- Medical Devices

- Congestive Heart Failure Treatment Devices Market

Congestive Heart Failure Treatment Devices Market Size, Share, and Growth Forecast, 2025 - 2032

Congestive Heart Failure Treatment Devices Market by Product Type (Ventricular Assist Devices (VADs), Implantable Cardioverter Defibrillators (ICD), Pacemakers, Cardiac Resynchronization Therapy, Counter Pulsation Devices), End-user, and Regional Analysis for 2025 - 2032

Congestive Heart Failure Treatment Devices Market Size and Trends Analysis

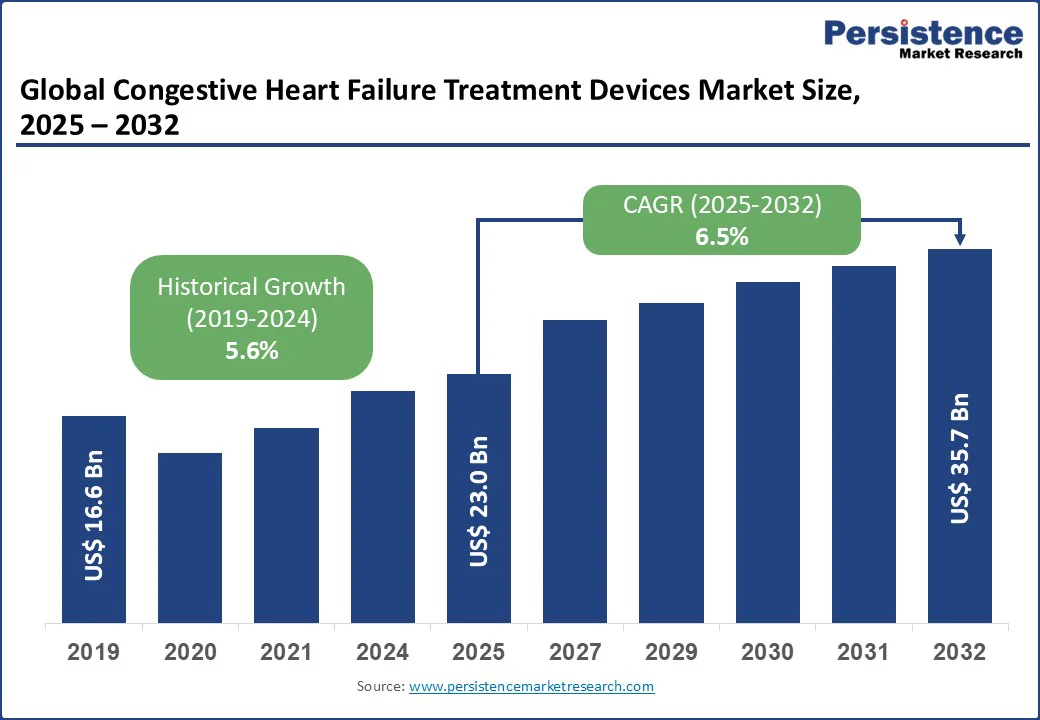

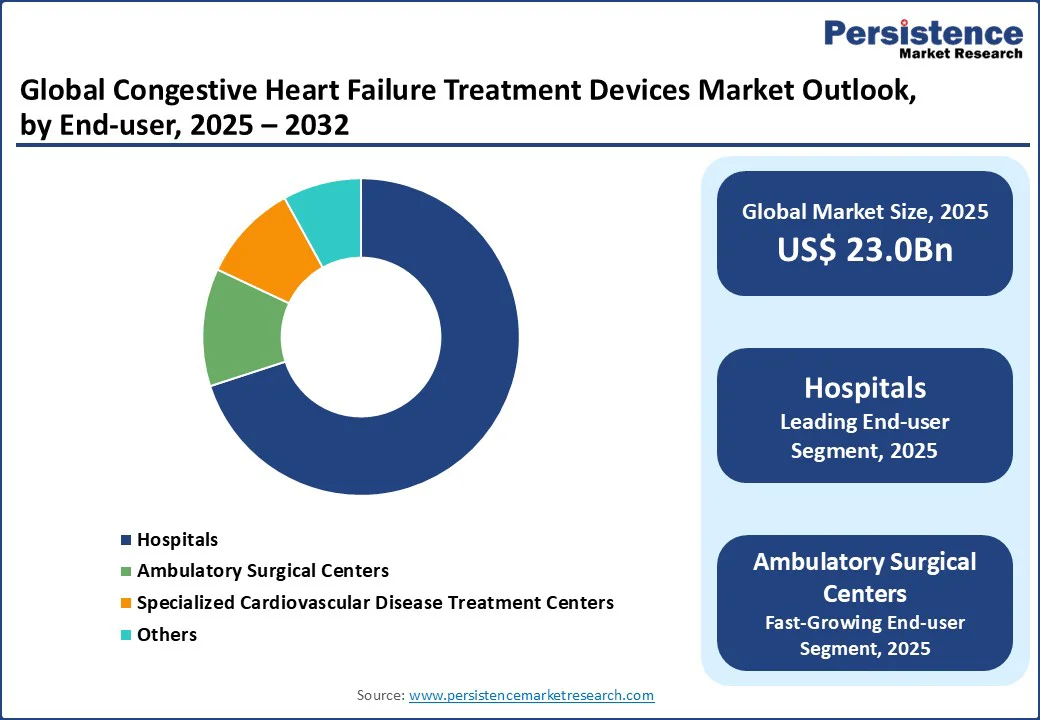

The global congestive heart failure treatment devices market size is likely to be valued at US$23.0 Bn in 2025 and US$35.7 Bn by 2032, registering a robust CAGR of 6.5% during the forecast period from 2025 to 2032.

The industry has experienced significant growth, fueled by the increasing demand for advanced cardiac care solutions, advancements in implantable device technologies, and a global push toward managing chronic heart conditions.

Key Industry Highlights:

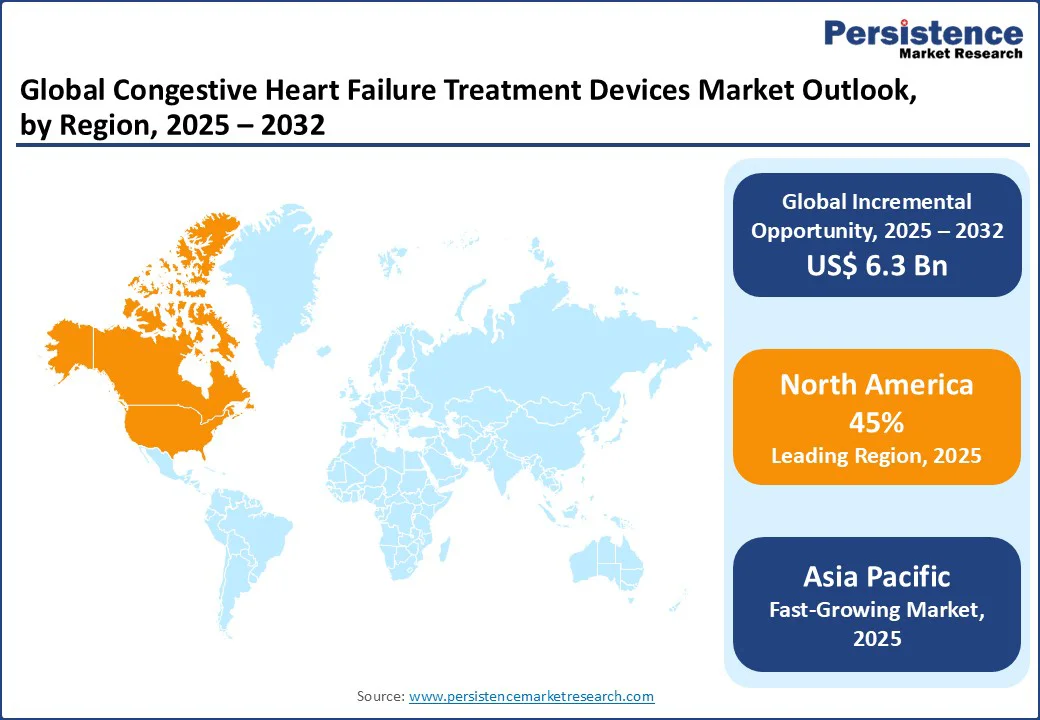

- Leading Region: North America holds a 45% market share in 2025, driven by advanced healthcare infrastructure, widespread adoption of innovative cardiac devices, and significant investments in cardiovascular research.

- Fastest-growing Region: Asia Pacific, propelled by increasing prevalence of heart diseases, urbanization, and expanding healthcare access in countries such as China and India.

- Dominant Product Type: Ventricular Assist Devices (VADs) account for approximately 45% share in 2025, owing to their critical role in mechanical circulatory support and advancements in durability.

- Leading End-user: Hospitals lead with a 70% share, reflecting its critical role in acute care and device implantation procedures.

| Key Insights | Details |

|---|---|

| Congestive Heart Failure Treatment Devices Market Size (2025E) | US$23.0 Bn |

| Market Value Forecast (2032F) | US$35.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.6% |

Market Dynamics

Driver - Rising Demand for Advanced Cardiac Care Amid Increasing Prevalence of Heart Failure

The global surge in demand for advanced cardiac care is a primary driver of the congestive heart failure treatment devices market. According to the European Society of Cardiology, heart failure affects more than 60 million people worldwide, with its advanced stages being more deadly than most malignancies.

This alarming prevalence is exacerbated by an aging population and rising lifestyle-related risk factors, with cardiovascular diseases becoming a leading global health burden. In response, governments and healthcare organizations are investing heavily in cardiac infrastructure, with the United States leading in the adoption of devices such as ventricular assist devices (VADs) to support end-stage heart failure patients.

In Europe, where heart failure cases are steadily increasing, initiatives such as international congresses highlight the growing focus on innovative treatments.

Restraint - High Initial Costs and Need for Skilled Personnel

The congestive heart failure treatment devices market faces significant challenges due to high initial costs and the requirement for skilled personnel. Implanting advanced devices such as ventricular assist devices (VADs) involves specialized procedures and equipment, which can be extremely expensive, including surgery and follow-up care, thereby deterring adoption in developing regions.

These expenses are further compounded by the need for rigorous clinical trials and strict regulatory approvals, which increase development costs and delay market entry. Additionally, the lack of standardized implantation techniques leads to variability in patient outcomes, raising the risk of complications and rework costs.

Another major restraint is the shortage of skilled cardiologists and surgeons proficient in device implantation. Training opportunities remain limited, and expertise is largely concentrated in developed regions such as North America and Europe, making it difficult for emerging markets to scale adoption.

Regulatory hurdles, including complex approval processes for new devices, further escalate costs and timelines. Collectively, these challenges can deter smaller healthcare facilities and slow market penetration in cost-sensitive sectors such as ambulatory surgical centers.

Opportunity - Innovation in Sustainable Systems and Multi-Application Use

Technological innovations in congestive heart failure (CHF) treatment devices are opening significant growth opportunities, particularly as healthcare shifts toward minimally invasive and patient-centric care. The development of next-generation solutions, such as wireless ventricular assist devices (VADs) and bioresorbable implants, is transforming the congestive heart failure treatment devices market landscape.

Advanced VADs with compact, more durable pumps enable extended use as destination therapy, offering viable alternatives for patients who are not candidates for heart transplants. These devices also support improved mobility and quality of life, addressing long-standing limitations of traditional systems.

Furthermore, integration with remote monitoring and telemedicine platforms enhances real-time patient management, allowing healthcare providers to track performance and intervene proactively.

Hybrid devices are also being tailored to address specific conditions such as heart failure with preserved ejection fraction (HFpEF), broadening therapeutic options. Alongside these advances, emerging markets are prioritizing affordable and scalable solutions, while collaborations between medical technology companies and research institutions accelerate innovation and commercial adoption.

Category-wise Analysis

Product Type Insights

The congestive heart failure treatment devices market is segmented into ventricular assist devices (VADs), implantable cardioverter defibrillators (icd), pacemakers, cardiac resynchronization therapy, and counter pulsation devices.

Implantable cardioverter defibrillators (ICD) dominate, holding approximately 45% share in 2025, due to their proven efficacy in preventing arrhythmias, life-saving shock delivery, and integration into standard heart failure protocols. ICDs are widely used in high-risk patients, offering remote monitoring capabilities that reduce hospital readmissions.

Ventricular assist devices (VADs) are the fastest-growing segment, driven by increasing demand for mechanical support in end-stage heart failure. VADs provide circulatory assistance as bridge-to-transplant or destination therapy, with advancements in durability and miniaturization making them suitable for long-term use in aging population.

End-user Insights

The global congestive heart failure treatment devices market is divided into hospitals, specialized cardiovascular disease treatment centers, and ambulatory surgical centers. Hospitals dominate with a 70% share in 2025, driven by their role in acute interventions and comprehensive care. Hospitals handle complex implantations and post-operative management, supported by multidisciplinary teams.

Ambulatory surgical centers are the fastest-growing end-user segment, propelled by the shift toward outpatient procedures and cost-effective care. These centers offer minimally invasive device implantations, reducing hospital stays and aligning with healthcare cost-containment efforts.

Regional Insights

North America Congestive Heart Failure Treatment Devices Market Trends

North America dominates the global congestive heart failure treatment devices market, expected to account for 40% of market share in 2025. The region benefits from a high prevalence of heart failure, which continues to fuel demand for advanced treatment options, including ventricular assist devices (VADs), implantable cardioverter defibrillators (ICDs), and pacemakers. Strong healthcare infrastructure and significant investment in cardiac research and device innovation further strengthen the industry.

A key trend is the adoption of AI-integrated VADs, enabling personalized treatment and monitoring in both specialized hospitals and ambulatory care centers. Additionally, regulatory support has accelerated the availability of novel devices targeting heart failure with preserved ejection fraction (HFpEF), expanding treatment options. Collaborations with leading medtech companies, such as Medtronic, continue to reinforce North America’s leadership position.

Europe Congestive Heart Failure Treatment Devices Market Trends

Europe holds a significant share of the global congestive heart failure (CHF) treatment devices market, with the UK, Germany, and France leading regional growth. The UK is advancing through large-scale investments in cardiac resynchronization programs, which are driving higher adoption of implantable cardioverter defibrillators (ICDs) and related therapies. Germany’s strong network of advanced heart centers supports the widespread use of ventricular assist devices (VADs), particularly in managing complex heart failure cases.

France is focusing on modernizing pacemaker systems with upgrades that emphasize personalized and patient-friendly therapy, reflecting its commitment to innovation in cardiac care. Additionally, the European Union’s stringent medical device regulations and sustainability initiatives are encouraging the development of safer, eco-friendly implants, creating opportunities for manufacturers while ensuring high standards of patient safety.

Asia Pacific Congestive Heart Failure Treatment Devices Market Trends

Asia Pacific is the fastest-growing region in the global congestive heart failure (CHF) treatment devices market, driven by the healthcare momentum in China, India, and Japan. China’s rapid expansion of healthcare infrastructure and rising prevalence of heart disease are fueling demand for pacemakers and implantable cardioverter defibrillators (ICDs). India’s large-scale cardiovascular health initiatives, combined with growing public and private investments, are accelerating the adoption of ventricular assist devices (VADs) and advanced monitoring technologies.

Japan, with its rapidly aging population, is witnessing a sharp rise in device demand, particularly for pacemakers and cardiac resynchronization therapy (CRT). Expanding hospital networks, growing access to specialized cardiac centers, and rising healthcare budgets across the region further strengthen market growth, making Asia Pacific a critical hub for innovation and adoption in heart failure management.

Competitive Landscape

The global congestive heart failure treatment devices market is highly competitive, with global and regional players competing through innovation, competitive pricing, and reliability. The rise of AI-integrated devices and minimally invasive technologies intensifies competition, as companies strive to meet the diverse needs of cardiac care sectors. Strategic partnerships, mergers, and certifications for medical standards are key differentiators in this dynamic market.

Key Developments

- January 2025: Alleviant Medical Inc. received FDA Breakthrough Device designation for its no-implant atrial shunt. The device, intended for heart failure patients with reduced ejection fraction, creates a connection between the left and right atria via a single procedure without leaving a permanent implant behind.

- December 2024: The FDA has expanded the indications for the Impella 5.5 with SmartAssist and Impella CP with SmartAssist heart pumps, according to a statement from Johnson & Johnson MedTech. An important step forward in the treatment options for critically ill children has been made possible by this premarket approval, which permits their use in specific pediatric patients with symptomatic acute decompensated heart failure and cardiogenic shock.

Companies Covered in Congestive Heart Failure Treatment Devices Market

- Jarvik Heart Inc.

- ReliantHeart, Inc.

- Biotronik SE & Co. KG

- Berlin Heart GmbH

- Medtronic

- Boston Scientific Corp.

- Biotronik SE & Co. KG

- Abbott

Frequently Asked Questions

The congestive heart failure treatment devices market is projected to reach US$23.0 Bn in 2025.

Rising prevalence of heart failure, technological advancements in devices, and government initiatives for cardiac care are key drivers.

The congestive heart failure treatment devices market is poised to witness a CAGR of 6.5% from 2025 to 2032.

Innovations in AI-integrated devices and multi-application solutions, such as remote monitoring, present significant growth opportunities.

Medtronic, Boston Scientific Corp., Abbott, and Biotronik SE & Co. KG are among the leading players, known for their innovative cardiac solutions.