rise of specialty chains. Hot and cold beverage volumes are directly correlated with sleeve demand, as thermal protection and branding are essential for customer experience. Beverage price inflation incentivizes retailers to protect quality, further supporting sleeve adoption. Industry reports indicate consistent coffee consumption growth averaging 3-4% annually, creating a structural increase in unit demand.

Co-branded or private-label sleeve contracts with chain outlets capture the majority of incremental market volume. Sleeve demand is projected to rise in line with coffee and takeaway beverage sales, with premium chains driving adoption of customized sleeves.

Regulatory Pressure and Sustainability Mandates

Governments and municipalities are increasingly restricting single-use plastics and promoting recyclable or reusable materials. Fiber-based and compostable coatings are being adopted to comply with regulatory requirements. The European Union’s Single-Use Plastics Directive exemplifies a policy-driven adoption trend, prompting suppliers to innovate with recyclable-coated papers and reusable silicone sleeves. This creates a willingness to pay among buyers for compliant solutions and strengthens manufacturers' positions in offering environmentally aligned products. Material shifts toward Kraft, coated paper, and silicone increase supplier margins. Compliance with regulations offers differentiation and long-term market positioning.

Branding and Premiumization

Insulated cup sleeves serve as high-frequency branding and marketing tools. Cafes, QSRs, and beverage brands are increasingly using coated, embossed, or spot-varnish sleeves for promotions and loyalty programs. Premiumization supports higher per-unit prices and encourages suppliers to provide design services, inventory management, and just-in-time delivery. The trend is particularly evident in mature markets, where value-added sleeve SKUs have gained traction among major chains. Suppliers with premium and customizable offerings gain higher margins and long-term contracts, driving sector consolidation around quality-focused providers.

Barrier Analysis - Cost and Raw-Material Volatility

Price fluctuations in paper pulp, specialty coatings, and recycled feedstocks introduce input cost volatility, compressing margins. Small-scale operators may resist passing costs to consumers, which can slow the penetration of premium sleeves. Historical data indicate that when raw-material costs spike by 10-15% year-on-year, uptake of higher-priced SKUs is delayed. Larger suppliers mitigate risk through vertical integration or material hedging, while smaller operators remain highly price-sensitive.

Fragmented Buyer Specifications and Recycling Gaps

The lack of harmonized recycling infrastructure and heterogeneous buyer requirements complicates supply chain management. Sleeve recyclability rates can be reduced by 20-40% in regions with inconsistent systems. Compliance, verification, and third-party certifications add cost pressures. Suppliers must invest in verification, take-back programs, and buyer education to secure institutional contracts.

Opportunity Analysis - Reusable Sleeve Ecosystems and Subscription Models

Environmental regulations targeting single-use packaging waste, combined with corporate ESG commitments, are accelerating the development of structured reusable sleeve ecosystems. Silicone, neoprene, and textile-based sleeves are increasingly integrated into subscription-based beverage programs, workplace pantry services, university campuses, and large event venues, where daily consumption volumes justify reusable deployment. Deposit-return and incentive-driven models reduce loss rates and improve circulation efficiency, particularly in closed-loop environments such as corporate offices and co-working spaces.

Early pilot programs across North America and Europe indicate that high-frequency users can achieve breakeven within 12-24 months, depending on circulation rates and cleaning logistics. This financial viability strengthens the business case for QSR operators and specialty coffee chains seeking measurable reductions in their carbon footprints. Over time, reusable sleeves also enhance brand visibility through customization and co-branding, transforming them from purely functional accessories into marketing assets embedded within broader circular packaging strategies.

Material Innovation and Low-Impact Coatings

Advancements in fiber-based barrier coatings and compostable laminates are reshaping the performance profile of paper sleeves. Traditional polyethylene linings are increasingly replaced with water-based, dispersion, or bio-based coatings that maintain moisture resistance and structural stability while improving recyclability. These innovations enable sleeves to meet regulatory compliance standards in regions with strict packaging waste directives, without compromising thermal insulation or print clarity.

Suppliers investing in scalable, eco-friendly coating technologies benefit from stronger alignment with sustainable procurement policies adopted by multinational café chains and QSR operators. Certification readiness, including chain-of-custody documentation and recyclability validation, enhances supplier competitiveness. Premium coated formats also allow converters to command modest price premiums while supporting high-definition digital printing for limited-edition campaigns and seasonal promotions. As environmental scrutiny intensifies, material innovation serves as both a compliance enabler and a strategic differentiation lever within the market.

Category-wise Analysis

Material Insights

Kraft Paper is anticipated to account for approximately 46.7% of the market share in 2026, maintaining its leadership due to cost efficiency, eco-friendly perception, and wide availability of raw materials. Cafés and quick-service restaurant (QSR) chains such as Starbucks and McDonald's often specify Kraft sleeves as the default for hot beverage packaging. The material delivers reliable thermal insulation, strong structural integrity, and excellent printability for branding. Mature supply chains across North America and Asia ensure scalable production, stable pricing, and short lead times, reinforcing their dominance in high-volume consumption environments.

Coated Paper is projected to be the fastest-growing material segment, driven by premiumization trends and increasing demand for moisture resistance. Specialty coatings improve durability, water resistance, and visual appeal, enabling high-resolution graphics for seasonal promotions and limited-edition campaigns. Major beverage brands increasingly use coated sleeves to enhance shelf impact and customer engagement. Ongoing R&D in recyclable and water-based barrier coatings aligns with circular economy initiatives while maintaining print quality, expanding the segment’s addressable market across environmentally conscious regions.

Product Type Insights

Disposable sleeves are expected to capture approximately 63.8% of the market revenue in 2026, driven by high convenience, low per-unit cost, and compatibility with single-use paper cups. Large global coffee chains and QSR operators rely on disposable sleeves to streamline operations and ensure compliance with hygiene standards. Bulk procurement agreements and established logistics networks allow operators to maintain a consistent supply for daily replenishment. The format is particularly dominant in high-footfall urban cafés, transport hubs, and drive-through models where speed of service is critical.

Reusable sleeves, including silicone and textile variants, are expected to witness the fastest growth over the forecast period. Sustainability regulations in regions such as the European Union and corporate ESG commitments are accelerating adoption. Programs introduced by brands like Costa Coffee encourage customers to bring reusable accessories through incentive-based discounts. Workplace beverage programs, subscription coffee models, and hybrid office culture further stimulate demand. Over time, lifecycle cost savings and enhanced brand visibility through customizable designs strengthen the business case for reusable formats.

Regional Insights

North America Insulated Cup Sleeves Market Trends - Premiumization, Reuse Pilots, and Regulatory-Driven Fiber Shift

North America is anticipated to account for approximately 34.2% of revenue share in 2026, supported by high per-capita coffee consumption and a dense network of quick-service restaurants (QSRs) and specialty cafés. The U.S. remains the primary growth engine, with large chains such as Starbucks and Dunkin' procuring high volumes of disposable kraft and premium-coated sleeves to support daily footfall and seasonal promotional campaigns. In 2023, Starbucks expanded its North American reusable cup and returnable packaging pilots, reinforcing demand for compatible reusable sleeve formats and signaling a broader shift toward circular beverage packaging.

Growth in the region remains steady, anchored in premiumization trends, sustainability commitments, and private-label co-branding initiatives between coffee chains and consumer brands. State-level regulations such as California’s packaging waste reduction framework are influencing procurement strategies, encouraging recyclable fiber-based sleeves and discouraging non-recyclable foam formats. Canada is also advancing reuse systems, with brands like Tim Hortons piloting reusable cup programs in select provinces. These initiatives stimulate demand for durable silicone and textile sleeves while accelerating supplier investment in water-based coatings, digital printing, and vertically integrated converting facilities across the U.S. and Canada.

Europe Insulated Cup Sleeves Market Trends - EU Plastics Directive Compliance and Certified Fiber Innovation

Europe represents a regulation-driven and innovation-focused market, shaped strongly by the European Union Single-Use Plastics Directive and broader circular economy mandates. Key markets, including Germany, the U.K., France, and Spain, demonstrate distinct regulatory and consumer dynamics. Germany’s national packaging law and deposit-return culture encourage recyclable fiber-based sleeves and traceable chain-of-custody certification, prompting converters to adopt FSC-certified kraft and compostable barrier coatings.

In the U.K., brands such as Costa Coffee and Pret A Manger have expanded incentives for reusable cup programs, indirectly increasing consumer familiarity with reusable sleeve formats. France has implemented stricter in-store dining packaging rules, accelerating demand for compliant fiber-based alternatives. Spain combines tourism-driven beverage demand with sustainability campaigns, encouraging compostable and recyclable sleeve options in high-footfall urban areas.

Suppliers across Europe are investing in low-impact aqueous coatings and high-definition digital printing systems to meet brand customization needs while satisfying environmental certification standards, thereby strengthening supplier differentiation and compliance positioning.

Asia Pacific Insulated Cup Sleeves Market Trends - Rapid Café Expansion and Cost-Competitive Manufacturing Scale

Asia Pacific is projected to be the fastest-growing regional market, driven by rapid urbanization, rising disposable incomes, and aggressive café chain expansion across China, India, Japan, South Korea, and Southeast Asia. China leads regional consumption growth, supported by the expansion strategies of domestic brands such as Luckin Coffee and international operators, including Starbucks, which continues to expand store density in tier-1 and tier-2 cities. The resulting increase in takeaway beverage volumes directly boosts demand for cost-effective disposable sleeves while creating parallel opportunities for premium coated formats used in branded campaigns.

India is witnessing growth through chains such as Tata Starbucks and regional QSR brands, where organized café penetration remains comparatively low but is expanding quickly. Governments in markets such as Australia and South Korea are tightening packaging waste rules and promoting recycling targets, encouraging a shift toward recyclable kraft and innovative barrier coatings.

Manufacturing strength in China and Southeast Asia ensures cost-competitive production and export capacity, enabling regional suppliers to invest in advanced coating lines, automated die-cutting, and scalable digital printing infrastructure. As per-capita coffee consumption continues to rise, Asia Pacific’s higher CAGR relative to mature Western markets positions it as a strategic growth frontier for both domestic converters and multinational packaging firms.

Competitive Landscape

The global insulated cup sleeves market is moderately fragmented. Several multinational packaging companies hold significant shares via scale and chain partnerships, while regional converters provide local solutions. Top players account for the bulk of premium contracts, but smaller converters maintain niche offerings. Competition focuses on material innovation, sustainability credentials, speed-to-market, and custom branding services.

Leading suppliers prioritize sustainability, premiumization, and expansion into reusable/circular models, differentiating through coatings R&D, short-run digital print, and integrated logistics to support major chain rollouts.

Key Industry Developments:

- In September 2025, Coveris won the Green Packaging Star Award for its sustainable SleeveFlexR Stretch solution, a recyclable sleeve that contains up to 75% post-consumer recycled material and supports cleaner separation in recycling streams, reinforcing circular packaging adoption in beverage and related sectors.

Companies Covered in Insulated Cup Sleeves Market

- Graphic Packaging International

- WestRock Company

- Huhtamaki

- Georgia-Pacific

- Detpak

- International Paper

- Stora Enso

- Smurfit Kappa

- Mondi Group

- Sonoco Products Company

- Dart Container Corporation

- Pactiv Evergreen

- Genpak

- Lollicup USA

- Benders Paper Cups

- KapStone Paper and Packaging

- Hotpack Global

- BioPak

Frequently Asked Questions

The global insulated cup sleeves market is estimated to reach approximately US$25.3 billion in 2026.

By 2033, the insulated cup sleeves market is projected to reach approximately US$35.8 billion.

Key trends include the shift toward recyclable and compostable kraft materials, adoption of water-based and recyclable barrier coatings, growth of reusable silicone and textile sleeves, expansion of digital printing for brand customization, and regulatory-driven transition away from foam-based products in North America and Europe.

Kraft Paper is the leading material segment, anticipated to hold approximately 46.7% share in 2026, due to its cost efficiency, eco-friendly perception, printability, and compatibility with high-volume QSR procurement strategies.

The insulated cup sleeves market is expected to grow at a CAGR of 5.1% through 2033.

Major players include Graphic Packaging International, WestRock Company, Huhtamaki, Georgia-Pacific, and Detpak.