- Home Appliances

- Household Kitchen Appliances Market

Household Kitchen Appliances Market Size, Share, and Growth Forecast, 2025 - 2032

Household Kitchen Appliances Market By Product Type (Cooking Appliances, Refrigeration Appliances), Distribution Channel (Offline Retail, E-commerce/Online Channels), End-user, and Regional Analysis for 2025 - 2032

Household Kitchen Appliances Market Size and Trends Analysis

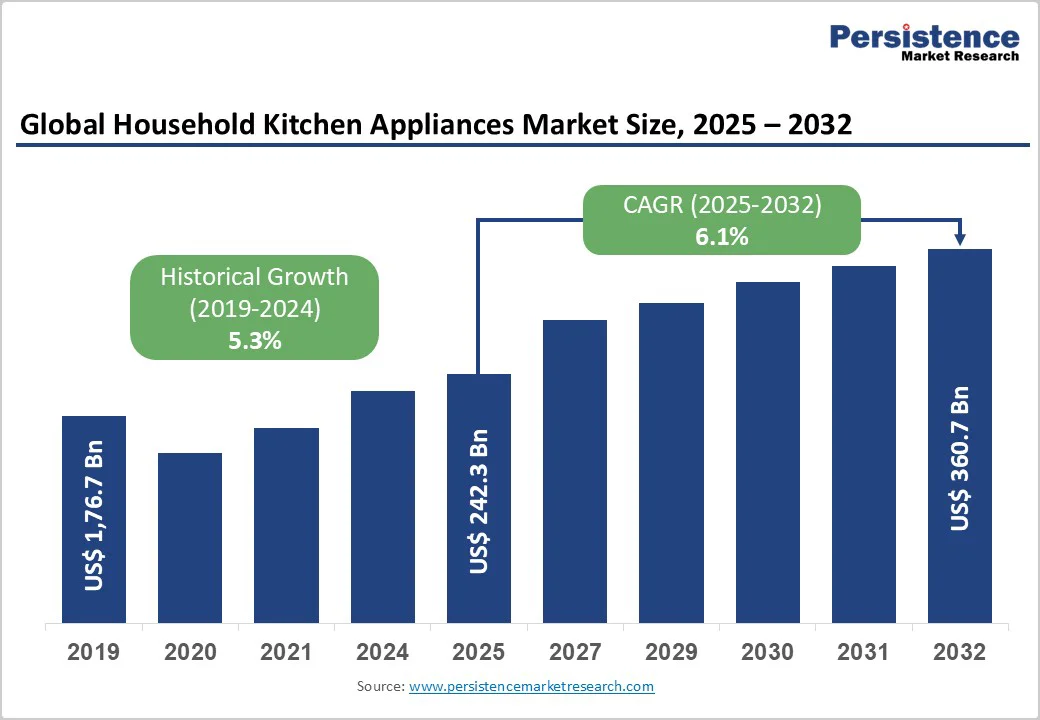

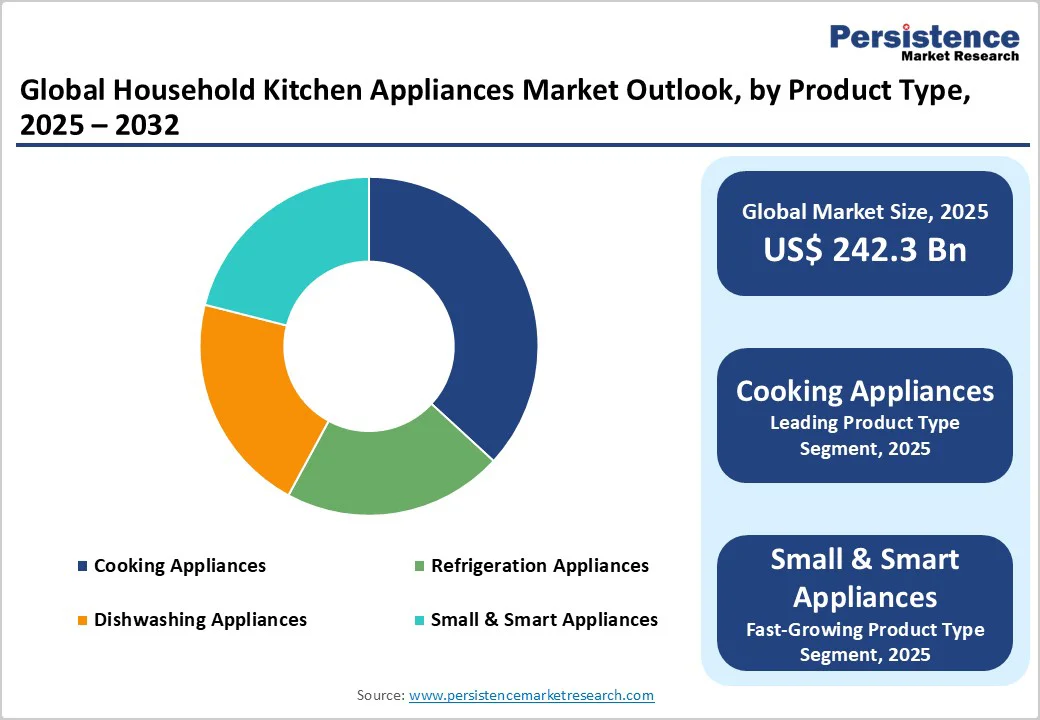

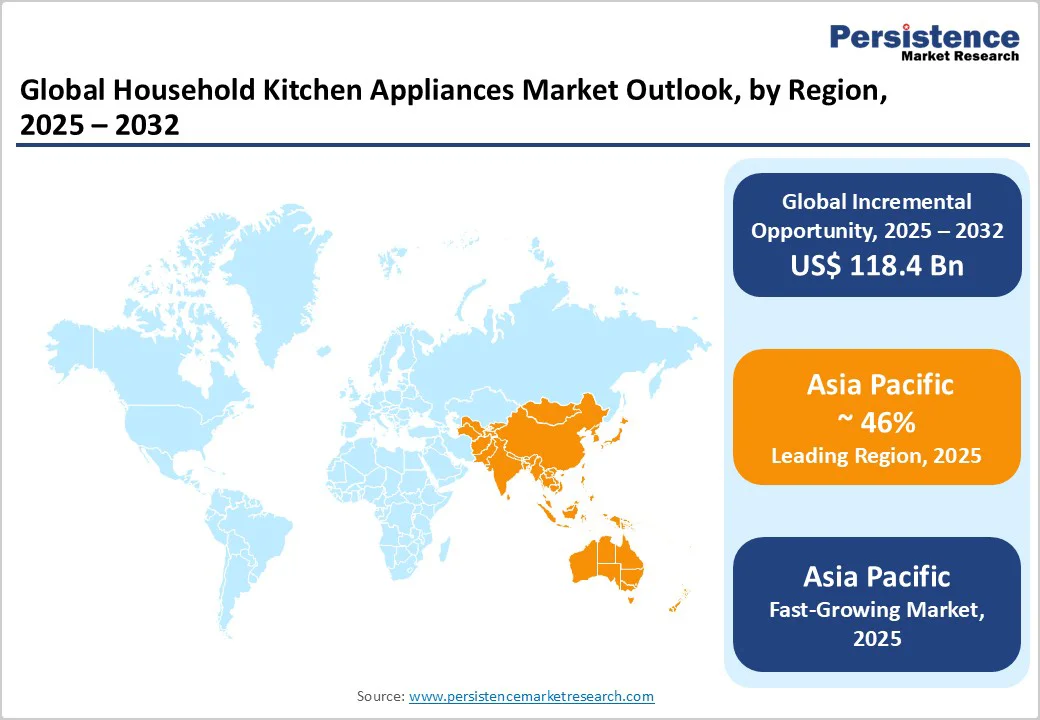

The global household kitchen appliances market size is likely to be valued at US$242.3 billion in 2025 and is expected to reach US$360.7 billion by 2032, growing at a CAGR of 6.1% during the forecast period from 2025 to 2032, driven by the rising adoption of smart and energy-efficient appliances, urbanization, and increasing disposable incomes in emerging markets.

Renovation cycles and the shift to connected appliances are driving demand. Post-pandemic supply-chain recovery and R&D in modular kitchens and energy efficiency are key growth drivers. The market is trending toward premium products and digital integration.

Key Industry Highlights

- Leading Region: Asia Pacific, accounting for approximately 46% of the global market volume in 2025, driven by China’s manufacturing scale and domestic consumption.

- Fastest-Growing Region: Asia Pacific, projected CAGR of 7% between 2025 and 2032, fueled by urbanization, rising disposable incomes, and government trade-in/subsidy programs.

- Investment Plans: Expansion of smart appliance manufacturing lines (e.g., Midea in Guangdong, 2025) and regional distribution hubs in India and ASEAN to capture growing urban and e-commerce demand.

- Dominant Product Type: Cooking Appliances (Ranges, Ovens, Hobs, Built-in Cook Centers), holding 34.5% of total market revenue in 2025.

- Leading Distribution Channel: Offline Retail (Specialty Stores, Big-box Retailers, and Authorized Dealerships), contributing 36% of revenue due to installation support and warranty services.

| Key Insights | Details |

|---|---|

| Household Kitchen Appliances Market Size (2025E) | US$242.3 Bn |

| Market Value Forecast (2032F) | US$360.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Smart and Connected Appliances Adoption

Connected kitchen appliances, including smart ovens, refrigerators, and multifunction devices, are growing at a double-digit CAGR. These appliances offer remote control, recipe integration, and predictive maintenance, increasing average selling prices and enabling recurring revenue streams from software and service subscriptions. Companies implementing open standards experience faster adoption and reduced market friction, creating a significant competitive advantage for early movers.

Energy Efficiency and Regulatory Push

Energy-labeling and ecodesign regulations in Europe and other markets are accelerating the replacement of legacy appliances with high-efficiency models. Compliance raises product ASPs but provides competitive positioning through sustainability. Manufacturers investing in energy-efficient technologies such as induction cooking, advanced compressors, and power electronics benefit from regulatory incentives and improved market access.

Asia Pacific Consumption and Stimulus Programs

Stimulus programs and appliance trade-in initiatives in China and India have boosted domestic consumption. Asia Pacific leads global volume and acts as a manufacturing hub, allowing for scalable production and faster product refresh cycles. Rising middle-class income and urbanization support increased appliance adoption, making the region a primary growth engine.

Barrier Analysis - Raw Material and Component Cost Volatility

Fluctuating prices of metals and semiconductors increase manufacturing costs and reduce margins, particularly for mid-range players. Price adjustments to consumers are limited due to intense competition, leading to cost optimization pressures and potential delays in product upgrades.

Fragmented Retail and Aftermarket Competition

The small-appliance segment is highly fragmented, with numerous regional players and private labels. This results in intense price competition and extended replacement cycles, particularly in mature markets. Compliance with regulatory standards further raises barriers for smaller manufacturers, increasing consolidation pressure.

Opportunity Analysis - Services and Subscription Ecosystems

Connected appliances enable monetization through diagnostics, consumable replenishment, and extended warranty subscriptions. Even converting a small portion of the installed base to subscription-based services can generate multi-billion-dollar revenue potential. This approach allows OEMs to increase customer lifetime value and differentiate themselves from competitors.

Emerging Market Premiumization and Trade-In Programs

Government-backed trade-in and subsidy programs in Asia Pacific reduce purchase barriers for high-efficiency and premium appliances. By leveraging these programs, companies can accelerate replacement cycles, increase penetration in mid-income households, and capture higher-margin sales. Local partnerships and financing solutions further enhance market access and adoption.

Category-wise Analysis

Product Type Insights

Cooking appliances remain the largest revenue contributor in the household kitchen appliances market. This category includes ranges, ovens, hobs, induction cooktops, microwaves, and built-in cook centers. Cooking appliances accounted for approximately 34.5% of the total market, reflecting high penetration in both urban and suburban households.

Consumer preference for reliable, durable, and high-performance cooking solutions ensures sustained demand. For instance, Whirlpool’s built-in ranges and Bosch’s wall ovens continue to command premium pricing due to energy efficiency and smart connectivity features. In developed markets, including the U.S., Europe, and Japan, kitchen remodeling trends further drive revenue growth for high-end and built-in cooking solutions.

Small and smart kitchen appliances are rapidly emerging as the fastest-growing sub-segment. Products such as air fryers, connected blenders, espresso machines, and multifunction ovens are gaining popularity in compact urban homes where convenience, multifunctionality, and digital integration are key purchasing drivers.

Smart appliances equipped with Wi-Fi or Bluetooth allow users to control and monitor cooking remotely, access recipe databases, and schedule maintenance alerts. For example, Philips’ smart air fryers and Breville’s connected espresso machines have shown strong adoption in North America and Asia Pacific due to their convenience, connectivity, and integration with mobile apps.

This sub-segment is also driving higher average selling prices (ASPs) and recurring revenue opportunities through associated software and consumables.

Distribution Channel Insights

Offline retail channels, including specialty appliance stores, big-box retailers (e.g., Best Buy, Lowe’s, Currys), and authorized dealerships, remain the primary sales channel for major kitchen appliances, holding a market share of 36%. Consumers prefer these channels for hands-on experience, installation services, warranty support, and after-sales maintenance.

In regions such as North America and Europe, offline retail contributes the majority of revenue for high-value appliances such as refrigerators, ranges, and dishwashers. For example, LG and Samsung utilize showroom displays and live demonstrations in stores to highlight product features, particularly smart and energy-efficient functions, which helps build trust and drives premium purchases.

E-commerce is experiencing rapid growth, particularly for small and smart kitchen appliances. Online platforms such as Amazon, Tmall, Flipkart, and BestBuy.com provide direct-to-consumer access, enabling faster product launches, wider geographical reach, and first-party data collection for customer insights and aftermarket services.

The COVID-19 pandemic accelerated online adoption, with small appliances such as air fryers, induction cookers, and countertop coffee machines showing significant online traction. For instance, Breville and Philips leverage e-commerce platforms to introduce limited-edition products and subscription-based services, improving customer engagement and repeat sales.

Omnichannel strategies, combining online discovery with offline experience centers, further enhance conversion rates.

End-user Insights

Urban residential households are the largest revenue contributors due to higher appliance penetration, disposable income, and frequent replacement cycles. Key drivers include apartment living, modernization of kitchens, and consumer preference for compact and integrated appliances.

For example, Samsung’s smart refrigerators and Bosch’s induction cooktops are popular in metropolitan areas such as New York, London, and Tokyo, where space efficiency, connectivity, and energy savings are important factors. Urban households often adopt premium features such as Wi-Fi-enabled controls, voice assistance, and IoT integration, which further increase ASPs and revenue per household.

The commercial and institutional segment, including small restaurants, cloud kitchens, co-working kitchens, serviced apartments, and boutique hotels, is expanding rapidly. This segment requires high-duty appliances with robust warranties and long operational lifespans, such as commercial-grade ovens, high-capacity refrigerators, and automated dishwashers.

In Asia Pacific, cloud kitchens in cities, including Mumbai, Shanghai, and Bangkok, are driving demand for compact, multi-functional appliances capable of handling high-volume operations.

Similarly, hotels and serviced apartments in Europe and the Middle East are adopting smart kitchen appliances that combine efficiency with remote monitoring, leading to higher average selling prices and predictable replacement cycles. This sub-segment is expected to maintain a strong CAGR due to the growing foodservice sector, urbanization, and investment in hospitality infrastructure.

Regional Insights

North America Household Kitchen Appliances Market Trends - Premiumization and Smart Appliance Adoption Drive Market Growth

North America represents a high-value market for household kitchen appliances, with the United States accounting for the majority of global per-capita spending. The market is projected to grow steadily, driven by factors such as premiumization, replacement demand, and kitchen renovation cycles.

Consumers are increasingly prioritizing energy-efficient and smart appliances, supported by federal and state-level incentive programs such as ENERGY STAR rebates and local utility subsidies. The integration of IoT technology is widespread, with smart refrigerators, connected ovens, and Wi-Fi-enabled dishwashers leading adoption.

The U.S. appliance market is characterized by high average selling prices and a rapid uptake of connected technologies. Notable developments include Samsung’s launch of AI-powered smart refrigerators in 2024, featuring recipe suggestions, inventory tracking, and remote diagnostics.

Whirlpool has also expanded its subscription-based home appliance maintenance services across 25 states in 2025, reflecting a growing trend toward service monetization. Other significant innovations include LG’s AI ThinQ-enabled smart ovens introduced in 2025 and GE Appliances’ connected dishwasher models with predictive maintenance alerts rolled out in 2024.

The market remains concentrated among global leaders such as Whirlpool, LG, Samsung, and GE, who emphasize strong after-sales networks, warranty services, and loyalty programs to enhance customer lifetime value.

Europe Household Kitchen Appliances Market Trends - Energy Regulations and Sustainability Fuel Demand for Connected, High-Efficiency Appliances

Europe is a high-value market driven by consumer preferences for premium products, stringent energy efficiency regulations, and growing sustainability awareness. Germany, the U.K., France, and Spain are the largest contributors to the region’s appliance revenues.

The European Union’s updated energy-labeling and ecodesign standards are accelerating the replacement of older models with high-efficiency refrigerators, induction cooktops, and built-in ovens. Urban renovation trends and the rising popularity of modular kitchens further support demand for integrated appliance solutions.

Germany remains a hub for innovation in high-efficiency and premium appliances, with companies such as Miele and Bosch leading the way. For example, Bosch’s 2024 rollout of Wi-Fi-enabled induction hobs offers remote diagnostics and automated maintenance scheduling, reflecting strong consumer demand for connected and sustainable appliances.

Additional recent developments include Electrolux’s launch of eco-labeled dishwashers with water-saving features across EU markets in 2025, and Siemens’ partnerships with European smart-home providers to integrate kitchen appliances into home automation systems.

Both European OEMs and global brands invest heavily in localized research and development, sustainable materials, and circular economy initiatives to ensure regulatory compliance and maintain competitive differentiation.

Asia Pacific Household Kitchen Appliances Market Trends - Smart Ecosystems, Urban Demand, and Localized Innovation Accelerate Market Expansion

Asia Pacific is the leading market, holding a market share of 46% and the fastest-growing region in the kitchen appliance sector. China leads in manufacturing scale and domestic consumption, Japan drives premium and technological innovation, and India shows rapid growth in retail penetration, particularly through urban e-commerce channels.

Rising disposable incomes, urbanization, and government-backed trade-in or subsidy programs are accelerating the adoption of smart and energy-efficient appliances throughout the region.

Local certifications, after-sales service networks, and regional customization remain critical to successful market penetration. China is not only a manufacturing powerhouse but also a rapidly expanding domestic market.

Midea’s launch of a smart IoT-enabled kitchen ecosystem in 2025 integrates refrigerators, ovens, and air fryers through a single mobile app, while TCL has introduced compact multifunction ovens targeted at tier-2 cities to address space efficiency and connectivity needs.

India’s appliance market is propelled by urban housing expansion and a growing middle class. Companies such as Havells and TTK Prestige are broadening their smart cooking and refrigeration portfolios, while e-commerce giants Flipkart and Amazon dominate online distribution, enabling rapid adoption of small and smart appliances.

Recent regional developments include Haier’s 2024 launch of IoT-connected refrigerators with inventory management features across China and Southeast Asia, Midea’s expansion of smart appliance manufacturing lines in Guangdong in 2025 to meet domestic and export demand, and TCL’s introduction of multifunction air fryers and ovens for mid-income urban households in China and India.

Leading OEMs such as Midea, Haier, and TCL dominate production and export markets, while opportunities persist in local assembly plants, regional distribution hubs, and smart feature localization tailored to consumer behaviors across China, India, and the ASEAN region.

Competitive Landscape

The global household kitchen appliances market is moderately consolidated, with leading companies holding double-digit shares. Small-appliance and regional segments remain fragmented. Competitive positioning centers on product breadth, brand reputation, energy efficiency, and connected ecosystems.

Key strategies include innovation in smart and energy-efficient appliances, cost leadership through scale, and market expansion via local manufacturing. Differentiators include platform ecosystems, extended warranties, subscription services, and regulatory compliance capabilities.

Key Industry Developments

- In March 2025, TCL introduced compact multifunction ovens and air fryers in China and India, designed for space-conscious urban kitchens, targeting mid-income households seeking convenience and smart functionality.

- In May 2025, LG Electronics launched AI ThinQ-enabled smart ovens in North America, featuring automated cooking programs, app-based remote control, and recipe suggestions to enhance user convenience and kitchen efficiency.

- In July 2025, Siemens partnered with European smart-home providers to integrate kitchen appliances into home automation platforms, improving connectivity, remote monitoring, and seamless user experience across multiple devices.

Companies Covered in Household Kitchen Appliances Market

- Whirlpool Corporation

- Haier Group

- Samsung Electronics

- LG Electronics

- BSH Hausgeräte (Bosch/Siemens)

- Electrolux AB

- Midea Group

- Panasonic Holdings

- Miele & Cie. KG

- Tefal / Groupe SEB

- TTK Prestige Ltd.

- Breville / Sage Group

- Sharp Corporation

- Hisense Group

- Arçelik A.Ş. (Beko)

- Panasonic Corporation

- Haier Smart Home

- Whirlpool India

- Viking Range LLC

- Fagor Industrial

Frequently Asked Questions

The market size is estimated at US$242.3 Billion in 2025.

The household kitchen appliances market is projected to reach US$360.7 Billion by 2032.

Key trends include rising adoption of smart and connected appliances, growth of energy-efficient products, expansion of e-commerce distribution channels, and increasing premiumization in developed markets.

Cooking appliances (ranges, ovens, hobs, built-in cook centers) remain the leading segment, contributing around 34.5% of total market revenue.

The household kitchen appliances market is expected to grow at a CAGR of 6.1% between 2025 and 2032.

Major players include Whirlpool Corporation, Haier Group, Samsung Electronics, LG Electronics, and BSH Hausgeräte (Bosch/Siemens).