- Electrical Equipment & Services

- Optical Ground Wire Market

Optical Ground Wire Market Size, Share, and Growth Forecast, 2026 - 2033

Optical Ground Wire Market by Design Type (Layer Stranding Structure, Central Tube Structure), Network Application (Transmission, Distribution), and Regional Analysis 2026 - 2033

Optical Ground Wire Market Size and Trends Analysis

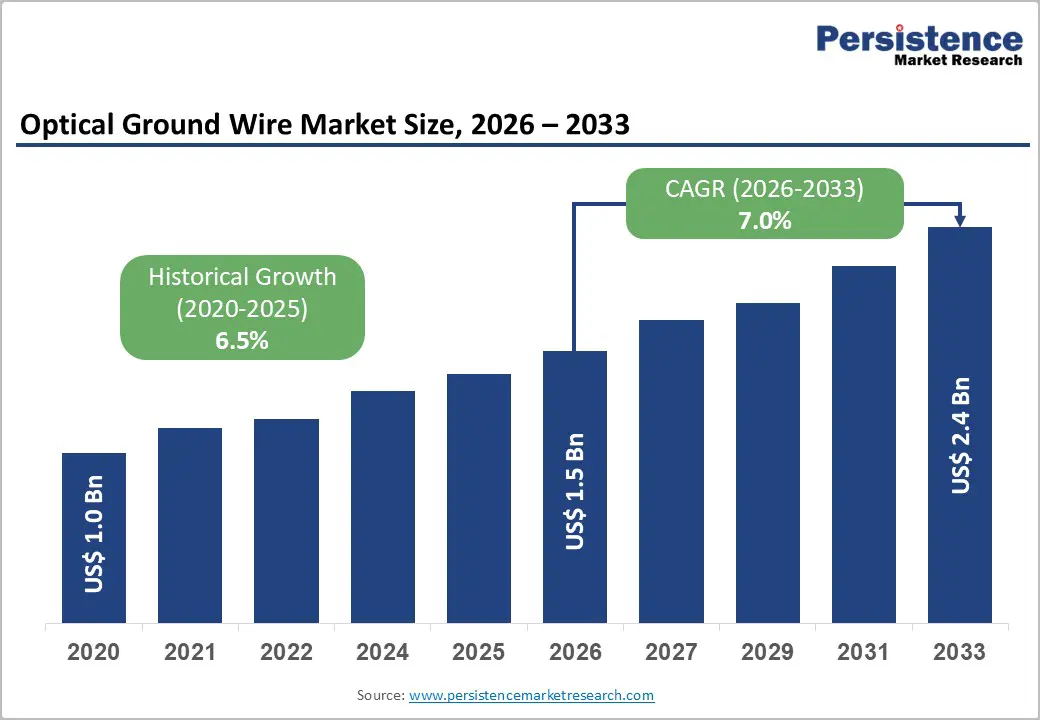

The global optical ground wire market size is likely to be valued at US$1.5 billion in 2026 and is expected to reach US$2.4 billion by 2033, growing at a CAGR of 7% during the forecast period from 2026 to 2033, driven by ongoing grid modernization efforts, with utilities increasingly integrating fiber optics into power transmission lines to enable real-time monitoring and improved communication across geographically dispersed assets.

Advancements in composite materials are enhancing the durability and performance of optical ground wires, particularly in harsh environmental conditions, thereby supporting broader adoption across transmission networks. This steady progress is further reinforced by rising energy demand and the expansion of digital infrastructure. Additionally, the development of high-voltage transmission networks in emerging economies continues to create a strong foundation for sustained market growth.

Key Industry Highlights:

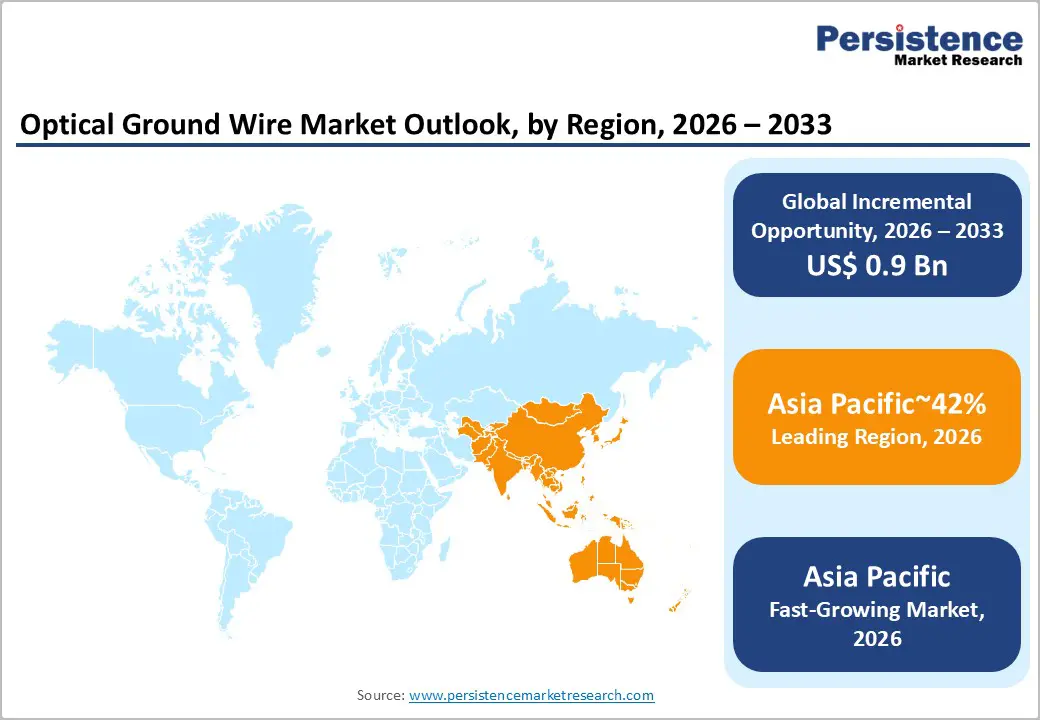

- Leading Region: Asia Pacific is projected to lead, accounting for approximately 42% share in 2026, supported by expansive grid expansions, high-voltage transmission investments, and dense population-driven electrification.

- Fastest-growing Region: Asia Pacific is anticipated to grow fastest, driven by accelerated renewable integration, urban power upgrades, and policy-backed smart grid rollouts.

- Leading Design Type: Layer stranding structure is expected to lead, accounting for approximately 64% share in 2026, anchored by proven tensile strength, widespread deployment in long-haul lines, and compatibility with existing infrastructure.

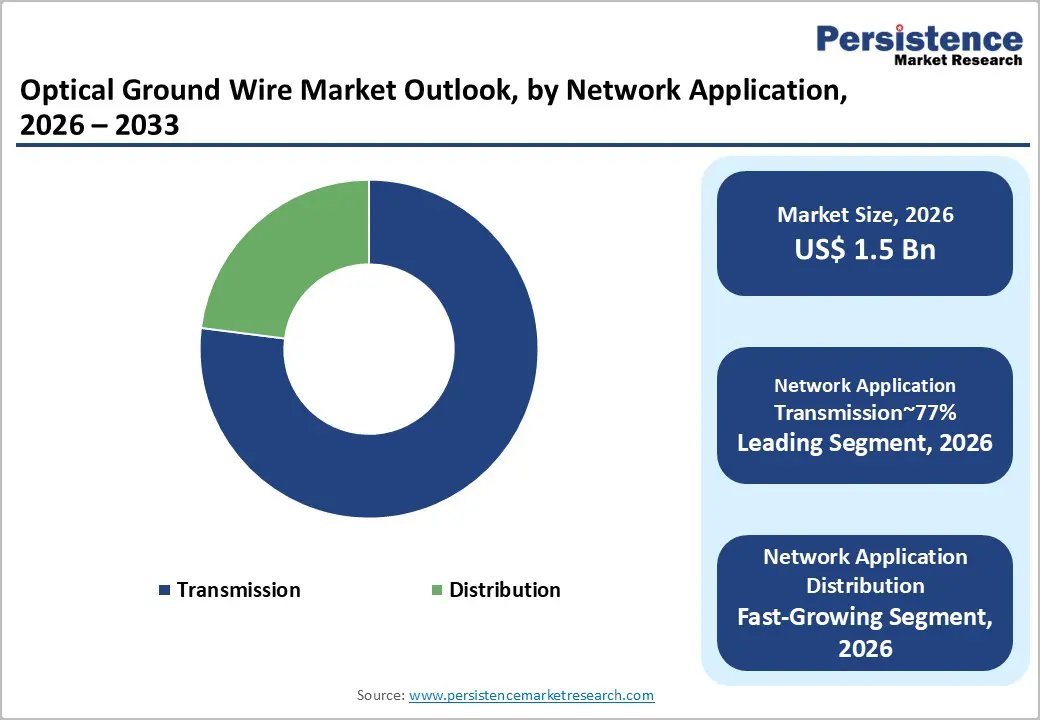

- Leading Network Application: Transmission is anticipated to dominate, accounting for approximately 77% share in 2026, anchored by its backbone role in high-capacity power delivery, remote sensing needs, and regulatory mandates for reliability.

| Key Insights | Details |

|---|---|

|

Optical Ground Wire Market Size (2026E) |

US$1.5 Bn |

|

Market Value Forecast (2033F) |

US$2.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.5% |

Market Factors - Driver, Restraint, and Opportunity Analysis

Driver Analysis - Grid Modernization Pressures Intensifying Integrated Fiber Deployment

Utilities are compelled to modernize aging transmission infrastructure to ensure consistent and reliable power delivery. This transition drives the procurement of optical ground wire systems embedding communication and sensing capabilities. Integrated fiber architectures enable real-time monitoring, strengthening grid visibility across geographically dispersed transmission corridors. Enhanced situational awareness reduces outage frequency while enabling predictive maintenance across critical network assets. Regulatory frameworks increasingly mandate resilience standards, accelerating the adoption of communication-enabled transmission infrastructure upgrades. Cost structures favor integrated solutions by consolidating grounding, shielding, and data transmission within unified cable systems.

Industry players such as Prysmian Group with OPGW Access enhance network visibility across remote and topographically complex deployment regions. These solutions align with operator requirements for secure, scalable, and interference-resistant communication backbones. Technology integration reduces incremental deployment costs compared to standalone communication infrastructure alternatives. Procurement strategies increasingly prioritize multi-functional cable systems supporting both electrical and digital transmission requirements. This convergence structurally reinforces demand for OPGW across modernization-driven grid expansion initiatives.

Renewable Energy Integration Driving Demand for Fiber-Enabled Grounding Infrastructure

Decarbonization mandates are accelerating the integration of intermittent renewable generation into existing transmission networks. This transition necessitates advanced conductors supporting simultaneous grounding and high-capacity telemetry for grid stability. Variable generation profiles from wind and solar intensify requirements for real-time data transmission. Integrated optical ground wires enable dynamic load balancing through continuous monitoring and communication capabilities. Regulatory frameworks emphasize grid flexibility, compelling utilities to deploy multi-functional transmission infrastructure systems. Cost efficiencies emerge as fiber-integrated cables replace discrete shielding and communication network installations.

Expansion of offshore wind installations requires specialized cabling solutions linking remote generation assets with mainland grids. Harsh maritime environments demand materials offering high corrosion resistance and superior mechanical durability under stress. Prysmian Group, with Sirocco Extreme, delivers high-density fiber configurations within structurally reinforced protective cable architectures. These capabilities align with operator requirements for resilient, high-performance transmission connectivity across offshore deployments. Integrated solutions reduce lifecycle maintenance costs while ensuring consistent data integrity under adverse environmental conditions. This alignment between renewable infrastructure expansion and cable innovation sustains procurement momentum across energy networks.

Restraint Analysis - High Installation Complexity Constraining Retrofit Deployment Efficiency

Overhead transmission retrofits require specialized equipment and skilled labor to prevent service disruptions. Fiber integration into energized lines introduces coordination complexity across maintenance teams and network operators. Structural modifications extend project timelines, particularly within densely interconnected and urban transmission corridors. Utilities must manage outage scheduling constraints while maintaining grid stability during phased installation procedures. Regulatory compliance requirements further complicate deployment through stringent safety and operational validation protocols. Elevated installation complexity increases execution risk, directly influencing contractor availability and project sequencing decisions.

Cost structures intensify as downtime penalties accumulate alongside extended labor and equipment utilization requirements. ZTT’s OPGW-24B4 encounters adoption constraints where retrofit projects demand minimal conductor handling. Prysmian Group with OPGW Access reflects engineering trade-offs under high-wind operational conditions. These technical constraints reduce flexibility during installation across environmentally sensitive or unstable transmission environments. Budget-limited utilities delay procurement decisions due to heightened upfront deployment and risk mitigation costs. Prolonged qualification cycles further slow vendor approvals as operators prioritize reliability within risk-averse procurement frameworks.

Raw Material Price Volatility Disrupting Cost Stability and Procurement Planning

Manufacturing of high-performance grounding cables depends on aluminum, stainless steel, and optical-grade glass inputs. Volatility in global commodity markets introduces unpredictable cost structures across cable production and pricing cycles. Supply chain disruptions arising from geopolitical tensions constrain the availability of critical raw materials. These constraints extend lead times and complicate synchronized delivery schedules for large-scale transmission projects. Regulatory trade barriers further amplify sourcing risks by limiting supplier diversification across international markets. This uncertainty undermines long-term infrastructure planning, requiring stable material cost forecasting and procurement visibility.

Suppliers deploy hedging strategies to offset commodity fluctuations, yet cost burdens shift toward utility buyers. Sudden price escalations force contract renegotiations, delaying procurement cycles and altering planned network expansion scopes. LS Cable & System with OPGW Fiber maintains performance reliability despite exposure to volatile input pricing conditions. However, pricing structures remain closely linked to upstream material cost movements and supply availability constraints. Budget-sensitive utilities adjust capital allocation strategies under persistent cost uncertainty and procurement risk pressures. This dependence on external commodity cycles acts as a structural barrier to stable market expansion trajectories.

Opportunity Analysis - Fiber Density Enhancements Enabling Telecom–Power Convergence Infrastructure

Advancements in high-fiber-count optical ground wires address bandwidth constraints within evolving telecom-power integrated networks. Utilities increasingly require infrastructure supporting simultaneous power transmission and high-capacity data backhaul capabilities. Deployment of dense fiber architectures enables integration of emerging communication standards within existing transmission corridors. This convergence supports real-time data exchange essential for grid automation and distributed energy coordination. Regulatory support for digital infrastructure expansion reinforces the adoption of multi-functional transmission assets across utilities. Cost efficiencies arise through shared infrastructure models, reducing duplication between telecom and power network investments.

ZTT with OPGW-48B12 advances dense fiber configurations tailored for urban transmission overlays and data-intensive corridors. Prysmian Group with OPGW Enhanced Capacity targets integrated utility and telecom deployment requirements. These platforms enable scalable bandwidth provisioning aligned with increasing data consumption across smart grid ecosystems. Cross-sector collaboration between utilities and telecom operators expands revenue potential through shared network utilization models. Technology integration enhances asset monetization by supporting multiple communication protocols within a single transmission infrastructure. This alignment strengthens the role of OPGW within converged digital and energy network architectures.

5G Infrastructure Rollout Strengthening Fiber Utilization across Power Corridors

Global deployment of fifth-generation networks requires dense fiber infrastructure supporting low-latency and high-capacity data transmission. Power transmission corridors provide pre-established pathways, reducing regulatory barriers associated with urban trenching activities. This alignment enables utilities to integrate telecom backhaul capabilities within existing electrical infrastructure networks. Shared infrastructure models improve capital efficiency while supporting simultaneous expansion of energy and communication systems. Regulatory encouragement for digital connectivity further supports utility participation within broader telecommunications value chains. Cost advantages emerge through the avoidance of civil construction, accelerating deployment timelines across constrained urban environments.

Expansion of network towers into suburban and rural regions increases demand for reliable high-capacity fiber connectivity. Integrated grounding cables deliver communication capability while preserving electrical safety and shielding requirements. Sterlite Technologies with Celesta OPGW offers high-fiber-count configurations optimized for dense data transmission environments. These solutions support scalable bandwidth requirements across distributed telecom infrastructure deployments. Cross-sector collaboration enhances the utilization of transmission assets by enabling dual-purpose energy and data transport. This convergence expands the operational scope of utilities within integrated digital and power network ecosystems.

Category–wise Analysis

Design Type Insights

Layer stranding structure is expected to lead, accounting for approximately 64% share in 2026, supported by superior mechanical protection and high tensile strength across demanding transmission environments. Multi-layered stranding enhances load distribution, ensuring fiber integrity under thermal expansion and mechanical stress conditions. Utilities prioritize this configuration for high-voltage corridors requiring durability and long-term operational reliability. Protective outer layers shield optical fibers from installation stress and environmental exposure across extended service lifecycles. Continuous refinements in alloy composition improve conductivity, weight balance, and structural resilience within complex cable systems.

The central tube structure is expected to be the fastest-growing segment in the optical ground wire market, driven by demand for lightweight configurations supporting efficient deployment across lower voltage distribution networks. Centralized tube architectures simplify cable geometry, reducing manufacturing complexity and installation handling requirements. Sumitomo Electric Industries with S-OPGW and Furukawa Electric with PowerFlow OPGW enable streamlined deployment across space-constrained and weight-sensitive infrastructure environments. Gel-filled tubes provide effective moisture resistance and vibration damping for sensitive optical fibers. This efficiency supports increasing adoption across utilities, expanding monitoring capabilities within decentralized grid architectures.

Network Application Insights

Transmission is projected to lead, accounting for approximately 77% of the share in 2026, supported by its central role in long-distance power transfer and grid communication stability. High-voltage networks require embedded fiber systems for real-time telemetry, protective relaying, and fault diagnostics across remote substations. Integrated grounding cables reduce dependence on standalone communication infrastructure while maintaining signal integrity within high-interference environments. ZTT with OPGW-24B4, Prysmian Group with OPGW Access, and Nexans with OPGW Blueform ensure operational reliability across backbone transmission corridors. Continuous improvements in attenuation resistance enhance performance under varying environmental and load conditions. This alignment of scale, resilience, and infrastructure integration sustains leadership across national energy networks.

Distribution is expected to be the fastest-growing segment, driven by increasing deployment of smart grid technologies within localized energy networks. Decentralized systems integrating distributed generation require enhanced monitoring and rapid response capabilities at feeder levels. Fiber-enabled grounding cables support load balancing, outage prediction, and automated restoration processes within complex urban environments. Sterlite Technologies with Celesta OPGW and LS Cable & System with OPGW Fiber enable efficient deployment across lower voltage distribution infrastructures. Advanced data analytics integration improves operational responsiveness across dynamic demand and supply conditions. This convergence of decentralization, digitalization, and infrastructure efficiency accelerates adoption within modern distribution networks.

Regional Insights

Asia Pacific Optical Ground Wire Market Trends

Asia Pacific is anticipated to lead, accounting for approximately 42% share in 2026, supported by rapid industrialization and the continuous expansion of high-voltage transmission networks. Large-scale infrastructure projects in emerging economies are driving the procurement of advanced grounding solutions to ensure grid reliability and support digital connectivity. High population density and increasing urbanization necessitate the construction of robust power corridors capable of handling massive energy loads and high-speed data traffic. Regional vendors benefit from strong government support for domestic manufacturing and grid modernization initiatives that prioritize local supply chains. The presence of established textile and electronics manufacturing hubs further reinforces the demand for stable power and high-bandwidth communication. This concentration of demand and manufacturing capability positions the region as the central anchor of the global market.

Asia Pacific is also expected to be the fastest-growing region, as government-led infrastructure buildouts and manufacturing scaling accelerate the adoption of integrated cabling technologies. Aggressive renewable energy targets are compelling nations to invest in long-distance transmission lines that connect remote generation sites with urban load centers. India is expected to anchor regional momentum through sustained investments in automated grid technologies. Government-led programs promoting domestic manufacturing and digital connectivity are anticipated to accelerate the adoption of high-fiber-count grounding wires across rural and urban hubs. Sterlite Technologies (STL) with Celesta OPGW is expected to benefit from localization strategies that enhance the affordability of advanced infrastructure within cost-sensitive environments. The shift toward digitalized utility operations is creating a surge in demand for high-fiber-count architectures that support smart grid functionalities. As energy demand continues to rise, the procurement of multi-functional cable systems is expected to maintain a strong upward trajectory.

North America Optical Ground Wire Market Trends

North America is expected to remain a mature and structurally stable regional market, with demand primarily anchored in replacement cycles and grid hardening. The market's stability is supported by extensive investments in upgrading aging power infrastructure to withstand extreme weather events and enhance overall network security. Utilities in this region prioritize high-performance materials and advanced monitoring capabilities to comply with stringent reliability standards set by regulatory bodies. Furthermore, the rapid expansion of 5G networks is driving the utilization of existing transmission rights-of-way for fiber-optic backhaul. This focus on reliability and digital integration ensures a consistent demand for premium integrated grounding solutions across the utility sector.

The U.S. is expected to drive regional procurement as utilities accelerate the modernization of transmission networks under federal infrastructure funding programs. Sweeping investments in renewable energy integration and rural broadband expansion are anticipated to increase the demand for high-capacity grounding lines. Regulatory pressures to improve grid resilience against cyber threats and physical damage are projected to favor vendors offering advanced integrated sensing capabilities. Ongoing efforts to simplify the permitting process for new transmission projects are likely to unlock additional opportunities for large-scale cable deployments.

Europe Optical Ground Wire Market Trends

Europe demonstrates steady expansion, supported by energy transition policies integrating fiber-enabled grounding within cross-border transmission infrastructure systems. Decarbonization initiatives increase reliance on offshore wind assets, requiring precise monitoring and resilient communication backbones. Harmonized regional standards streamline deployment protocols, reducing integration complexity across interconnected national grid systems. Nexans with OPGW Blueform secures deployments across Baltic transmission corridors supporting renewable integration strategies. Innovation in low-sag conductor designs enhances suitability for dense transmission routes with constrained spatial configurations.

Germany leads regional momentum through Energiewende initiatives, restructuring grid architecture toward renewable-dominant energy systems. Expansion of north-to-south transmission corridors drives demand for fiber-integrated grounding solutions, enabling real-time system control. Prysmian Group, with Sirocco Extreme, supports high-capacity deployments aligned with national infrastructure modernization objectives. Regulatory emphasis on grid stability and accelerated phase-out of conventional generation intensifies procurement of data-enabled transmission assets. Strong focus on digitalization enhances the adoption of advanced monitoring systems embedded within transmission networks. This alignment between policy, infrastructure expansion, and technology integration sustains regional market progression.

Competitive Landscape

The global optical ground wire market is moderately fragmented, with leadership concentrated among global suppliers such as ZTT, Prysmian Group, Nexans, and LS Cable & System. This structure reflects localized manufacturing requirements and heterogeneous voltage standards across regional transmission networks. Leading players shape procurement through benchmarks in tensile strength and optical attenuation performance. Their technological footprints influence utility specifications, embedding long-term alignment with grid modernization programs. Sustained engagement through lifecycle services strengthens vendor positioning within critical infrastructure procurement ecosystems.

Competitive positioning emphasizes vertical differentiation through tailored tensile engineering and fiber integration capabilities across varied deployment environments. Premium vendors prioritize advanced material science, while value-oriented players optimize manufacturing efficiency and cost structures. Platform evolution increasingly incorporates hybrid configurations supporting dual-use energy and communication transmission requirements. Strategic partnerships with telecom operators extend infrastructure monetization, reinforcing convergence across power and digital network ecosystems.

Key Industry Developments:

- In March 2026, Finolex Cables set a INR 1,000 Crore revenue target for its Tamil Nadu operations for the upcoming fiscal year. This aggressive regional target signifies the company's intent to capitalize on the state's booming data center hub, EV manufacturing ecosystem, and massive infrastructure expansion to outpace competitors in the South Asian corridor.

- In February 2026, Sharika Enterprises secured an additional order for 48F OPGW cables from LS Cable India. Continuous repeat orders indicate a consolidation of supply chain partnerships between specialized EPC firms and global cable giants to meet immediate grid demands.

Companies Covered in Optical Ground Wire Market

- Prysmian Group

- Nexans

- ZTT

- Fujikura Ltd.

- Sumitomo Electric Industries

- LS Cable & System

- Furukawa Electric

- Sterlite Technologies

- Hengtong Group

- Tongding Interconnection

- Tratos

- Guangdong Zhonglian Cable Group

- Shenzhen SDG Information

- Taihan Cable & Solution

- AFL Global

- Elsewedy Electric

Frequently Asked Questions

The global optical ground wire market is expected to be valued at approximately US$1.5 billion in 2026 and is projected to grow to around US$2.4 billion by 2033. This expansion represents a compound annual growth rate (CAGR) of about 7% over the forecast period.

The primary driver of growth in the optical ground wire market is grid modernization, which is increasing the need for integrated monitoring and communication systems. The expansion of renewable energy sources further drives demand for real-time data transmission, while supportive smart grid policies are accelerating the adoption of fiber-optic solutions.

The optical ground wire market is projected to grow at a CAGR of 7% from 2026 to 2033. This outlook builds on a historical growth rate of around 6.5%, with continued expansion driven by utility-led infrastructure upgrades and modernization initiatives.

Asia Pacific leads with approximately 42% share in 2026. Expansive transmission projects underpin this position. Policy support sustains dominance.

Key players in the optical ground wire market include ZTT (with OPGW-24B4), Prysmian Group (with OPGW Access), Nexans (with OPGW Blueform), and LS Cable & System (with OPGW-LST). These companies primarily focus on transmission-grade solutions and high-resilience cable designs. Regional specialists such as Furukawa Electric complement the presence of global leaders by catering to localized requirements and niche applications.