- Electrical Equipment & Services

- Industrial Cable Reels Market

Industrial Cable Reels Market Size, Share, and Growth Forecast, 2026 - 2033

Industrial Cable Reels Market by Product Type (Spring-Loaded, Motorized/Electric, Hydraulic, Pneumatic, Manual/Hand-Crank, and Miscellaneous Cable Reels.), Application (Power Supply & Distribution, Cranes & Hoists, Ports & Marine Handling, Mining & Heavy Machinery, Manufacturing and Assembly Lines, Garages and workshops, Utilities/Wastewater/Renewables), Material Type (Steel (Mild & Stainless), Aluminum, Composites, Engineering Plastics) Industry and Regional Analysis, 2026 - 2033

Industrial Cable Reels Market Size and Trends Analysis

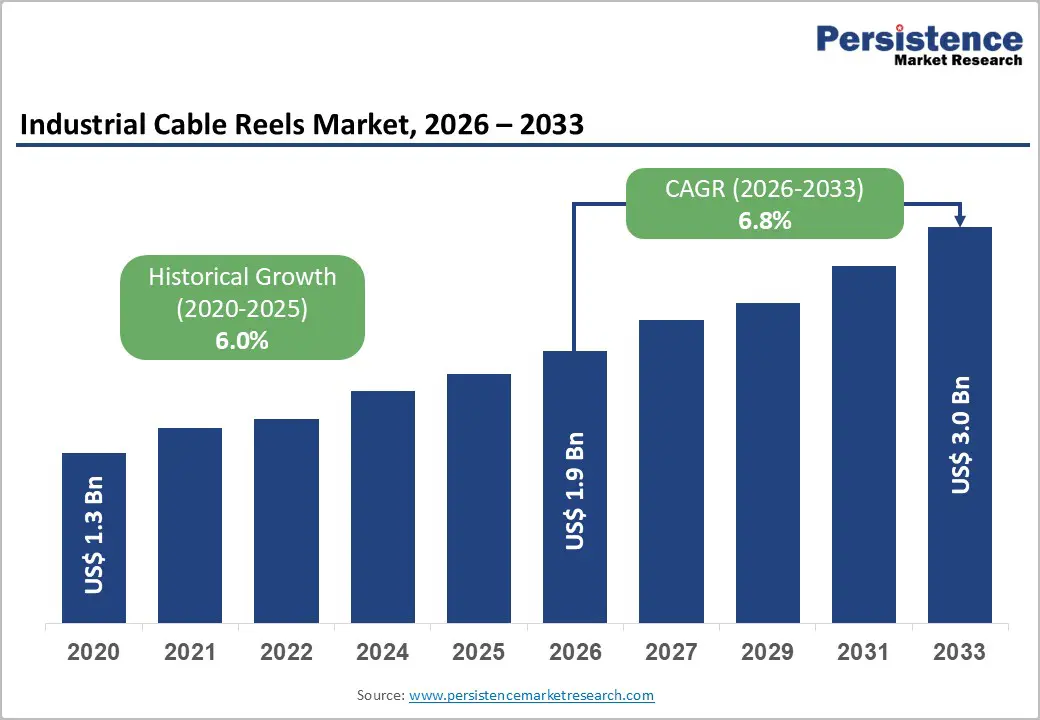

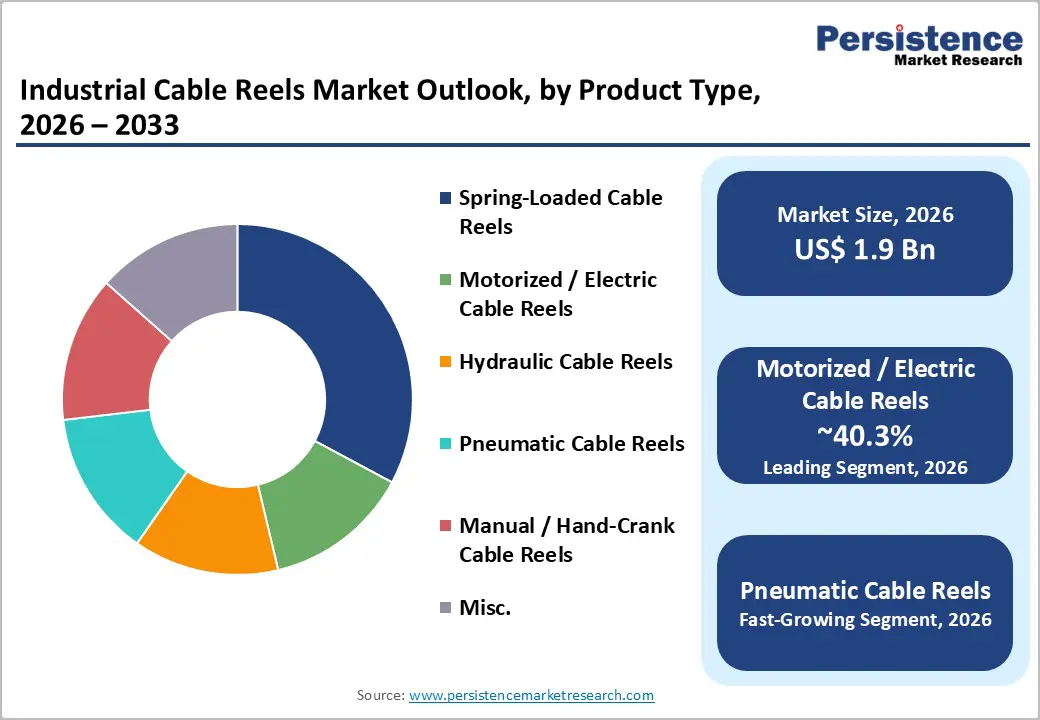

The global industrial cable reels market size is likely to be valued at US$ 1.9 billion in 2026 and is projected to reach US$ 3.0 billion by 2033, growing at a CAGR of 6.8% between 2026 and 2033.

This expansion reflects fundamental structural drives across global power infrastructure, renewable energy deployment, and industrial automation ecosystems. Motorized and pneumatic cable reel systems are fundamentally reshaping how global industries manage power distribution, marine operations, and complex manufacturing environments, with particular momentum in renewable energy, 3PL operations, and port & marine handling.

Key Industry Highlights:

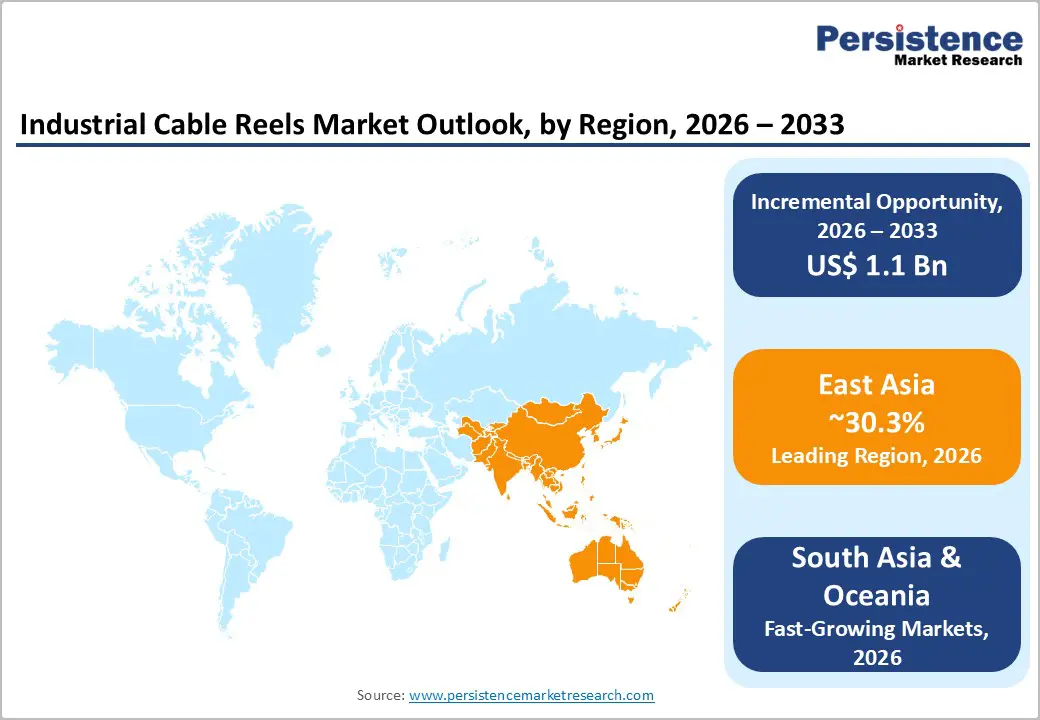

- Leading Regional Market: East Asia holds 30.3% of the Industrial Cable Reels market, driven by China’s manufacturing expansion, renewable energy deployment, and infrastructure modernisation.

- High-Value Regional Contributor: Europe represents 24% of global market value, supported by stringent environmental regulations, advanced HVDC transmission projects, and grid modernisation initiatives.

- Dominant Product Segment: Motorised and electric cable reel systems account for 40.3% of the market, reflecting widespread adoption across manufacturing, port handling, and power distribution applications.

- Fastest-Growing Product Segment: Pneumatic cable reels are the fastest-growing category, driven by demand in harsh industrial environments, mining, offshore operations, and explosive atmospheres.

- Regulatory Growth Indicator: Electrification mandates, renewable energy policies, and smart grid deployment across North America, Europe, and the Asia-Pacific are accelerating the adoption of advanced cable management solutions.

- Industrial End-user: Power supply & distribution applications dominate with 24.7% share, while utilities, renewable energy, and wastewater sectors demonstrate the fastest growth due to complex infrastructure and clean energy integration.

| Key Insights | Details |

|---|---|

| Industrial Cable Reels Market Size (2026E) | US$ 1.9 Bn |

| Market Value Forecast (2033F) | US$ 3.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.0% |

Market Dynamics

Drivers - Global Renewable Energy Expansion and Electrification Infrastructure

Renewable energy deployment represents a transformative structural force reshaping the global industrial cable reels market, necessitating specialised cable management solutions for solar farms, wind installations, and grid modernisation projects. According to the International Energy Agency (IEA), global energy demand grew by 2.2 Percent in 2024, with electricity demand surging by 4.3 percent, driven primarily by record temperatures, electrification, and digitalisation. Renewables led the expansion of the energy supply, accounting for 38 percent of new energy growth, with global renewable capacity additions reaching 700 GW in 2024, 80 percent of which was attributed to solar PV installations.

Grid-scale battery storage is projected to expand nearly 35-fold between 2022 and 2030, reaching 970 GW globally, with 170 GW expected to be added in 2030 alone, creating substantial demand for cable handling systems in energy storage facilities.

India exemplifies this dynamic, with plans to approve approximately 500 gigawatts of solar projects, including a 30 GW solar plant under development in Gujarat by Adani, NTPC, and others. Additionally, India's Pradhan Mantri KUSUM scheme promotes rooftop solar installations, creating demand for DC and evacuation cables that require specialised cable-reel management. Offshore wind projects demand submarine cables with array cables (33-66 kV) and export cables (33-400 kV), necessitating advanced pneumatic and motorised reel systems for deployment and management in marine environments.

Industrial Automation, Material Handling, and Port/Marine Operations Modernisation

Industrial automation and port operations represent critical growth vectors, driven by e-commerce logistics expansion, growth in containerised shipping volumes, and the deployment of heavy machinery in the mining and manufacturing sectors. Port and maritime handling equipment markets experienced substantial growth, with global shipping and port material handling equipment, driven by container throughput expansion and vessel fleet modernisation. Bulk material handling creating proportional demand for cable management infrastructure.

Cavotec's order from TAKRAF India Pvt. Ltd for seven cable reel systems and six hose reel systems for a phosphate and sulphur processing company in Morocco demonstrates market penetration in heavy industrial operations in North Africa. Magnetek's industrial cable reel product line, featuring spring-driven and motorised electric reels, serves overhead cranes, mobile and port gantry cranes, monorails, excavators, and welding systems. Manufacturing and assembly operations require integrated motorised cable reels for automated welding systems, robotic material handling, and continuous production processes. The Industrial Cable Reels Market responds by deploying motorised electric and pneumatic systems engineered for continuous duty cycles, harsh environmental conditions, and seamless integration with industrial control systems.

Restraint - Tariff Rise and Supply Chain Fragmentation

Trade restrictions and tariff policies create material cost pressures for cable reel manufacturers and distributors, particularly those that rely heavily on imported components and raw materials. According to market analyses, the industrial cable reels market growth forecast was reduced by 0.7% in 2025 due to tariff impacts between the U.S. and other countries, with particular pressure on corrosion-resistant steel and retraction mechanisms imported from India and Brazil. Reciprocal tariffs and geopolitical trade tensions directly increase manufacturing costs, compress margins, and delay project implementations.

Supply chain fragmentation across multiple manufacturing regions creates logistical complexity and cost volatility that disproportionately affect smaller manufacturers, who are unable to absorb tariff shocks or maintain geographically distributed production capacity. Many customers respond to tariff-driven cost increases by deferring capital expenditures, consolidating reel requirements, or seeking imported alternatives, creating cyclical demand patterns that amplify industry margin pressure.

Opportunity - Renewable Energy Cable Infrastructure Deployment and Offshore Wind Expansion

The industrial cable reels market presents a transformative opportunity as offshore wind energy deployment and distributed solar installation programs accelerate, requiring specialised cable management solutions. Offshore wind projects present a particularly strong opportunity, as they require submarine array cables (33-66 kV) and export cables (33-400 kV) that necessitate advanced motorised and pneumatic reels for underwater deployment, maintenance, and emergency retrieval. India has established ambitious 30 GW targets for offshore wind capacity, requiring substantial investment in submarine cable infrastructure and associated reel management systems. The renewable energy cable market demonstrates structural momentum.

The industrial cable reels market captures a proportion of the value from this renewable transition, as each new offshore wind project, distributed solar array, and grid interconnection requires specialised cable management infrastructure. Manufacturers developing reel systems engineered for submarine cable deployment, deep-sea operations, and extreme environmental conditions will capture premium market positioning and superior margins. The renewable energy cable opportunity extends beyond generation facilities to grid modernisation, with the IEA highlighting that advanced economies prioritise grid reinforcement, smart grid deployment, and HVDC technology adoption, creating sustained demand for motorised cable reels throughout distribution networks.

Electrification Ecosystem Development and EV Charging Infrastructure

Government electrification mandates and transportation decarbonization initiatives create substantial demand for cable reel systems supporting EV charging networks, high-voltage distribution infrastructure, and renewable energy integration. India has established ambitious EV adoption targets of 30 percent for private cars, 70 percent for commercial vehicles, and 100 % for buses by 2030, which will require extensive deployment of charging infrastructure across the country. This electrification requirement necessitates robust cable management systems for the rapid installation and maintenance of charging networks. The Industrial Cable Reels Market benefits through demand for motorised, pneumatic, and spring-loaded systems optimised for mobile power distribution and rapid cable deployment across geographically dispersed charging stations.

Data center infrastructure expansion further amplifies this opportunity, with approximately 150-200 megawatts of new data center capacity expected across India over 12-24 months, driven by global technology giants (Amazon, Google, Microsoft) and leading local operators. Each data center requires sophisticated power distribution infrastructure incorporating cable management systems. The combined electrification ecosystem EV charging infrastructure, data centre power systems, renewable energy integration, and grid modernization creates a sustained demand trajectory for advanced motorised and automated cable reel systems through 2033.

Category-wise Analysis

Product Type Insights

Motorized and electric cable reel systems command the largest product category, representing 40.3% of market share in 2026 and reflecting dominant market preference for powered, automated cable management solutions across industrial applications. Motorised reels provide consistent tension control, operator safety, and productivity optimisation critical for high-volume operations in manufacturing, power distribution, and port handling environments. Electric-powered systems eliminate manual labour requirements, reduce installation timelines, and enable integration with automation control systems capabilities, particularly valuable in containerised port operations, manufacturing assembly lines, and renewable energy infrastructure deployment. Motorized reels maintain market leadership through established customer preference, widespread infrastructure compatibility, and proven operational reliability across diverse end-use applications. Growth projections indicate motorized systems will sustain market dominance through 2033, though at moderated growth rates as pneumatic and spring-loaded systems capture emerging application segments.

Pneumatic cable reel systems represent the fastest-growing product category, driven by deployment in harsh industrial environments, explosive/flammable atmospheres, and operations requiring non-electrical power sources. Pneumatic reels eliminate electrical safety concerns in hazardous locations, operate effectively in extreme temperature environments, require minimal maintenance relative to electrical systems, and demonstrate superior reliability in mining, chemical processing, and offshore operations.

Application Insights

Power supply and distribution applications constitute the largest industrial cable reel segment, accounting for 24.7% of the market in 2026 and reflecting a fundamental reliance on cable management infrastructure for reliable power transmission across utilities, industrial facilities, and commercial establishments. Power distribution networks require motorized, hydraulic, and pneumatic cable reel systems for both installation and ongoing maintenance of transmission lines, distribution networks, and backup power systems.

Utilities deploying smart grid technologies, renewable energy integration infrastructure, and modernized distribution systems require advanced cable management solutions. This segment's market dominance reflects widespread adoption across developed and emerging economies, creating sustained demand driven by ageing infrastructure replacement, capacity expansion, and renewable energy integration requirements. Power supply and distribution segments demonstrate robust growth potential as global electricity demand continues to accelerate, with particular momentum in emerging markets investing in grid modernisation and electrification infrastructure.

Utilities, wastewater treatment, and renewable energy applications represent the fastest-growing end-use segment, reflecting a fundamental structural shift toward clean energy deployment and environmental infrastructure modernisation. Renewable energy facilities, such as solar farms, wind installations, hydroelectric plants, and energy storage systems, require specialized motorized, pneumatic, and spring-loaded cable reel systems engineered for harsh environmental conditions, complex electrical specifications, and integration with distributed energy management systems.

Regional Insights and Trends

North America Industrial Cable Reels Market Trends

North America represents a mature, technologically sophisticated market commanding approximately 21% of the global Industrial Cable Reels Market share in 2026, characterised by established manufacturing infrastructure, stringent regulatory compliance requirements, and substantial investment in renewable energy and power infrastructure modernization. The region's cable reel market benefits from U.S. construction spending reaching US$ 1.6 trillion in 2023, supporting sustained demand from construction, infrastructure, and industrial sectors. North America holds approximately 35.4% of the Mobile Cable Reel Market in 2024, reflecting strong adoption of mobile power solutions across telecommunications, entertainment, and construction industries.

Regulatory frameworks, particularly ANSI and IEC 61316:2021 standards adoption, create compliance-driven procurement patterns favouring established manufacturers with engineering and certification capabilities. The U.S. renewable energy sector demonstrates robust momentum, with solar and wind projects surpassing coal generation in several regions, creating substantial cable infrastructure investment. The SunZia Wind Project (3.5 GW) initiated large-scale transmission cable deployment in 2024, linking renewable power from New Mexico to Arizona.

The U.S. energy storage market achieved a 5.6 GW quarterly installation record in Q2 2025, with the utility-scale segment adding 4.9 GWsufficient to power 3.7 million homes, creating proportional demand for cable management systems in energy storage facilities. Key growth states include Texas, California, and Arizona, each adding over 1 GW in 2025. The region's mature manufacturing base, sophisticated customer base, and regulatory compliance requirements support premium-priced motorized and pneumatic cable reel systems with advanced safety and automation features. Market growth projections range from 5.5-6.2% annually, reflecting market maturity and saturation in traditional segments offset by strong renewable energy and infrastructure modernization momentum.

East Asia Industrial Cable Reels Market Trends

East Asia represents the largest and fastest-growing regional market, commanding approximately 30.3% of the global Industrial Cable Reels Market share in 2026 and demonstrating exceptional growth momentum driven by manufacturing-intensive industrialisation, renewable energy deployment, and infrastructure modernisation. China's industrial sector dominates the region, with manufacturing-intensive operations creating substantial cable management infrastructure demand. However, China's energy demand growth slowed to under 3 Percent in 2024, approximately half the 2023 rate, reflecting macroeconomic normalisation. Despite slower energy demand growth, China recorded the largest absolute increase in global energy consumption and contributed over half of the 700 GW global renewable capacity additions in 2024, demonstrating a structural commitment to renewable energy deployment.

Approximately 150-200 megawatts of new data center capacity are expected across India over 12 to 24 months, driven by global technology giants and leading Indian operators. South Korea's highly connected society supports rapid adoption of advanced cable management systems, with smart apartment complexes and tech-friendly households seeking premium, integrated reel solutions. East Asia's estimated annual growth rates range from 8 to 12 percent, substantially exceeding global averages, reflecting structural manufacturing expansion, renewable energy deployment momentum, and infrastructure modernisation investments.

Europe Industrial Cable Reels Market Trends

Europe represents a mature, technologically sophisticated market commanding approximately 24% of the global Industrial Cable Reels Market share in 2026, characterized by stringent environmental regulations, advanced manufacturing standards, and substantial renewable energy infrastructure investment. Advanced economies, including the European Union, returned to energy demand growth in 2024, posting their first growth since 2017 outside post-Covid rebound, reflecting infrastructure modernization and electrification momentum. European Union renewable energy targets mandate substantial solar and wind deployment, with solar and wind generation surpassing coal generation across the region. Germany's SuedLink HVDC project deploys long-distance high-voltage cables transporting renewable energy from northern generation sources to southern consumption centres, representing multi-year infrastructure investment and cable management infrastructure demand.

The European Union emphasizes sustainable manufacturing practices, circular economy principles, and material efficiency, thereby creating market preference for environmentally optimised cable reel designs with reduced material consumption and extended operational lifespans. Manufacturing and product innovation focus reflects regulatory compliance with REACH directives, RoHS restrictions, and circular economy mandates.

Competitive Landscape

The global industrial cable reels market is moderately consolidated, dominated by a few major multinational players, while still having numerous smaller regional suppliers. Leading companies such as Nederman Holding AB, Hannay Reels Inc., Reelcraft Industries, Inc., Coxreels, Conductix-Wampfler GmbH, and Cavotec SA hold significant market share and compete on product reliability, customization, and service networks.

The market exhibits fragmented characteristics at regional and niche levels, with local players catering to specific industrial sectors like mining, manufacturing, and energy. Competition is driven by technological innovation, including automated and heavy-duty reel solutions. Strategic partnerships, global production facilities, and strong aftermarket support further strengthen the position of top players, while smaller firms continue to serve specialised demands.

Key Industry Developments:

- In January 2026, Cavotec secured an order from TAKRAF India Pvt. Ltd. for the supply of seven cable reel systems and six hose reel systems for a major phosphate and sulphur processing company in Morocco. The systems are designed to deliver safe and reliable power and fluid supply to bulk material handling equipment in harsh environments. This development underscores Cavotec’s focus on the mining, minerals, and bulk material handling sectors and reflects the growing demand for robust industrial cable reel solutions in North Africa.

- In October 2024, Nexans launched its MOBIWAY® SPEED cable reel system in Canada, designed to improve efficiency, ergonomics, and safety for electricians in residential projects. The system features ergonomic handles, plug-and-play operation, stackability, and a higher cable capacity of up to 200 meters, surpassing traditional reels. This development reflects the growing demand for efficient, safe, and high-capacity cable handling solutions driven by electrification trends, including electric vehicles, smart homes, and renewable energy adoption across Canada.

Companies Covered in Industrial Cable Reels Market

- Nederman Holding AB

- Hannay Reels Inc.

- Reelcraft Industries, Inc.

- Coxreels

- Conductix-Wampfler GmbH

- Cavotec SA

- Paul Vahle GmbH & Co. KG

- Scame Parre

- DEMAC S.r.l.

- Stemmann-Technik GmbH (Wabtec)

Frequently Asked Questions

The global industrial cable reels market is projected to be valued at US$ 1.9 Bn in 2026.

The Motorized / Electric Reels segment is expected to account for approximately 40.3% of the global industrial cable reels market.

The industrial cable reels market is expected to witness a CAGR of 6.8% from 2026 to 2033.

The Industrial Cable Reels Market growth is driven by global renewable energy expansion, electrification infrastructure, industrial automation, and modernisation of port, material handling, and manufacturing operations requiring motorised, pneumatic, and hydraulic cable management solutions.

The key market opportunities in the Industrial Cable Reels Market lie in renewable energy cable infrastructure, offshore wind and solar projects, EV charging network deployment, high-voltage distribution, and expanding data center power systems requiring advanced motorized, pneumatic, and spring-loaded cable management solutions.

Key players in the Industrial Cable Reels Market include Nederman Holding AB, Hannay Reels Inc., Reelcraft Industries, Inc., Coxreels, Conductix-Wampfler GmbH, and Cavotec SA.