- Medical Devices

- Heart Attack Diagnostics Market

Heart Attack Diagnostics Market Size, Share, and Growth Forecast 2026 - 2033

Heart Attack Diagnostics Market By Test Type (Electrocardiogram, Blood Test, Computerized Cardiac Tomography, Others), End-user (Hospitals, Ambulatory Surgical Centers), and Regional Analysis for 2026 - 2033

Heart Attack Diagnostics Market Size and Trends Analysis

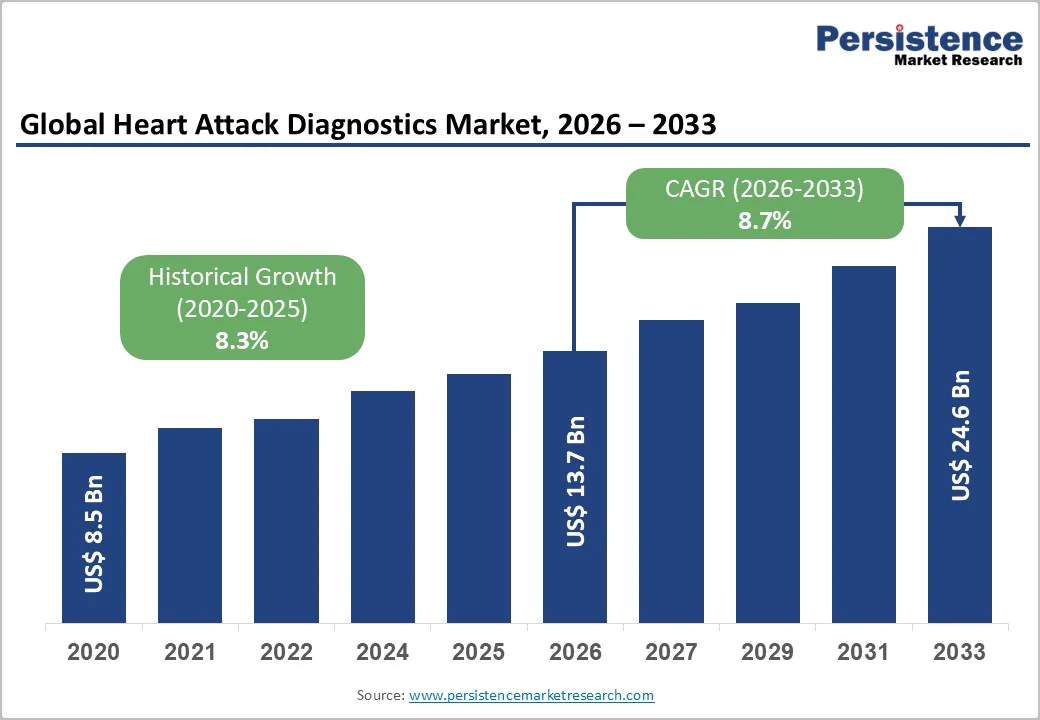

The global heart attack diagnostics market size is likely to be valued at US$13.7 billion in 2026 and is expected to reach US$24.6 billion by 2033 growing at a CAGR of 8.7% during the forecast period from 2026 to 2033, driven by the rising prevalence of cardiovascular diseases and increasing heart-disease-related mortality, which continues to accelerate the adoption of diagnostic tools such as ECG, cardiac biomarkers, and troponin tests.

Technological advances in AI-enabled diagnostics, point-of-care testing, and high-sensitivity biomarkers are boosting early detection and clinical accuracy. Growth is further supported by expanding healthcare infrastructure, rising demand for emergency care, greater awareness of preventive cardiac screening, and increasing adoption of rapid, portable diagnostic tools for faster triage.

Key Industry Highlights

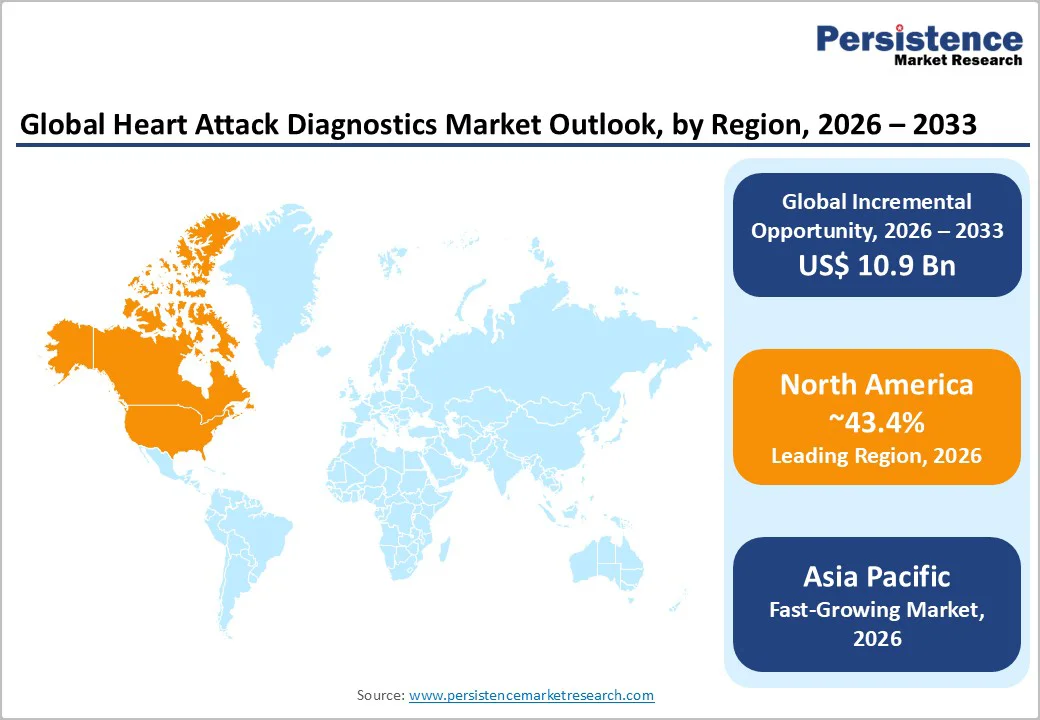

- Leading Region: North America is anticipated to lead the market with around 43.4% share in 2026, driven by advanced technology adoption, high healthcare spending, awareness campaigns, and FDA-backed innovations such as AI-ECG, competitive leadership from GE Healthcare and Roche, and growing opportunities in rural point-of-care access.

- Fastest-growing Region: Asia Pacific to emerge as the fastest-growing region, driven by rapid urbanization in China, Japan, and India, surging CVD prevalence, infrastructure investments, aging populations, and awareness programs, with Japan leading in advanced technology adoption.

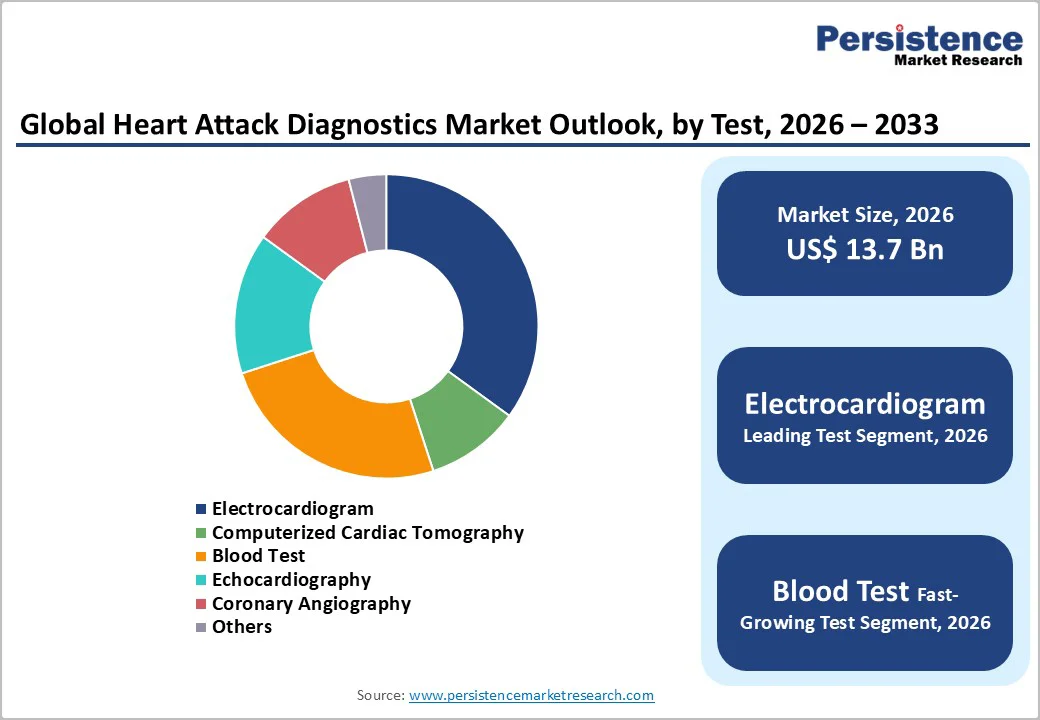

- Leading Test Type: Electrocardiogram is anticipated to lead the heart attack diagnostics market, capturing around 35% share in 2026, driven by its non-invasive speed, cost-effectiveness, and widespread hospital adoption.

- Fastest-Growing Product Type: Blood tests represent the fastest-growing, fueled by high-sensitivity biomarkers and rising demand for early CVD detection.

- Leading End-user Type: The hospitals segment is likely to lead the market with over 46.3% market share, offering comprehensive cardiac diagnostic tools and leveraging high patient volumes and emergency infrastructure.

- Fastest-growing End-user: Ambulatory surgical centers represent the fastest-growing segment, driven by outpatient cost savings and the increasing shift toward non-emergency cardiac testing.

| Key Insights | Details |

|---|---|

| Heart Attack Diagnostics Market Size (2026E) | US$13.7 Bn |

| Market Value Forecast (2033F) | US$24.6 Bn |

| Projected Growth CAGR (2026 - 2033) | 8.7% |

| Historical Market Growth (2020 - 2025) | 8.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Cardiovascular Disease Incidence

Rising cardiovascular disease (CVD) incidence remains one of the most influential drivers shaping the cardiac diagnostics market, as global cases continue to escalate due to aging populations, sedentary lifestyles, air pollution exposure, and metabolic disorders such as diabetes and hypertension.

In major markets such as the U.S., Europe, China, and India, CVD consistently ranks as the leading cause of mortality, prompting healthcare systems to prioritize early detection.

Hospitals and outpatient centers are adopting technologically advanced diagnostic solutions, including AI-enabled ECG interpretation, portable testing platforms, and high-sensitivity biomarker assays to efficiently manage growing patient volumes. The shift toward preventive healthcare further supports market growth, as clinicians emphasize early risk assessment to reduce emergency admissions and long-term treatment costs.

Regulatory Hurdles

Regulatory hurdles remain a significant restraint in the cardiac diagnostics market, as companies must navigate stringent approval pathways that vary widely across regions. Cardiac technologies must demonstrate high accuracy, reproducibility, and clinical safety, which demands extensive clinical trials, multi-stage validation, and continuous performance monitoring.

These requirements often prolong development timelines and increase overall costs, slowing the entry of innovative tools such as portable ECGs, high-sensitivity blood tests, and advanced imaging platforms.

Cardiac diagnostics fall within some of the most tightly monitored categories of medical devices due to their direct role in patient survival, necessitating rigorous documentation, post-market surveillance, and adherence to quality management systems. This high compliance burden challenges smaller companies and start-ups, which may struggle with the financial and operational demands of regulatory processes.

Delays in certification also hinder the timely adoption of new technologies by healthcare providers, slowing market expansion.

Personalized Diagnostics

Healthcare shifts from generalized evaluation to patient-specific risk prediction, monitoring, and treatment planning. Advances in genomics and high-sensitivity biomarkers are enabling clinicians to detect subtle variations in cardiac function, predict disease progression, and tailor interventions earlier than ever before.

Tools such as AI-ECG algorithms, multi-omics cardiac panels, and individualized imaging assessment are helping identify high-risk patients long before symptoms appear, reducing emergency events and improving long-term outcomes.

The rise of wearable cardiac devices, remote monitoring platforms, and cloud-integrated reporting systems supports personalized care by delivering continuous, real-time data rather than one-time test results.

These technologies enable cardiologists to tailor treatment plans to each patient’s unique physiological patterns, improving diagnostic precision and reducing unnecessary procedures. Healthcare providers increasingly prioritize preventive and precision medicine; demand for personalized cardiac diagnostic solutions is expected to accelerate.

Category-wise Analysis

Test Type Insights

The electrocardiogram is anticipated to lead the global heart attack diagnostics market, capturing around 35% of total revenue share in 2026, owing to its indispensable role in rapid cardiac assessment. ECG’s non-invasive nature, immediate results, and widespread availability in hospitals and emergency departments make it the first-line tool for detecting arrhythmias, myocardial ischemia, conduction disorders, and acute cardiac events.

For example, major healthcare systems in the U.S. and Europe have expanded deployment of portable and wireless ECG devices to accelerate triage in emergency settings, improving early detection rates. Its cost-effectiveness and ease of use further strengthen adoption across high- and low-resource settings.

Blood tests, particularly those measuring cardiac biomarkers such as troponin, represent the fastest-growing segment and are likely to be supported by the rising demand for early, sensitive detection of myocardial injury. High-sensitivity assays are improving diagnostic accuracy for acute coronary syndrome and facilitating faster triage decisions.

For example, the increasing adoption of hs-cTn I and T assays in hospitals across North America and Europe, where clinicians rely on rapid biomarker testing to shorten door-to-diagnosis times for patients suspected of having a heart attack. Growth is also propelled by the shift toward decentralized testing, with point-of-care (POC) troponin devices reducing dependence on centralized laboratories and enabling quicker clinical decisions.

End-user Insights

The hospitals segment is expected to lead the market, accounting for around 46.3% of total revenue in 2026, owing to their comprehensive infrastructure and access to advanced diagnostic equipment. Facilities such as ECG units, cardiac CT, echocardiography labs, and angiography suites are typically concentrated within hospitals, enabling full-spectrum cardiac evaluation in both emergency and scheduled care settings.

For example, major tertiary hospitals in the U.S. and Europe routinely manage high patient volumes and deploy integrated cardiac emergency response teams combining ECG, biomarker testing, and imaging, ensuring rapid and accurate diagnosis of acute coronary syndromes. The availability of trained cardiologists, round-the-clock emergency care, and robust cardiac care units reinforces hospitals’ dominant position in heart-attack diagnostics.

Ambulatory surgical centers represent the fastest-growing end-user segment, driven by the healthcare industry's shifts toward cost-efficient outpatient cardiac care. ASCs offer faster turnaround times, reduced procedure costs, and streamlined diagnostic workflows, making them increasingly attractive for non-emergency cardiac assessments.

With improvements in portable imaging, handheld ECGs, and compact biomarker analyzers, many diagnostic procedures traditionally performed in hospitals can now be safely completed in outpatient settings. For example, outpatient cardiology clinics are increasingly adopting handheld ECG devices and portable echocardiography systems to quickly assess chest discomfort, enabling earlier detection of ischemic changes without sending every patient to a hospital.

Regional Insights

North America Heart Attack Diagnostics Market Trends

North America is projected to be the leading region, accounting for 43.4% of the market share in 2026, driven by its advanced healthcare infrastructure, high disease burden, and rapid adoption of cutting-edge diagnostic technologies. The region’s strong focus on early detection and on efficiency in emergency care has accelerated the use of high-sensitivity cardiac biomarkers, particularly troponin assays.

Extensive integration of ECG-based screening, cardiac imaging, and rapid laboratory workflows across hospitals further strengthens its leadership.

North America is seeing an increase in the implementation of AI-driven diagnostic tools, which enhance accuracy and speed in emergency decision-making.

AI-enabled ECG interpretation systems and algorithm-supported risk stratification platforms are increasingly utilized to differentiate cardiac from non-cardiac chest pain, reducing diagnostic uncertainty and improving outcomes. Growth in portable and point-of-care diagnostic devices is also transforming care delivery, enabling immediate assessment in ambulances, urgent care centers, and remote settings.

Europe Heart Attack Diagnostics Market Trends

Europe remains a significant market for heart attack diagnostics, due to the high prevalence of cardiovascular disease, and increased public-health awareness drives demand for timely, accurate diagnosis. The region remains a major global hub, accounting for roughly a quarter to a third of the worldwide market share.

There is strong uptake of high-sensitivity cardiac biomarker assays across hospitals and clinics, with the majority of European laboratories now using high-sensitivity methods and structured serial-sampling protocols for early myocardial injury detection.

Europe is experiencing rising demand as artificial intelligence and digital health tools are increasingly integrated into diagnostic workflows to enhance speed and accuracy. AI-driven ECG models can now identify blocked coronary arteries with accuracy comparable to high-sensitivity troponin tests, offering significant potential to streamline emergency diagnosis in high-volume hospital settings.

The region is also seeing wider adoption of portable and point-of-care testing systems, enabling rapid diagnostics beyond traditional laboratory settings, improving access, and shortening time to treatment.

Asia Pacific Heart Attack Diagnostics Market Trends

Asia Pacific is likely to be the fastest-growing region in the global heart attack diagnostics market in 2026, driven by rapidly increasing cardiovascular disease incidence, large aging populations, and expanding healthcare infrastructure across China, India, Japan, and Southeast Asia.

The region’s accelerating urbanization, lifestyle shifts, and rising prevalence of diabetes and hypertension are contributing to a substantial rise in heart attack cases, pushing healthcare systems to adopt faster and more reliable diagnostic tools.

The Asia Pacific region is experiencing rapid adoption of digital and AI-enabled cardiac diagnostics. Countries such as Japan, South Korea, China, and Singapore are investing heavily in smart healthcare technologies, enabling AI-driven ECG interpretation, remote cardiac monitoring, and cloud-based decision-support platforms.

The growing availability of portable and point-of-care testing devices is improving accessibility in rural and underserved regions, where traditional laboratory infrastructure is limited.

Competitive Landscape

The global heart attack diagnostics market exhibits a moderately fragmented structure, driven by rising CVD incidence, rapid innovation in high-sensitivity biomarkers and imaging, and expanding point-of-care capabilities that encourage both established and niche players to invest aggressively in diagnostics.

With key leaders including GE Healthcare, F. Hoffmann-La Roche, Siemens Healthineers, Abbott, and Philips. These incumbents lead through broad portfolios spanning ECG systems, high-sensitivity troponin assays, cardiac imaging platforms, and integrated software solutions.

These players compete through sustained R&D and product differentiation, notably AI-enabled ECG interpretation, faster POC troponin tests, and integrated diagnostic workflows that shorten time-to-treatment, and by pursuing partnerships, strategic acquisitions, and expanded service networks to secure market access.

Recent M&A and investment activity have strengthened imaging and AI capabilities, forcing regional vendors to respond with lower-cost or specialized solutions for emerging markets.

Key Industry Developments:

- In April 2024, GE HealthCare showcased Caption AI on Vscan Air SL at the American College of Cardiology Expo, featuring AutoEF to automatically calculate ejection fraction and help more clinicians confidently capture cardiac images for rapid assessments.

- In July 2025, Philips launched its ECG AI Marketplace, a unified platform enabling cardiac teams to access and deploy AI-powered diagnostic tools from multiple vendors for faster, more accurate early detection.

- In November 2025, Caristo’s CaRi-Plaque™ secured Medicare reimbursement, enabling hospitals and clinics to adopt its AI-driven plaque analysis tool for streamlined, preventive heart attack assessment.

Companies Covered in Heart Attack Diagnostics Market

- GENERAL ELECTRIC

- FUJIFILM Holdings

- Koninklijke Philips N.V.

- Midmark Corporation

- F. Hoffmann-La Roche Ltd

- SCHILLER

- Beckman Coulter, Inc.

- Toshiba Corporation

- Hill-Rom Services (Welch Allyn)

Frequently Asked Questions

The heart attack diagnostics market is valued at US$13.7 billion in 2026 and is expected to reach US$24.6 billion by 2033, reflecting robust growth.

Key drivers include rising cardiovascular disease prevalence, rapid adoption of advanced diagnostic technologies, and increasing emphasis on early and accurate detection.

The hospitals segment leads the market with over 46.3% market share in 2026, offering comprehensive cardiac diagnostic tools and leveraging high patient volumes and emergency infrastructure.

North America leads the market with about 43.4% share, driven by advanced technology adoption, high healthcare spending, strong public awareness, and FDA-supported innovations like AI-enabled ECG systems. The presence of major players such as GE Healthcare and Roche, along with growing point-of-care opportunities in rural areas, further strengthens regional growth.

A key opportunity lies in expanding AI-enabled and personalized diagnostic solutions for faster, more precise cardiac risk detection.