- Industrial Goods & Service

- Pre-Insulated Pipe Market

Pre-Insulated Pipe Market Size, Share, and Growth Forecast 2025 - 2032

Pre-Insulated Pipe Market Analysis By Product Type (Flexible Pre-insulated), Pipe Material (Steel, Copper, Plastic), Insulation Type (Polyurethane (PUR), Polyisocyanurate (PIR), Polyethylene (PE)) End-use, and Regional Analysis 2025 - 2032

Pre-Insulated Pipe Market Share and Trends Analysis

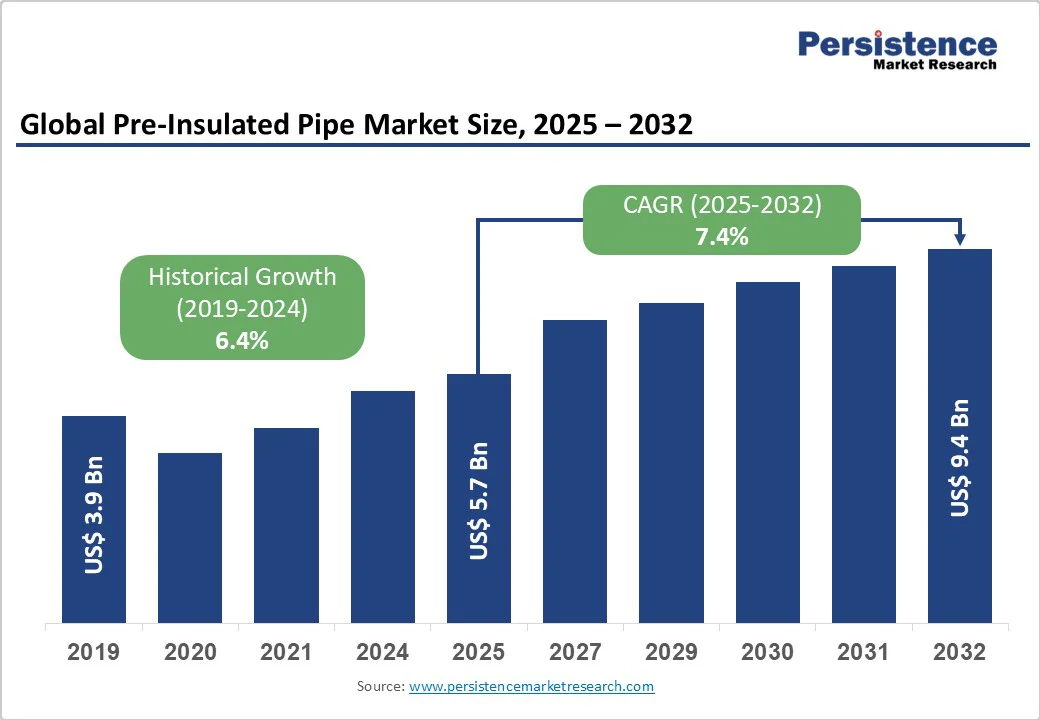

The global pre-insulated pipe market size is likely to value US$ 5.7 Billion in 2025 and is projected to reach US$ 9.4 billion by 2032, growing at a CAGR of 7.4% between 2025 and 2032.

The market expansion is primarily driven by growing demand for energy-efficient infrastructure solutions and rapid urbanization worldwide. Huge emphasis on district heating and cooling systems, particularly in Europe and the Asia Pacific, has accelerated the adoption of pre-insulated pipes to minimize thermal losses and optimize operational efficiency across residential, commercial, and industrial applications.

Key Market Highlights:

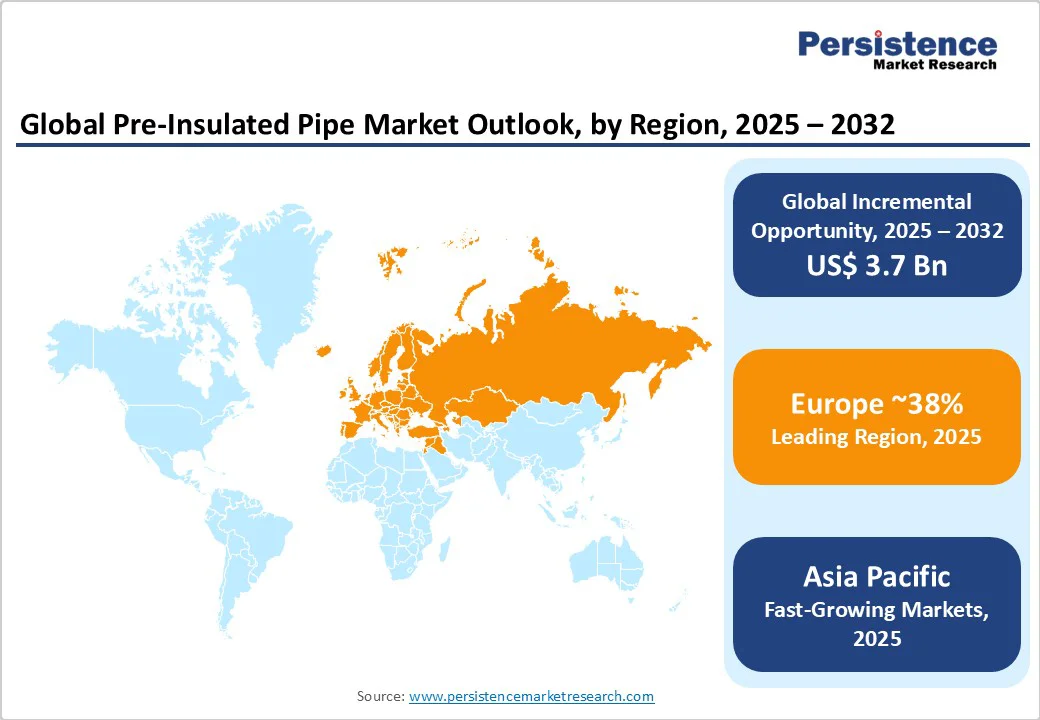

- Leading Region: Europe represents the largest regional market due to established district heating infrastructure, supportive regulatory frameworks, and aggressive decarbonization targets driving adoption of energy-efficient thermal distribution systems.

- Fastest-Growing Region: Asia Pacific emerges as the fastest-growing region driven by rapid urbanization, government infrastructure investments, and expanding industrial sectors requiring advanced thermal management solutions.

- Leading Product Type: Flexible Pre-Insulated Pipes dominate the product segments with a 72% market share, thanks to their superior installation advantages, reduced joint requirements, and adaptability to complex routing requirements.

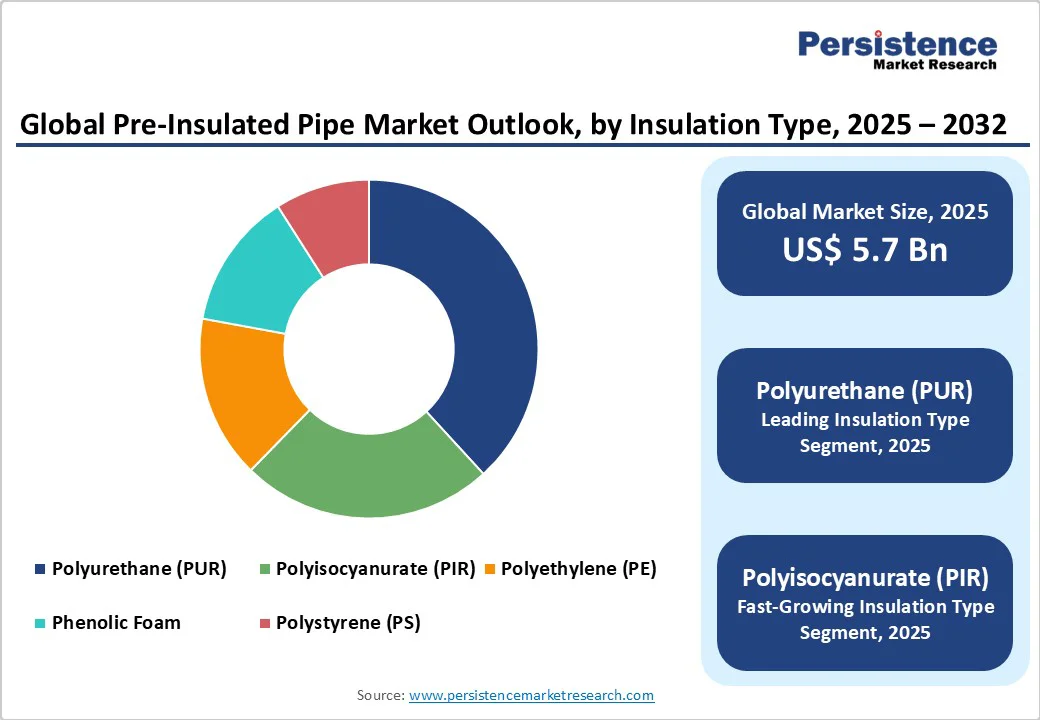

- Leading Insulation Type: Polyurethane (PUR) insulation leads the material segments with a 38% market share, due to its superior thermal conductivity, mechanical properties, and widespread industry acceptance across diverse applications.

- Leading End Use: District Heating and Cooling applications present the largest market opportunity through European leadership expansion and growing adoption across Asia Pacific urban development, which requires centralized thermal distribution systems.

| Key Insights | Details |

|---|---|

| Pre-Insulated Pipe Market Size (2025E) | US$5.7 billion |

| Market Value Forecast (2032F) | US$9.4 billion |

| Projected Growth CAGR (2025-2032) | 7.4% |

| Historical Market Growth (2019-2024) | 6.4% |

Market Dynamics

Driver - Rising Demand for Energy-Efficient Infrastructure Solutions

The global push towards sustainable development and energy conservation has emerged as a primary catalyst for the expansion of the pre-insulated pipe market. The European Union's Green Deal and stringent energy efficiency directives mandate the adoption of technologies that reduce heat loss and improve thermal performance in building systems. Pre-insulated pipes achieve energy savings of up to 40% compared to traditional uninsulated alternatives, making them essential for meeting regulatory standards.

The Copenhagen district heating model, powered by renewable energy sources and utilizing pre-insulated piping systems, demonstrates successful implementation of energy-efficient thermal distribution networks. Additionally, the growing focus on achieving Net Zero carbon goals by 2050 across developed nations has accelerated infrastructure modernization projects that incorporate advanced insulation technologies.

Rapid Urbanization and District Heating System Expansion

Accelerating urbanization rates, particularly across emerging economies, drive substantial demand for centralized heating and cooling distribution networks. The United Nations projects that 68% of the global population will reside in urban areas by 2050, necessitating efficient thermal management systems for densely populated regions.

China's district heating market covers over 100 million urban households, with an installed heat capacity exceeding 400 GW, representing annual growth rates of nearly 5%. Sweden maintains the highest district heating penetration with over 60% of urban households connected to nearly 300 district heating systems nationwide.

Pre-insulated pipes enable cost-effective implementation of centralized energy distribution by minimizing installation complexity and reducing long-term maintenance requirements across metropolitan developments.

Restraints - High Initial Capital Investment Requirements

The substantial upfront costs associated with pre-insulated pipe installations present significant barriers for market adoption, particularly in cost-sensitive construction and infrastructure projects. Initial setup costs for district cooling systems can be several times higher than those of conventional alternatives due to the extensive piping networks, thermal storage facilities, and centralized production requirements.

Small and medium-scale developments often favor traditional piping solutions due to budget constraints and limited access to financing for advanced thermal management technologies. This cost sensitivity particularly affects emerging markets where infrastructure investments compete with immediate development priorities.

Competition from Alternative Insulation Technologies

The growing availability of alternative insulation materials and installation methods creates competitive pressure on pre-insulated pipe systems. Cross-linked polyethylene and other eco-friendly materials offer comparable thermal performance with potentially lower material costs and simplified installation procedures.

Traditional on-site insulation applications offer flexibility in retrofitting existing infrastructure, eliminating the need for complete system replacement. Advanced spray foam technologies deliver superior performance in specific applications while offering customizable insulation thickness and coverage options that challenge standardized pre-insulated pipe specifications.

Market Opportunities

Integration with Renewable Energy Infrastructure

The accelerating transition towards renewable energy sources creates substantial growth opportunities for pre-insulated pipe systems in next-generation thermal distribution networks. Denmark leads globally in integrating solar thermal installations into district heating systems, with biomass currently accounting for 25% of heat generation expected to decline as industrial waste heat and heat pumps fill supply gaps.

Smart city initiatives increasingly incorporate district heating and cooling as key components of sustainable urban infrastructure, requiring high-performance piping systems for optimal energy distribution. India's approval of 12 new industrial smart cities in August 2024 demonstrates a growing government commitment to energy-efficient infrastructure development that supports pre-insulated pipe market expansion.

Industrial Process Optimization and Decarbonization

Expanding industrial applications across chemical processing, pharmaceuticals, food and beverage, and oil and gas sectors present significant market opportunities for specialized pre-insulated piping solutions. California's 2025 Title 24 energy code mandates the use of pipe insulation for process heating and cooling applications in industrial facilities, establishing a regulatory precedent for similar requirements in other jurisdictions.

Industrial facilities are increasingly prioritizing operational efficiency and reducing their carbon footprint, driving the adoption of advanced thermal management systems that minimize energy losses during fluid transportation. Cryogenic applications, including LNG facilities and medical oxygen distribution systems, require customized, pre-insulated pipes designed for ultra-low-temperature operations, representing high-value niche market segments.

Category-wise Insights

Product Type Analysis

Flexible Pre-Insulated Pipes dominate the market with approximately 72% market share, driven by superior installation advantages and adaptability to complex routing requirements. Flexible systems offer significant benefits, including reduced installation time, minimal joint requirements, and the capability for directional drilling applications in challenging terrains.

BRUGG Pipes' FLEXWELL system represents the only flexible pipe technology suitable for horizontal directional drilling, enabling installations in urban environments with minimal surface disruption. The flexibility advantage becomes particularly pronounced in retrofit applications where existing infrastructure constraints require adaptive routing solutions. Additionally, flexible pre-insulated pipes deliver lower total installation costs through reduced labor requirements and simplified connection procedures compared to rigid alternatives.

Pipe Material Analysis

Steel carrier pipes maintain the largest market share at approximately 45% due to superior mechanical strength, high-pressure capabilities, and established performance in district heating applications. Steel pipes demonstrate excellent durability under extreme temperature conditions and provide reliable long-term performance in demanding industrial environments. European Standard EN 253 specifically addresses bonded single pipe systems with steel service pipes, polyurethane thermal insulation, and polyethylene casing for directly buried hot water networks.

Copper materials are gaining traction in specialized applications that require corrosion resistance and thermal conductivity, particularly in the pharmaceutical and food processing industries. Plastic alternatives, including PE100 and PP-R materials, show rapid growth due to lightweight properties, corrosion resistance, and cost-effectiveness in residential and commercial applications.

Insulation Type Analysis

Polyurethane (PUR) insulation holds approximately a 38% market share due to its superior thermal performance characteristics and widespread industry acceptance. PUR foam provides thermal conductivity coefficients as low as 0.020 W/mK, ensuring minimal heat loss during fluid transportation across extended distribution networks. The closed-cell structure delivers excellent mechanical properties, moisture resistance, and dimensional stability under varying temperature conditions.

Polyisocyanurate (PIR) insulation demonstrates growing adoption in high-temperature applications exceeding 140°C, offering enhanced fire resistance and thermal stability compared to standard polyurethane formulations. Advanced HFO PUR foam incorporating Hydrofluoroolefins as foaming agents provides very low environmental impact while maintaining superior insulation performance characteristics.

End-use Analysis

District Heating and Cooling applications represent approximately 35% of market demand, driven by European leadership in centralized thermal distribution systems and expanding adoption across Asia Pacific urban developments. Europe maintains an over 134 billion market value in district heating, with countries like Denmark, Sweden, and Germany achieving high penetration rates through supportive regulatory frameworks.

The oil and Gas pipe sector accounts for a significant share through offshore pipeline applications and onshore thermal management requirements for crude oil and natural gas transportation. Industrial Process Piping demonstrates consistent growth across chemical processing, food and beverage, pharmaceutical, and manufacturing applications requiring precise temperature control and energy efficiency optimization.

Regional Insights

North America Pre-Insulated Pipe Market Trends

North America demonstrates strong market potential through infrastructure modernization initiatives and increasing investments in energy-efficient building systems. The United States leads regional development with California's 2025 Title 24 energy code mandating pipe insulation for industrial process applications, establishing regulatory precedent for nationwide adoption. Memphis Light, Gas, and Water's US$ 30 million gas infrastructure modernization project in January 2025 includes 5.4 miles of new 24-inch high-pressure pipeline replacing aging infrastructure.

Canada supports market growth through municipal energy initiatives and district energy system expansion in major metropolitan areas. The region benefits from strong regulatory frameworks promoting energy conservation and sustainability standards that favor advanced piping technologies. Smart city developments across North America increasingly integrate district heating and cooling systems as core infrastructure components, driving consistent demand for high-performance pre-insulated piping solutions.

Europe Pre-Insulated Pipe Market Trends

Europe maintains global leadership in pre-insulated pipe market development through comprehensive regulatory support and established district heating infrastructure. Germany received European Commission approval for a US$3.13 billion plan to boost green district heating based on waste heat and renewable energy sources in August 2022. Denmark achieves the highest district heating penetration globally, with 70% of households connected to district heating systems, compared to 15% in Germany.

Poland demonstrates significant market expansion through decarbonization initiatives and biomass district heating projects, with DP securing Poland's biomass district heating project featuring a 12.5 MW boiler installation. The European Union's Green Deal and energy efficiency directives create mandatory requirements for sustainable heating technologies, establishing favorable market conditions for pre-insulated pipe adoption across residential, commercial, and industrial sectors.

Asia Pacific Pre-Insulated Pipe Market Trends

Asia Pacific represents the fastest-growing regional market driven by rapid urbanization, government-led infrastructure investments, and expanding industrial sectors. China dominates regional development as the world's largest district heating market by volume, with government data reporting an installed heat capacity of over 400 GW and annual growth rates of nearly 5%. SP Group received a 10-year contract worth approximately US$ 16.7 million to operate Chengdu Future Medical City's district cooling and heating system in December 2024.

India demonstrates substantial growth potential through Smart Cities Mission and National Infrastructure Pipeline initiatives promoting energy-efficient infrastructure development. The country's urban population is expected to reach 600 million by 2031, creating significant demand for centralized thermal distribution systems. South Korea and Japan contribute to regional market expansion through technological innovation and modernization of existing infrastructure to meet energy efficiency standards and environmental regulations.

Competitive Landscape

The global pre-insulated pipe market exhibits moderate consolidation with leading manufacturers maintaining significant market shares through technological innovation, strategic partnerships, and comprehensive product portfolios. Market concentration reflects the technical expertise required for advanced insulation technologies and the substantial capital investments necessary for global manufacturing and distribution capabilities. Leading companies differentiate through proprietary insulation formulations, specialized installation systems, and comprehensive technical support services.

Strategic acquisitions and joint ventures enable market participants to expand geographical presence and enhance technological capabilities across diverse end-use applications. Emerging business models focus on turnkey project solutions, comprehensive lifecycle support, and integration with smart monitoring technologies for enhanced system performance and predictive maintenance capabilities.

Key Market Developments

- In March 2025, Uponor showcased its new Ecoflex VIP 2.0 pre-insulated pipe system at ISH Frankfurt, featuring cutting-edge Vacuum Insulated Panel (VIP) technology that delivers industry-leading thermal performance with a smaller outer diameter, enabling faster and more sustainable installations.

- In January 2025, BRUGG Pipes USA announced the successful start of production for the CALPEX PUR-KING high-performance flexible pipe system at its Joliet, Illinois, facility, reducing lead times and strengthening local service capabilities in North American markets.

- In August 2024, India approved 12 new industrial smart cities and infrastructure projects aimed at boosting the manufacturing ecosystem, thereby creating substantial demand for energy-efficient piping systems in urban development initiatives.

Companies Covered in Pre-Insulated Pipe Market

- Aquatherm

- Brugg Group

- Brugg Pipesystems

- CPV Ltd.

- Durotan

- Flexalen

- Georg Fischer

- Insulcon

- Isoplus

- Uponor

- FEB

- Pipelife International

- Thermaflex

- Danfoss

- Armacell

- LOGSTOR

- Watts Water Technologies

- Thermal Pipe Systems Inc.

- Perma-Pipe International Holdings Inc.

- Polypipe

Frequently Asked Questions

The global Pre-Insulated Pipe Market is projected to reach US$ 9.4 billion by 2032, growing from US$ 5.7 billion in 2025 at a CAGR of 7.4% during the forecast period.

Key demand drivers include rising demand for energy-efficient infrastructure solutions, rapid urbanization driving district heating system expansion, stringent regulatory requirements for thermal efficiency, and integration with renewable energy infrastructure developments.

Flexible Pre-Insulated Pipes dominate the market with approximately 72% market share due to superior installation advantages, reduced joint requirements, and adaptability to complex routing requirements in urban environments.

Europe represents the largest regional market through established district heating infrastructure, comprehensive regulatory support, and aggressive decarbonization targets. Denmark achieves 70% household connection rates to district heating systems.

Major opportunities include integration with renewable energy infrastructure, industrial process optimization and decarbonization, smart city developments, and expansion across emerging markets with growing urbanization rates.

Leading market players include Aquatherm, BRUGG Group, Georg Fischer, Uponor, Thermaflex, Danfoss, Armacell, LOGSTOR, Pipelife International, and Isoplus, among others, offering comprehensive product portfolios and global market presence.