- Pharmaceuticals

- OTC Scar Treatment Market

OTC Scar Treatment Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

OTC Scar Treatment Market by Product (Gels, Ointments, Oils, Sheets, Sprays, and Others), by Application (Atrophic Scars, Hypertrophic Scars and Keloids, Contractures, Burns, and Stretch Marks), by Distribution Channel (Hospitals Pharmacies, Retail Pharmacies, and Online Pharmacies), and Regional Analysis from 2026 to 2033.

OTC Scar Treatment Market Share and Trend Analysis

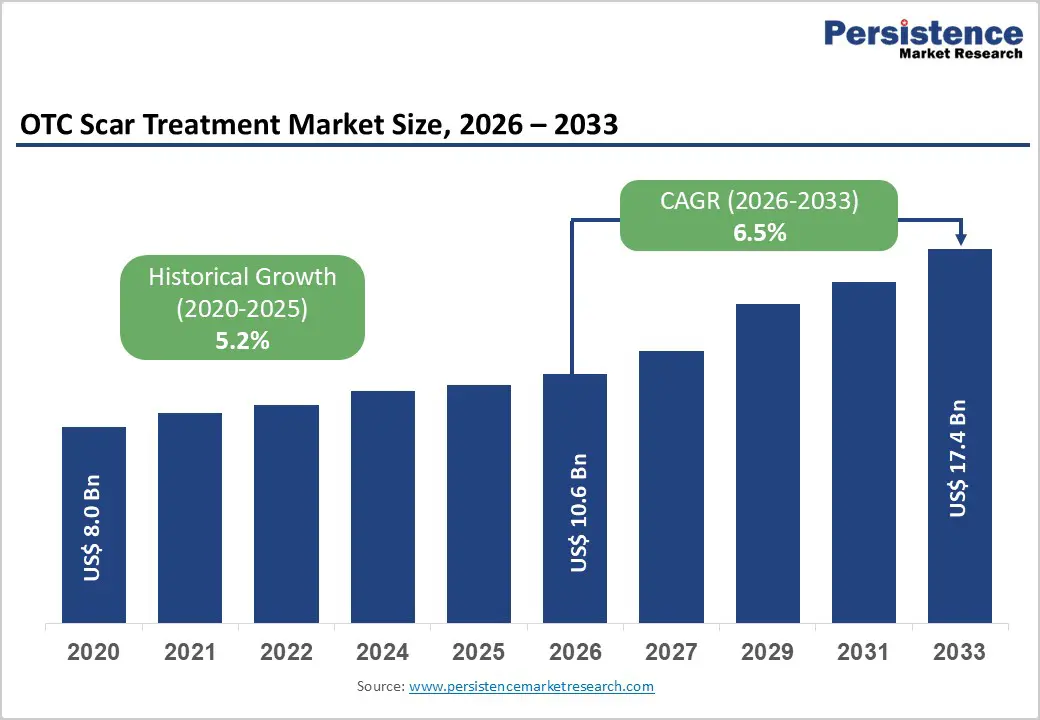

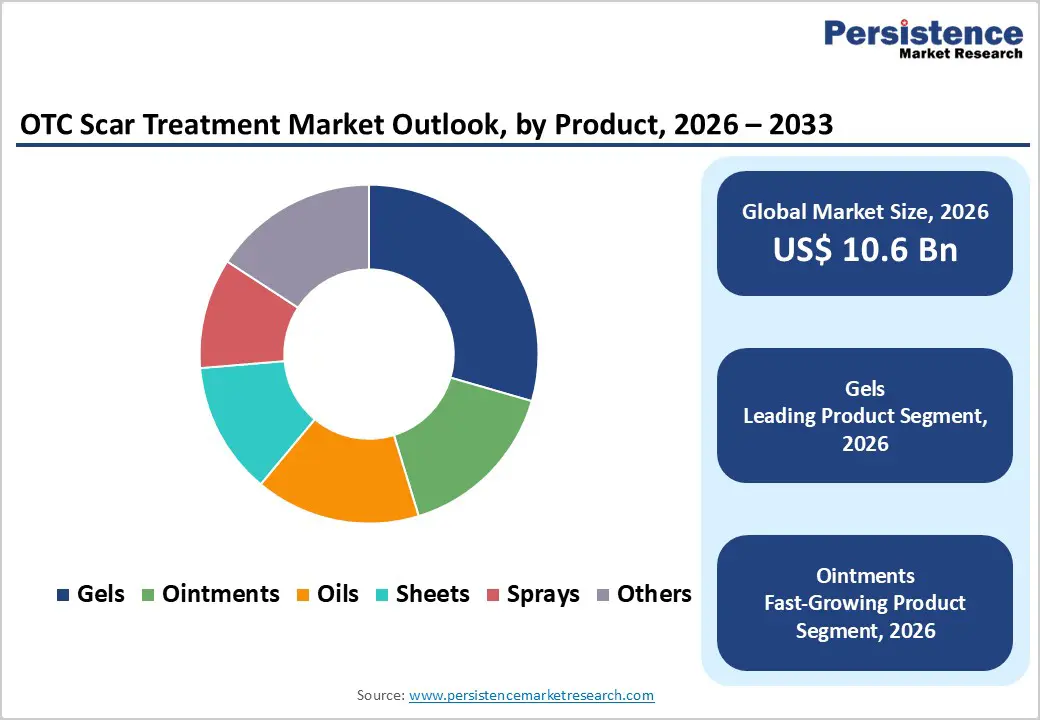

The global OTC scar treatment market size is estimated to grow from US$ 10.6 Bn in 2026 to US$ 17.4 Bn by 2033. The market is projected to grow at a CAGR of 6.5% from 2026 to 2033.

Global demand for OTC (over-the-counter) scar treatment products is steadily increasing, driven by the rising prevalence of skin injuries and conditions, such as acne, surgical procedures, burns, trauma, and cosmetic interventions that result in visible scarring. Growing consumer emphasis on aesthetic appearance, skin health, and early scar management is supporting sustained market growth. Increased awareness of non-invasive, at-home treatment options, coupled with wider availability of dermatologist-recommended OTC formulations, is accelerating adoption globally. OTC scar treatments are widely used for managing post-acne scars, surgical scars, stretch marks, and minor burn scars due to their affordability, ease of use, and accessibility without prescriptions.

Expanding retail pharmacy networks and the rapid growth of online pharmacies are further strengthening product reach. Advancements in topical formulations, including silicone-based gels, combination therapies, and natural ingredient blends, are improving treatment outcomes and consumer confidence. Additionally, rising cosmetic procedure volumes, growing influence of social media-driven beauty standards, and increasing focus on preventive skincare are reinforcing long-term demand for OTC scar treatment products worldwide.

Key Industry Highlights

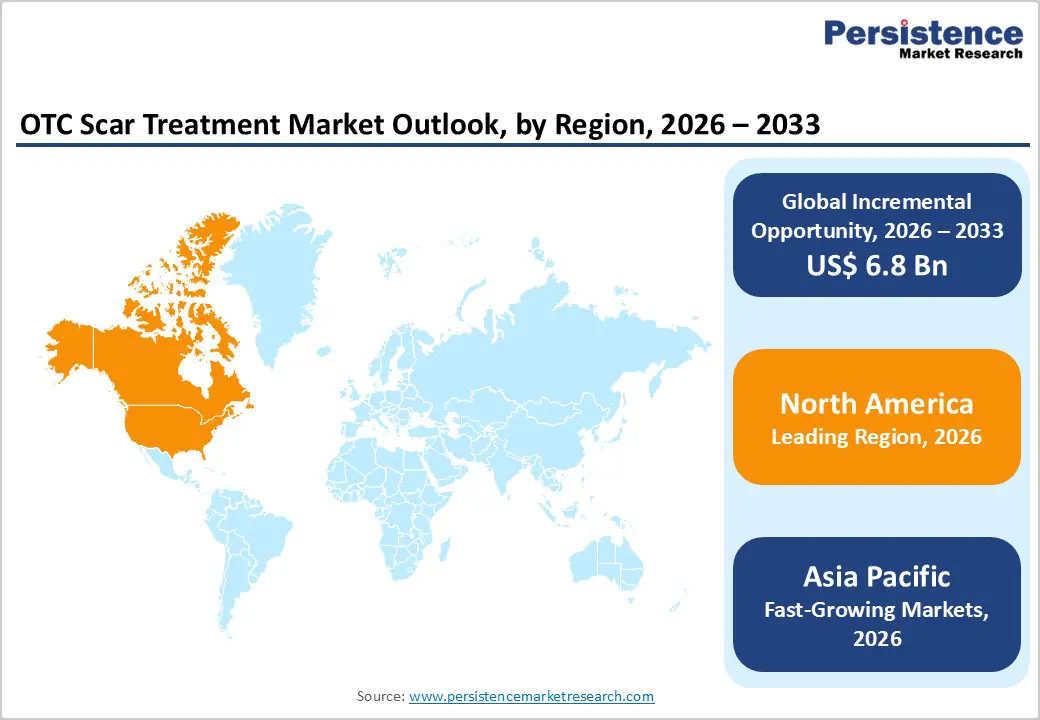

- Leading Region: North America holds the largest share at 47.3%, supported by high consumer awareness, strong purchasing power, a well-developed OTC pharmaceutical ecosystem, widespread retail pharmacy penetration, and high adoption of scar management products following surgical and cosmetic procedures.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to rising skincare awareness, rising disposable incomes, rapid urbanization, increasing acne prevalence, expansion of retail and online pharmacy channels, and the strong influence of beauty and dermatology trends. Leading Product Segment: Gels dominate the market due to ease of application, fast absorption, non-greasy texture, and high consumer preference for daily-use scar management across multiple scar types.

- Fastest-Growing Product Segment: Ointments are growing rapidly as consumers increasingly seek intensive moisturizing and barrier-based formulations for post-surgical, burn, and long-term scar care.

- Leading Application Segment: Atrophic scars remain the top segment, driven by the high incidence of acne scarring and post-injury depressions, particularly among adolescents and young adults.

- Fastest-Growing Application Segment: Hypertrophic scars and keloids are scaling quickly as awareness of early scar intervention rises and demand grows for silicone-based and clinically supported OTC treatments.

| Global Market Attributes | Key Insights |

|---|---|

| OTC Scar Treatment Market Size (2026E) | US$ 10.6 Bn |

| Market Value Forecast (2033F) | US$ 17.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.2% |

Market Dynamics

Driver – Rising Prevalence of Skin Injuries, Cosmetic Awareness, and Shift Toward Self-Care Dermatology

Growth is primarily driven by the increasing prevalence of skin injuries and conditions that result in visible scarring, including acne, surgical procedures, burns, traumatic wounds, and cosmetic interventions. Acne-related scarring remains one of the most common dermatological concerns globally, particularly among adolescents and young adults, creating sustained demand for accessible, non-prescription scar management solutions. In parallel, the rising number of surgical procedures—ranging from orthopedic and cardiovascular surgeries to cosmetic and minimally invasive procedures—has significantly expanded the post-procedure scar care population.

Growing aesthetic awareness and heightened focus on personal appearance, influenced by social media and beauty standards, are further accelerating adoption of OTC scar treatment products. Consumers increasingly prefer non-invasive, at-home solutions that are affordable, easy to use, and supported by dermatological recommendations. Advancements in topical formulations, including silicone-based gels, combination therapies, and natural ingredient blends, have improved clinical outcomes and user satisfaction. Additionally, expanding retail pharmacy networks, increasing online availability, and aggressive brand marketing are enhancing product visibility and accessibility. The global shift toward preventive skincare and early scar intervention continues to reinforce long-term demand for OTC scar treatment products.

Restraints – Variable Treatment Outcomes, Limited Clinical Evidence, and Consumer Price Sensitivity

The market faces restraints related to inconsistent treatment outcomes and limited standardized clinical evidence across OTC scar treatment products. Scar formation varies significantly depending on skin type, injury severity, genetic factors, and wound care practices, leading to unpredictable results and varied consumer satisfaction. Many OTC products rely on cosmetic claims rather than robust clinical validation, which can reduce confidence among dermatologists and informed consumers.

Price sensitivity, particularly in emerging economies, also limits adoption of premium scar treatment products, especially silicone-based sheets and advanced formulations that require prolonged use. In addition, improper or inconsistent product usage by consumers can diminish perceived effectiveness, contributing to negative reviews and repeat-purchase hesitation. Regulatory variations across regions regarding labeling, ingredient approvals, and advertising claims further complicate market expansion for manufacturers operating globally. Competition from in-clinic procedures such as laser therapy, microneedling, and injectable treatments may also divert consumers seeking faster or more visible results. Collectively, these factors create challenges in building long-term consumer trust, ensuring consistent efficacy, and maintaining sustained brand loyalty in the OTC scar treatment landscape.

Opportunity – Innovation in Formulations, Expansion in Emerging Markets, and Digital Health Influence

Significant growth opportunities are emerging from innovation in topical formulations and expanding demand in emerging markets. Development of advanced silicone-based gels, multi-ingredient formulations combining antioxidants, peptides, and botanical extracts, and products tailored for specific scar types offer strong differentiation potential. Increasing consumer preference for clean-label, natural, and dermatologically tested products further supports innovation-led growth.

Emerging economies across Asia Pacific, Latin America, and the Middle East present substantial untapped potential due to rising disposable incomes, growing awareness of skincare, and expanding retail and online pharmacy infrastructure. Government-led healthcare awareness programs and increased access to dermatology education are improving early scar management adoption. The rapid growth of e-commerce, influencer-driven marketing, and tele-dermatology platforms is reshaping consumer purchasing behavior, enabling brands to reach younger and digitally engaged populations more effectively. Additionally, partnerships with dermatologists, cosmetic clinics, and pharmacies to promote post-procedure scar care regimens are opening new distribution and recommendation channels. As preventive skincare gains prominence and consumers increasingly prioritize long-term skin appearance, OTC scar treatment products are well positioned to capture sustained demand and unlock long-term market expansion opportunities.

Category-wise Analysis

By Product, Gels Lead Due to Ease of Application, High Consumer Acceptance, and Proven Clinical Effectiveness

Gels are projected to dominate the global OTC scar treatment market in 2026, accounting for a revenue share of 28.0%. This dominance is primarily attributed to their lightweight texture, rapid absorption, non-greasy nature, and high patient compliance across a wide range of scar types. Gel-based formulations are extensively used for post-surgical scars, acne scars, and minor traumatic scars due to their ability to form a breathable layer over the skin while delivering active ingredients effectively. Their compatibility with sensitive skin and suitability for both facial and body application further strengthen adoption. Additionally, the availability of silicone-based and herbal-infused gel products has expanded consumer choice and boosted repeat usage. Continuous product innovation, dermatological endorsements, and aggressive marketing through retail and online channels are reinforcing the leadership of gels in the OTC scar treatment market globally.

By Application, Atrophic Scars Dominate Due to High Prevalence of Acne-Related and Post-Injury Scarring

The atrophic scars segment is expected to dominate the global OTC scar treatment market in 2026, capturing a revenue share of 37.2%. This leadership is driven by the widespread prevalence of acne scars, post-surgical depressions, and injury-related skin indentations, particularly among adolescents and young adults. Atrophic scars often require long-term topical management, making OTC products a preferred first-line solution before clinical interventions. Growing aesthetic awareness, rising social media influence, and increasing demand for self-care dermatology products have significantly increased consumer spending on at-home scar management. OTC gels, creams, and oils are commonly used for mild to moderate atrophic scars due to their affordability and accessibility. Additionally, increasing dermatological recommendations for early topical intervention are supporting sustained demand. As acne incidence and cosmetic consciousness continue to rise globally, the atrophic scars segment is expected to remain the largest revenue contributor.

By Distribution Channel, Retail Pharmacies Lead Due to Strong Physical Reach and Consumer Trust in OTC Purchases

Retail pharmacies are projected to dominate the global OTC scar treatment market in 2026, accounting for a revenue share of 40.3%. This leadership is driven by widespread geographic presence, immediate product availability, and strong consumer trust in pharmacist-recommended OTC solutions. Retail pharmacies serve as a primary point of purchase for post-surgical patients and individuals seeking quick scar remedies without prescriptions. The ability to physically compare products, receive basic guidance, and access trusted brands significantly influences purchasing decisions. Additionally, strong relationships between pharmaceutical manufacturers and retail pharmacy chains support effective product placement and promotional visibility. While online channels are expanding rapidly, retail pharmacies continue to dominate due to impulse buying, emergency needs, and consumer preference for in-store healthcare products. As OTC dermatology products remain a core pharmacy category, retail pharmacies are expected to sustain their leadership position.

Region-wise Insights

North America OTC Scar Treatment Market Trends

North America is expected to dominate the global OTC scar treatment market with a value share of 47.3% in 2026, led primarily by the United States. The region benefits from high consumer awareness regarding skin health, strong purchasing power, and a well-established OTC pharmaceutical and dermatology product ecosystem. A high incidence of acne, cosmetic procedures, surgical interventions, and sports-related injuries contributes to consistent demand for scar management products.

The presence of leading manufacturers, advanced distribution infrastructure, and strong brand penetration supports market growth. Additionally, favorable regulatory frameworks allow rapid commercialization of innovative OTC formulations, including silicone-based gels and natural ingredient blends. Strong emphasis on aesthetics, preventive skincare, and early scar intervention further drives product adoption. Extensive marketing campaigns, dermatologist-backed product endorsements, and widespread availability across retail and online channels reinforce North America’s dominant position. Continuous product innovation and consumer preference for premium OTC solutions are expected to sustain regional leadership.

Europe OTC Scar Treatment Market Trends

The Europe OTC scar treatment market is expected to grow steadily, supported by strong dermatological awareness and expanding cosmetic and post-surgical care across countries such as Germany, the U.K., France, Italy, and Spain. The region benefits from a well-developed healthcare infrastructure, high-quality regulatory standards, and strong consumer trust in pharmacy-dispensed OTC products. Rising demand for scar management following cosmetic surgeries, orthopedic procedures, and burn treatments is supporting market expansion. Europe’s aging population also contributes to increased surgical interventions, indirectly boosting scar treatment demand.

Additionally, growing preference for silicone-based and natural ingredient formulations aligns with regional consumer trends toward safety and efficacy. Strong pharmacy networks and increasing penetration of private-label dermatology products further support market growth. As awareness of early scar treatment continues to improve, Europe is expected to maintain consistent, long-term expansion in the OTC scar treatment market.

Asia Pacific OTC Scar Treatment Market Trends

The Asia Pacific OTC scar treatment market is expected to register a relatively higher CAGR of around 8.8% between 2026 and 2033, driven by rising healthcare awareness, expanding middle-class populations, and increasing access to OTC dermatology products. Countries such as China, India, Japan, South Korea, and Australia are witnessing growing demand for scar treatment due to high acne prevalence, rising cosmetic procedures, and increased road and workplace injuries. Rapid urbanization and lifestyle changes are further contributing to skin-related concerns. Expanding retail pharmacy chains, strong growth of e-commerce platforms, and improving affordability of OTC products are enhancing market penetration.

Additionally, increasing influence of social media, beauty standards, and dermatology education campaigns are driving early adoption of scar management solutions. Local manufacturing, competitive pricing, and growing presence of international brands are improving accessibility. As consumer awareness and disposable income continue to rise, Asia Pacific is expected to emerge as the fastest-growing regional market.

Market Competitive Landscape

The global OTC scar treatment market is highly competitive, with strong participation from companies such as Smith + Nephew, Merz Inc., Enaltus LLC, Occulus Innovative Sciences Inc., and Cynosure Inc. These players leverage established global distribution networks, strong brand recognition, and diversified medical and dermatology-focused product portfolios to address growing consumer demand for effective, non-prescription scar management solutions.

Their offerings emphasize clinically proven formulations, ease of application, long-term scar appearance improvement, and suitability across multiple scar types, including post-surgical, acne, burn, and hypertrophic scars. Continuous product innovation, regulatory compliance, dermatological validation, and adherence to international quality and manufacturing standards remain critical to sustaining competitive positioning in the global OTC scar treatment market.

Key Industry Developments:

- In January 2026, researchers at the University of Zurich highlighted significant advancements in bio-engineered skin grafts for severe burn injuries, demonstrating the potential to improve post-burn healing outcomes and reduce long-term scarring a key driver for increased interest in advanced scar management products and therapies.

Companies Covered in OTC Scar Treatment Market

- Smith + Nephew

- Merz Inc.

- Enaltus LLC

- Occulus Innovative Sciences Inc.

- Cynosure Inc

- Avita Medical Limited

- Lumenis

- Syneron Medical Ltd.

- Nutramarks Inc.

- Mölnlycke Health Care

- Pacific World Corporation

- Valeant Pharmaceuticals International Inc.

- SkinCeuticals

- A. Menarini Singapore Pte. Ltd.

- Others

Frequently Asked Questions

The global OTC scar treatment market is projected to be valued at US$ 10.6 Bn in 2026.

The market is driven by rising prevalence of skin injuries and conditions (post-surgical scars, acne, trauma, burns), increasing consumer awareness of skincare and aesthetic appearance, growing demand for non-invasive at-home treatments, advancements in topical formulations, and expanding e-commerce access and dermatological endorsement.

The global OTC scar treatment market is poised to witness a CAGR of 6.5% between 2026 and 2033.

Expansion into emerging markets and development of advanced, natural, and clean-label formulations to meet diverse consumer preferences.

Smith + Nephew, Merz Inc., Enaltus LLC, Occulus Innovative Sciences Inc., and Cynosure Inc., are some of the key players in the OTC scar treatment market.