- Bulk Chemicals

- Ground And Precipitated Calcium Carbonate Market

Ground And Precipitated Calcium Carbonate Market Size, Share, and Growth Forecast 2025 - 2032

Ground and Precipitated Calcium Carbonate Market Analysis By Product (Ground Calcium Carbonate (GCC), Precipitated Calcium Carbonate(PCC)), Industry (Paper, Plastics, Paints & Coatings, Adhesives & Sealants), and Regional Analysis 2025 - 2032

Ground and Precipitated Calcium Carbonate Market Share and Trends Analysis

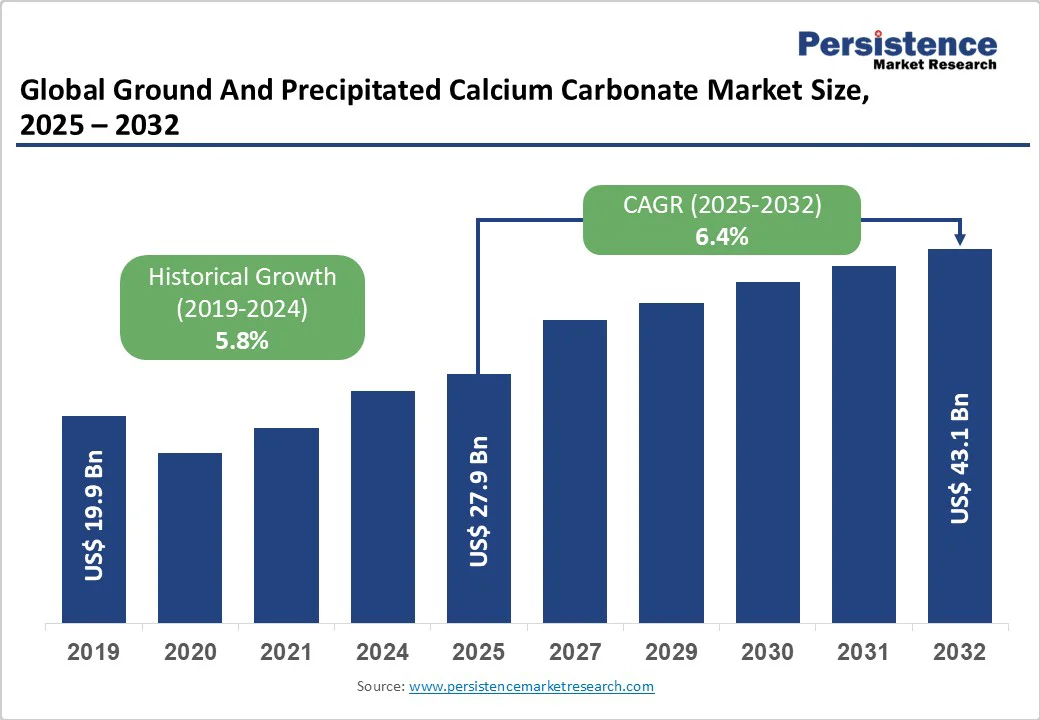

The global ground and precipitated calcium carbonate market size is likely to be valued at US$27.9 billion in 2025 and is projected to reach US$43.1 billion by 2032, growing at a CAGR of 6.4% between 2025 and 2032. Robust demand from the paper and packaging industries is driving market expansion, as manufacturers seek cost-effective mineral fillers to enhance product performance while reducing production costs.

The growing applications of plastics, construction materials, and pharmaceutical formulations further accelerate market growth, supported by technological advances in surface treatment and nanoparticle development.

Key Market Highlights:

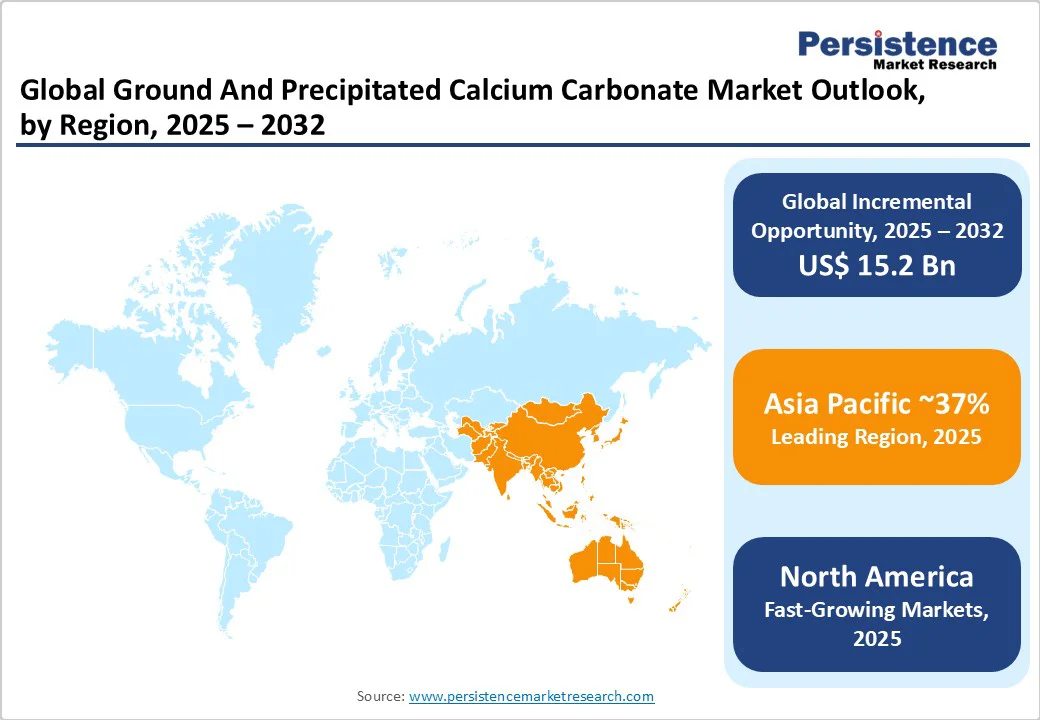

- Leading Region: Asia Pacific leads global consumption with 37% market share, driven by rapid industrialization, infrastructure development, and manufacturing competitiveness in China, Japan, and India.

- Fastest-Growing Region: North America is the fastest-growing regional market, with a 5.8% CAGR, driven by technological innovation, regulatory compliance requirements, and expanding construction activity

- .

- Leading Product Type: Ground Calcium Carbonate dominates the product segments with a 68% market share, driven by its cost-effectiveness, abundant raw material availability, and widespread applications.

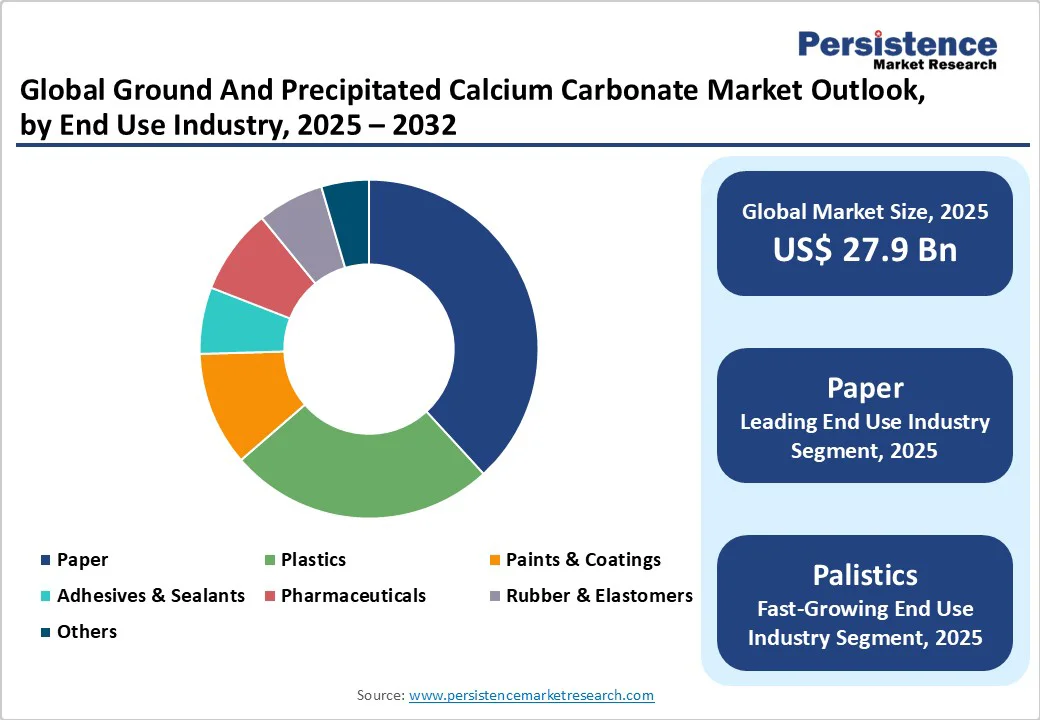

- Leading End-Use segment: The paper industry maintains its position as the largest end-use segment, accounting for 42% of the total market volume through coating and filler applications.

- Key Market Opportunity: Pharmaceutical and nutraceutical applications present a key growth opportunity with increasing demand for high-purity PCC driven by health consciousness and an aging population.

| Key Insights | Details |

|---|---|

|

Ground And Precipitated Calcium Carbonate Size (2025E) |

US$27.9 billion |

|

Market Value Forecast (2032F) |

US$43.1 billion |

|

Projected Growth CAGR (2025-2032) |

6.4% |

|

Historical Market Growth (2019-2024) |

5.8% |

Market Dynamics

Drivers - Expanding Paper and Packaging Industry Demand

The paper and packaging industry remains the largest consumer of calcium carbonate, accounting for nearly 42% of total global demand. Ground Calcium Carbonate (GCC) and Precipitated Calcium Carbonate (PCC) are widely used as fillers and coating pigments due to their ability to enhance the performance characteristics of paper significantly. They improve opacity, smoothness, and printability while ensuring brightness levels above 95%. Moreover, these additives help reduce dependence on costly wood pulp, lowering overall production expenses for paper manufacturers without compromising quality.

In recent years, the surge in e-commerce has fueled an unprecedented rise in the consumption of corrugated packaging materials. Global paper production reached nearly 450 million tonnes in 2024, driven by strong demand for packaging across the retail, food delivery, and logistics sectors. PCC, with its uniform particle size and superior brightness, has gained prominence in high-quality printing and premium paper grades, where visual appearance and durability are crucial.

Growing Plastic Industry Applications and Construction Sector Expansion

The plastics industry is rapidly incorporating calcium carbonate as a key reinforcing filler due to its cost-effectiveness and performance-enhancing properties. By substituting 15–20% of polymers with calcium carbonate, manufacturers can reduce raw material usage while improving the tensile strength, rigidity, impact resistance, and dimensional stability of plastic products. Applications range from automotive parts and household appliances to packaging films, where calcium carbonate provides both mechanical benefits and aesthetic enhancements such as improved surface finish and reduced shrinkage. Global plastic production reached about 390 million tonnes in 2023, underscoring the scale of opportunity for calcium carbonate suppliers.

Meanwhile, the construction sector has emerged as another strong growth driver. Expanding infrastructure projects in developing economies are generating substantial demand for paints, coatings, adhesives, sealants, and cement, where calcium carbonate acts as an extender pigment. Its properties improve opacity, weather resistance, and durability in architectural and industrial coatings. According to the U.S. Census Bureau, construction spending rose by 6.4% in 2024, strengthening the demand outlook for calcium carbonate in decorative paints and protective coatings across residential, commercial, and industrial applications.

Restraints - Environmental Regulations and Mining Restrictions

Stringent environmental regulations governing limestone quarrying and calcium carbonate processing continue to pose a significant challenge for global producers. Authorities in North America and Europe have tightened requirements for mining permits and environmental impact assessments, delaying new quarry development and increasing compliance costs. Producers are required to follow stricter reclamation practices and pollution control measures, which adds further operational expenses.

PCC production involves an energy-intensive calcination process that generates considerable carbon emissions. With growing concerns about climate change, manufacturers are under pressure to adopt low-carbon technologies, energy-efficient machinery, and renewable energy sources. Failure to adapt to these environmental mandates risks fines, operational restrictions, and reputational damage in highly regulated markets.

Competition from Alternative Filler Materials and Raw Material Volatility

The calcium carbonate industry is increasingly challenged by competition from alternative filler materials, including talc, kaolin, and engineered synthetic materials. These substitutes often provide distinct advantages in certain applications, such as enhanced smoothness in cosmetics or superior heat resistance in plastics, reducing calcium carbonate’s competitive edge in niche markets.

At the same time, the market faces price volatility in limestone raw materials, coupled with rising transportation and energy costs. This creates pressure on profit margins, particularly in high-purity applications that require advanced processing. Emerging bio-based fillers and recycled alternatives, aligned with the principles of the circular economy, are also gaining traction. Their sustainability appeal positions them as potential substitutes, particularly in environmentally conscious sectors such as packaging and construction.

Opportunities - Pharmaceutical and Nutraceutical Sector Expansion

The pharmaceutical and nutraceutical industries offer significant opportunities for high-purity Precipitated Calcium Carbonate (PCC). Its superior biocompatibility, consistent particle morphology, and controlled quality make it highly suitable for dietary supplements, antacids, and drug excipient formulations. Rising health awareness, particularly regarding calcium deficiency and bone health, has increased demand among aging populations and health-conscious consumers. This trend supports the use of pharmaceutical-grade PCC, which provides reliable calcium supplementation in a form that is easily absorbed.

Pharmaceutical-grade calcium carbonate requires advanced processing and strict adherence to purity standards, allowing qualified manufacturers to command premium prices. Expanding demand for osteoporosis prevention, coupled with the Marine Calcium Market’s projected 6.0% CAGR from 2024 to 2031, further highlights growth potential. Companies with certifications and strong quality control systems are well positioned to secure higher margins by catering to pharmaceutical and nutraceutical end users worldwide.

Technological Innovation and Sustainable Product Development

Technological advancements are creating new opportunities in the calcium carbonate market, particularly through the application of nanotechnology. Nano-calcium carbonate provides superior dispersion, enhanced surface activity, and improved interaction with polymer matrices, making it highly valuable in automotive components, advanced polymer composites, and specialty coatings. These properties deliver better tensile strength, impact resistance, and functional performance compared to conventional fillers, creating demand in high-performance applications.

The sustainability trend is driving the adoption of eco-friendly materials, with calcium carbonate playing a key role. Its compatibility with biodegradable plastics makes it essential in developing environmentally conscious packaging and green construction materials. Additionally, AI-driven production optimization and predictive demand planning tools are enabling manufacturers to reduce waste, improve energy efficiency, and streamline supply chains. By combining technological innovation with sustainable practices, producers can strengthen competitiveness and align with global sustainability targets.

Category-wise Insights

Product Type Analysis

Ground Calcium Carbonate (GCC) dominates the market with nearly 68% share, largely due to its cost-effectiveness and abundant availability from limestone and marble reserves worldwide. GCC is produced through mechanical crushing and grinding, which requires less energy compared to PCC manufacturing. This makes it a preferred choice for volume-driven industries where affordability and reliable performance are critical. The segment also benefits from well-established production facilities and extensive supplier networks that support its global presence.

Recent advances in grinding and air classification systems have further enhanced GCC’s competitiveness. Surface modification techniques now enable finer particle sizes and improved dispersion, narrowing performance differences with PCC. These improvements allow GCC to deliver superior brightness and opacity while retaining its strong cost advantages. As a result, it remains the material of choice in paper fillers, plastic compounds, and large-scale construction applications where high performance at a lower cost is essential.

Industry Analysis

The paper industry remains the leading consumer of calcium carbonate, accounting for approximately 42% of global demand. Both GCC and PCC are widely used as fillers and coating pigments, helping improve brightness, opacity, and printability while reducing reliance on costly wood pulp. PCC is particularly valuable in premium printing and specialty paper due to its controlled particle size distribution and enhanced ink absorption, making it indispensable for high-quality publishing and packaging applications.

The plastics industry follows as the second-largest consumer, leveraging calcium carbonate to improve stiffness, durability, and impact resistance in polymer-based products. Strategic use of fillers enables 13–17% cost reductions while improving material performance across automotive, packaging, and consumer goods. Additionally, paints and coatings represent a significant segment, using calcium carbonate as an extender pigment to enhance opacity, surface finish, and weather resistance. Its role in eco-friendly formulations supports demand in architectural and industrial coating systems worldwide.

Regional Insights

North America Ground And Precipitated Calcium Carbonate Market Trends

The United States leads North American market development through technological innovation, advanced manufacturing capabilities, and stringent quality requirements that create strong demand for high-purity PCC in pharmaceutical, food-grade, and specialty industrial applications. Regulatory frameworks that emphasize low-VOC materials and environmental compliance standards support the increased adoption of calcium carbonate in architectural coatings and construction materials. The U.S. Calcium Carbonate Market demonstrates robust growth patterns driven by the expansion of residential and commercial construction, particularly in California, Texas, and Florida, where population growth fuels building activity.

Regional paper mills are increasingly integrating calcium carbonate technologies to improve the quality of recycled paper, enhance brightness characteristics, and reduce fiber costs while meeting sustainability targets. The demand for agricultural products remains stable across Midwest farming regions, where calcium carbonate plays a crucial role in adjusting soil pH, enhancing nutrients, and optimizing crop yields, thereby contributing to market stability and providing countercyclical demand patterns that support overall regional market resilience.

Europe Ground And Precipitated Calcium Carbonate Market Trends

European calcium carbonate markets experienced significant price increases in November 2024, driven by strong construction demand, supply chain disruptions, and rising energy costs that affected production. The European Union's updated Construction Products Regulation (CPR) promotes harmonized technical standards across member states, facilitating cross-border trade and enhancing market access for compliant calcium carbonate products. Germany, the United Kingdom, France, and Spain drive regional consumption through robust manufacturing sectors, stringent environmental regulations favoring natural mineral fillers, and increasing demand for sustainable construction materials.

REACH and CLP regulatory frameworks ensure high safety and environmental standards while supporting innovation in specialized pharmaceutical and food-grade applications. European manufacturers are investing substantially in energy-efficient production technologies, renewable energy integration, and initiatives to reduce their carbon footprint, all while maintaining competitiveness and meeting increasingly stringent environmental requirements. This approach supports circular-economy principles through recycling and waste-reduction programs.

Asia Pacific Ground And Precipitated Calcium Carbonate Market Trends

The Asia Pacific region dominates global consumption, accounting for over 37% of the market share, driven by rapid industrialization, massive infrastructure development programs, and cost-competitive manufacturing advantages in China, Japan, and India. China's construction sector generated approximately 4 trillion USD in output during 2022, creating enormous demand for calcium carbonate in cement production, building materials, and architectural coatings. Japan maintains a technological leadership in high-performance applications, with companies like TBM Co., Ltd. developing innovative LIMEX calcium carbonate-based materials that over 8,000 companies use as sustainable alternatives to plastic.

India is the world's largest importer of calcium carbonate, with $ 133 million in limestone imports in 2022, reflecting strong domestic demand growth across the paper, plastics, pharmaceuticals, and construction industries. ASEAN countries are demonstrating rapid market expansion, supported by government infrastructure investments, foreign manufacturing relocations, and growing middle-class consumption patterns that drive demand for packaging, automotive, and consumer goods, requiring calcium carbonate fillers and functional additives.

Competitive Landscape

The global ground and precipitated calcium carbonate market is highly fragmented, with numerous global and regional players competing across varied applications such as paper, plastics, paints, coatings, and construction. Competition is shaped by factors including production scale, raw material access, and supply chain efficiency. Many producers focus on strategic localization to reduce transportation costs and maintain proximity to key end-use industries, while also offering extensive technical support and customized product solutions to strengthen customer relationships.

Innovation remains a key differentiator, particularly in advanced surface treatment processes, nanotechnology, and sustainable product development. Companies are increasingly adopting renewable energy, improving energy efficiency, and implementing circular economy practices to meet environmental targets. Consolidation trends are evident through acquisitions, partnerships, and joint ventures, which enable technology sharing and broader application development, especially in high-performance and eco-friendly material solutions.

Key Market Developments

- In May 2025, Mississippi Lime Company, in collaboration with Singleton Birch and Centrica, reached a significant funding milestone for developing hydrogen-powered low-carbon lime production technologies. This initiative underscores the industry's commitment to sustainable manufacturing practices and aims to reduce carbon emissions in lime production.

- In March 2025, Domtar and Omya inaugurated a new Precipitated Calcium Carbonate (PCC) plant at Domtar’s Nekoosa site in Wisconsin, USA. This facility, which became operational in September 2024, aims to reduce logistical costs and carbon emissions by supplying PCC locally, replacing a previously closed mill located 200 kilometers away.

- In June 2024, Omya announced the completion of the first stage of improvements at its specialty fertilizer granulation plant in Wathena, Kansas. The $6 million investment focuses on enhancing plant assets and infrastructure, aiming to elevate environmental health and safety standards and improve operational efficiency.

Companies Covered in Ground And Precipitated Calcium Carbonate Market

- Omya AG

- Imerys SA

- Minerals Technologies Inc. (MTI)

- Mississippi Lime Company

- Huber Engineered Materials

- Schaefer Kalk GmbH & Co. KG

- Carmeuse

- Nordkalk Corporation,

- Maruo Calcium Co., Ltd.

- Shiraishi Kogyo Kaisha, Ltd.,

- Lhoist Group

- Graymont Limited,

- Cimbar Resources, Inc.,

- GLC Minerals, LLC

- Indo Chemicals Pvt. Ltd.

Frequently Asked Questions

The global ground and precipitated calcium carbonate market is projected to reach US$ 43.1 billion by 2032, growing from US$ 27.9 billion in 2025 at a CAGR of 6.4%.

Key demand drivers include expanding paper and packaging industry applications, growing plastic sector adoption for cost reduction and performance enhancement, and increasing construction activity driving paints and coatings consumption.

Ground Calcium Carbonate (GCC) dominates with approximately 68% market share due to cost-effectiveness, abundant limestone raw material availability, and widespread industrial applications.

Asia Pacific leads global consumption with over 37% market share, driven by rapid industrialization, infrastructure development, and manufacturing advantages in China, Japan, and India.

Pharmaceutical and nutraceutical applications present significant opportunities with growing demand for high-purity PCC in dietary supplements and drug formulations, supported by aging populations and health awareness trends.

Omya AG leads with 23.2% market share, followed by Imerys SA with 4.9% and Minerals Technologies Inc. with 3.0%, competing through innovation and global distribution networks.