- Technology

- Ground Surveillance Radar (GSR) Systems Market

Ground Surveillance Radar (GSR) Systems Market Size, Share, and Growth Forecast 2026 - 2033

Ground Surveillance Radar (GSR) Systems Market by Range Category (Short Range, Mid Range, Long Range), by Application (Border Surveillance, Battlefield Surveillance, Critical Infrastructure Protection, Perimeter Security, Coastal and Maritime Ground Surveillance, Disaster Management and Search Operations, Others), by Platform Type (Man-Portable GSR Systems, Vehicle-Mounted GSR Systems, Fixed Ground GSR, Coastal and Border Surveillance GSR), by End User (Military and Armed Forces, Homeland Security and Border Forces, Law Enforcement Agencies, Intelligence Agencies, Critical Infrastructure Operators, Private Security Agencies), by Regional Analysis, 2026-2033

Ground Surveillance Radar (GSR) Systems Market Size and Trend Analysis

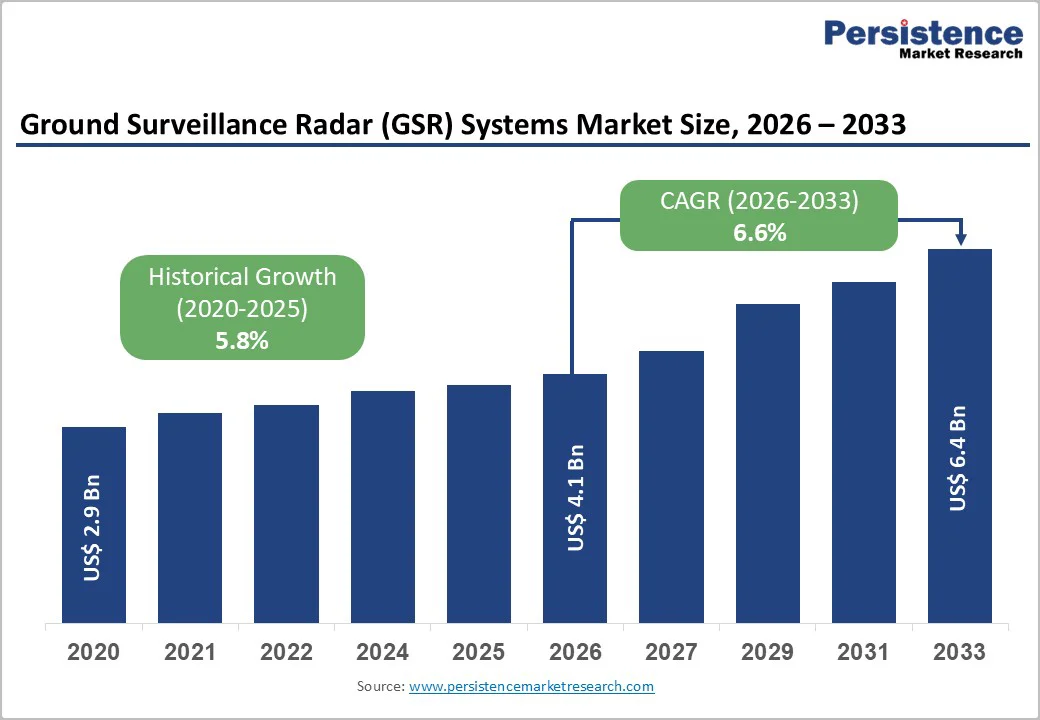

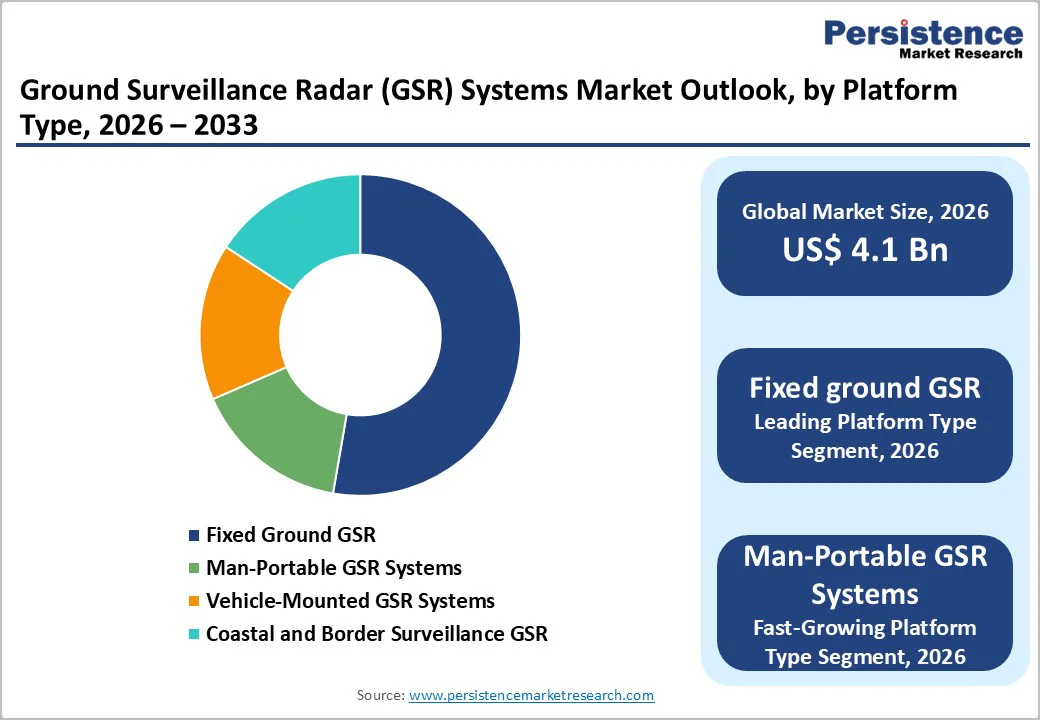

The global Ground Surveillance Radar (GSR) Systems market size is expected to be valued at US$ 4.1 billion in 2026 and projected to reach US$ 6.4 billion by 2033, growing at a CAGR of 6.6% between 2026 and 2033.

The ground surveillance radar (GSR) systems market is expanding due to rising geopolitical tensions and border security needs, with global defense spending surpassing USD 2.4 trillion in 2024, rapid advancement of AESA and GaN-based radar technologies with AI-enabled target classification, integration with unmanned systems and multi-sensor surveillance ecosystems for enhanced situational awareness, and growing mandates for critical infrastructure protection, where short-range GSR systems hold 46.7% market share in 2025.

Key Market Highlights

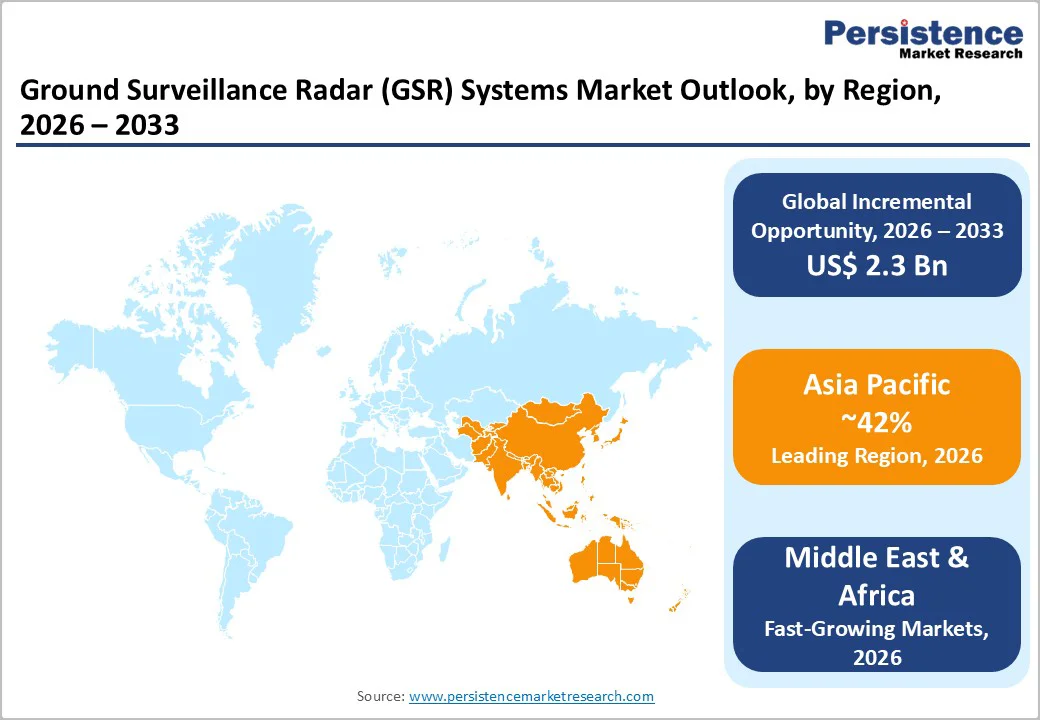

- Leading Region: Asia Pacific leads the GSR systems market with a 42% share in 2025, driven by advanced border surveillance initiatives in India, China, Japan, and Southeast Asia.

- Fastest-Growing Region: Middle East & Africa is expected to grow fastest at an 8.1% CAGR from 2026-2033, supported by GCC defense modernization and Africa’s expanding adoption of surveillance.

- Dominant Segment: Short-range GSR systems hold 46.7% market share in 2025 due to cost-effective, rapid deployment and precise localized detection.

- Fastest Growing Segment: Man-portable GSR systems are projected to grow at 7.9% CAGR from 2026 to 2033, driven by tactical flexibility, emerging market adoption, and disaster management applications.

- Key Market Opportunity: Integrating GSR platforms with autonomous systems, AI-based target recognition, multi-sensor fusion, and command-and-control workflows creates opportunities for next-generation surveillance.

| Global Market Attributes | Key Insights |

|---|---|

| Ground Surveillance Radar (GSR) Systems Market Size (2026E) | US$ 4.1 billion |

| Market Value Forecast (2033F) | US$ 6.4 billion |

| Projected Growth CAGR (2026-2033) | 6.6% |

| Historical Market Growth (2020-2025) | 5.8% |

Market Dynamics

Market Growth Drivers

Escalating Global Border Security Imperatives and Geopolitical Tensions

The unprecedented intensification of border security challenges worldwide is driving the deployment of GSR systems, with countries investing in advanced surveillance capabilities to detect unauthorized movement, prevent smuggling, and counter drone threats across vast geographic areas. Advanced border surveillance radars with AI-enabled target classification can distinguish between personnel, vehicles, and UAVs with detection ranges of 40-200 km, depending on system architecture and environmental conditions.

India’s acquisition of 18 Ashwini Low-Level Transportable Radars (LLTR) through a USD 330 million contract signedin March 2025 with Bharat Electronics Limited (BEL) exemplifies escalating defense modernization investments, with systems offering AESA technology, 200 km detection range, and 360-degree coverage in rapid-deployment configurations optimized for rugged mountainous terrain. The Swedish Defence Materiel Administration’s April 2025 contract with Thales Group for delivery of the Ground Master 200 Multi-Mission Compact Radar (GM200 MM/C) demonstrates sustained European investment in radar modernization, with the system providing comprehensive all-weather surveillance against aerial and maritime threats.

Technological Innovation in AESA Radar Systems and GaN-Based Semiconductor Integration

The revolutionary advancement of Active Electronically Scanned Array (AESA) radar technology utilizing Gallium Nitride (GaN) semiconductor architecture is fundamentally transforming GSR system performance, reliability, and cost economics. GaN-based AESA systems provide superior power efficiency, extended detection ranges, enhanced jamming resistance, and reduced thermal dissipation compared to traditional gallium arsenide (GaAs) implementations.

India’s next-generation Low Level Lightweight Radar (LLLWR) utilizing GaN-based AESA technology delivers advanced 3D processing, digital beam-forming capabilities, 360-degree coverage, and low probability of intercept (LPI) characteristics supporting detection of emerging threats including micro-UAVs and low-radar cross-section targets. The integration of AI-enabled target recognition algorithms, machine learning for clutter suppression, and real-time sensor fusion with electro-optical systems enables autonomous target detection and classification, reducing operator workload and accelerating decision-making cycles.

Sweden’s Saab Group is developing Giraffe 4A radar, incorporating AESA technology, which provides simultaneous identification and tracking of numerous aerial and maritime targets with a software-updatable architecture supporting long-term capability modernization without costly hardware replacement. Cost reduction achieved through advanced manufacturing processes, integration of commercial COTS components, and simplified maintenance requirements enables broader customer accessibility and market expansion across defense-constrained emerging market militaries.

Market Restraints

High Capital Investment Requirements and Budget Constraints in Emerging Market Nations

The deployment of advanced GSR systems requires substantial capital investment ranging from USD 5-15 million per system for comprehensive border surveillance implementations, creating significant barriers for defense-constrained nations and smaller economies. Complete border surveillance solutions incorporating multiple GSR platforms, control centers, communication networks, and integration infrastructure demand multi-year procurement programs, sophisticated technical expertise, and sustained operational funding for maintenance, training, and system upgrades.

Public sector procurement constraints in emerging markets, particularly across Latin America, Africa, and South Asia, limit acquisition velocity and force the prioritization of legacy systems despite superior performance offered by modern radar platforms. The complexity of technology transfer agreements, export control restrictions, and licensing requirements for AESA and GaN-based systems further elevates acquisition costs and extends deployment timelines. Economic pressures forcing budget reductions in defense spending disproportionately affect procurement of surveillance systems relative to platforms with immediate operational visibility.

Technical Complexity and Integration Challenges with Legacy Infrastructure

GSR systems integration with existing command and control infrastructure, communication networks, and legacy sensor platforms presents substantial technical challenges requiring specialized expertise, extensive software development, and system interoperability validation. Modern AI-enabled radar systems demand sophisticated data processing capabilities, cloud-based analytics infrastructure, and cybersecurity protocols to protect sensitive surveillance information from adversarial cyber threats.

The requirement for continuous calibration, periodic maintenance, and specialized technical training creates ongoing operational burdens and expense. Organizational resistance to technology adoption, inadequate personnel training, and institutional factors often limit effective utilization of advanced GSR capabilities, reducing return on investment and delaying capability realization.

Market Opportunities

Integration of GSR Systems with Autonomous Unmanned Systems and Multi-Sensor Fusion Architectures

The convergence of ground-based GSR platforms with unmanned aerial vehicles (UAVs), autonomous ground vehicles, and integrated sensor networks creates exceptional opportunities for the development of a comprehensive surveillance ecosystem. Manufacturers combining fixed GSR systems with drone detection and counter-drone capabilities are establishing comprehensive perimeter defense architectures to address the emerging counter-drone market, projected to grow at an 8.7% CAGR. Meteksan Defence’s KAPAN Counter Drone System, integrating advanced drone detection radar, electro-optic, and jammer subsystems, exemplifies integrated solutions addressing multiple threat vectors simultaneously.

Integration of GSR with artificial intelligence-enabled target recognition, real-time sensor fusion, and automated command and control workflows enables autonomous border surveillance operations reducing personnel requirements while improving detection accuracy and response times. Commercial opportunities exist in civilian applications including critical infrastructure protection, disaster management, and search-and-rescue operations, with GSR systems providing real-time awareness of large geographical areas supporting emergency response coordination and resource allocation optimization.

Expansion of Portable and Man-Portable GSR Systems for Rapid Deployment and Cost-Effective Solutions

The development of lightweight, man-portable GSR systems, including Thales Ground Observer 12 (GO 12) with 17 kg sensor weight, 70W power consumption, and 27 km detection range and Leonardo MSTAR V6 providing 27 km range detection with 1,800+ units deployed globally represents significant market opportunity for emerging market penetration and cost-sensitive applications. Man-portable radar systems demonstrates strong demand for portable surveillance solutions suitable for border posts, remote checkpoints, disaster management, and counter-terrorism operations. Advances in miniaturization, battery technology, and solid-state electronics enable rapid 5-minute deployment from man-pack configurations, supporting military mobility and operational flexibility. Commercial demand for portable surveillance systems in private security, facility protection, and event security creates additional market segments beyond traditional defense applications. Emerging manufacturers in India, Europe, and Israel are developing cost-competitive portable GSR solutions accessible to police forces, border security agencies, and smaller military establishments previously unable to acquire expensive fixed infrastructure.

Category-wise Insights

Range Category Analysis

Short-range GSR systems lead the range category with 46.7% market share in 2025, driven by deployment at border posts, checkpoints, and critical infrastructure sites where rapid threat detection and localized surveillance are essential. These systems offer detection ranges of 10–25 km and feature AI-enabled target discrimination to reduce false alarms and improve operational efficiency. Integration with automated response systems, surveillance cameras, and access control mechanisms provides comprehensive perimeter security for airports, power plants, and military installations. Compact form factors and lower costs make them accessible to police forces, private security agencies, and smaller military establishments. The short-range segment is projected to grow at a 6.2% CAGR from 2026 to 2033, fueled by counter-drone detection, perimeter upgrades, and infrastructure protection initiatives.

Application Analysis

Border surveillance dominates the application category with 41.9% market share in 2025, driven by increasing demand for monitoring unauthorized crossings, vehicle interdiction, and counter-smuggling operations across land borders and maritime boundaries. Advanced systems operate 24/7 under all weather conditions, offering automatic target detection, classification, and integration with patrol force coordination for rapid response. They are increasingly integrated with AI-enabled sensor fusion and automated decision-support platforms, enhancing situational awareness and operational efficiency. Border surveillance is forecast to grow at a 6.4% CAGR from 2026 to 2033, supported by rising geopolitical tensions, defense modernization programs, and expanding investments in border infrastructure and technology upgrades across Asia Pacific, the Middle East, and Africa.

Platform Type Analysis

Fixed ground GSR systems dominate the platform category with 52% market share in 2025, providing permanent or semi-permanent installations at border posts, military bases, and critical infrastructure sites. These systems ensure continuous 24/7 surveillance, optimized power reliability, and seamless integration with command centers for effective monitoring. Fixed systems support AI-enabled detection, automated threat alerts, and interoperability with auxiliary sensors, enabling real-time decision-making in critical security environments. The segment is projected to grow steadily from 2026 to 2033 as governments prioritize long-term infrastructure protection, strategic surveillance, and sustained perimeter monitoring, while operational reliability and integration with centralized control systems drive adoption among military and homeland security agencies globally.

End User Analysis

Military and armed forces dominate the end-user segment with 54% market share in 2025, driven by army surveillance, air defense integration, and battlefield intelligence requirements. GSR systems support reconnaissance, early-warning capabilities, and force protection operations across land borders, critical infrastructure, and strategic installations. The segment benefits from high government defense expenditure, investment in advanced radar technologies, and growing adoption of AI-enabled sensor fusion platforms. Military applications are projected to grow at 6.3% CAGR from 2026 to 2033, while operational flexibility, modernization programs, and integration with unmanned systems further support expansion, establishing armed forces as the largest and most strategic consumer of GSR solutions worldwide.

Regional Insights

North America Ground Surveillance Radar (GSR) Systems Market Trends and Insights

North America commands approximately 31% of the global GSR Systems market share in 2025, with the United States representing the dominant contributor driven by extensive border security requirements, substantial defense budgets, and advanced technology innovation ecosystem. The U.S. Department of Defense continues investing in next-generation radar systems including Raytheon’s PhantomStrike radar completing first flight testing in May 2025 and Lockheed Martin’s delivery of TPY-4 ground-based long-range air surveillance radar supporting the Three-Dimensional Expeditionary Long-Range Radar (3DELRR) program.

U.S.-Mexico border surveillance represents a primary GSR application, with systems deployed across thousands of miles of land border requiring persistent surveillance, unauthorized crossing detection, and drug trafficking interdiction. Canadian and U.S. government investments in northern border surveillance address geopolitical concerns and sovereign domain protection. Advanced counter-drone capabilities and autonomous threat detection systems are increasingly integrated into North American GSR platforms addressing emerging airspace security challenges. The North American market is projected to grow at 5.9% CAGR from 2026-2033, with growth concentrated in critical infrastructure protection modernization, counter-drone system deployment, and integration of AI-enabled autonomous surveillance capabilities.

Europe Ground Surveillance Radar (GSR) Systems Market Trends and Insights

Europe GSR market is characterized by robust defense modernization initiatives, NATO standardization requirements, and strategic border protection imperatives. Germany, France, United Kingdom, and Spain maintain the largest European GSR deployments, with NATO alliance members coordinating surveillance capabilities and establishing interoperable command and control systems.

Sweden’s continued radar modernization exemplified by Saab’s Giraffe 4A AESA radar contracts and Thales Ground Master 200 MM/C procurement demonstrates sustained European investment in advanced surveillance technologies. European emphasis on integration with broader defense systems, cybersecurity compliance, and technology transfer opportunities characterize regional market dynamics. Border security within Schengen area and maritime surveillance across European waters represent important GSR applications. The European market is projected to grow at 6.1% CAGR from 2026-2033, with growth driven by NATO capability upgrades, Russian security concerns, and integration of multiple surveillance modalities into consolidated command systems.

Asia Pacific Ground Surveillance Radar (GSR) Systems Market Trends and Insights

Asia Pacific dominates the global GSR Systems market with approximately 42% market share in 2025, propelled by rapid defense modernization investments, geopolitical tensions, and border security imperatives across China, India, Japan, and regional nations. India’s aggressive radar modernization program including the USD 330 million Ashwini LLTR acquisition and development of indigenous AESA systems represents the fastest-growing regional market at 7.4% CAGR from 2026-2033.

China’s extensive border surveillance systems and development of advanced radar technologies are driving competitive dynamics and accelerating innovation across Asia Pacific. Japan’s technological leadership in compact, high-performance radar systems and integration with autonomous systems establishes market innovation standards. Southeast Asian nations including Vietnam, Thailand, and Indonesia are increasing GSR investments for border security and maritime surveillance. The region’s manufacturing advantages, growing defense budgets, and emerging threats are creating sustained demand for sophisticated surveillance capabilities. Asia Pacific is forecast to grow at 7.2% CAGR from 2026-2033, making it the fastest-growing global region.

Competitive Landscape

Market Structure Analysis

The global Ground Surveillance Radar (GSR) systems market exhibits moderate consolidation, with top defense contractors collectively commanding approximately 45–50% of total market revenue. Market fragmentation remains in specialized segments, including man-portable systems, coastal surveillance radars, and solutions tailored for emerging markets, where regional manufacturers and niche players maintain competitiveness through localized production, cost efficiency, and application-specific expertise.

Key strategies driving market competition include vertical integration across radar technology development and manufacturing to secure proprietary capabilities and margin growth, geographic expansion into high-growth regions through joint ventures and localized facilities, and technology differentiation via AESA and GaN-based radar systems, AI-enabled target recognition, and autonomous surveillance functionalities. Strategic mergers and acquisitions enable consolidation and access to specialized radar technologies, while partnerships with military integrators, command-and-control providers, and sensor fusion platforms enhance solution offerings. Emerging models, such as radar-as-a-service, leverage cloud analytics, predictive maintenance, and continuous capability upgrades to create recurring revenue streams and long-term client engagement.

Key Market Developments

- May 2025: Raytheon Technologies (a subsidiary of RTX Corporation) successfully executed the first flight test of its advanced PhantomStrike radar mounted on a Multi-Program Testbed aircraft in Ontario, California, achieving critical validation milestone for next-generation airborne and ground-based surveillance capabilities supporting advanced threat detection and tracking in complex operational environments.

- March 2025: India’s Ministry of Defense finalized a USD 330 million contract with Bharat Electronics Limited (BEL) to acquire 18 Ashwini Low-Level Transportable Radars (LLTR) equipped with cutting-edge AESA technology, delivering 200 km detection range, 360-degree horizontal coverage, and enhanced early warning capabilities for the Indian Air Force addressing escalating aerial defense requirements along regional borders.

- April 2025: The Swedish Defence Materiel Administration (FMV) signed a contract with Thales Group for delivery of Thales Ground Master 200 Multi-Mission Compact (GM200 MM/C) radar systems, replacing the aging PS-871 system and providing comprehensive sensor capability for modern battlefield awareness with integrated air defense and surveillance functions.

Companies Covered in Ground Surveillance Radar (GSR) Systems Market

- Thales SA

- Lockheed Martin Corporation

- Saab AB

- Elbit Systems Ltd.

- Raytheon Company

- FLIR Systems Inc.

- Israel Aerospace Industries Ltd.

- Blighter Surveillance Systems

- Kongsberg Gruppen

Frequently Asked Questions

The global GSR systems market is expected to reach US$ 4.1 billion in 2026, growing to US$ 6.4 billion by 2033 at a 6.6% CAGR.

Key drivers include geopolitical tensions, border security needs, AESA and GaN radar advancements, AI-enabled surveillance integration, and counter-drone requirements.

Asia Pacific leads with 42% market share, driven by defense modernization in India, China’s border surveillance, Japan’s technology, and Southeast Asian adoption.

Opportunities lie in integrating GSR platforms with autonomous systems, multi-sensor fusion, AI target recognition, and command-and-control workflows.

The market is dominated by global defense leaders including Thales Group, Lockheed Martin Corporation, Raytheon Technologies (RTX), Saab AB, Elbit Systems, and Israel Aerospace Industries.