- Biotechnology

- Genetic Toxicology Testing Market

Genetic Toxicology Testing Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Genetic Toxicology Testing Market by Product (Kits and Reagents, Consumables and Services), Type (In Vitro and In Vivo), Assay (Comet Assay, Micronucleus Assay, Chromosomal Aberration Test, Genetic Mutation Test, and Others), Application (Pharmaceutical & Biotechnology, Food Industry, Cosmetics Industry, and Other) End-user (Pharmaceutical Companies, Contract Research Organizations, Academic and Research Institutions, and Others), and Regional Analysis from 2026 to 2033

Genetic Toxicology Testing Market Share and Trends Analysis

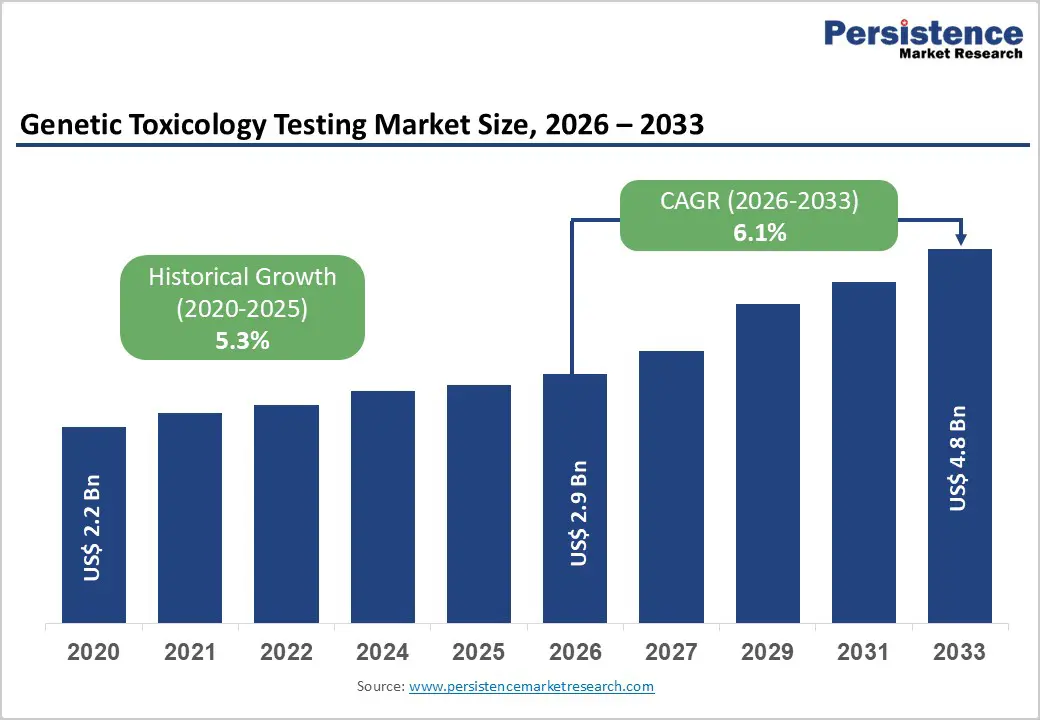

The global genetic toxicology testing market size is estimated to grow from US$ 2.9 billion in 2026 to US$ 4.8 billion by 2033, growing at a CAGR of 6.1% during the forecast period from 2026 to 2033.

The global demand for genetic toxicology testing is rising steadily, driven by increasing regulatory emphasis on drug safety, growing complexity of pharmaceutical and biotechnology pipelines, and heightened awareness of genotoxic risk assessment across regulated industries. Pharmaceutical companies, CROs, and research laboratories are increasingly adopting genetic toxicology studies to evaluate mutagenicity, clastogenicity, and DNA damage potential during early discovery, preclinical development, and regulatory submissions.

Expanding use of in vitro screening assays, followed by targeted in vivo confirmatory studies, is improving decision-making efficiency while reducing late-stage attrition. Rising investments in biopharmaceutical R&D, expansion of GLP- and GMP-compliant testing facilities, and growth of toxicology research institutes are accelerating global adoption. Continuous advancements in high-throughput screening, mechanism-based genotoxicity assays, automation, and AI-enabled data interpretation are improving predictive accuracy and study throughput. Additionally, increasing chronic disease burden, rising oncology pipelines, and stricter global regulatory requirements for impurity and safety profiling are further propelling overall market growth.

Key Industry Highlights:

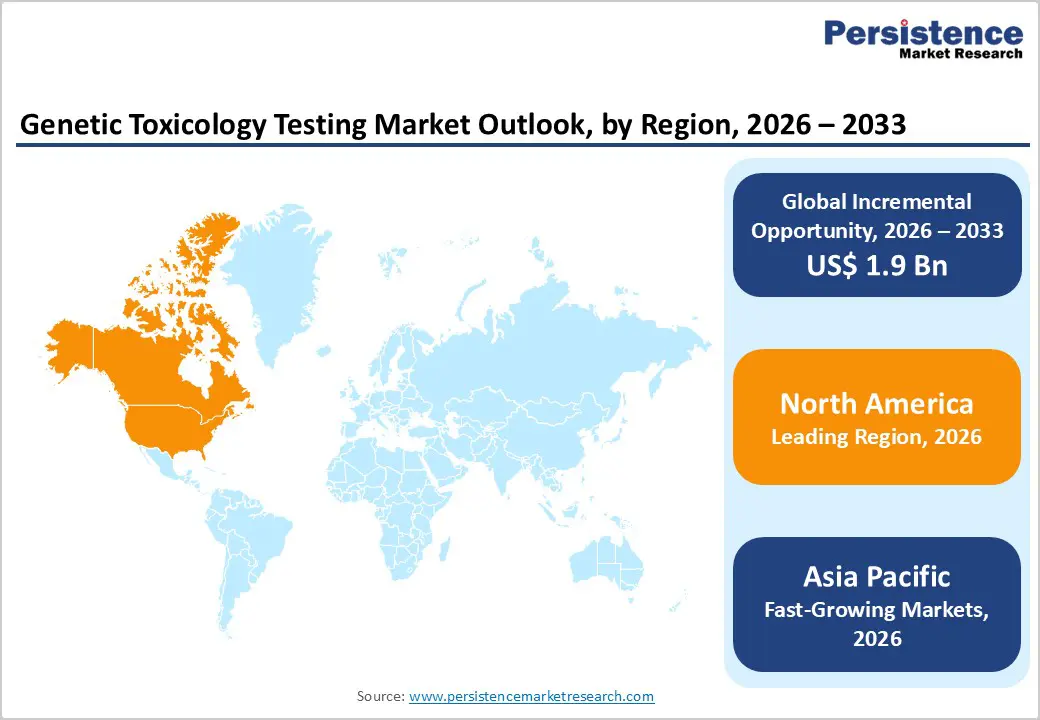

- Leading Region: North America holds the largest share at 48.3%, supported by strong regulatory oversight, advanced biopharmaceutical R&D infrastructure, widespread adoption of OECD-compliant testing guidelines, and early integration of genetic toxicology in drug development programs.

- Fastest-Growing Region: Asia Pacific is expanding the fastest due to rapid growth in pharmaceutical manufacturing, increasing outsourcing to regional CROs, improving regulatory harmonization, and rising investments in preclinical research infrastructure.

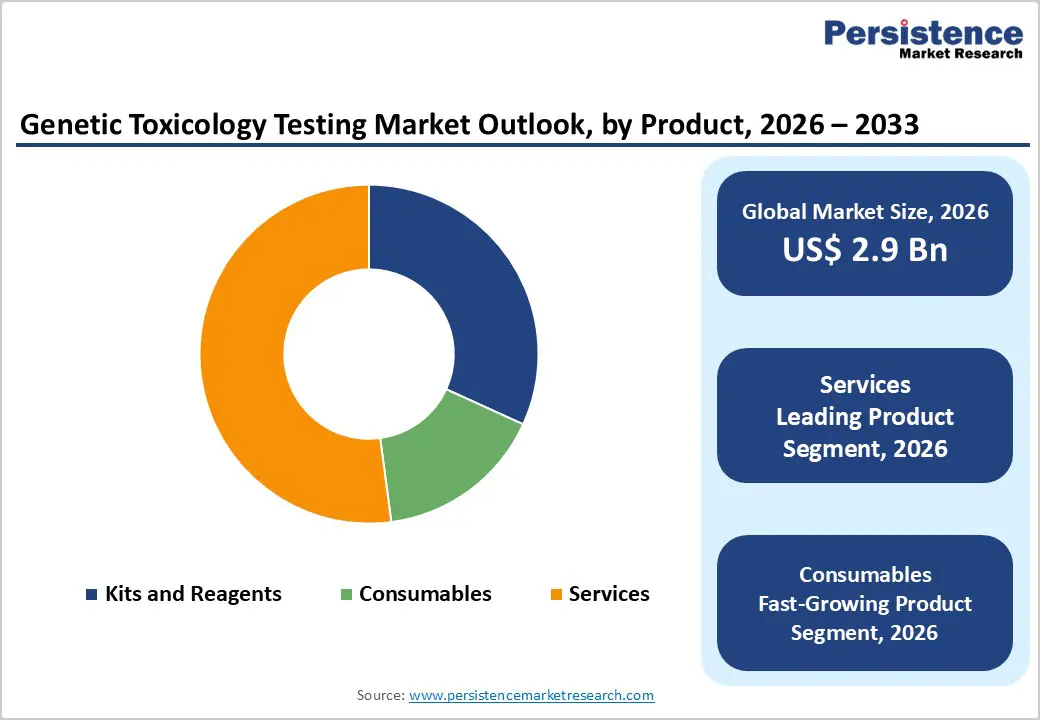

- Leading Product Segment: Services dominate the market due to extensive outsourcing of genetic toxicology studies, regulatory consulting, and integrated testing solutions across pharmaceutical, biotechnology, chemical, and cosmetic industries.

- Fastest-Growing Product Segment: Consumables are growing rapidly as rising testing volumes drive increased use of assay kits, reagents, cell lines, and laboratory supplies across routine and high-throughput genotoxicity testing workflows.

- Leading Type Segment: In vitro testing remains the leading segment, driven by regulatory preference for early-stage screening, cost efficiency, high throughput, and alignment with animal-reduction initiatives.

- Fastest-Growing Type Segment: In vivo testing is expanding steadily as confirmatory studies remain essential for regulatory approval, particularly for complex drug candidates, impurities, and risk-based safety evaluations.

| Key Insights | Details |

|---|---|

| Genetic Toxicology Testing Market Size (2026E) | US$ 2.9 Bn |

| Market Value Forecast (2033F) | US$ 4.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

Market Dynamics

Driver - Rising Disease Burden and Regulatory Stringency Accelerate Adoption of Genetic Toxicology Testing

The rising global burden of cancer, chronic diseases, and complex metabolic and neurological disorders is a major driver of demand for genetic toxicology testing, as these conditions fuel sustained growth in pharmaceutical and biotechnology R&D pipelines. Increasing oncology incidence, long-term chronic disease management, and the development of novel small molecules, biologics, and combination therapies require comprehensive genotoxicity evaluation to ensure patient safety. As drug candidates become more potent and structurally complex, regulators increasingly mandate early and robust assessment of mutagenicity, chromosomal damage, and DNA strand breaks. Genetic toxicology testing plays a critical role in identifying safety risks during discovery and preclinical development, reducing late-stage clinical failures and costly regulatory delays.

Additionally, technological advancements are strengthening adoption. High-throughput in vitro assays, improved cell-based models, and mechanism-driven genetic mutation tests are enabling faster, more predictive screening with reduced animal use. Automation, digital data capture, and AI-assisted interpretation are improving assay reproducibility and decision-making accuracy. These innovations allow sponsors to integrate genetic toxicology earlier in development workflows, supporting safer candidate selection and regulatory compliance. As regulatory agencies globally place greater emphasis on genotoxic impurity control, lifecycle safety assessment, and risk-based testing strategies, demand for advanced genetic toxicology testing continues to rise steadily.

Restraints - High Testing Costs and Regulatory Complexity Limit Market Expansion

The genetic toxicology testing market faces notable restraints related to cost intensity and regulatory complexity. Conducting compliant genetic toxicology studies requires GLP-certified laboratories, specialized instrumentation, validated assay platforms, and highly trained toxicologists. In vivo genotoxicity studies, in particular, involve significant time, ethical oversight, and financial investment. Even advanced in vitro assays require ongoing expenditure on reagents, consumables, quality controls, and data validation systems. For small and mid-sized pharmaceutical or biotechnology companies, maintaining in-house genetic toxicology capabilities can be cost-prohibitive, increasing dependence on external service providers and limiting flexibility.

Regulatory challenges further constrain market growth. Genetic toxicology requirements vary across regions, with differences in accepted test batteries, data expectations, and follow-up study requirements between the FDA, EMA, PMDA, and other agencies. Lack of full global harmonization leads to duplicated testing, longer development timelines, and higher overall costs. Additionally, evolving guidelines for genotoxic impurities, nitrosamines, and novel drug modalities require continuous method updates and regulatory interpretation. These complexities increase development risk and uncertainty, particularly for innovative compounds, potentially slowing market expansion despite growing underlying demand.

Opportunity - Expansion of Drug Pipelines and Innovation in Alternative Testing Create Strong Growth Potential

Significant opportunities are emerging in the genetic toxicology testing market due to expanding global drug pipelines and innovation in alternative and integrated testing strategies. The growth of oncology, rare disease, and advanced therapy pipelines is increasing the volume and diversity of compounds requiring genetic safety evaluation. Pharmaceutical companies are placing greater emphasis on early risk identification, creating opportunities for high-throughput screening, mechanism-based assays, and integrated testing approaches that combine multiple endpoints. These strategies help reduce late-stage failures while aligning with regulatory expectations for robust safety assessment.

Additionally, increasing regulatory and societal pressure to reduce animal testing is accelerating innovation in validated in vitro genetic toxicology models. Advanced human-relevant cell systems, 3D cultures, and computational toxicology tools are gaining traction as complementary or alternative approaches. Investment in automation, digital toxicology platforms, and AI-driven data analysis is improving scalability, cost efficiency, and predictive performance. Governments, academic institutions, and industry players are actively funding toxicology research and infrastructure development, particularly in emerging markets. As testing technologies evolve and global pharmaceutical development expands, genetic toxicology testing providers are well positioned to capture long-term growth opportunities across regulated industries.

Category-wise Analysis

By Product Insights

The services segment is projected to dominate the global genetic toxicology testing market in 2026, accounting for a significant revenue share of 52.1%. This leadership is driven by the growing outsourcing of genotoxicity assessments by pharmaceutical, biotechnology, chemical, and cosmetic companies to specialized testing providers. Genetic toxicology studies require GLP-compliant laboratories, regulatory expertise, validated assay platforms, and experienced toxicologists, prompting sponsors to rely on contract service providers rather than investing in in-house infrastructure. Services such as in vitro genotoxicity screening, in vivo follow-up studies, regulatory-compliant test batteries, and integrated risk assessment support faster development timelines and regulatory submissions. Increasing regulatory expectations from agencies such as the FDA, EMA, and OECD further reinforce demand for standardized third-party testing services. Additionally, rising small-molecule pipelines, biologics development, and impurity testing requirements are accelerating service adoption across early discovery, preclinical development, and post-approval safety monitoring.

By Application Insights

The pharmaceutical & biotechnology segment is expected to dominate the global genetic toxicology testing market in 2026 with a revenue share of 60.5%. This dominance is attributed to the critical role of genotoxicity testing in drug discovery, lead optimization, and regulatory approval processes. Genetic toxicology studies are mandatory for assessing mutagenic, clastogenic, and DNA-damaging potential of new chemical entities, biologics, and impurities before advancing into clinical trials. Increasing R&D investment, expansion of oncology and rare disease pipelines, and rising regulatory scrutiny on drug safety profiles are driving sustained testing demand. Pharmaceutical and biotech companies increasingly integrate genetic toxicology data early in development to reduce late-stage attrition and improve risk assessment accuracy. The growing adoption of in vitro assays, mechanism-based testing, and weight-of-evidence approaches further supports this segment’s leadership, reinforcing its central role in ensuring patient safety and regulatory compliance worldwide.

By End-user Insights

The pharmaceutical companies segment is projected to dominate the global genetic toxicology testing market in 2026, capturing a revenue share of 40.0%. Large pharmaceutical manufacturers generate high volumes of genetic toxicology testing due to extensive drug pipelines spanning small molecules, biologics, combination therapies, and impurities. These organizations typically maintain strong internal toxicology expertise, advanced screening capabilities, and long-term partnerships with contract research organizations to manage complex study requirements. Genetic toxicology testing is integrated across multiple development stages, including candidate selection, regulatory filings, and lifecycle safety monitoring. High testing frequency, repeat studies for formulation changes, and impurity profiling contribute to sustained demand from pharmaceutical companies. Additionally, increasing focus on regulatory alignment, quality assurance, and global submission strategies strengthens reliance on robust genetic safety data, reinforcing pharmaceutical companies’ position as the leading end-user segment globally.

Regional Insights

North America Genetic Toxicology Testing Market Trends

North America is expected to maintain global dominance in the genetic toxicology testing market with a market share value of 48.3%, supported by its strong regulatory framework, advanced life sciences infrastructure, and high concentration of pharmaceutical and biotechnology companies. The United States leads the region due to stringent FDA safety requirements, widespread adoption of OECD-compliant test guidelines, and early integration of genetic toxicology in drug development workflows. A large number of GLP-certified laboratories, CROs, and academic research centers enable rapid execution of in vitro and in vivo genotoxicity studies.

Increasing R&D investments, expansion of oncology and rare disease pipelines, and growing focus on impurity and nitrosamine testing are driving consistent testing demand. The region also benefits from advanced automation, digital toxicology platforms, and data-driven risk assessment tools that improve study efficiency and regulatory predictability. Strong collaboration between industry, regulators, and research institutions continues to support North America’s leadership in genetic toxicology testing.

Europe Genetic Toxicology Testing Market Trends

Europe represents a mature and steadily growing market for genetic toxicology testing, supported by well-established regulatory standards, strong academic research networks, and widespread compliance with EMA and OECD testing guidelines. Countries such as Germany, the U.K., France, Italy, Switzerland, and the Nordic region play a central role in regional market growth due to their concentration of pharmaceutical manufacturers and contract research organizations.

The region places a strong emphasis on safety evaluation, mechanistic toxicology, and alternative testing strategies, driving adoption of advanced in vitro assays and integrated testing approaches. Increasing regulatory scrutiny of genotoxic impurities, cosmetic ingredients, and food additives further strengthens demand. European initiatives promoting the reduction of animal testing have accelerated innovation in validated in vitro genetic toxicology models. Additionally, strong public-private research collaborations and government funding for toxicology research continue to enhance testing capabilities, supporting sustained market expansion across Europe.

Asia Pacific Genetic Toxicology Testing Market Trends

Asia Pacific is projected to be the fastest-growing region in the genetic toxicology testing market, registering a CAGR of 8.3%, driven by rapid expansion of pharmaceutical manufacturing, rising clinical research activity, and improving regulatory alignment with global standards. Countries such as China, Japan, South Korea, India, and Singapore are investing heavily in preclinical research infrastructure, GLP-certified laboratories, and CRO capabilities. Increasing outsourcing of genetic toxicology studies by global pharmaceutical companies to cost-efficient regional service providers is accelerating market growth.

Rising domestic drug development, growing generics and biosimilars pipelines, and stricter regulatory oversight of drug safety are further boosting testing demand. Governments across the region are strengthening toxicology guidelines and encouraging the adoption of standardized genotoxicity testing protocols. Expanding healthcare investments, skilled scientific workforce availability, and growing participation in global drug development programs continue to position Asia Pacific as a high-growth market.

Competitive Landscape

The global genetic toxicology testing market is highly competitive, with strong participation from companies such as Thermo Fisher Scientific Inc., Charles River Laboratories International, Inc., Eurofins Scientific, SGS Société Générale de Surveillance SA, and Inotiv. These players leverage broad toxicology service portfolios, advanced in vitro and in vivo genotoxicity platforms, validated assay systems, and extensive regulatory and preclinical expertise to strengthen their global market presence. Increasing regulatory scrutiny across pharmaceuticals, biotechnology, chemicals, food additives, and cosmetics is driving sustained demand for robust genetic safety evaluation.

Market participants are increasingly focusing on advanced assay technologies, including high-throughput in vitro genotoxicity tests, integrated testing strategies (ITS), and mechanistic genetic mutation and DNA damage assays to improve predictivity and regulatory acceptance. Strategic priorities include expanding GLP-compliant laboratory infrastructure, enhancing automation and digital data management, strengthening regulatory consulting capabilities, and forming collaborations with pharmaceutical companies and academic research institutes to support early-stage screening, regulatory submissions, and long-term market growth.

Key Industry Developments:

- In September 2024, Scantox, together with its majority owner Impilo, completed the acquisition of Gentronix Ltd, a UK-based GLP-compliant genetic toxicology CRO. Gentronix is widely recognized for its high-quality genetic toxicology services and strong scientific expertise, serving a broad global client base. The acquisition significantly expands Scantox Group’s service capabilities, strengthening its position as a leading CRO supporting pre-IND enabling studies.

- In August 2024, Lhasa Limited announced a major enhancement to Sarah Nexus with the launch of a new chromosome damage prediction model. The added module enables comprehensive in silico genotoxicity assessment by integrating mutagenicity and chromosome damage predictions within a single platform. Built using curated in vitro and in vivo data from the Vitic database and Lhasa member contributions, the model provides reliable, transparent predictions to support confident genetic toxicity risk evaluation.

- In April 2024, Merck launched the industry’s first all-in-one validated genetic stability assay. The Aptegra CHO genetic stability assay combines whole genome sequencing with advanced bioinformatics to accelerate biosafety testing and support faster progression of clients’ programs into commercial production.

Companies Covered in Genetic Toxicology Testing Market

- Thermo Fisher Scientific Inc.

- Charles River Laboratories International, Inc.

- Eurofins Scientific

- SGS Société Générale de Surveillance SA

- Inotiv

- MB Research Laboratories

- Gentronix

- Syngene International Limited

- Creative Bioarray

- Toxys

- XENOMETRIX AG

- KOREA INSTITUTE OF TOXICOLOGY

- Nelson Laboratories, LLC

- CompareNetworks, Inc.

- Others

Frequently Asked Questions

The global genetic toxicology testing market is projected to be valued at US$ 2.9 Bn in 2026.

Growing adoption of targeted and controlled drug-delivery systems to improve therapeutic efficacy and reduce systemic toxicity are driving the global injectable nanomedicines market.

The global genetic toxicology testing market is poised to witness a CAGR of 6.1% between 2026 and 2033.

Expanding use of nanomedicine platforms in oncology, rare diseases, and personalized injectable therapies are creating opportunities in the market.

Thermo Fisher Scientific Inc., Charles River Laboratories International, Inc, Eurofins Scientific, SGS Société Générale de Surveillance SA, and Inotiv are some of the key players in the genetic toxicology testing market.