- Home Care & Utilities

- Insulated Drinkware Market

Insulated Drinkware Market Size, Share, and Growth Forecast 2026 - 2033

Insulated Drinkware Market by Product (Water Bottles, Cans, Mugs), Material (Stainless Steel, Plastic-Insulated), Capacity (<500 mL, 750 mL, 1 Liter, 1.25 Liters to 2 Liters, Above 2 Liters), Sales Channel (Supermarkets & Hypermarkets, Convenience Stores, Specialty Stores, Online Stores, Other Channels), and Regional Analysis, 2026 - 2033

Insulated Drinkware Market Size and Trend Analysis

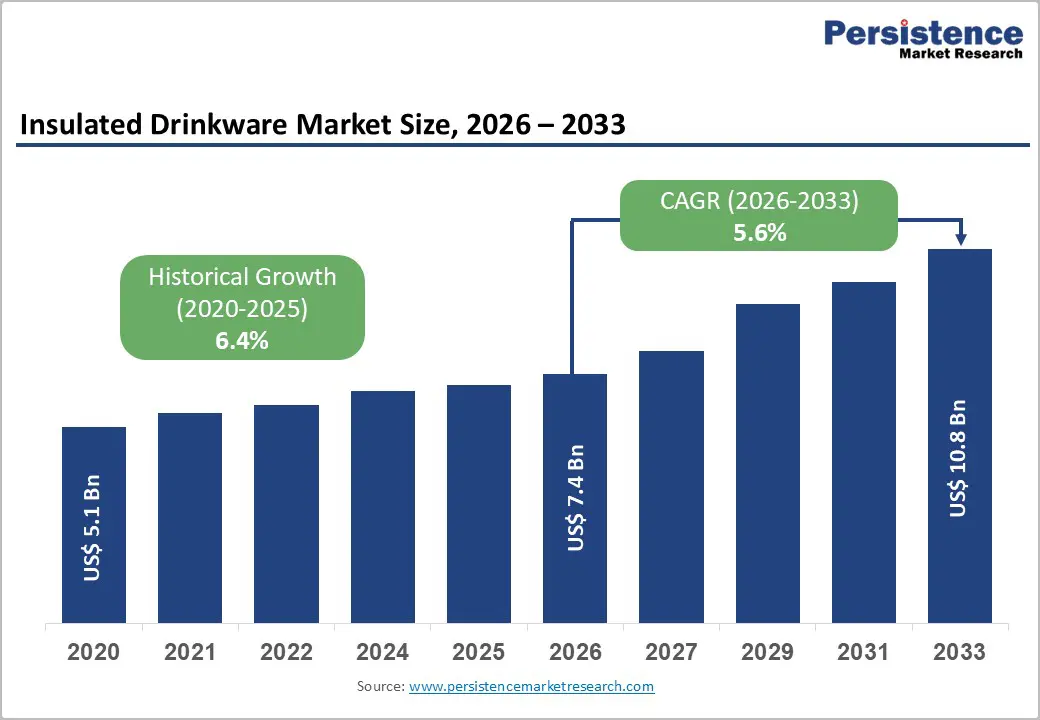

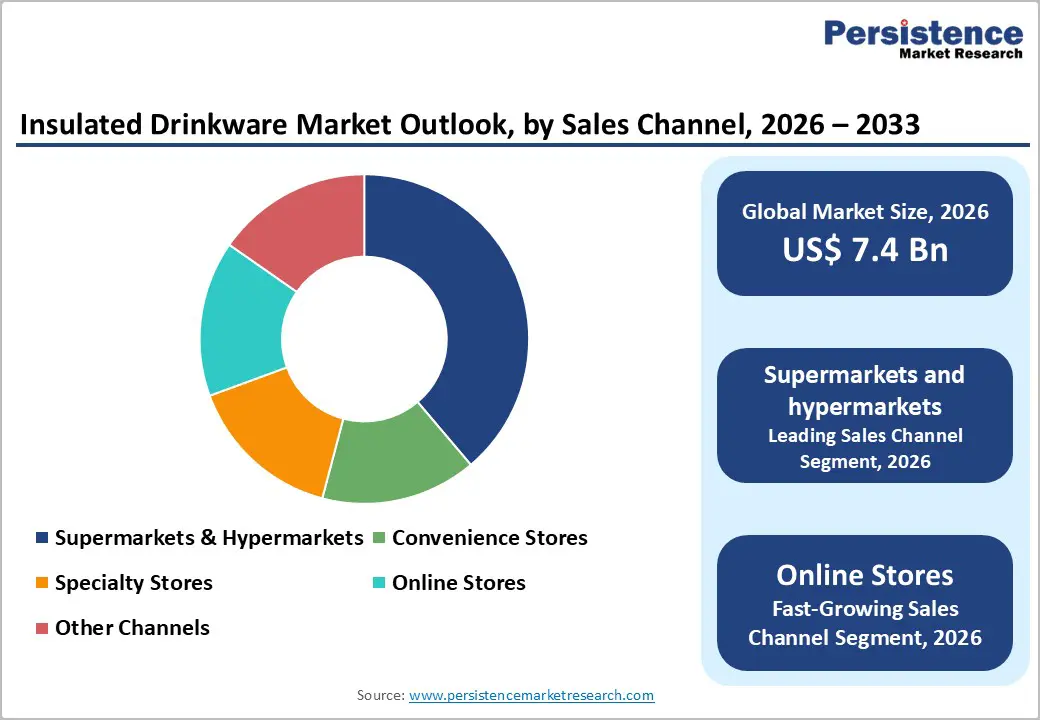

The global insulated drinkware market size is expected to be valued at US$ 7.4 billion in 2026 and projected to reach US$ 10.8 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

This sustained expansion is primarily underpinned by heightened consumer awareness around health and hydration, accelerating the adoption of sustainable reusable products in the wake of global single-use plastic bans, and a robust rise in outdoor and fitness lifestyle activities. Premiumization trends, with consumers willing to invest in high-performance, aesthetically crafted products, alongside strong e-commerce proliferation, are reinforcing consistent revenue generation across all major geographies. The historical period (2020-2025) recorded a CAGR of 6.4%, reflecting the category’s resilience even through pandemic-era supply disruptions.

Key Industry Highlights:

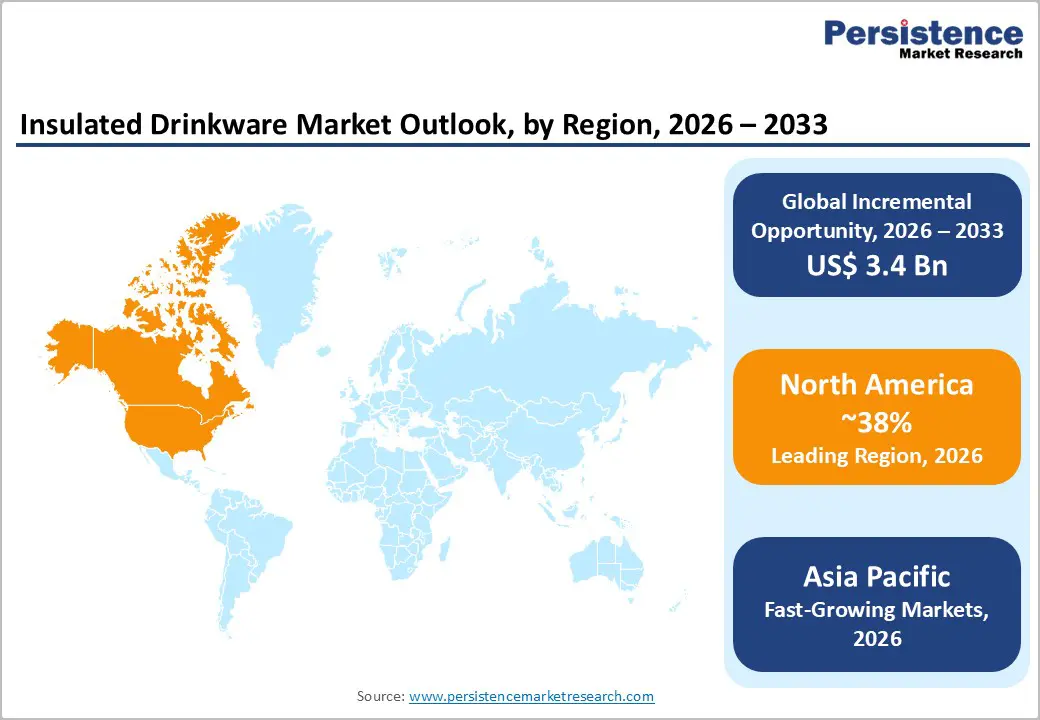

- Leading Region: North America leads the global insulated drinkware market, accounting for approximately 38% of revenue in 2025, driven by a mature outdoor recreation culture, strong brand ecosystems, and progressive plastic-reduction regulations.

- Fastest-Growing Region: Asia Pacific is the fastest-growing regional market, propelled by rapid urbanization in China, India, and ASEAN nations, expanding middle-class purchasing power, and favorable government sustainability initiatives.

- Dominant Segment: Water Bottles dominate the product category with approximately 52% market share in 2025, supported by universal consumer applicability, fitness industry alignment, and continuous product innovation by leading brands.

- Fastest-Growing Segment: Online Stores represent the fastest-growing sales channel, benefitting from digital-native consumer behavior, direct-to-consumer brand strategies, and expanding e-commerce reach into emerging markets globally.

- Key Opportunity: The growing outdoor recreation economy, valued at over US$ 862 billion in the U.S. alone, presents a significant untapped opportunity for high-capacity and rugged insulated drinkware, especially across adventure and nature-based tourism segments.

| Key Insights | Details |

|---|---|

| Insulated Drinkware Market Size (2026E) | US$ 7.4 Billion |

| Market Value Forecast (2033F) | US$ 10.8 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.6% |

| Historical Market Growth (2020 - 2025) | 6.4% |

Market Dynamics

Drivers - Rising Health and Hydration Consciousness Fueling Sustained Product Demand

Globally, the emphasis on personal health and daily hydration practices has seen a marked uptick, driving growing demand for insulated drinkware. According to the World Health Organization (WHO), inadequate fluid intake remains a significant public health concern, with recommendations of 2-3 liters of water per day for adults, prompting consumers to invest in portable hydration solutions. In the United States, data from the Centers for Disease Control and Prevention (CDC) indicates that nearly 43% of adults do not consume enough water daily, driving behavioral shifts toward consistent on-the-go hydration tools. The wellness industry boom, particularly the surge in gym memberships, yoga, and trail activities, has made insulated water bottles and mugs an everyday lifestyle necessity, creating a self-sustaining demand cycle that rewards both functional and premium product offerings.

Accelerating Global Shift Away from Single-Use Plastics

Stringent government regulations targeting single-use plastics across major economies are providing a significant structural tailwind for the insulated drinkware market. The European Union’s Single-Use Plastics Directive (Directive 2019/904/EU), which banned a range of single-use plastic items effective July 2021, has compelled millions of consumers to pivot toward durable, reusable alternatives. Similarly, in the United States, over 500 municipalities have enacted plastic restriction ordinances, according to data tracked by the National Conference of State Legislatures (NCSL). In Asia, countries such as India have implemented a ban on single-use plastics since July 2022 under the Environment Protection Act. These regulatory catalysts are not only driving first-time purchases but also accelerating the replacement cycle for insulated drinkware, supporting long-term volume growth across all product categories.

Restraints - High Product Pricing Limiting Penetration in Price-Sensitive Markets

Premium insulated drinkware, particularly double-wall vacuum stainless steel products from brands such as YETI Holding Inc. and Hydro Flask, commands significant price premiums- often retailing between US$ 30 and US$100- relative to conventional plastic bottles priced under US$ 10. In developing economies across South Asia, Sub-Saharan Africa, and parts of Latin America, where per capita consumer spending on discretionary goods remains constrained, this pricing gap substantially limits broad market adoption. The World Bank estimates that over 700 million people globally still live on less than US$ 2.15 per day, underscoring the structural affordability barrier. This pricing disparity restricts volume growth in high-population markets and compels manufacturers to balance premium positioning with accessible entry-level product lines.

Intense Market Competition and Raw Material Cost Volatility

The insulated drinkware market faces significant pressure from both fluctuations in raw material costs and intensifying competitive dynamics. Stainless steel, the dominant raw material, is subject to commodity price volatility-the London Metal Exchange (LME) recorded stainless steel nickel surcharges fluctuating by as much as 20-25% year-over-year in recent periods. These input cost swings compress manufacturers’ margins, particularly for small and mid-tier players lacking backward integration. Simultaneously, the market’s growing attractiveness has drawn numerous private-label and low-cost manufacturers, especially from China, intensifying price competition and eroding brand differentiation for established players.

Opportunity - Rapid Expansion of E-Commerce and Direct-to-Consumer Channels

The proliferation of e-commerce platforms presents a transformative revenue opportunity for insulated drinkware brands seeking to bypass traditional retail markups and build direct consumer relationships. According to the United Nations Conference on Trade and Development (UNCTAD), global e-commerce sales surpassed US$ 27 trillion in 2022 and continue to grow, with consumer goods among the fastest-growing categories. Brands like S’Well Corporation and Klean Kanteen Inc. have leveraged social commerce, influencer-led marketing on platforms such as Instagram and TikTok, and subscription-based models to build loyal communities and generate recurring revenue. The direct-to-consumer (DTC) approach also enables richer data collection on consumer preferences, facilitating faster product iteration cycles. For emerging brands and even established players, online marketplaces and branded storefronts represent a critical vehicle for international market entry with relatively lower capital outlay.

Growing Outdoor Recreation and Adventure Tourism Industry

The global outdoor recreation economy represents one of the most fertile opportunity landscapes for insulated drinkware manufacturers. The Outdoor Industry Association (OIA) valued the U.S. outdoor recreation economy at approximately US$ 862 billion in 2021, supporting 5 million jobs. Globally, adventure tourism is projected to recover and grow robustly post-pandemic, with the World Tourism Organization (UNWTO) highlighting adventure and nature-based travel as among the fastest-recovering and expanding travel niches. This boom is driving strong demand for high-capacity, rugged, and thermally superior insulated products such as canteens, wide-mouth bottles, and coolers across camping, hiking, mountaineering, and water sports. Companies like CamelBak Products LLC and Pelican Products Inc. are already well-positioned in this space, while new entrants can capitalize on niche product development for specific adventure sub-categories.

Category-wise Analysis

Product Insights

Water bottles represent the dominant product segment within the insulated drinkware market, accounting for approximately 52% of total market share in 2025. This leadership is firmly rooted in the product’s universal applicability. Water bottles serve both everyday hydration at the workplace and gym as well as outdoor and sporting activities, making them the highest-volume category across all demographics. The surge in consumer preference for reusable, eco-conscious hydration vessels has particularly boosted water bottle adoption, with brands like Hydro Flask, Klean Kanteen Inc., and S’Well Corporation reporting sustained double-digit unit growth. Institutional procurement, such as schools, corporate offices, and hospitals, also adds a consistent demand layer. Additionally, frequent product innovation in lid mechanisms, color options, and personalization has sustained repeat purchase behavior, reinforcing water bottles as the undisputed category leader. The fastest-growing product segment is Cans, driven by consumer interest in compact, portable, and stylish formats ideal for on-the-go consumption and single-serve beverage storage.

Material Insights

Stainless steel commands the leading position in the material category, holding an estimated 65% market share in 2025. The material’s dominance is attributable to its superior thermal retention properties, durability, corrosion resistance, and safety profile, being free of BPA (Bisphenol A) and other potentially harmful chemical leachates associated with some plastic variants. Consumer awareness around plastic-related health risks has significantly reinforced stainless steel’s positioning as the preferred material choice. According to the U.S. Food and Drug Administration (FDA) and European Food Safety Authority (EFSA), food-grade stainless steel (typically 18/8 or 304-grade) is affirmed safe for long-term food contact, providing regulatory confidence to both consumers and manufacturers. Industry leaders, including YETI Holding Inc., Thermos L.L.C., and Hydro Flask, have built their entire product portfolios predominantly around stainless steel constructions. The fastest-growing material is Plastic-Insulated, particularly variants that use BPA-free Tritan and other advanced polymer composites, offering a lighter-weight alternative at a lower price point and appealing strongly to budget-conscious and youth demographics.

Capacity Analysis

The 750 mL capacity segment leads the insulated drinkware market with an estimated 30% share in 2025, reflecting its status as the consumer sweet spot for daily hydration. A 750 mL bottle comfortably accommodates approximately three to four servings of fluid intake and aligns well with the widely promoted daily hydration goals, without being overly cumbersome for everyday carry. The format is particularly popular among commuters, office workers, gym-goers, and school-going populations. Fitness industry associations, including the American College of Sports Medicine (ACSM), recommend consistent fluid intake during moderate exercise, and the 750 mL volume strikes the ideal balance between portability and hydration adequacy. Leading brands, including Contigo and CamelBak Products LLC, have centered significant portions of their SKU ranges around this capacity tier. The fastest growing capacity segment is above 2 Liters, driven by the outdoor recreation boom, demand from professional athletes, and growing use in fieldwork environments where refill access is limited.

Sales Channel Insights

Supermarkets and hypermarkets retain the leading position in the insulated drinkware sales channel landscape, accounting for approximately 34% of total sales in 2025. The dominance of this channel stems from its unmatched geographic penetration, high consumer footfall, and the ability to facilitate impulse and trial purchases, particularly important for new consumers entering the category. Major retail chains such as Walmart, Target, and Costco in North America, and Tesco, Carrefour, and ALDI in Europe, stock a wide assortment of insulated drinkware from entry-level to mid-premium brands. In-store visibility, promotional pricing, and bundled deals further drive volume through this channel. However, it is noteworthy that Online Stores are the fastest-growing channel, recording the highest CAGR of the forecast period (2026-2033), propelled by digital-native consumer behavior, personalization capabilities, and expanding reach into Tier-2 and Tier-3 cities globally.

Regional Insights

North America Insulated Drinkware Market Trends and Insights

North America holds the dominant position in the global insulated drinkware market, commanding an estimated 38% revenue share in 2025. The United States is the primary engine of this regional dominance, underpinned by a deeply entrenched outdoor recreation culture, high consumer spending capacity, and a mature ecosystem of premium brands, including YETI Holding Inc., Hydro Flask, and CamelBak Products LLC. The Outdoor Industry Association (OIA) reports that approximately 160 million Americans participated in outdoor recreation in 2022, directly sustaining robust demand for insulated hydration products. Furthermore, federal and state-level plastic reduction regulations, such as California’s SB-54, signed in 2022, have fortified the structural shift toward reusable drinkware.

The U.S. market also benefits from a vibrant innovation ecosystem, with frequent launches of smart and connected hydration products integrating temperature display and hydration tracking. Canada contributes meaningfully, particularly in winter-weather-driven demand for thermally superior mugs and bottles used in skiing and cold-climate outdoor activities. The region’s e-commerce infrastructure and widespread social media influence further accelerate product discovery and adoption among younger demographics.

Europe Insulated Drinkware Market Trends and Insights

Europe represents the second-largest regional market, with Germany, the United Kingdom, France, and the Netherlands being the leading country contributors. Environmental consciousness is exceptionally high across the region, driven by the European Green Deal and the EU Single-Use Plastics Directive, which together have catalyzed substantial behavioral shifts toward reusable drinkware. Germany, in particular, benefits from a strong culture of sustainability and zero-waste living, reinforced by the country’s well-developed waste management infrastructure. Dutch brand Dopper has emerged as a regional sustainability icon, combining functional design with a social mission to reduce plastic waste.

In the United Kingdom, rising sustainability awareness aligned with the government’s Resources and Waste Strategy has significantly boosted premium insulated bottle sales. France and Spain are witnessing accelerating demand, particularly through specialty outdoor and sports retail channels. Across the region, regulatory harmonization under EU food contact material regulations (EC No 1935/2004) ensures consistent product safety standards, facilitating cross-border trade and enabling brands to operate efficiently at a pan-European scale.

Asia Pacific Insulated Drinkware Market Trends and Insights

Asia Pacific is the fastest-growing regional market for insulated drinkware, projected to record the highest CAGR during the forecast period of 2026-2033. China dominates the regional landscape as both the largest manufacturing hub and a rapidly growing consumption market, with domestic brands and global players alike scaling operations to meet surging urban consumer demand. The Chinese government’s push under its “Beautiful China” ecological initiative and its plastic reduction policies announced by the National Development and Reform Commission (NDRC) are creating favorable regulatory conditions for the adoption of reusable drinkware.

India is emerging as a high-growth market, driven by a young, urbanizing population, expanding middle class, and government initiatives such as the Swachh Bharat Mission promoting hygiene and sustainable habits. Japan’s market is characterized by premiumization and a strong cultural affinity for compact, high-quality personal accessories, supporting demand for precision-engineered insulated mugs and bottles. Across ASEAN markets-particularly Vietnam, Indonesia, and Thailand-rising disposable incomes, an expanding fitness culture, and growing tourism activity are collectively driving first-time purchases of insulated drinkware, making the region a critical long-term growth frontier for global manufacturers.

Competitive Landscape

The global insulated drinkware market displays a moderately fragmented structure, with a mix of established premium brands and numerous regional or private-label manufacturers. Competition is driven by innovation in thermal efficiency, smart-connected features, and eco-friendly materials, alongside lifestyle-oriented marketing strategies. Market players focus on geographic expansion, particularly into high-growth regions, and strategic partnerships with retail and online channels to enhance visibility and accessibility. Emerging entrants leverage direct-to-consumer e-commerce and social commerce platforms to quickly build brand awareness, while established companies employ acquisitions and portfolio expansion to strengthen market presence. Sustainability, product differentiation, and consumer engagement through digital platforms remain central to maintaining competitive advantage in this evolving market landscape.

Key Developments

- February 2026: FrostSkin Holdings LLC unveils its patent-pending Instant Chill smart hydration bottle with active cooling, filtration, and UV-C purification, launching on Kickstarter February 17 to create cold water anywhere on demand.

- January 2026: EcoKeep, a US startup, reports rapid business growth after partnering with Toptrue to source FDA and EU-certified insulated water bottles, boosting sales, expanding product lines, and entering major retail and B2B channels.

Companies Covered in Insulated Drinkware Market

- YETI Holding Inc.

- Thermos L.L.C.

- Contigo

- Pelican Products Inc.

- PMI Worldwide

- CamelBak Products LLC

- Tupperware Brands Corporation

- Hydro Flask (Helen of Troy Limited)

- Dopper

- The Coleman Company Inc.

- Aquasana Inc.

- Cool Gear International LLC

- BRITA GmbH

- Klean Kanteen Inc.

- S’Well Corporation

- Nalgene (Implus Footcare LLC)

- Stanley (Pacific Market International LLC / PMI Worldwide)

- Zojirushi Corporation

- Tiger Corporation

- Manna Hydration

Frequently Asked Questions

The market is projected at US$ 7.4 billion, driven by reusable hydration demand, wellness trends, and single-use plastic regulations.

Rising health awareness, single-use plastic bans, and growth in outdoor recreation fuel demand.

North America leads, with the U.S. contributing the largest share due to outdoor culture, high spending, and strong regulations.

Expansion of e-commerce and direct-to-consumer sales, and the growing outdoor recreation and adventure tourism sector.

The global insulated drinkware market features prominent players including YETI Holding Inc., Hydro Flask (Helen of Troy Limited), Thermos L.L.C., CamelBak Products LLC, Klean Kanteen Inc., S’Well Corporation, etc.