- Biotechnology

- Neurogenetic Testing Market

Neurogenetic Testing Market Size, Share, and Growth Forecast, 2026 - 2033

Neurogenetic Testing Market by Test Type (Predictive Testing, Carrier Testing, Diagnostic Testing, Pharmacogenetic Testing, Preimplantation Testing), End-User (Hospitals & Clinics, Research Institutes, Pharmaceutical Companies, Diagnostic Laboratories, Academic Institutions), Technology (SNP-based Testing, WES, WGS, NGS, Microarray), and Regional Analysis for 2026 - 2033

Neurogenetic Testing Market Share and Trends Analysis

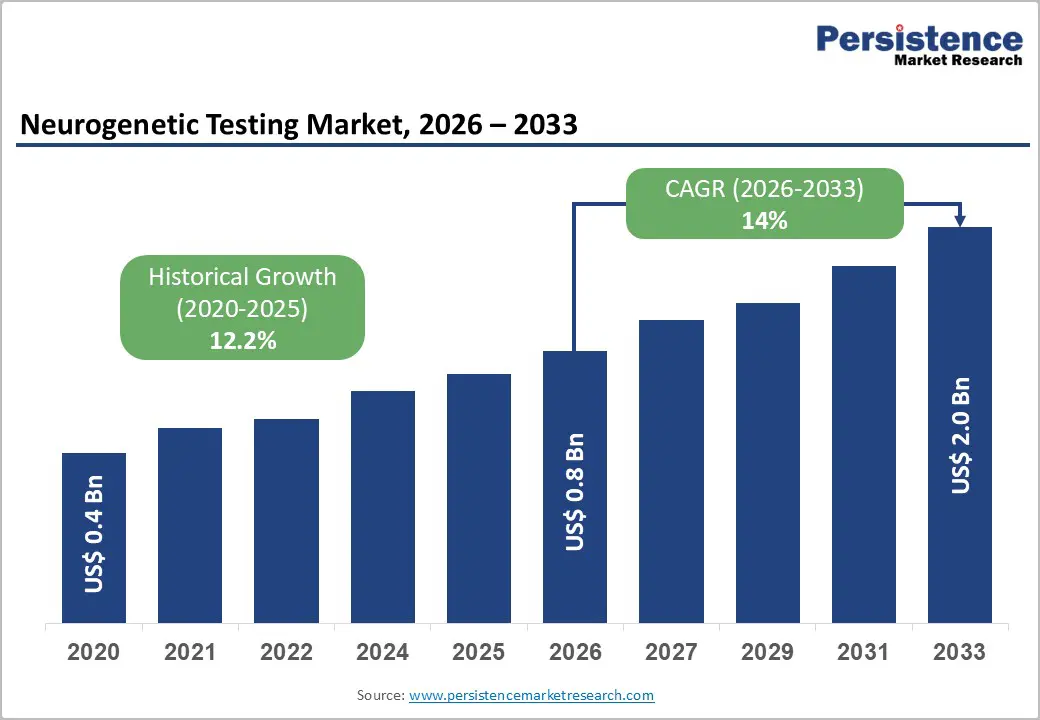

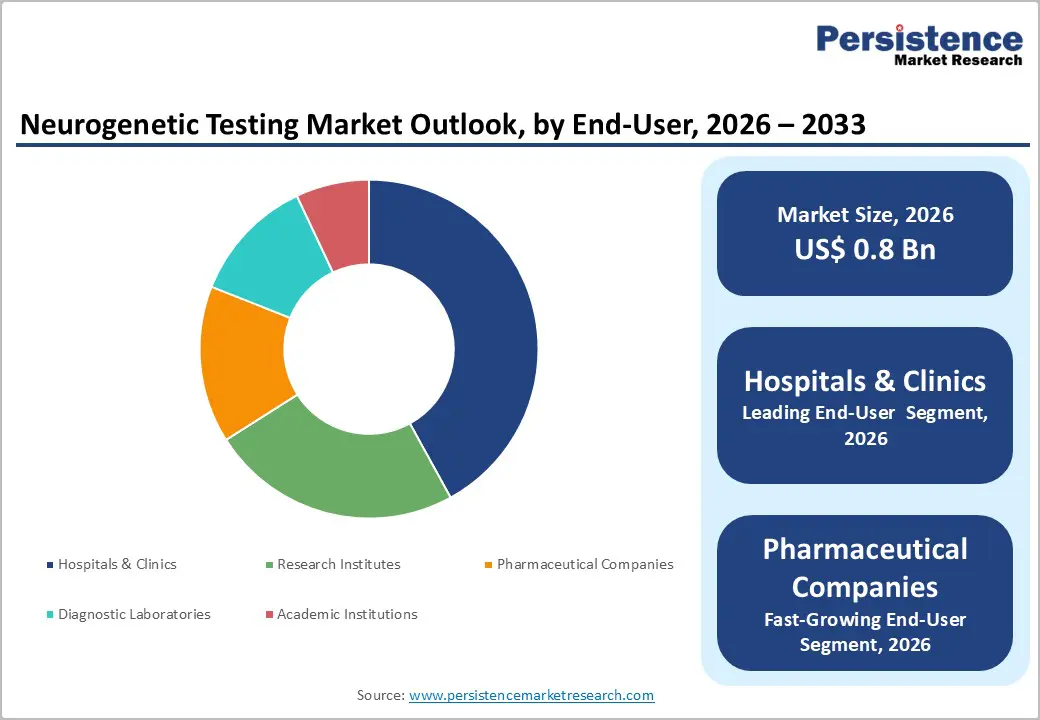

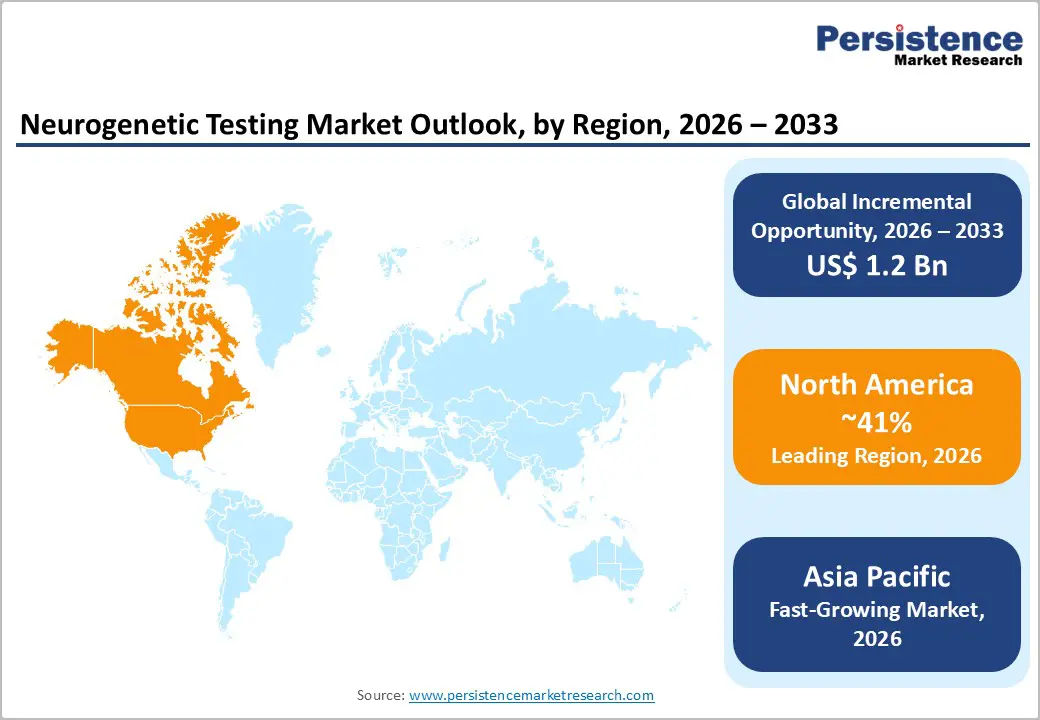

The global neurogenetic testing market size is likely to be valued at US$ 0.8 billion in 2026, and is projected to reach US$ 2.0 billion by 2033, growing at a CAGR of 14% during the forecast period 2026 - 2033.

Increasing prevalence of neurological diseases, deeper clinical integration of genetic diagnostics, and ongoing improvements in genomic infrastructure are brightening market prospects. Growth in diagnosed cases of neurodegenerative and inherited neurological disorders reinforces the clinical relevance of genetic testing across neurology care pathways. Enhanced laboratory capacity, standardized sequencing workflows, and advanced bioinformatics integration further support scalable deployment across healthcare systems. Population aging across developed and emerging economies increases exposure to age-associated and hereditary neurological conditions, thereby structurally expanding the patient base. This demographic transition directly elevates demand for early-stage risk assessment, precise molecular diagnosis, and informed clinical decision-making.

Key Industry Highlights

- Dominant Region: North America is projected to hold an estimated 41% market share in 2026, driven by precision medicine integration and high adoption of molecular diagnostics.

- Fastest-growing Market: Asia Pacific is expected to be the fastest-growing market from 2026 to 2033, due to widening awareness of neurological conditions and increasing adoption of advanced genomic diagnostics.

- Leading End-User: Hospitals and clinics are projected to command nearly 42% of the market revenue share in 2026, supported by centralized diagnostic workflows and strong patient trust.

- Fastest-growing End-User: Pharmaceutical companies are forecasted to be the fastest-growing segment from 2026 to 2033, fueled by skyrocketing drug development needs.

| Key Insights | Details |

|---|---|

| Neurogenetic Testing Market Size (2026E) | US$ 0.8 Bn |

| Market Value Forecast (2033F) | US$ 2.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 14% |

| Historical Market Growth (CAGR 2020 to 2025) | 12.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Neurological and Neurodevelopmental Disorders

Demographic aging, extended life expectancy, and enhanced disease surveillance continue to increase the diagnosed incidence of neurological and neurodevelopmental conditions across multiple regions. Neurodegenerative and inherited disorders such as Parkinson disease, Alzheimer disease, Huntington disease, inherited neuropathies, and epilepsy exhibit strong genetic associations, reinforcing the clinical relevance of molecular diagnostics. Epilepsy affects around 50 million people worldwide, as of 2023 estimates, positioning it among the most common neurological disorders globally, and a substantial proportion of cases demonstrate identifiable genetic contributors. Health policy frameworks issued by national neurological institutes and public health departments increasingly prioritize early diagnosis, risk stratification, and precision care planning to reduce long-term disability and institutional care burden.

Expansion of newborn screening programs and pediatric neurology initiatives further strengthens demand by enabling early identification of inherited neurological and neurodevelopmental disorders. These initiatives align with public health recommendations focused on reducing lifetime disability-adjusted disease burden and improving functional outcomes through early intervention. Early molecular confirmation supports timely therapeutic decision-making, anticipatory care planning, and informed family counseling, thereby improving continuity of care across neurology, rehabilitation, and supportive services. Pediatric genetic diagnosis also contributes to more efficient allocation of healthcare resources by preventing delayed diagnosis and inappropriate treatment pathways.

Ethical, Regulatory, and Data Governance Constraints

Rapid expansion of genomic testing capabilities and increasing integration of neurogenetic diagnostics in clinical practice create complex ethical, regulatory, and data governance challenges. Patient genomic information is highly sensitive, requiring strict protocols for collection, storage, sharing, and analysis. Variability in international regulations governing genetic data, consent procedures, and reporting standards introduces operational complexities for laboratories and healthcare providers. Inconsistent regulatory frameworks across regions can delay test approval, limit cross-border research collaboration, and increase compliance costs. Concerns over potential misuse of genetic data, including unauthorized access, discrimination in employment or insurance, and privacy breaches, heighten scrutiny from regulatory authorities and public stakeholders, constraining widespread adoption.

Data governance requirements further impose significant operational and technological burdens. Establishing secure bioinformatics infrastructure, implementing robust encryption and anonymization protocols, and ensuring traceable data handling practices demand substantial investment from testing providers. Compliance with evolving legal frameworks, such as national genetic information acts or international data protection regulations, requires continuous monitoring and procedural updates. The need for informed consent documentation, clear communication of potential risks, and patient education adds administrative layers that can slow clinical deployment.

Advancements in Genomic Technologies

Integration of advanced genomic technologies is transforming neurogenetic diagnostics by increasing analytical depth, accuracy, and efficiency. High-throughput sequencing platforms, including next-generation sequencing (NGS) and whole-exome sequencing (WES), allow comprehensive evaluation of complex neurological gene panels with reduced turnaround times. Sophisticated bioinformatics tools support interpretation of large genomic datasets, enabling identification of pathogenic variants and clinically actionable mutations with high precision. Automation in sample processing and data analysis minimizes operational errors, reduces costs, and improves laboratory throughput, enhancing patient access. Integration of multi-omics approaches, including transcriptomics and epigenomics, provides deeper insights into disease mechanisms, enabling early detection and refined diagnostic stratification.

Expansion of genomic infrastructure also drives research, therapeutic development, and clinical adoption. High-resolution sequencing and advanced computational analysis facilitate the discovery of novel biomarkers and genetic variants associated with neurological disorders, supporting the development of targeted therapies. Cloud-based and collaborative data platforms enable longitudinal studies and real-world evidence generation across regions, fostering diagnostic innovation. Cost-effective, scalable genomic workflows increase accessibility in both developed and emerging healthcare systems. Improved accuracy and reproducibility strengthen clinician confidence and regulatory acceptance, supporting integration into standard care pathways.

Category-wise Analysis

Test Type Insights

Diagnostic testing is anticipated to secure around 38% of the neurogenetic testing market share in 2026, reflecting strong clinical reliance on genetic confirmation for neurological disorders. Neurologists increasingly require molecular validation to differentiate phenotypically similar conditions and establish definitive diagnoses, particularly for complex or rare neurodegenerative and inherited disorders. Diagnostic testing provides critical support for treatment planning, prognosis assessment, and patient counseling, enabling more informed clinical decision-making.

Growing awareness among healthcare providers regarding the value of early and accurate genetic confirmation reinforces preference for these tests. The diagnostic testing benefits from both clinical trust and measurable impact on patient management outcomes.

Pharmacogenetic testing is expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by precision therapy adoption. Neurological treatments increasingly demonstrate genotype-dependent efficacy and adverse event profiles, making pharmacogenetic insights essential for personalized therapy. Clinicians leverage these insights to optimize drug selection, dosing, and treatment schedules, thereby improving efficacy while reducing the risk of toxicity.

Growth is driven by rising adoption of targeted therapeutics, integration of genetic testing in clinical trial design, and regulatory encouragement of precision medicine initiatives. Expanding awareness among healthcare providers and inclusion in post-market surveillance programs further accelerate segment growth.

End-User Insights

Hospitals and clinics are poised to dominate with a forecasted market share of approximately 42% in 2026, powered by centralized diagnostic workflows and patient trust. Tertiary care hospitals serve as primary referral centers for complex neurological cases, handling high patient volumes that require advanced diagnostic capabilities. Integration of neurology, genetics, and laboratory services within hospital networks streamlines adoption of neurogenetic testing. Centralized reporting, standardized protocols, and dedicated genetic counseling services improve operational efficiency and clinician confidence. Patient trust in hospital-led diagnostics and direct access to multidisciplinary expertise reinforce preference for institutional testing over decentralized or standalone laboratory services.

Pharmaceutical companies are estimated to be the fastest-growing segment from 2026 to 2033, fueled by drug development requirements. Neurogenetic testing enables precise patient stratification, biomarker identification, and therapy optimization during both clinical trials and post-market evaluation. Pharmaceutical pipelines targeting neurological disorders are expanding, increasing demand for genetic profiling at various stages of research and development. Testing facilitates the identification of responder populations, the monitoring of adverse effects, and the tailoring of therapeutic regimens to genetic subtypes. Integration of neurogenetic insights enhances trial efficiency, accelerates drug development timelines, and strengthens regulatory submissions for targeted neurological therapies.

Technology Insights

Next-generation sequencing is likely to be the leading application segment with a projected 45% of the neurogenetic testing market revenue share in 2026 due to scalability and clinical credibility. NGS enables simultaneous analysis of multiple genes, allowing detection of single-nucleotide variants, insertions, deletions, and copy number variations with high accuracy and throughput. Laboratories benefit from standardized workflows, reduced manual intervention, and automation, which enhance efficiency and reproducibility. Clinicians rely on NGS for precise molecular characterization of complex neurological disorders, guiding diagnosis, prognosis, and therapeutic planning.

Whole genome sequencing is anticipated to be the fastest-growing application segment from 2026 to 2033, driven by declining costs and advances in interpretation. WGS enables analysis of the entire genomic landscape, providing comprehensive insight into coding and non-coding regions that contribute to complex neurological disorders. Advanced bioinformatics pipelines and artificial intelligence tools enhance the interpretation of large-scale genomic data, supporting the discovery of rare and novel variants. Clinical and research adoption is increasing as WGS improves understanding of disease mechanisms, enables identification of genotype-phenotype correlations, and facilitates precision medicine strategies for individualized patient care.

Regional Insights

North America Neurogenetic Testing Market Trends

By 2026, North America is expected to lead with an estimated 41% of the neurogenetic testing market share, supported by advanced healthcare infrastructure and precision medicine integration. High prevalence of neurodegenerative and inherited neurological conditions among aging populations creates a substantial patient base for genetic diagnostics. Centralized sequencing laboratories, automated bioinformatics pipelines, and robust clinical networks enable rapid, high-throughput testing with reliable accuracy.

Healthcare providers increasingly utilize molecular diagnostics for early intervention, differential diagnosis, and personalized treatment planning. Established reimbursement frameworks and insurance coverage reduce financial barriers, facilitating widespread clinical adoption. Collaboration between academic institutions, tertiary care centers, and commercial laboratories accelerates test development, validation, and clinical translation, reinforcing sustained leadership in adoption.

Strong regulatory and clinical ecosystems further strengthen the market dominance of North America. Standardized diagnostic guidelines and predictable approval pathways streamline the introduction of new testing technologies. High clinician awareness of genotype-phenotype correlations in neurological disorders drives preference for molecular confirmation over conventional methods. Population-scale screening initiatives, including pediatric and high-risk adult programs, expand early detection and establish long-term testing pipelines.

Integration of electronic health records with genomic data platforms supports care coordination, longitudinal monitoring, and outcome tracking. Targeted research funding in neuroscience and precision medicine fuels discovery of novel biomarkers and therapeutic approaches, maintaining continuous demand for neurogenetic testing.

Europe Neurogenetic Testing Market Trends

Europe represents a strategically significant market for neurogenetic testing, combining advanced healthcare infrastructure with strong regulatory oversight and high clinical adoption rates. Established networks of tertiary hospitals and specialized neurology centers support integration of molecular diagnostics into routine care pathways. Widespread implementation of NGS and targeted gene panels enables precise identification of pathogenic variants, improving diagnosis, prognosis, and treatment planning for neurodegenerative and inherited neurological disorders.

Aging populations, coupled with increasing awareness of neurological disease burden among healthcare providers, create a structurally expanding patient base. National public health initiatives and insurance coverage policies facilitate access to testing, ensuring consistent adoption across key countries.

Research and innovation also reinforce Europe’s market relevance. Significant investment in neuroscience research, precision medicine programs, and collaborative consortia accelerates discovery of novel biomarkers and genotype-phenotype correlations. Regulatory frameworks, such as the European Union (EU) In Vitro Diagnostic Regulation (IVDR), establish clear guidelines for validation, safety, and clinical reporting, enhancing trust among clinicians and patients. Integration of bioinformatics infrastructure with electronic health records (EHRs) allows seamless clinical implementation, longitudinal monitoring, and multi-center data sharing. Growth of pharmacogenetic testing and companion diagnostics further expands the clinical application spectrum, linking genetic insights to therapeutic optimization.

Asia Pacific Neurogenetic Testing Market Trends

Asia Pacific is forecast to be the fastest-growing market for neurogenetic testing between 2026 and 2033, driven by expanding healthcare infrastructure and rising neurological awareness. Rising prevalence of neurodegenerative and inherited neurological conditions, driven by population aging and improved disease recognition, creates a structurally expanding patient base for genetic diagnostics. Investments in centralized laboratory networks, automation, and digital sample logistics enable high-throughput testing with reduced turnaround times. Integration of molecular diagnostics into tertiary hospitals, specialized clinics, and reference laboratories supports adoption across urban and semi-urban healthcare settings. Strategic collaborations between academic institutions, hospitals, and diagnostic providers facilitate technology transfer, training, and deployment of NGS and WGS platforms, accelerating clinical uptake.

Government initiatives promoting early diagnosis, preventive care, and pediatric screening further reinforce adoption, particularly for inherited neurological conditions that require early intervention. Rising clinician awareness of genotype-guided treatment strategies strengthens adoption of neurogenetic testing across care pathways. Declining sequencing costs and growing affordability improve access in both metropolitan and regional centers. Expansion of pharmaceutical R&D in neurological therapeutics drives demand for pharmacogenetic and companion diagnostic testing, while cloud-based data platforms and standardized reporting protocols enhance multi-center research and translational applications. Focused regulatory frameworks and public health strategies supporting precision medicine further accelerate integration.

Competitive Landscape

The global neurogenetic testing market structure exhibits moderate fragmentation, with a mix of large multinational diagnostic companies and specialized regional laboratories maintaining meaningful market positions. Leading players such as Illumina, Thermo Fisher Scientific, F. Hoffmann-La Roche, and Agilent Technologies leverage advanced genomic platforms and integrated service models to capture substantial revenue share. Investment in high-throughput sequencing technologies, automated workflows, and bioinformatics solutions enables these companies to deliver accurate and reproducible results at scale. Their strong brand recognition, established client networks, and ongoing research collaborations enhance credibility among healthcare providers and research institutions.

Competitive dynamics in the market emphasize precision, turnaround time, and regulatory compliance as key differentiators. Rapid and reliable testing, supported by standardized laboratory protocols and quality assurance frameworks, remains critical for customer retention and market expansion. Companies invest in continuous product development, assay optimization, and regulatory certification to meet evolving clinical requirements and reimbursement standards. Strategic partnerships with hospitals, academic centers, and pharmaceutical organizations enable co-development of targeted tests and companion diagnostics, extending commercial reach.

Key Industry Developments

- In November 2025, a Filipino neuroscientist unveiled a pioneering neurogenetics program to combat rising early-onset stroke rates by bringing advanced genetic research into patient care at a major medical center, aiming to establish the country’s first neurogenetics laboratory within a Department of Health hospital.

- In September 2025, UniQure's AMT-130 gene therapy slowed Huntington's disease progression by 75% at 36 months on the composite Unified Huntington's Disease Rating Scale and 60% on functional abilities in Phase I/II trials for early manifest patients. The company plans to submit an FDA marketing application in early 2026.

- In February 2025, University of Florida researchers identified a novel genetic mutation linked to increased Alzheimer’s risk that could improve diagnosis and unlock new therapeutic pathways by revealing toxic protein buildup mechanisms in the brain.

Companies Covered in Neurogenetic Testing Market

- Illumina, Inc.

- Thermo Fisher Scientific Inc.

- F. Hoffmann-La Roche Ltd

- Agilent Technologies

- QIAGEN

- BGI

- Eurofins Scientific

- Natera, Inc.

- PacBio

- Labcorp

Frequently Asked Questions

The global neurogenetic testing market is projected to reach US$ 0.8 billion in 2026.

Rising prevalence of neurological disorders, integration of precision medicine, and advancements in genomic technologies drive the market.

The market is poised to witness a CAGR of 14% from 2026 to 2033.

Expansion of personalized medicine, early diagnostic programs, and adoption of advanced genomic technologies represent key market opportunities.

Some of the key market players include Illumina, Inc., Thermo Fisher Scientific Inc., Agilent Technologies, and F. Hoffmann-La Roche Ltd.