- Biotechnology

- Miscarriage Testing Market

Miscarriage Testing Market Size, Share, and Growth Forecast, 2026 - 2033

Miscarriage Testing Market by Technology (Chromosomal Microarray Analysis (CMA), Next-Generation Sequencing (NGS), Conventional Karyotyping, Fluorescence in Situ Hybridization), Application (Recurrent Pregnancy Loss (RPL), First-Time Sporadic, Stillbirth Analysis, Threatened Miscarriage Evaluation), End-User (Hospitals, Fertility Clinics, Research and Academic Institutions), and Regional Analysis for 2026-2033

Miscarriage Testing Market Share and Trends Analysis

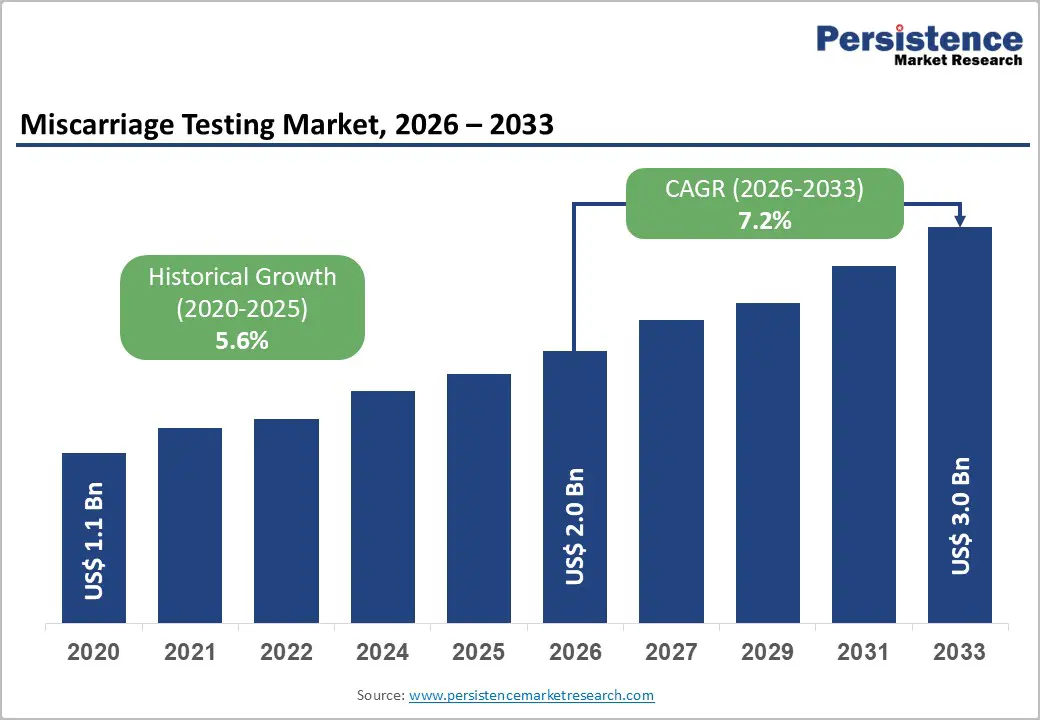

The global miscarriage testing market size is likely to be valued at US$ 2.0 billion in 2026, and is projected to reach US$ 3.0 billion by 2033, growing at a CAGR of 7.2% during the forecast period 2026−2033. Growth is being driven by increasing maternal age worldwide, which is elevating the clinical need for genetic evaluation following pregnancy loss. At the same time, patients and clinicians are recognizing the value of evidence-based testing in guiding future reproductive planning.

Hospitals and fertility centers are therefore integrating structured diagnostic pathways to support informed counseling and personalized care strategies. Technological innovation is strengthening diagnostic precision and accessibility. Next-generation sequencing (NGS) and chromosomal microarray analysis (CMA) are enabling detailed assessment of chromosomal abnormalities that often contribute to miscarriage. These platforms are improving detection rates while reducing turnaround time and overall testing costs. As laboratories are adopting automated workflows and standardized protocols, service delivery is becoming more efficient and scalable.

Key Industry Highlights

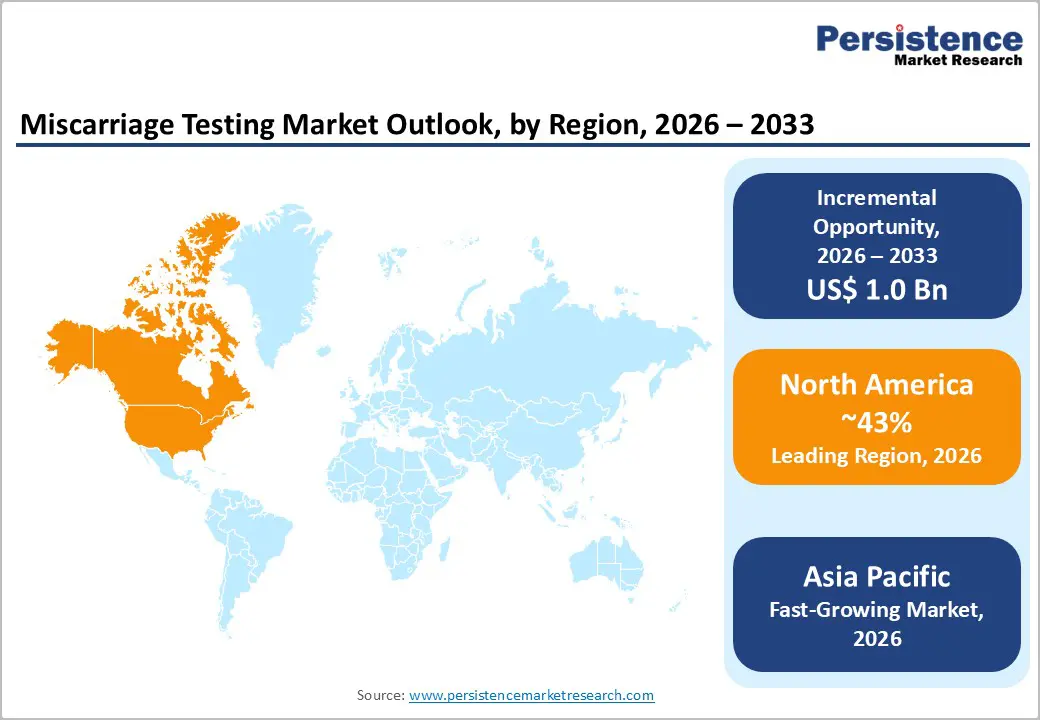

- Dominant Region: North America is expected to capture an estimated market share of 43% in 2026, supported by an advanced healthcare infrastructure and comprehensive insurance coverage frameworks.

- Fastest-growing Market: The Asia Pacific market is set to record the highest growth through 2033, owing to supportive government reproductive health policies.

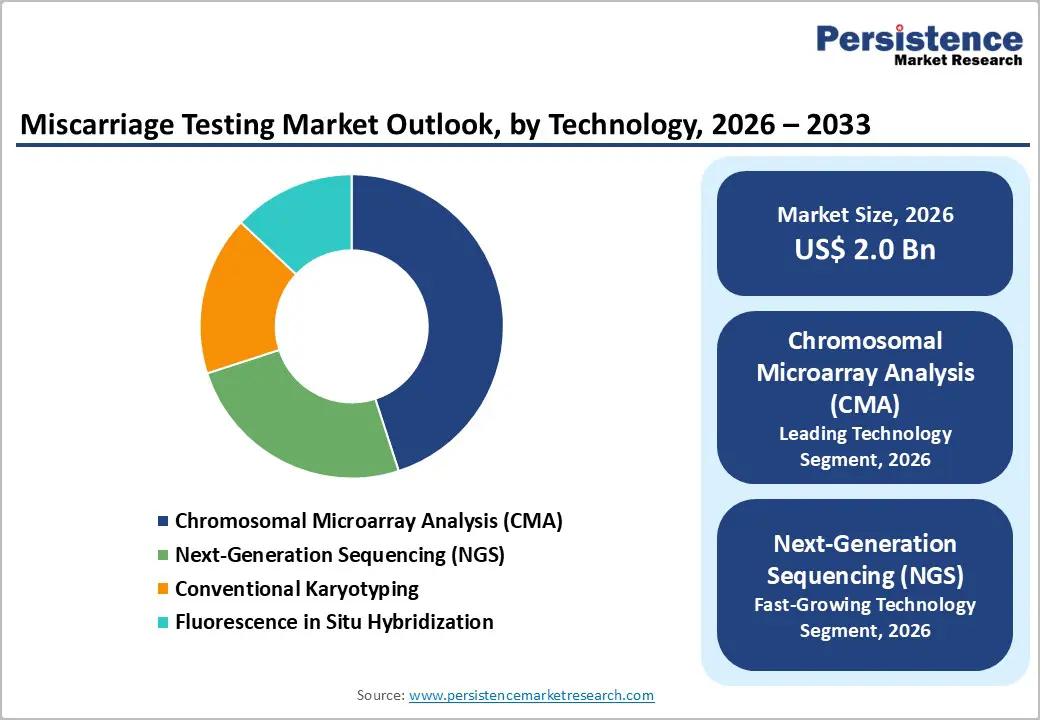

- Dominant & Fastest-growing Technology: CMA is likely to dominate in 2026, while NGS is anticipated to be the fastest-growing technology during the 2026-2033 forecast period.

- Market Driver: Advancements in NGS and CMA technologies are transforming miscarriage testing practices worldwide.

- October 2025: Researchers from the University of Warwick and University Hospitals Coventry and Warwickshire (UHCW) NHS Trust identified an abnormal decidual reaction in the endometrium (womb lining) that can be a hidden cause of recurrent miscarriage by creating an unstable environment for embryo implantation.

| Key Insights | Details |

|---|---|

| Miscarriage Testing Market Size (2026E) | US$ 2.0 Bn |

| Market Value Forecast (2033F) | US$ 3.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Advancements in Genetic Testing Methodologies

Next-generation sequencing and chromosomal microarray analysis are transforming miscarriage testing practices worldwide. These cutting-edge tools directly tackle the core limitations of traditional cytogenetic karyotyping. Standard methods frequently face culture failures and maternal cell contamination issues, both of which generate unreliable results. In contrast, NGS and CMA provide superior diagnostic precision. They uncover subtle chromosomal anomalies that conventional techniques simply miss. Healthcare providers gain confidence in their findings, which supports more informed patient counseling. Businesses stand to benefit greatly by integrating these innovations into their offerings, as they open doors to wider patient demographics and diverse care settings.

CMA leverages single nucleotide polymorphism (SNP) microarrays to elevate detection capabilities without the need for lengthy cell cultures. Engineers have introduced rapid karyotyping systems that deliver outcomes swiftly and cost-effectively. Laboratories now distribute these services beyond elite academic institutions to everyday community hospitals and outpatient facilities. Insurers actively expand reimbursement policies, which accelerates uptake among varied populations. Strategic executives should seize this momentum to streamline workflows, emphasize premium diagnostic solutions, and solidify their roles in reproductive health. Firms position themselves for sustained growth by aligning operations with these accessible advancements, ultimately driving better clinical decisions and patient trust.

Sample Quality Challenges and Technical Complexity

The unpredictable nature of miscarriage events creates inherent difficulties in sample collection and processing that significantly constrain diagnostic success rates. Miscarriages frequently occur outside clinical settings, which results in degraded tissue samples or maternal contamination from endometrial tissue. Healthcare providers face considerable challenges in obtaining optimal specimens when patients experience pregnancy loss at home or in non-medical environments. The quality of these samples directly impacts the ability to perform accurate chromosomal analysis. Moreover, distinguishing fetal cells from maternal cells requires specialized laboratory protocols and technical expertise that remain unavailable across many healthcare facilities.

This technical complexity means that even when samples reach laboratories, the analytical process demands sophisticated equipment and highly trained personnel to ensure reliable results. Regional variations in laboratory infrastructure present additional barriers to market expansion, particularly in emerging markets where access to advanced genetic testing remains limited. Complex genetic assays require substantial equipment investments, specialized technical staff, and rigorous quality control systems that exceed the operational capacity of many community hospitals. These resource constraints force healthcare providers to refer samples to centralized specialty laboratories, which introduces coordination challenges between referring physicians and testing facilities. The referral process extends turnaround times for results delivery and adds transportation costs that ultimately increase the financial burden on patients and healthcare systems.

Integration with Comprehensive Fertility Treatment Pathways

The convergence of miscarriage testing with broader assisted reproductive technology (ART) services represents a high-value market opportunity that transforms how patients access genetic diagnostics. Fertility clinics increasingly recognize the strategic advantage of offering integrated genetic testing portfolios that encompass carrier screening, preimplantation genetic testing, non-invasive prenatal testing, and products of conception analysis as comprehensive care packages. This bundled approach fundamentally improves the patient experience by establishing coordinated testing workflows that eliminate the need for multiple provider interactions and fragmented care delivery. Patients benefit from centralized communication, streamlined sample collection procedures, and unified genetic counseling that addresses their complete reproductive health journey.

The expanding global in-vitro fertilization (IVF) market provides an established and rapidly growing distribution channel for miscarriage testing services, particularly given the clinical reality that IVF pregnancies experience early loss at meaningful rates. Technology platforms that enable seamless data integration between different genetic tests create substantial clinical value by allowing reproductive endocrinologists to correlate preimplantation screening results with subsequent miscarriage chromosomal analysis findings. These integrated data systems help physicians identify patterns, refine treatment protocols, and provide patients with more informed guidance for future conception attempts.

Category-wise Analysis

Technology Insights

Chromosomal microarray analysis is poised to dominate the technology type category, commanding approximately 45% of the miscarriage testing market revenue share in 2026. CMA scans the entire genome for copy number variations and loss of heterozygosity with high resolution. It bypasses culture-dependent steps that plague traditional methods, which ensures reliable results from challenging samples. Laboratories integrate CMA into standard protocols because it delivers actionable insights for recurrent pregnancy loss cases. Clinicians rely on its comprehensive detection of structural anomalies, which guides precise patient counseling and family planning decisions. This established position stems from widespread validation across diverse clinical settings.

Next-generation sequencing is likely to be the fastest-growing segment during the 2026-2033 forecast period. NGS sequences DNA directly to reveal single-nucleotide variants, insertions, deletions, and mosaicism that other methods overlook. Developers enhance NGS platforms for rapid turnaround and lower costs, which broadens access in community labs. Researchers pair with bioinformatics tools to interpret complex datasets efficiently. Healthcare networks adopt to address unmet needs in personalized reproductive diagnostics. Its versatility positions to capture share from legacy approaches as demand rises for advanced genetic insights.

Application Insights

Recurrent pregnancy loss (RPL) represents the dominant application segment for 2026, capturing an estimated 52% of the miscarriage testing market share in 2026. Professional society guidelines from the American College of Obstetricians and Gynecologists (ACOG) and the American Society for Reproductive Medicine (ASRM) recommend chromosomal analysis after two or more consecutive pregnancy losses, with many institutions adopting protocols for testing after any loss in patients with risk factors including advanced maternal age, known parental chromosomal abnormalities, or concerning fetal anatomic findings on ultrasound prior to loss. RPL patients demonstrate higher testing uptake due to stronger clinical recommendations, better insurance reimbursement, and increased patient motivation to identify causative factors after experiencing multiple losses.

First-time sporadic is expected to be the fastest-growing segment over the 2026-2033 forecast period. Providers now offer early genetic analysis on products of conception to detect aneuploidies or structural variants that inform future pregnancy planning. Laboratories streamline workflows to accommodate single-event testing, making it accessible beyond tertiary centers. Heightened awareness campaigns and patient advocacy push insurers toward broader coverage. This trend reflects a move toward proactive, patient-centered care that captures growing volumes from previously underserved cases.

End-User Insights

The hospitals segment is expected to lead with an approximate 65% market revenue share in 2026, reflecting the extensive centralization of genetic testing services in specialized laboratory facilities. Major reference laboratories, including Quest Diagnostics, LabCorp, and regional academic medical center laboratories, process the majority of miscarriage testing, leveraging established cytogenetic expertise, comprehensive test menus, and insurance payer relationships. Hospital-based testing benefits from integrated sample collection protocols, established tissue banking systems, and direct communication channels between laboratory directors and treating physicians that facilitate optimal test selection and results interpretation.

Fertility clinics are projected to be the fastest-growing segment during the 2026-2033 forecast period. These facilities increasingly offer comprehensive genetic testing portfolios as competitive differentiators in the competitive marketplace. Many fertility clinics have established in-house genetic testing capabilities or exclusive partnerships with specialty laboratories, enabling streamlined testing workflows, reduced turnaround times, and integrated patient counseling. This segment particularly drives adoption of advanced testing methodologies including NGS-based comprehensive chromosomal screening and molecular karyotyping, as fertility clinic patients typically demonstrate higher willingness to pay for premium testing services and value coordinated care delivery models that consolidate multiple testing touchpoints within their established provider relationship.

Regional Insights

North America Miscarriage Testing Market Trends

North America is set to hold a significant portion of the miscarriage testing market value at approximately 43% in 2026, driven by advanced healthcare infrastructure, comprehensive insurance coverage frameworks, and strong clinical practice guideline adoption among obstetricians and reproductive endocrinologists. The United States dominates regional performance within North America, driven by widespread adoption of assisted reproductive technology and demographic trends toward delayed childbearing among the maternal population. High utilization rates of fertility treatments naturally create substantial demand for miscarriage testing services, as these pregnancies require comprehensive genetic analysis when early losses occur. The regulatory environment plays a dual role in shaping market dynamics through Food and Drug Administration (FDA) oversight of laboratory-developed tests and Clinical Laboratory Improvement Amendments (CLIA) certification requirements.

These stringent quality standards ensure that patients receive accurate, reliable diagnostic results while simultaneously creating significant barriers to market entry. The American innovation ecosystem demonstrates remarkable strengths that position the country as a global leader in miscarriage testing advancement. Leading genomics technology companies such as Illumina and Thermo Fisher Scientific drive continuous technological innovation in sequencing platforms and analytical tools. Specialized reproductive genetics laboratories including Natera, Cooper Genomics, and Igenomix develop proprietary testing methodologies that enhance diagnostic accuracy and reduce turnaround times. Investment trends reflect strong market confidence, with venture capital and private equity firms directing substantial funding into reproductive health technology companies developing next-generation miscarriage testing solutions.

Europe Miscarriage Testing Market Trends

Europe claims a prominent position in the global market for miscarriage testing solutions. The regional market benefits from advanced genomic capabilities and unified regulatory standards. Germany stands out as the frontrunner. Robust healthcare systems support widespread genetic counseling within pregnancy loss pathways. Public insurance programs cover essential diagnostic tests. The United Kingdom advances through National Health Service (NHS) efforts that broaden access to genetic evaluations. Prestigious institutions such as Oxford and Cambridge drive cutting-edge research on pregnancy outcomes. France advances chromosomal microarray analysis adoption via government-backed precision medicine strategies and reproductive health funding.

The European Medicines Agency (EMA) and the European Union In Vitro Diagnostic Regulation (EU IVDR) establish consistent quality benchmarks across nations. These frameworks enable seamless laboratory networks and prioritize patient safety. A strong presence of European diagnostic companies, such as Eurofins and CENTOGENE, alongside U.S.-based multinationals, with increasing consolidation through mergers and acquisitions (M&A) is providing an extra boost for the market here. Investment trends focus on healthcare digitalization, telemedicine-enabled genetic counseling, and integration of artificial intelligence for chromosomal analysis automation. Market opportunities include Eastern European expansion as healthcare systems modernize and adoption of comprehensive testing protocols in Southern European countries where traditional karyotyping remains common practice.

Asia Pacific Miscarriage Testing Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing market for miscarriage testing from 2026 to 2033. China leads through rapid genetic testing network growth and supportive government reproductive health policies. Local firms such as BGI Genomics and Berry Genomics provide strong reproductive diagnostics at competitive prices. Japan achieves high testing uptake with advanced healthcare systems and emphasis on detailed prenatal care. India reveals vast potential from expanding middle-class populations and rising urban healthcare access. ASEAN countries, primarily Thailand, Singapore, and Malaysia, have transformed into medical tourism hubs, drawing fertility patients with advanced services.

Strategic advisors urge targeted actions in Asia Pacific's vibrant environment. Labs benefit from lower operational costs, skilled workforces, and biotechnology incentives. Venture capital supports local genetic companies actively. Global diagnostics firms collaborate with regional partners to accelerate technology transfers. Executives build reference laboratory networks to cover wider territories effectively. Companies develop budget-friendly tests tailored to local economic realities. Providers are expanding into secondary and tertiary cities alongside infrastructure improvements, while market leaders are combining international standards with local adaptations gain enduring competitive edges.

Competitive Landscape

The global miscarriage testing market structure is moderately consolidated, with established diagnostic and genomics companies shaping competitive intensity. Key participants include Natera, Quest Diagnostics Incorporated, Cooper Genomics, Thermo Fisher Scientific, and Illumina. These organizations are expanding their reproductive health portfolios by acquiring specialized genetics laboratories and integrating advanced molecular diagnostics capabilities. Consolidation is strengthening test menus, improving geographic reach, and enhancing laboratory scale efficiencies. As larger firms are broadening service offerings, they are reinforcing referral networks with obstetricians, fertility clinics, and hospital systems.

At the same time, technology-driven entrants are introducing rapid next-generation sequencing platforms and streamlined analytical workflows that are reducing turnaround time and operational costs. These innovations are challenging incumbent models that rely on centralized laboratory infrastructure. Market leaders are therefore balancing acquisition-led expansion with internal research and development investments to maintain agility. Executives are focusing on scalable automation, digital reporting systems, and clinical decision support tools to preserve differentiation.

Key Industry Developments

- In November 2025, researchers at the University of Sydney uncovered new biological insights into recurrent miscarriage in a study published in Human Reproduction, focusing on how differences in vitamin B3 processing and nicotinamide adenine dinucleotide (NAD) metabolism may contribute to repeated pregnancy loss. The team observed distinct metabolic changes linked with inflammation in women with a history of consecutive miscarriages, suggesting that altered cellular energy pathways may play a role in reproductive outcomes.

- In September 2025, researchers in China created a machine learning (ML) model that is using routine blood test data to forecast the risk of threatened miscarriage, a form of early pregnancy loss where bleeding occurs but the fetus remains viable. The algorithm is designed to detect at-risk pregnancies before clinical symptoms fully develop, potentially enabling earlier intervention by healthcare providers.

- In April 2025, the U.K. National Institute for Health and Care Research (NIHR) awarded £1 million in funding to Calla Lily Clinical Care for moving a novel device called Callavid into clinical testing to address threatened miscarriage. The technology is designed to deliver progesterone in a controlled and reliable way, reducing medication leakage and inconvenience compared with current vaginal pessary methods, and could become the first drug-device combination for this purpose if approved.

Companies Covered in Miscarriage Testing Market

- Natera, Inc.

- Quest Diagnostics Incorporated

- Laboratory Corporation of America Holdings

- Cooper Genomics

- Igenomix

- Thermo Fisher Scientific Inc.

- Illumina, Inc.

- BGI Genomics Co., Ltd.

- Invitae Corporation

- Integrated Genetics

- Reproductive Genetic Innovations

- Progenesis

- Berry Genomics Co., Ltd.

- CENTOGENE GmbH

- Myriad Genetics, Inc.

Frequently Asked Questions

The global miscarriage testing market is projected to reach US$ 2.0 billion in 2026.

The market is driven by rising awareness of pregnancy loss causes, advances in genetic diagnostics such as NGS and CMA, and expanding access to reproductive healthcare.

The market is poised to witness a CAGR of 7.2% from 2026 to 2033.

Major opportunities lie in emerging economies that offer expansion potential through affordable testing, technological innovations such as rapid testing platforms and integration with digital reproductive health tools.

Natera, Inc., Quest Diagnostics Incorporated, Cooper Genomics, Thermo Fisher Scientific Inc., and Illumina, Inc. are some of the key players in the market.