- Medical Devices

- Hip Resurfacing Implants Market

Hip Resurfacing Implants Market Size, Share, and Growth Forecast, 2025 - 2032

Hip Resurfacing Implants Market By Product Type (Total, Partial, Revision, Hip Resurfacing Implants), Material (Metal, Plastic, Ceramics), End-user (Hospitals, Orthopedic Clinics, Ambulatory Surgery Centers), and Regional Analysis for 2025 - 2032

Hip Resurfacing Implants Market Size and Trends Analysis

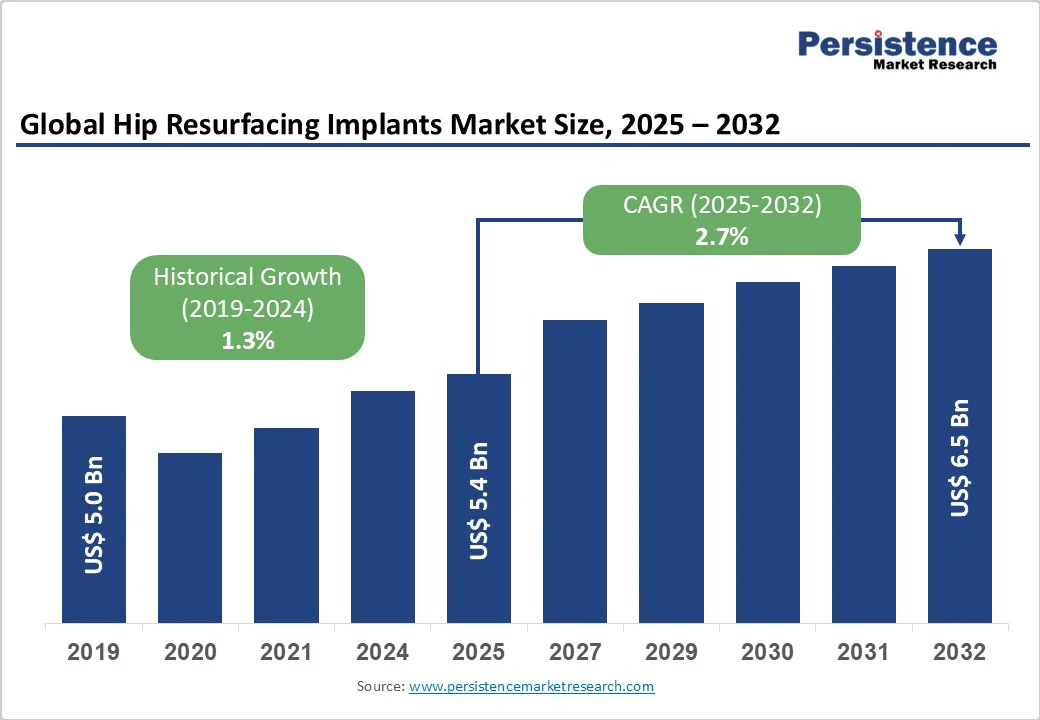

The global hip resurfacing implants market size is expected to be valued at US$5.4 billion in 2025. It is projected to reach US$6.5 billion in 2032, growing at a CAGR of 2.7% during the forecast period of 2025-2032, driven by the rising incidence of hip injuries resulting from trauma and sports-related accidents. The surging geriatric population, which is susceptible to hip degeneration, is also bolstering the market.

Key Industry Highlights:

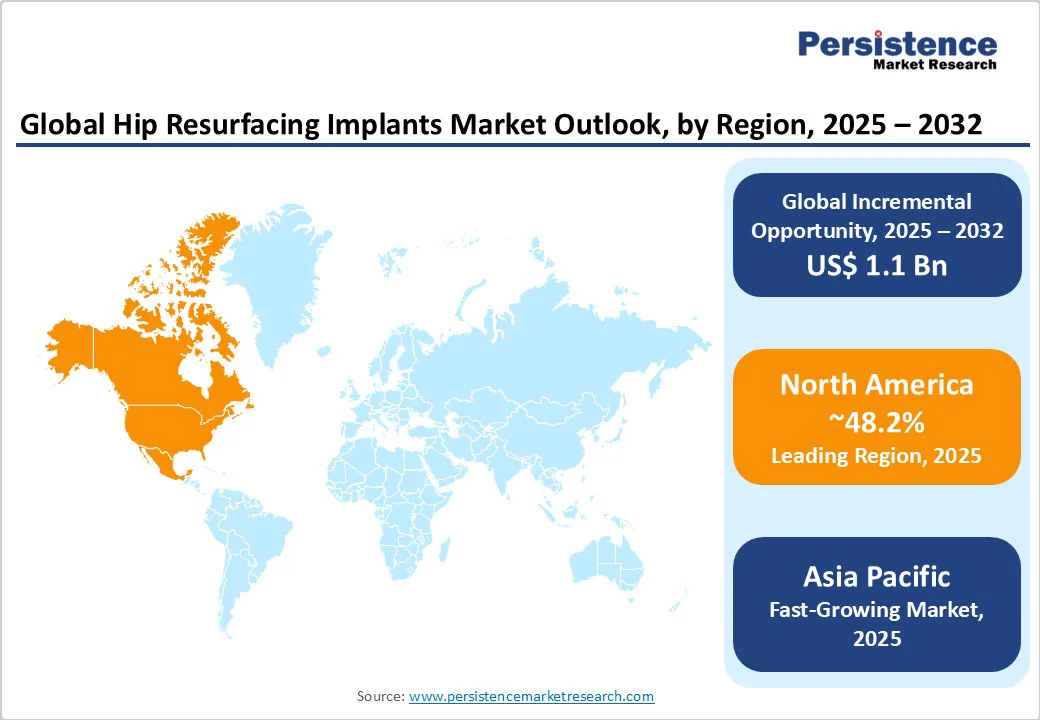

- Leading Region: North America is a leading region, accounting for approximately 48.2% of the market share in 2025, driven by high patient awareness and a well-established healthcare infrastructure.

- Fastest-growing Region: Asia Pacific, boosted by increasing medical tourism and a rising elderly population in India and China.

- Research Effort: Researchers at Imperial College London have developed a new H1 implant for women, enabling them to undergo a type of hip surgery previously suitable only for men, and it has been awarded a CE mark.

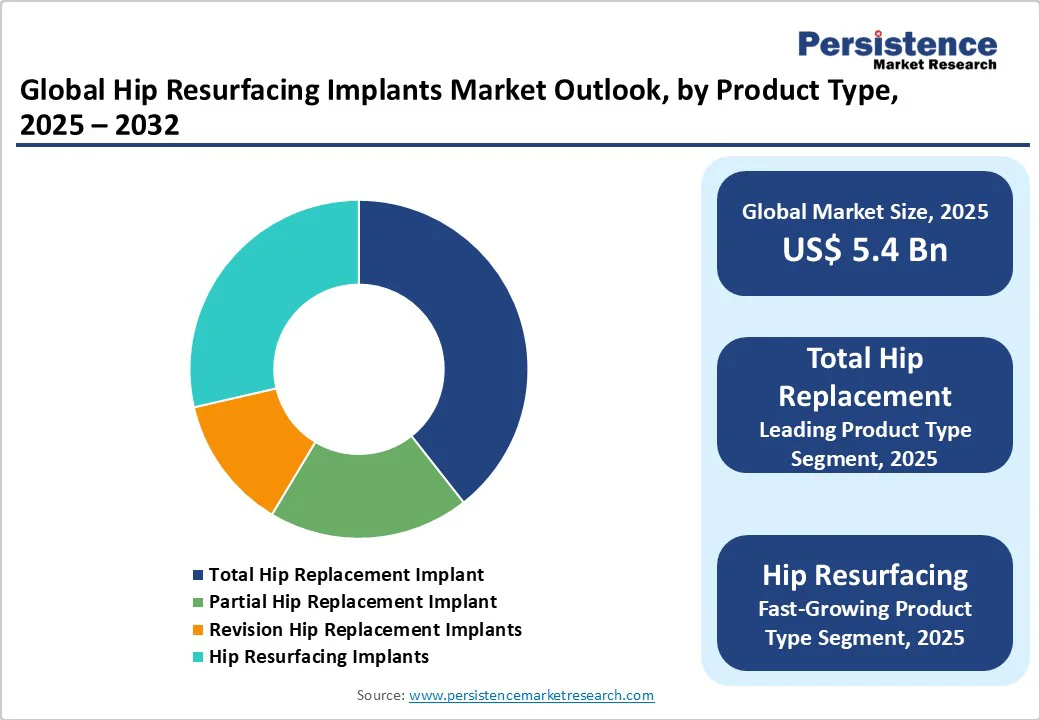

- Leading Product Type: Total hip replacement implants hold a nearly 39.4% share in 2025, due to their proven clinical success and versatility across various patient groups.

- Dominant Material: Metal implants, accounting for approximately 32.7% of the hip resurfacing implants market share in 2025, due to their superior load-bearing capacity and long-term reliability.

- Key End-user: Hospitals are projected to account for approximately 71.5% share in 2025, pushed by comprehensive infrastructure and skilled orthopedic teams.

| Key Insights | Details |

|---|---|

| Hip Resurfacing Implants Market Size (2025E) | US$5.4 Bn |

| Market Value Forecast (2032F) | US$6.5 Bn |

| Projected Growth (CAGR 2025 to 2032) | 2.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 1.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Increasing Prevalence of Traumatic Injuries

The frequency of traumatic injuries affecting the hip, including fractures from accidents, sports-related trauma, and high-impact falls, has increased, fueling demand for hip resurfacing implants. As per the American Association for the Surgery of Trauma (AAST), trauma is the leading cause of death for individuals up to the age of 45 years.

Patients, mainly young and active individuals, are seeking bone-preserving alternatives to total hip replacement that preserve bone and facilitate a rapid recovery. Recent studies in the U.S. indicate that emergency room visits for hip fractures among adults aged 45 to 65 have surged steadily, highlighting a rising patient pool for orthopedic interventions.

Companies, such as Zimmer Biomet and Stryker, are responding with implants designed for improved durability and minimally invasive surgical approaches, enabling patients to return to mobility quickly.

Rising Geriatric Population Worldwide

Europe, North America, and parts of the Asia Pacific are witnessing an increase in the elderly population, which is more susceptible to osteoarthritis, degenerative hip conditions, and fracture risks. This demographic shift is directly raising the requirement for hip resurfacing procedures, as older patients prefer bone-conserving alternatives to total hip replacement.

For instance, in Germany, the adoption of hip resurfacing has risen alongside initiatives promoting minimally invasive joint-preserving surgeries for patients over 60. Additionally, awareness campaigns and improvements in insurance coverage have made such procedures more accessible to older adults.

Barrier Analysis - Concerns over Metal Ion Release from Metal-on-Metal Implants

A major restraint for the hip resurfacing implants market is the risk associated with metal-on-metal components, which can release metal ions into surrounding tissues and the bloodstream. These ions tend to trigger adverse local tissue reactions, inflammation, and, in severe cases, implant failure, which may require revision surgery.

Regulatory scrutiny has increased, with the FDA and European authorities issuing warnings about metal-on-metal hip implants, which have influenced surgeon preference and patient acceptance. For instance, the Exactech recall in 2021, linked to implant wear issues, highlighted the long-term risks of metallic components and their potential legal and financial implications.

Opportunity Analysis - Requirement for Novel Surgical Expertise

Hip resurfacing is technically more demanding than conventional total hip replacement, as it requires precise bone preparation, implant positioning, and alignment to minimize complications such as femoral neck fractures or implant loosening. This complexity restricts the procedure to surgeons with specialized training and experience, limiting widespread adoption.

Hospitals and clinics must invest in innovative surgical training programs and technologies, such as robotic-assisted systems, to improve outcomes, which can be cost-prohibitive. For example, ROSA robotic-assisted hip surgery has demonstrated improved precision; however, its adoption is primarily limited to high-volume orthopedic centers due to the training requirements.

Advancing Surgical Accuracy to Improve Implant Durability

One of the major growth opportunities lies in improving surgical precision, which directly impacts implant longevity and patient outcomes. The integration of robotic-assisted systems and AI-guided preoperative planning enables surgeons to achieve accurate implant positioning, thereby reducing the risk of dislocation, uneven wear, and the need for revision surgeries.

For example, Zimmer Biomet’s ROSA robotic platform has been adopted in several hospitals across North America and Europe, demonstrating improved alignment and a quicker postoperative recovery for patients. By enabling patient-specific surgical approaches, these technological developments reduce human error and enhance implant longevity.

Development of Non-metal Bearing Surfaces

Another key growth avenue is the exploration of non-metal bearing surfaces, including highly cross-linked polyethylene (HXLPE) and ceramic-on-ceramic (CoC) options. Traditional metal-on-metal implants have faced challenges, including metal ion release and associated complications, prompting the market to focus on safer alternatives.

The approval of the ReCerf all-ceramic hip resurfacing implant in Europe demonstrates this shift, providing a metal-free solution that reduces the risk of adverse reactions while maintaining durability. These novel materials offer smooth articulation, low wear rates, and enhanced biocompatibility, thereby creating new opportunities for young patients and those with metal sensitivities.

Category-wise Analysis

Product Type Insights

Total hip replacement (THR) implants are expected to account for approximately 39.4% of the market share in 2025, driven by their established clinical success, versatility, and reliability across a wide range of patients. They provide comprehensive joint replacement, effectively addressing severe osteoarthritis, fractures, and other degenerative hip conditions. Surgeons favor THR for its predictable outcomes, lower revision rates compared to early-generation resurfacing, and compatibility with various surgical techniques.

Hip resurfacing implants are likely to exhibit steady growth as they deliver bone-conserving alternatives for young and active patients who require joint preservation. Unlike total hip replacement, resurfacing maintains more of the femoral bone, allowing for convenient revision if necessary and a better range of motion post-surgery. Recent developments, including ceramic-on-ceramic and highly cross-linked polyethylene options, have enhanced safety by reducing the risks of metal ion release.

Material Insights

Metal implants are speculated to account for approximately 32.7% of the market share in 2025, owing to their strength, durability, and proven track record in load-bearing applications. They can withstand high stress, making them suitable for young patients who require long-lasting support. Cobalt-chrome and titanium alloys are commonly used since they provide excellent biocompatibility and resistance to wear.

Ceramic implants are gaining traction due to their biocompatibility, low wear rates, and elimination of metal ion-related complications. The introduction of all-ceramic resurfacing systems demonstrates rising clinical confidence in metal-free alternatives. Ceramic-on-ceramic (CoC) implants offer smooth articulation, reducing friction and extending implant life, making them an appealing option for patients with metal sensitivities.

End-user Insights

Hospitals are estimated to account for nearly 71.5% of the market share in 2025, as they provide the necessary infrastructure, surgical expertise, and perioperative care for complex hip implant procedures. They can manage high-volume surgeries, provide novel imaging techniques, and maintain sterile operating theaters, all of which are crucial for implant success. Several hospitals also have multidisciplinary orthopedic teams, enabling post-operative rehabilitation and long-term follow-up, which are essential for patient recovery and implant monitoring.

Orthopedic clinics are experiencing considerable growth, driven by their specialization in joint replacement and patient-centered care. Clinics often cater to outpatients, providing consultations, follow-up care, and minimally invasive procedures, which are common for hip resurfacing.

They also deliver personalized treatment plans and specialized expertise, attracting patients who seek customized orthopedic solutions. The rising adoption of robotic-assisted and navigation-guided surgeries in clinics improves their role in implant procedures.

Regional Insights

North America Hip Resurfacing Implants Market Trends

North America is expected to account for approximately 48.2% of the market share in 2025, driven by advancements in implant technology and a growing patient population. The U.S. alone is projected to reach approximately US$2.3 Bn by 2032, with a CAGR of nearly 2.4% through 2032. Regulatory developments are also noteworthy.

CytexOrtho, a Durham-based company, has received U.S. Food and Drug Administration (FDA) approval for its ReNew absorbable hip implant, marking a significant milestone in orthopedic innovation.

The company plans to initiate human clinical trials in 2025, with potential FDA approval anticipated by 2028 or 2029. Demographic factors further influence market dynamics. The aging population in North America is contributing to an increased prevalence of osteoarthritis and hip fractures, leading to a high demand for hip resurfacing procedures.

Asia Pacific Hip Resurfacing Implants Market Trends

In the Asia Pacific, the market is experiencing considerable growth, driven by an aging population, rising urbanization, and advancements in medical technology. A notable development in the region is the approval of the ReCerf Hip Resurfacing Arthroplasty by Australia's Therapeutic Goods Administration (TGA) in December 2024. This implant is the world's first all-ceramic hip resurfacing system to receive regulatory approval, marking a valuable milestone in joint replacement technology and patient care.

The market is also witnessing technological developments, including the launch of hybrid alloys and titanium-based materials. These are likely to help in addressing long-standing safety issues associated with traditional implants. These developments are expected to improve the adoption of hip resurfacing procedures across the region.

Europe Hip Resurfacing Implants Market Trends

In Europe, the market is evolving with constant developments in implant materials and regulatory approvals. A key development is the ReCerf Hip Resurfacing Arthroplasty, which received its CE mark in July 2025. This implant, developed by MatOrtho in collaboration with CeramTec, is the world's first all-ceramic hip resurfacing implant approved by a regulatory authority.

Made with BIOLOX®delta ceramic-on-ceramic material, it delivers a metal-free alternative to traditional implants, aiming to reduce complications associated with metal-on-metal devices. Another significant milestone is the H1 implant, developed by Embody Orthopaedic. The device received the CE mark in July 2025, in accordance with the European Union’s new Medical Device Regulation (MDR) guidelines. It is the first non-metal resurfacing implant to receive regulatory approval worldwide.

Competitive Landscape

Renowned orthopedic device manufacturers dominate the global hip resurfacing implants market. Zimmer Biomet, DePuy Synthes, and Stryker Corporation are leading players, embracing their extensive product portfolios and global reach to maintain market leadership.

Smith & Nephew, B. Braun Melsungen AG, and Corin also hold significant positions, delivering novel solutions and focusing on specific market segments. The market is also witnessing technological developments, with companies investing in research and development to improve implant designs and surgical techniques.

Business Strategies

Emerging business model trends in the market include the adoption of value-based healthcare models, where companies focus on patient outcomes rather than the volume of procedures. Additionally, there is a shift toward personalized medicine, with implants being customized to individual patient anatomies, improving the fit and function of the implants. These trends reflect a broad market move toward patient-centered care and operational efficiency.

Key Industry Developments:

- In September 2025, Zimmer Biomet Holdings, Inc. received approval from the Pharmaceutical and Medical Devices Agency (PMDA) in Japan for iTaperloc Complete and iG7 Hip System. It is the world’s first approved orthopedic implant featuring Iodine Technology, which inhibits bacterial adhesion on the implant surface.

- In February 2024, Hip Innovation Technology, LLC, announced that its flagship product, the Reverse Hip Replacement System (Reverse HRS), was showcased at the 2024 American Academy of Orthopaedic Surgeons (AAOS) annual meeting. The presentation also included five-year RSA and patient-recorded outcome measures.

Companies Covered in Hip Resurfacing Implants Market

- Smith & Nephew Plc

- Johnson & Johnson

- Zimmer Biomet

- Stryker Corp.

- Exactech, Inc.

- MicroPort Scientific Corp.

- OMNIlife Science, Inc.

- DJO Global, Inc.

- B. Braun Melsungen AG

- ConMed Corp.

- Aesculap Implant Systems, LLC

Frequently Asked Questions

The hip resurfacing implants market is projected to reach US$5.4 Bn in 2025.

Rising traumatic hip injuries and an aging population are the key market drivers.

The hip resurfacing implants market is poised to witness a CAGR of 2.7% from 2025 to 2032.

The development of polyethylene implants and the emergence of minimally invasive surgical solutions are the key market opportunities.

Smith & Nephew Plc, Johnson & Johnson, and Zimmer Biomet are a few key market players.