- Medical Devices

- Genetic Testing Market

Genetic Testing Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Genetic Testing Market by Technology Type (Next Generation Sequencing, Array Technology, PCR-based Testing, FISH, Others), by Application (Ancestry & Ethnicity, Traits Screening, Genetic Disease Carrier Status, New Baby Screening, Health and Wellness-Predisposition/Risk/Tendency), by End-user, by Regional Analysis, from 2026 - 2033

Genetic Testing Market Share and Trends Analysis

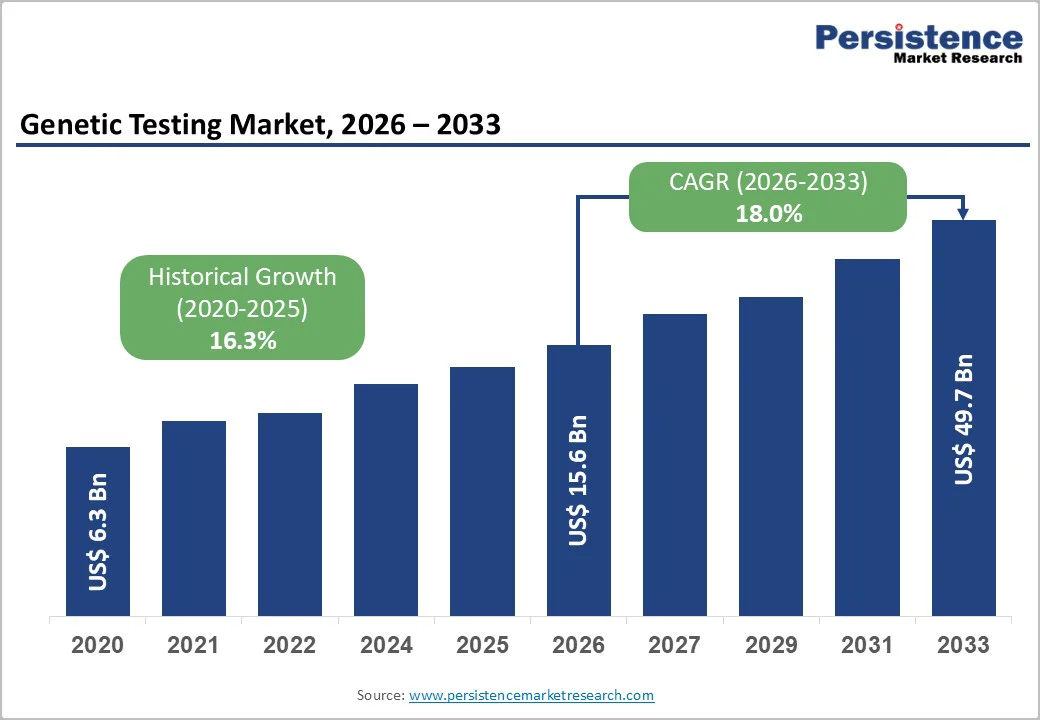

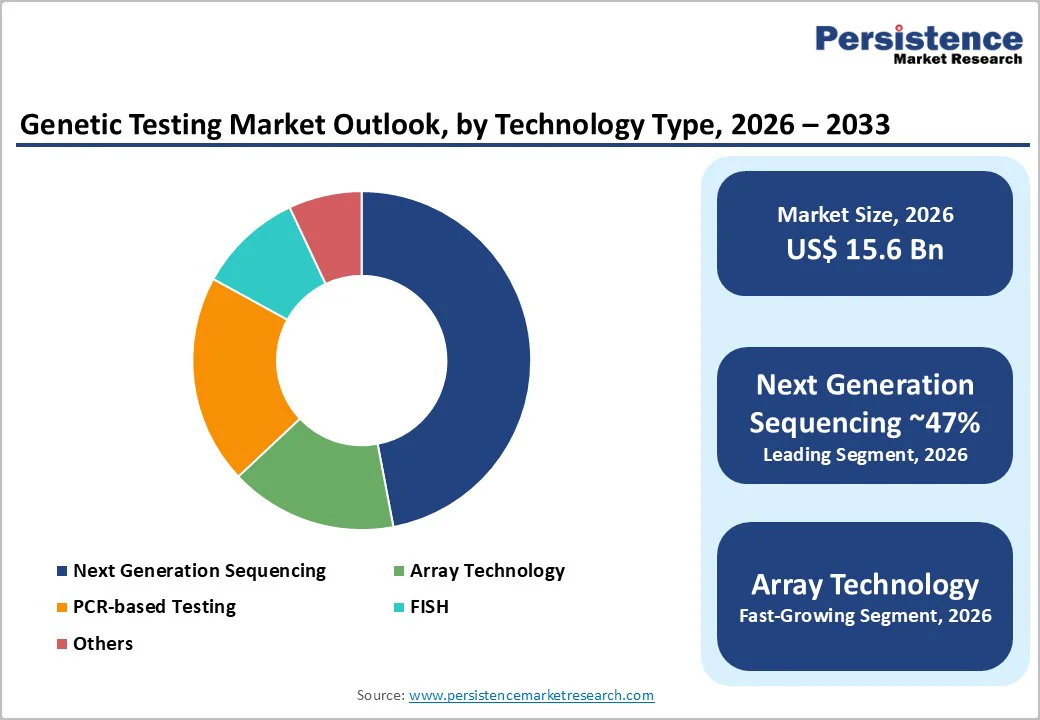

The global genetic testing market size is estimated to grow from US$15.6 billion in 2026 to US$49.7 billion by 2033, growing at a CAGR of 18.0% during the forecast period from 2026 to 2033. The global healthcare market is experiencing robust growth, driven by technology’s exceptional capabilities, including high accuracy, scalability, and versatility in analyzing DNA to provide health and ancestry insights.

Genetic testing, encompassing technologies such as next-generation sequencing (NGS), array technologies, PCR-based testing, and fluorescence in situ hybridization (FISH), is increasingly adopted across diverse applications, including ancestry and ethnicity, carrier status for genetic diseases, newborn screening, health and wellness, and trait screening.

The genetic testing market is expanding due to rising demand for personalized medicine in sectors such as oncology, reproductive health, and preventive care, alongside advancements in genomic technologies and personalized healthcare applications, including genome testing and gene analysis.

Key Industry Highlights:

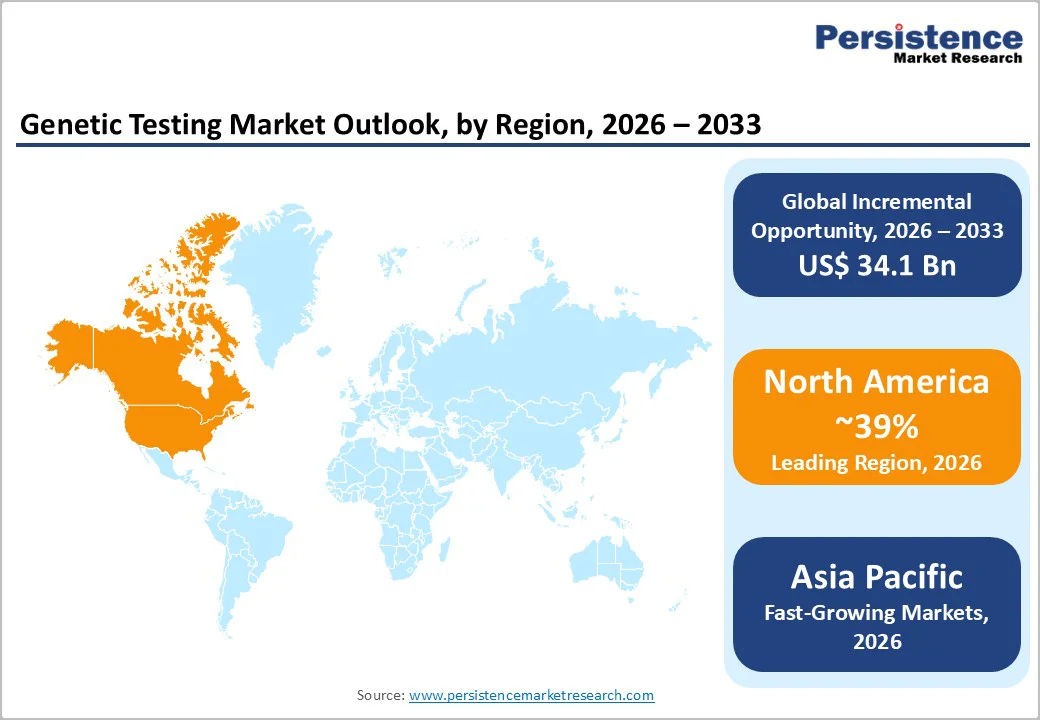

- Leading Region: North America remains the largest genetic testing market, driven by advanced healthcare infrastructure, high public awareness, and strong integration of genomics into clinical practice.

- Fastest Growing Region: Asia Pacific is expected to grow at the quickest pace, supported by government initiatives, rising healthcare access, and increasing adoption of genetic testing in China, India, and Japan.

- Dominant Segment: Next-Generation Sequencing (NGS) holds the largest share due to its scalability, high-throughput capabilities, and widespread use in oncology, reproductive health, and rare disease diagnostics.

- Fastest Growing Segment: Array Technology represents the fastest-growing segment, fueled by its ability to analyze multiple genetic markers simultaneously and the rising demand in both research and diagnostic applications.

| Key Insights | Details |

|---|---|

|

Genetic Testing Market Size (2026E) |

US$15.6 Bn |

|

Market Value Forecast (2033F) |

US$49.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

18.0% |

|

Historical Market Growth (CAGR 2020 to 2024) |

16.3% |

Market Dynamics

Driver - Genetic Testing Market Growth Fueled by Advanced Capabilities, Expanding Applications, and Increasing Healthcare Demand

The technology’s unique capabilities and expanding applications are boosting the market. The genetic testing market is experiencing robust growth driven by the technology’s exceptional capabilities and increasing range of applications. Genetic testing enables precise identification of genetic variations, mutations, and predispositions, making it ideal for advanced applications across diverse sectors.

Its use is expanding in health and wellness, new baby screening, genetic disease carrier status, ancestry and ethnicity, and traits screening, where accurate and scalable diagnostics are crucial. For instance, according to MedlinePlus (an NIH/NLM service), newborn screening "can identify genetic disorders early in life so treatment can be started as early as possible, "leading to better management and outcomes. As industries pursue personalized and preventive healthcare solutions, genetic testing offers significant advantages over traditional diagnostics.

The healthcare industry’s rapid growth is fueling demand for genetic testing. Due to their high accuracy and ability to analyze complex genetic data, genetic testing technologies are integral to developing personalized medicine, early disease detection, and ancestry insights. As per the World Health Organization (WHO), global health expenditure in 2022 was approximately US$9.8 trillion, reflecting the comprehensive scale of global healthcare services, including infrastructure, diagnostics, and therapeutics.

Restraints - High Costs and Regulatory Challenges Restraining the Genetic Testing Market

The genetic testing market faces significant restraints due to the high costs of advanced testing technologies. Next-generation sequencing (NGS) and other cutting-edge genetic tests involve expensive equipment, specialized labor, and complex data analysis, making them less accessible in cost-sensitive regions. Limited insurance coverage for these tests further burdens patients and healthcare providers financially.

As a result, widespread adoption in areas such as rare disease diagnosis, hereditary testing, and pharmacogenomics is constrained, despite the clinical benefits and potential of personalized medicine. Operational costs, including laboratory infrastructure and ongoing maintenance, also contribute to slower market penetration in emerging and mid-income regions.

In addition to financial challenges, regulatory and privacy concerns significantly impact market growth. Strict regulations, especially Europe’s General Data Protection Regulation (GDPR), increase compliance costs by 10–15% and require investments in secure data management systems.

Privacy concerns related to direct-to-consumer genetic testing discourage approximately 20% of potential users, particularly in privacy-sensitive regions such as Europe and North America. These regulatory and ethical considerations limit market expansion, as companies must balance innovation with legal compliance and consumer trust, slowing adoption despite increasing demand for personalized healthcare solutions.

Opportunity - Opportunities in the Genetic Testing Market through AI Integration, Digital Health Solutions, and Public-Private Partnerships

The genetic testing market is witnessing significant opportunities through the integration of digital health solutions. AI-driven platforms and cloud-based data analytics are transforming the field by enhancing diagnostic accuracy and streamlining patient monitoring. For example, AI platforms developed by companies like Illumina have been shown to improve result precision by up to 25% while reducing turnaround times by 30%.

These technologies enable remote access to test results, allowing timely interventions and personalized care, particularly in critical areas such as oncology and prenatal screening. Additionally, integration with electronic health records (EHRs) optimizes patient management, improves diagnostic efficiency, and supports better outcomes in personalized medicine across global healthcare systems.

Public-private partnerships also present substantial growth opportunities for the genetic testing market. Collaborations between private companies and government healthcare institutions, such as Myriad Genetics’ 2023 partnership with a hospital network, have enhanced diagnostic infrastructure in high-growth regions.

These partnerships have improved the accuracy of oncology testing by 20% and extended access to over one million previously undiagnosed individuals. By combining industry expertise with public resources, such initiatives advance precision medicine goals set by organizations like the WHO, supporting sustainable healthcare solutions. Such collaborations are particularly impactful in emerging markets, where access to advanced genetic testing and diagnostics is limited, driving both adoption and market expansion globally.

Category-wise Analysis

By Technology Insights

Next-generation sequencing (NGS) dominates the global genetic testing market, accounting for approximately 47% of the market share in 2025. Its capability to analyze thousands of genes simultaneously at reduced costs has revolutionized testing in oncology, rare diseases, and reproductive health. NGS-based tumor sequencing allows comprehensive profiling of actionable mutations, guiding targeted therapies and immuno-oncology treatments, while whole-exome sequencing improves diagnostic accuracy in children with suspected rare genetic disorders. Increased investments in large-scale genomic projects and biobanks, along with broader availability of NGS panels in hospital laboratories worldwide, strengthen its leadership over traditional PCR and array-based methods.

NGS leads due to its scalability, high-throughput processing, and suitability for extensive genetic analyses, making it widely adopted in sectors such as oncology, reproductive health, and wellness testing. Meanwhile, array technology is the fastest-growing method, as it can analyze multiple genetic markers simultaneously. Despite higher operational complexity, array technology is increasingly used in both research and diagnostic applications, supporting its rapid adoption in emerging markets.

By Application Insights

In the genetic testing market, the Health and Wellness–Predisposition/Risk/Tendency segment is the leading application, accounting for approximately 52% of total demand in 2025. This segment benefits from strong consumer interest in personalized health insights, particularly in preventive care. Direct-to-consumer genetic tests provide information on cardiometabolic risk, pharmacogenomic traits, nutrition response, and fitness markers, often combined with ancestry and trait analysis in a single report.

As individuals increasingly focus on proactive health management and lifestyle optimization, demand for these tests is rising, especially in regions with high internet penetration and widespread smartphone use. Regulatory guidance on health claims and access to genetic counseling are further supporting the integration of wellness-focused tests into primary care and corporate wellness programs, reinforcing the segment’s market leadership.

Newborn and prenatal screening represents the fastest-growing application within the genetic testing market. Rising awareness of early detection benefits and government initiatives promoting newborn screening programs are driving demand. This growth is particularly notable in emerging regions, where improved healthcare infrastructure and funding support expansion in early-life genetic diagnostics.

By End-user Insights

Hospitals and clinics are the leading end-user sector in the genetic testing market, estimated to account for around 41% of the market share in 2026. Their dominance is driven by the integration of genetic testing into routine healthcare, the adoption of personalized treatment plans, and the development of complex diagnostic workflows. Applications include oncology diagnostics, pharmacogenomics, prenatal screening, and rare disease identification. Academic medical centers and tertiary hospitals often serve as hubs for these genomic programs, supported by in-house molecular pathology laboratories or partnerships with specialized diagnostic centers.

Clinical guidelines from oncology societies and professional bodies increasingly recommend germline and somatic genetic testing to guide treatment decisions and assess family risk, further boosting test volumes within hospital settings. The integration of genomic data into electronic health records and multidisciplinary tumor boards enhances clinical decision-making, positioning hospitals and clinics as a critical channel for high-complexity and reimbursed genetic services.

Diagnostic laboratories are the fastest-growing end-user segment. Their growth is driven by advancements in high-throughput testing, specialized genetic analysis capabilities, and rising demand for outsourced genetic testing services from hospitals, research institutes, and direct-to-consumer providers, particularly in emerging markets.

Region-wise Insights

North America Genetic Testing Market Trends

North America maintains a dominant position in the global genetic testing market, led primarily by the U.S. This leadership is supported by advanced healthcare infrastructure, high public and professional awareness, and the strong integration of genomic testing into standard medical practice. Genetic testing is extensively incorporated into clinical workflows for oncology, prenatal care, pharmacogenomics, and rare disease diagnostics. Support from healthcare providers and insurance coverage further facilitates widespread adoption, making testing more accessible across both urban and specialized healthcare centers.

Technological advancements are a key driver of the market in North America. Innovations in next-generation sequencing (NGS), non-invasive prenatal testing (NIPT), and AI-assisted data interpretation are improving the accuracy, speed, and efficiency of genetic testing. These technologies enable clinicians to make more informed decisions and deliver personalized care effectively. Additionally, there is a notable surge in consumer-driven demand for direct-to-consumer genetic testing. Services offering ancestry, wellness, and health risk insights are increasingly popular, reflecting growing public interest in preventive medicine and personalized healthcare solutions.

This combination of clinical adoption, technological progress, and consumer demand continues to reinforce North America’s leading role in the genetic testing market.

Asia and Pacific Genetic Testing Market Trends

The Asia Pacific genetic testing market is experiencing rapid growth, driven by strong government initiatives, rising public health awareness, and advancements in biotechnology. China leads the region, supported by large-scale national programs such as the China Precision Medicine Initiative. Government backing, coupled with investments in research and biotechnology, is accelerating the adoption of genetic testing, particularly in oncology and reproductive health, enabling early diagnosis and targeted therapies.

In India, expanding public health awareness and government schemes like Ayushman Bharat are improving access to affordable genetic testing. The increasing focus on prenatal screening, early detection of genetic disorders, and personalized healthcare is driving adoption across both urban and rural areas. India’s growing healthcare infrastructure and rising disposable income further support market growth.

Japan’s market is fueled by innovations in personalized medicine and a mature pharmaceutical sector. Strategic investments by local and global biotech companies are enhancing the availability of genetic testing services in areas such as wellness, hereditary conditions, and preventive care. Strong research capabilities and integration of advanced diagnostics into healthcare systems position Japan as a key contributor to the regional market expansion.

Competitive Landscape

The global genetic testing market is highly competitive, with companies dominating through extensive product portfolios and global distribution networks. Players such as Illumina and 23andMe invest heavily in R&D to develop advanced genetic testing platforms, such as AI-integrated genome testing solutions. Collaborations with healthcare providers, as seen with Myriad Genetics’ hospital partnerships, enhance market penetration in high-prevalence regions. Companies such as Mapmygenome are expanding in Asia Pacific through localized manufacturing and distribution.

Key Industry Developments:

- In October 2025, a hospital in Hyderabad, India, introduced a genetic test that helps doctors determine the most effective medicines for patients.

- In July 2025, MedLife plans to launch Romania’s first large-scale genetic testing program, expanding access to advanced genomic diagnostics nationwide.

- In October 2024, Illumina, Inc., a global leader in DNA sequencing and array-based technologies, launched its MiSeq™ i100 Series sequencing systems, offering exceptional benchtop speed and ease of use to enhance next-generation sequencing (NGS) capabilities for laboratories.

- In October 2024, EpiMedTech Global launched epiGeneComplete, a clinical-grade NGS test combining DNA methylation and SNP markers to deliver comprehensive, highly accurate insights into aging, stress, metabolism, inflammation, and addiction risk.

Companies Covered in Genetic Testing Market

- 24 genetics

- Circle DNA

- Tellmegen

- 23andMe

- AncestryDNA

- MyDNA, Everly Well

- Igenomix

- VitaGen

- Myriad Genetics, Inc.

- Mapmygenome

- Helix OpCo LLC

- MyHeritage Ltd.

- Illumina, Inc.

- Amgen, Inc.

- Others

Frequently Asked Questions

The global genetic testing market is projected to be valued at US$ 15.6 Bn in 2026.

Rising global demand for personalized medicine, advancements in genomic technologies, and increasing consumer awareness of health and wellness testing are the key market drivers.

The global market is expected to witness a CAGR of 18.0% between 2026 and 2033.

Integration of digital health solutions, public-private partnerships, and expansion in emerging markets are the key market opportunities.

North America is the leading region in the global genetic testing market.