- Pharmaceuticals

- Scar Treatment Market

Scar Treatment Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Scar Treatment Market by Product (Topical products, Laser products, Surface treatment products, Injectable products), Technology (Atrophic scars, Hypertrophic Scars and Keloids, Contractures, Stretch Marks), End User (Hospitals, Clinics, Pharmacies & Drug stores, E-commerce), and Regional Analysis from 2026 to 2033

Scar Treatment Market Share Trends Analysis

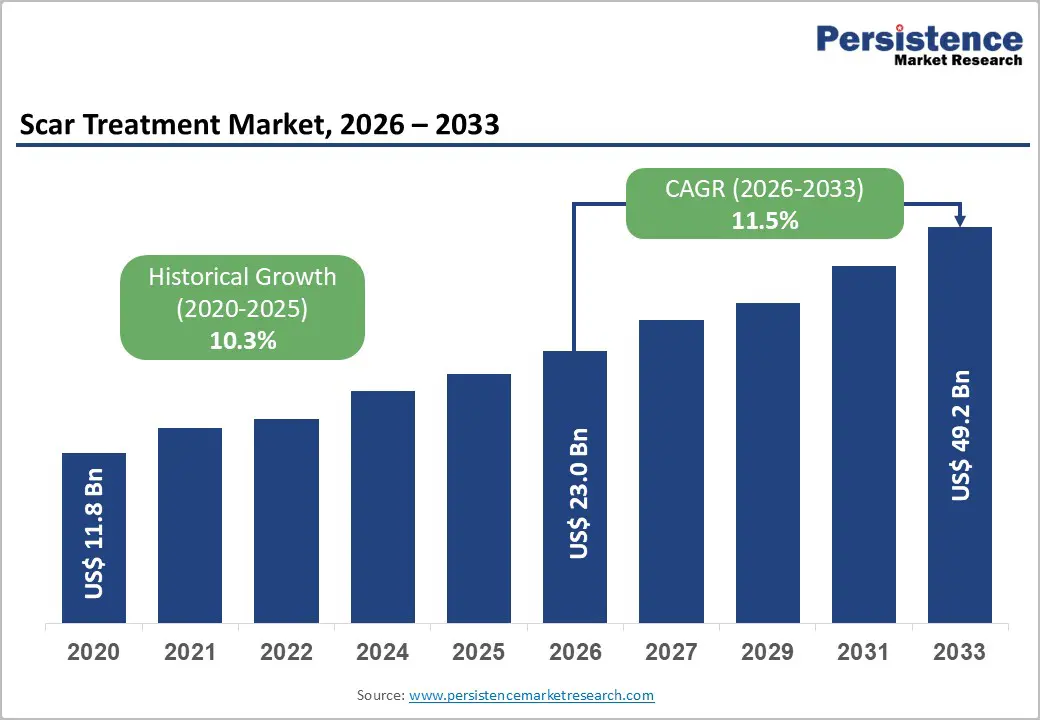

The global scar treatment market is estimated to grow from US$ 23.0 Bn in 2026 to US$ 49.2 Bn by 2033. The market is projected to grow at a CAGR of 11.5% from 2026 to 2033.

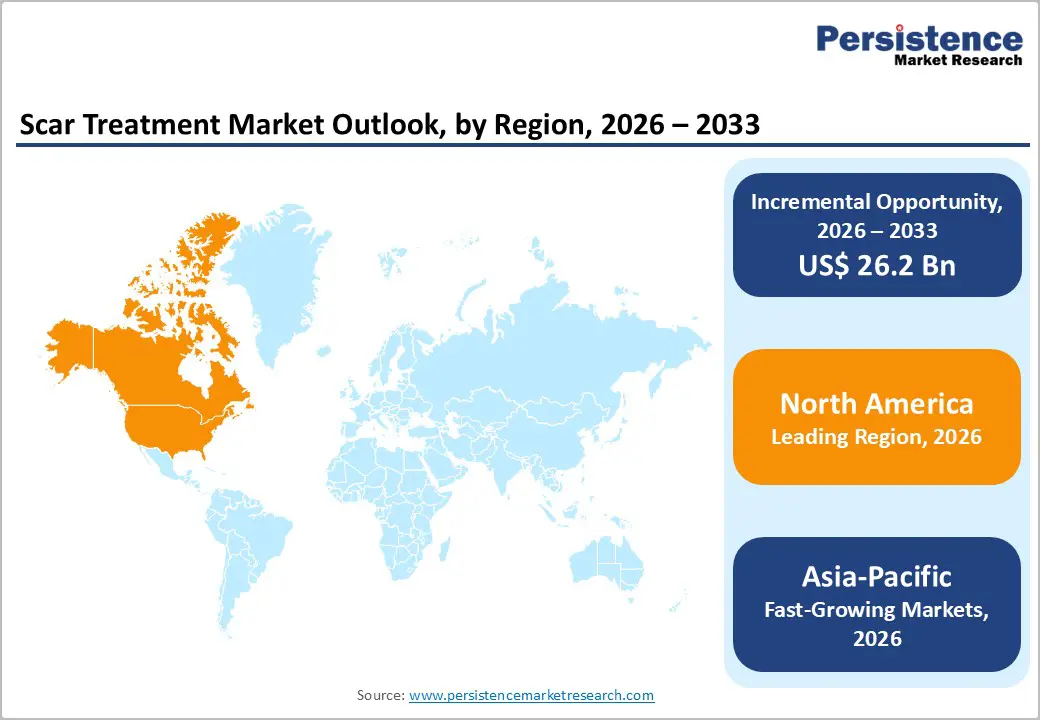

The global scar treatment market is growing steadily, driven by the adoption of digital healthcare, telehealth, and analytics. North America leads with strong infrastructure, strict regulations, and high-quality standards. Asia-Pacific is the fastest-growing region, fueled by expanding healthcare facilities, government initiatives, rising patient awareness, and increasing investments in diagnostic tools, services, and interoperable solutions.

Key Industry Highlights

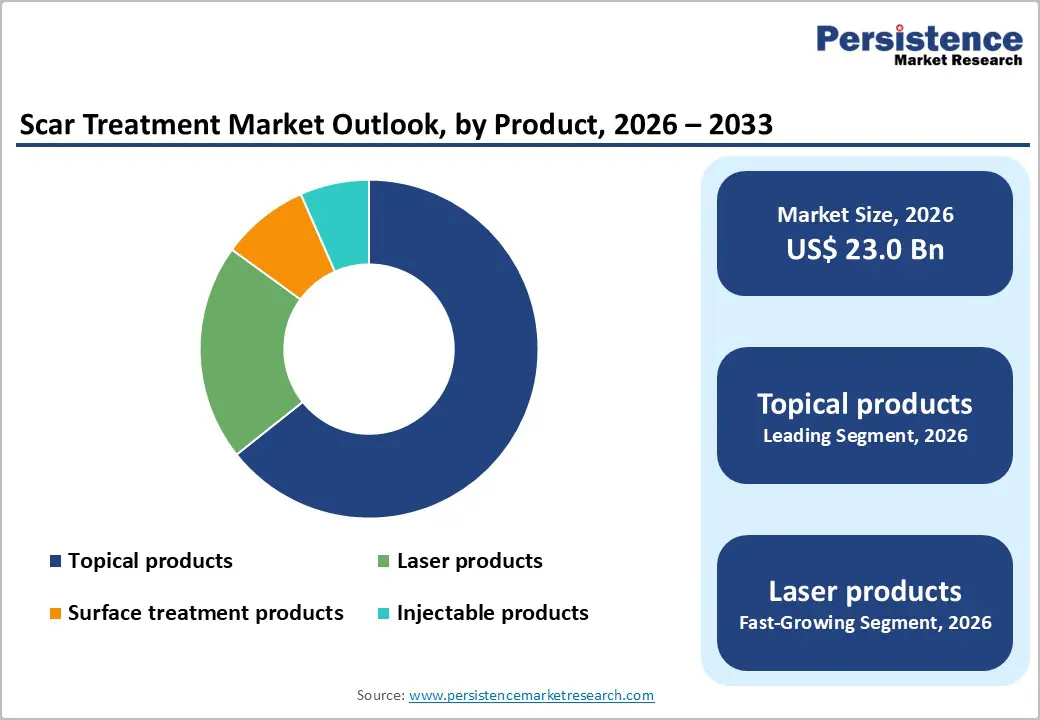

- Dominant Segment: Topical Products are a leading segment in the Scar Treatment Market, with a 64.3% share in 2025, offering effective scar reduction, ease of application, and high patient compliance. They provide consistent, reproducible results, support combination therapies, enhance healing and skin regeneration, and integrate with advanced dermatological protocols for improved cosmetic outcomes and patient satisfaction.

- Dominant Region: North America leads with strong infrastructure, regulatory support, and routine adoption of metabolic screening. Asia-Pacific is the fastest-growing region, driven by expanding healthcare facilities, rising prevalence of metabolic disorders, government health initiatives, and growing investments in diagnostic laboratories and digital testing technologies.

- Market Drivers: Rising diabetes and obesity rates, demand for early diagnosis, advanced assay technologies, and digital health integration fuel market growth.

- Market Opportunities: Point-of-care metabolic testing, AI-enabled diagnostics, multiplex metabolic panels, personalized disease management, telehealth integration, and expansion into emerging healthcare markets.

| Global Market Attributes | Key Insights |

|---|---|

| Scar Treatment Market Size (2026E) | US$ 23.0 Bn |

| Market Value Forecast (2033F) | US$ 49.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 11.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.3% |

Market Dynamics

Driver: Growing aesthetic and cosmetic awareness among patients

Global aesthetic and cosmetic procedures have risen sharply as patients become more aware of appearance-focused healthcare options. According to the International Society of Aesthetic Plastic Surgery (ISAPS), approximately 38 million aesthetic procedures were performed worldwide in 2024, including surgical and non-surgical treatments, representing a 42.5% increase from 2020. This reflects broad patient interest in improving skin and appearance, increasing demand for treatments that address scars, wrinkles, and other skin imperfections. Scar revision and related cosmetic interventions were among the procedures gaining traction alongside eyelid surgery and fillers.

In India, aesthetic adoption is also growing, with 1.29 million cosmetic and beauty treatments undertaken in 2024, including injectables, facial rejuvenation, and scar revision procedures, driven by social media influence and lifestyle shifts. The 7% annual increase in non-surgical procedures indicates rising public acceptance of cosmetic care. Greater awareness of available treatments and visible outcomes is expanding patient engagement with scar treatment solutions, supporting market growth as global aesthetic consciousness continues to rise.

Restraints: High cost of advanced scar treatment devices and procedures

Advanced scar treatments such as laser skin resurfacing and other energy-based therapies often carry high out-of-pocket costs because they are considered elective or cosmetic rather than medically necessary. In the United States, laser skin resurfacing, a procedure that can reduce scar visibility, averages around USD 1,800 per session, and additional clinical fees (facility, anesthesia, follow-ups) add to overall expenses. Most insurance plans do not cover cosmetic scar treatments, leaving patients responsible for all costs.

In India and similar markets, the per-session cost of laser scar treatments can range from several thousand to tens of thousands of rupees depending on technology and clinic location. For example, Fractional CO laser sessions may cost between 5,000 and 40,000 per session in major cities, with multiple sessions typically needed for significant improvement. Because these procedures are not covered by most health insurance schemes, the cumulative cost burden can deter patients from pursuing advanced scar treatments, limiting market growth and adoption.

Opportunity: Development of personalized scar management therapies

Personalized medicine, which tailors treatment based on an individual’s genetics, environment, and lifestyle, is gaining traction across healthcare because it improves treatment precision and outcomes by moving beyond one-size-fits-all approaches. The NIH’s Precision Medicine Initiative, through programs such as All of Us, which has enrolled hundreds of thousands to build diverse health datasets, is creating a foundation for individualized diagnostics and therapies by linking genetic and health information to treatment response patterns. This enables clinicians to anticipate which interventions work best for specific patient subgroups rather than relying on generalized protocols.

In dermatology, research into molecular biomarkers and precision strategies demonstrates how personalized approaches enhance the management of complex skin conditions by identifying disease mechanisms and matching treatments to individual profiles. While this research has thus far focused more on inflammatory and neoplastic skin diseases, the same frameworks, such as biomarker profiling and targeted intervention design, can be adapted to scar management. AI-assisted imaging and predictive models already show improved classification accuracy for scar types, enabling earlier, risk-stratified interventions that reduce ineffective treatment cycles, signaling a clear opportunity for personalized scar therapies to elevate clinical efficacy and patient satisfaction.

Category-wise Analysis

By Product, Topical products-Dominates the Scar Treatment Market

Topical occupies 64.3% share of the global market in 2025, due to its non-invasive nature, proven efficacy, and wide accessibility. Silicone-based gels and sheets, the most commonly used topicals, have been clinically shown to reduce scar height, pigmentation, and stiffness, making them a first-line therapy in post-surgical and traumatic scar management. They maintain hydration, modulate collagen deposition, and improve scar appearance without the need for invasive procedures. Topical treatments are convenient, cost-effective, and suitable for home use, reducing clinic visits and making them accessible in regions with limited dermatological care. Their affordability, safety, and clinical validation collectively make topical products the dominant segment in the scar treatment market.

By Application, Atrophic scars dominate due to high prevalence, facial visibility, and demand for collagen-stimulating treatments

Atrophic scar products dominate the scar treatment market because atrophic scars are the most common form of scarring encountered in dermatological practice. Clinical classification shows that 80–90% of acne scars result from a net loss of collagen, producing atrophic depressions rather than raised tissue, while hypertrophic and keloid scars account for a much smaller share.

This high prevalence drives demand for treatments tailored to atrophic scars, including resurfacing procedures, needling techniques, and topical agents that stimulate collagen remodeling. The frequency of atrophic scars in visible areas, such as the face, increases patients' motivation for effective therapies, reinforcing their dominance in clinical and aesthetic treatment portfolios.

Regional Insights

North America Scar Treatment Market Trends

North America dominates the scar treatment market with a 40.5% share in 2025, driven by advanced healthcare infrastructure, high consumer awareness, and widespread adoption of aesthetic and dermatological treatments. The American Society of Plastic Surgeons reports that over 28 million cosmetic, reconstructive, and minimally invasive procedures were performed in the U.S. in 2023, reflecting strong demand for scar-prevention and revision therapies. Patients seek treatments including laser therapy, injectables, and topical solutions to improve appearance and confidence.

The region benefits from regulatory support through the FDA, enabling faster adoption of innovative devices. High disposable incomes, a well-established network of dermatology clinics and med spas, and a cultural emphasis on aesthetics further reinforce North America’s leadership in scar treatment, making it the dominant global market.

Europe Scar Treatment Market Trends

Europe is an important region for scar treatment because the high incidence of injuries and surgeries contributes to a substantial scar burden and demand for effective therapies. An international epidemiological survey found that about 48.5% of adults report having at least one scar, reflecting widespread prevalence of scars from accidents, surgery, or skin conditions. Additionally, in the European Union in 2023, there were 20,380 road traffic fatalities, and official data indicate that for every fatality, there are multiple serious injuries, many resulting in long-term wounds that can lead to scarring. Pathological scarring from burn injuries (a common cause of scars) affects 32–72% of cases and contractures in 38–54%, underscoring the clinical need for scar management. This combination of high injury incidence and scar prevalence makes Europe a key region for scar treatment demand.

Asia-Pacific Scar Treatment Market Trends

Asia Pacific is the fastest-growing region for scar treatment because the underlying health conditions and injury burden that lead to scars are especially high and increasing across this area. The World Health Organization reports that the Asia-Pacific region (including South-East Asia and Western Pacific) accounts for a majority of global injury deaths and disabilities, with injuries from traffic collisions, burns and trauma causing significant long-term wounds that require scar management. In Asia alone, about 46 % of global burn cases and deaths occur, indicating a disproportionately high incidence of scar-causing injuries. Rapid urbanization and rising surgical volumes increase acute wound cases requiring effective scar care, while aging populations and conditions like diabetes elevate chronic wound and scar prevalence, driving accelerated demand for scar treatment solutions across the region.

Market Competitive Landscape

Leading companies in the scar treatment market prioritize advanced therapies, scalable manufacturing, and stringent regulatory compliance. They invest in research, clinical validation, and high-quality materials to improve outcomes. Strategic collaborations with clinicians and institutions, standardized treatment protocols, and integrated supply chains foster innovation and trust. Enhanced patient access, education, and evidence-based solutions drive adoption across dermatology and surgical care.

Key Industry Developments:

- In October 2025, Sonoma Pharmaceuticals, Inc. and Medline Industries announced that they had launched a new hypochlorous acid (HOCl)-based wound cleanser manufactured by Sonoma for distribution in U.S. hospitals and healthcare channels.

- In September 2025, Smith+Nephew, the global medical technology company, expanded its Advanced Wound Bioactives portfolio by launching the CENTRIO Platelet-Rich Plasma (PRP) System in the United States.

Companies Covered in Scar Treatment Market

- Smith and Nephew plc.

- HRA Pharma

- Sonoma Pharmaceuticals, Inc.

- CCA Industries Inc.

- Cynosure, Inc.

- Avita Medical Limited

- Mölnlycke Health Care AB

- Pacific World Corporation

- Shanghai Fosun Pharmaceuticals Ltd.

- Beijing Toplaser Technology Company Limited

- Bausch Health Companies Inc.

- Others

Frequently Asked Questions

The market is anticipated to reach a value of US$ 44.2 Bn by 2032.

Laser and other light treatments are the permanent solution for scar treatment and removal.

Rising demand for aesthetics along with increasing number of road accidents and burn cases are driving market growth.

North America is estimated to emerge as the leading region with a share of 25.4% in 2024.

Smith and Nephew plc., HRA Pharma, and Sonoma Pharmaceuticals, Inc.are the prominent companies in the market.