- Automotive Components & Materials

- Gear Box Housing Market

Gear Box Housing Market Size, Share, and Growth Forecast, 2026 - 2033

Gear Box Housing Market by Product Type (Manual Gear Box Housing, Automatic Gear Box Housing, Others), Material Type (Aluminum Gear Box Housing, Cast Iron Gear Box Housing, Steel Gear Box Housing, Others), and Regional Analysis for 2026 - 2033

Gear Box Housing Market Size and Trends Analysis

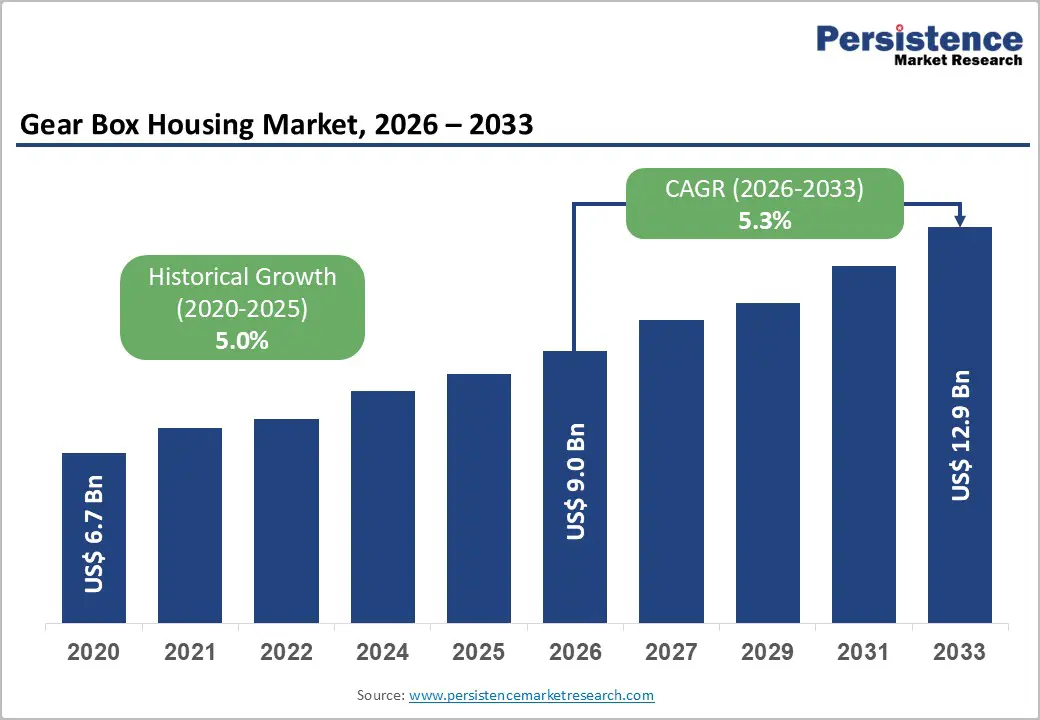

The global gear box housing market size is likely to be valued at US$9.0 billion in 2026 and is expected to reach US$12.9 billion by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033, driven by increasing vehicle production, rising demand for advanced transmission systems including manual, automatic, CVT, DCT, and electric gear boxes and expanding applications across industrial machinery, aerospace, marine, and railway sectors.

The adoption of lightweight and high-strength materials such as aluminum and magnesium alloys, which enhance fuel efficiency and EV performance, and advancements in precision manufacturing technologies such as CNC machining and additive manufacturing. The growth of electric and hybrid vehicles is creating demand for specialized gear box housings that accommodate compact motor integrations and high-torque requirements.

Key Industry Highlights:

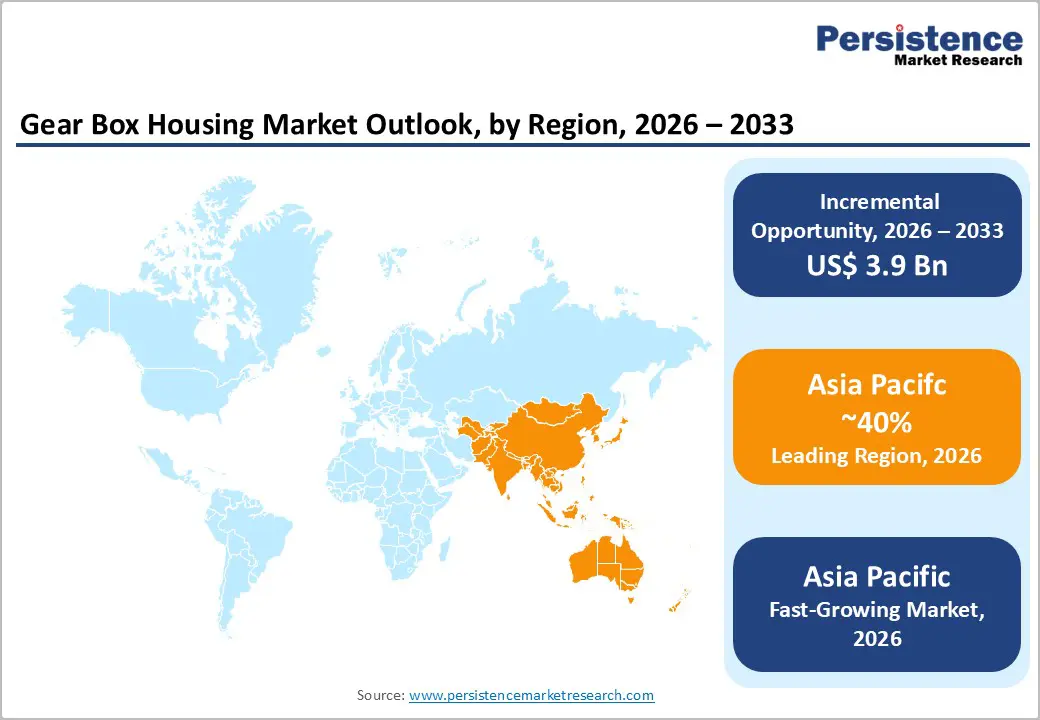

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by high vehicle production, rapid industrialization, growing adoption of electric and hybrid vehicles, supportive government policies, and strong manufacturing capabilities.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in the gear box housing in 2026, supported by rapid urbanization, rising middle-class vehicle ownership, expanding EV adoption, and robust automotive and industrial manufacturing capabilities across China, Japan, India, and ASEAN nations.

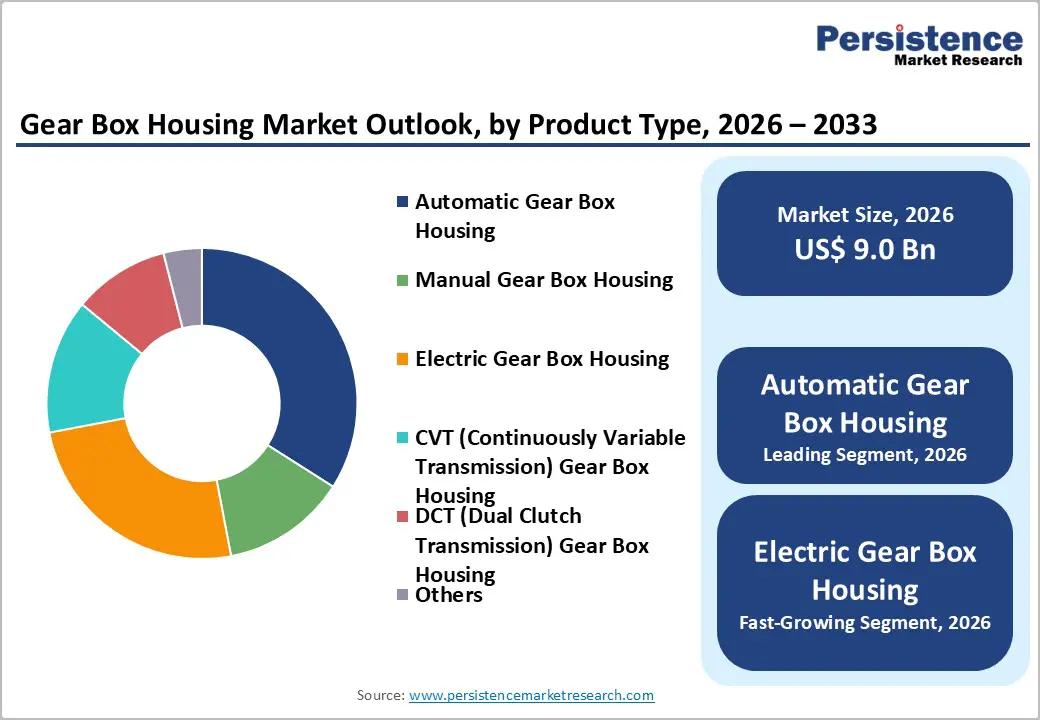

- Leading Product Type: Automatic gear box housings are projected to represent the leading product type in 2026, accounting for 45% of the revenue share, driven by rising consumer preference for convenience, widespread adoption in mid- to high-end vehicles, and improvements in transmission efficiency.

- Leading Material Type: Cast iron gear box housings are anticipated to be the leading material type, accounting for over 45% of the revenue share in 2026, supported by their durability, excellent vibration damping, and cost efficiency in heavy-duty applications.

| Key Insights | Details |

|---|---|

| Gear Box Housing Market Size (2026E) | US$9.0 Bn |

| Market Value Forecast (2033F) | US$12.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis

Increasing Vehicle Production and Automotive Electrification

Expanding automotive manufacturing, especially in regions such as Asia Pacific, Europe, and North America, increases demand for both traditional and electric transmission systems. Passenger cars, commercial vehicles, and SUVs require durable gear box housings to support smooth and reliable performance. Concurrently, the electrification of vehicles is reshaping market requirements, as electric motors demand specialized housings capable of handling high torque and thermal loads. This dual growth, conventional production, and EV adoption ensure sustained revenue expansion and support investments in innovative housing designs.

Electrification drives volume growth and transforms gear box housing design. EVs, hybrids, and plug-in hybrids require compact, lightweight housings to integrate motor assemblies efficiently. Manufacturers are leveraging aluminum and magnesium alloys to reduce weight while maintaining structural integrity. Increasing EV sales in China, Europe, and India, coupled with supportive policies, accelerate adoption rates. Aftermarket demand grows with rising vehicle ownership. The combination of high production volumes and the shift toward electrified powertrains positions the market for long-term growth, providing opportunities for manufacturers to innovate, scale operations, and meet evolving automotive requirements.

Advancements in Transmission Technologies and Regulatory Push for Efficiency

Technological advancements in transmissions, including CVT, DCT, and automated manual systems, are driving the gear box housing market. Modern transmissions require precise, durable housings to support complex gear arrangements and ensure optimal performance. Regulatory mandates for fuel efficiency and lower emissions accelerate the adoption of advanced designs, particularly in Europe, North America, and Asia Pacific. Governments incentivize lightweight, energy-efficient components, encouraging OEMs to invest in high-performance gear box housings. These regulatory pressures not only ensure compliance but also enhance overall vehicle efficiency.

The push for efficiency also drives the integration of smart technologies into gear box housings. Sensors for predictive maintenance, temperature monitoring, and torque control are increasingly embedded into housings, aligning with regulatory and consumer expectations for reliability. Advanced manufacturing techniques such as precision CNC machining, casting, and additive manufacturing support complex geometries and lightweight construction. These technological improvements reduce energy loss and improve drivetrain efficiency. The emphasis on emission reduction through regulatory policies accelerates the replacement of conventional components with advanced housings.

Barrier Analysis

Shift to Simplified EV Transmissions Limiting Traditional Housing Demand

Unlike conventional transmissions, many EVs utilize simplified or single-speed gear systems that require fewer housing components. As automakers increasingly adopt these designs to reduce cost, weight, and complexity, the demand for conventional multi-gear housings declines. Markets heavily investing in EVs, such as China and Europe, may see a gradual reduction in traditional housing revenue. Manufacturers dependent on conventional gear box designs must adapt, as decreasing component requirements for EVs could impact production volumes, limiting growth opportunities for traditional housing types across the automotive sector.

Simplified EV transmissions reduce the number of required housings and favor integrated motor-housing units, minimizing separate part demand. This structural shift challenges suppliers of conventional aluminum or cast iron housings, potentially affecting profit margins. The focus on modular, lightweight, and compact EV assemblies requires redesigns and innovation investment. Aftermarket replacement demand for traditional gear boxes may decline over time as EV penetration grows, creating long-term constraints.

Complexity of Advanced Designs and Margin Pressure from Alternative Technologies

Advanced gear box housings, particularly for high-performance and hybrid systems, are complex to design and manufacture. Precision casting, CNC machining, and lightweight alloys increase production costs and require significant capital investment. Suppliers face challenges in maintaining profitability due to rising raw material prices, labor costs, and stringent quality standards. Alternative transmission technologies, such as integrated EV powertrains and simplified modular designs, exert competitive pressure, limiting traditional revenue streams. The intricacy of meeting diverse automotive specifications across regions adds engineering and operational burdens.

The demand for lightweight, high-strength, and thermally resistant housings adds technical challenges, as small deviations can affect performance and safety. Continuous innovation is required to support CVT, DCT, and EV-specific designs, requiring R&D investment. Simultaneously, competition from low-cost regional manufacturers intensifies pricing pressure. Suppliers must balance performance, durability, and cost-efficiency, often leading to margin erosion. Customer expectations for shorter lead times and higher customization exacerbate operational challenges. The complexity of advanced gear box housings and pressures from alternative technologies constrain profitability and require strategic planning to sustain market participation.

Opportunity Analysis

Rising Adoption of Electric and Hybrid Gear box Housings

The accelerating adoption of electric and hybrid vehicles presents a significant growth opportunity for gear box housing manufacturers. Unlike traditional gear boxes, EV and hybrid housings require specialized designs to accommodate high torque, compact motors, and thermal management systems. Regulatory support for low-emission vehicles, coupled with EV adoption targets, drives increasing demand for these components. OEMs seek lightweight, durable, and thermally efficient housings, creating opportunities for material innovation and precision manufacturing. This growing market segment allows suppliers to expand product portfolios, enter new regions, and cater to emerging EV ecosystems.

Innovations in aluminum, magnesium alloys, and composite materials enable housings that are lighter yet structurally robust, aligning with energy efficiency targets. Strategic partnerships between automotive manufacturers and specialized housing suppliers enhance market access. With EV sales increasing rapidly in Asia Pacific, Europe, and North America, the adoption of electric and hybrid gear box housings offers long-term growth potential. Companies investing in R&D, advanced manufacturing, and lightweight solutions are well-positioned to capitalize on this fast-growing segment.

Technological Convergence and Lightweight Innovations

Technological convergence, combining lightweight materials, advanced manufacturing, and smart embedded systems, provides a key opportunity in the gear box housing market. Aluminum, magnesium, and composite housings reduce vehicle weight while maintaining strength, enhancing fuel efficiency, and EV performance. Integration of sensors and predictive maintenance technologies enables smarter housings, supporting vehicle safety and durability. Precision manufacturing and additive techniques allow complex designs, improved thermal management, and shorter production cycles.

Lightweight innovations improve vehicle efficiency and support electrification by reducing energy consumption and extending battery range. Manufacturers adopting these technologies can create modular, high-performance housings compatible with multiple transmission types, including EVs, hybrids, CVTs, and DCTs. The combination of lightweight materials and embedded technology reduces maintenance costs and enhances reliability, increasing aftermarket potential. As automotive and industrial applications demand higher performance with lower environmental impact, suppliers investing in technological convergence and lightweight solutions are positioned to capture a larger market share, driving sustainable growth and creating long-term competitive advantages.

Category-wise Analysis

Product Type Insights

Automatic gear box housing is expected to lead the gear box housing market, accounting for approximately 45% of revenue in 2026, driven by growing consumer preference for convenience in passenger vehicles and commercial applications, as well as widespread adoption in mid- to high-end models that prioritize smooth shifting and fuel efficiency. For example, Toyota’s Camry and Honda Accord, popular mid-range sedans, utilize automatic transmissions requiring robust housings to ensure durability and precise gear alignment. These housings provide structural support, protect internal gears from wear, and improve overall transmission efficiency.

Electric gear box housing is likely to represent the fastest-growing segment in 2026, supported by the rapid proliferation of electric vehicles and the need for specialized designs to handle instant torque. This segment is projected to grow significantly above the industry average, reflecting rising EV adoption, stringent regulatory emission targets, and advancements in battery and motor technology. For example, Tesla’s Model 3 uses an electric gear box housing engineered to accommodate high-torque electric motors while ensuring thermal management and structural stability. Unlike conventional housings, EV housings must integrate cooling systems and withstand higher power density, prompting manufacturers to innovate in lightweight materials such as aluminum alloys.

Material Type Insights

Cast iron gear box housings are expected to dominate the market, accounting for approximately 45% of the revenue share by 2026. This is due to their exceptional mechanical strength, durability, and superior vibration and noise damping properties. These characteristics make cast iron ideal for heavy-duty applications, including automotive transmissions, industrial machinery, construction equipment, and rail systems, where gear boxes endure continuous loads and tough operating conditions. For instance, ZF continues to use cast iron housings in its heavy-duty and rail drivetrain solutions, where reliability, long service life, and low lifecycle costs are crucial factors for both operators and OEMs.

Composite material gear boxes are projected to be the fastest-growing material type by 2026, fueled by the industry's shift toward lighter, more energy-efficient, and advanced mobility solutions. Though still holding a smaller share compared to traditional materials, composites are gaining traction due to their ability to significantly reduce overall system weight while providing excellent corrosion resistance and design flexibility. For example, Siemens Mobility has explored advanced composite and hybrid material solutions for drivetrain and mobility components, aiming to support lightweight designs and next-generation transportation systems, further strengthening the growth prospects for this material segment.

Regional Insights

North America Gear Box Housing Market Trends

North America is likely to be a significant market for gear box housing in 2026, driven by its well-established automotive and industrial manufacturing sectors that emphasize quality, durability, and technological innovation. The region benefits from high vehicle production levels, particularly in the United States, where demand for automatic transmissions and pickup trucks sustains strong adoption of robust gear box housings. For example, Magna Powertrain Inc., a key North American transmission systems supplier that provides engineered drivetrain components, including transmission housings for major automakers such as General Motors and Ford, underpins advanced drivetrain development and housing innovation.

Emerging trends in the North America gear box housing market reflect both evolving automotive powertrain strategies and industrial modernization. Electrification remains a key trend as OEMs shift toward hybrid and electric vehicles, promoting demand for lightweight, thermally efficient housings tailored to electric motors and integrated powertrain units. Legacy internal combustion engine demand persists, with companies adjusting production strategies to balance traditional and EV-related components. The rise of advanced manufacturing technologies such as automated machining, inline quality testing, and digital metrology systems enables greater precision and customization in housing components, reducing waste and enhancing performance reliability.

Europe Gear Box Housing Market Trends

Europe is likely to be a significant market for gear box housing in 2026, due to its long-standing automotive and industrial manufacturing excellence and a regulatory environment that emphasizes energy efficiency and emissions reduction. For example, Graziano Trasmissioni, an Italian specialist in precision transmission components, supplies advanced gear box units and housings for high-performance vehicles from McLaren and Ferrari, highlighting the region’s focus on precision engineering and premium segments.

Emerging trends in the Europe gear box housing market reflect the region’s evolving automotive landscape and industrial modernization efforts. A growing shift toward electrification is accelerating demand for specialized housings that integrate seamlessly with electric powertrains, particularly as EV sales grow across Germany, the UK, and France under supportive policy frameworks. European manufacturers focus on light weighting, digital manufacturing methods, and advanced casting technologies to deliver housings that meet rigorous performance and sustainability standards.

Asia Pacific Gear Box Housing Market Trends

The Asia Pacific region is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by rapid vehicle production, expanding industrial sectors, and robust manufacturing ecosystems in China, India, Japan, and Southeast Asia. Asia Pacific’s thriving automotive industry, bolstered by a growing middle class and urbanization, drives consistent demand for gear box housings across passenger cars, commercial vehicles, and increasingly in electric and hybrid powertrains.

Within this dynamic environment, key regional players are capitalizing on growth opportunities by enhancing production capacity and innovation. For example, JATCO Ltd., a Japan-based transmission specialist with significant operations in China and Thailand, has expanded its presence in Asia Pacific to support strong demand for automatic and CVT gear box housings tailored to both conventional and electrified vehicles. JATCO’s strategic facilities in Guangzhou and Suzhou reflect localized manufacturing that aligns with rising vehicle production and export demand.

Competitive Landscape

The global gear box housing market exhibits a moderately fragmented structure, driven by the presence of both large multinational manufacturers and numerous specialized regional suppliers competing for share through product innovation, quality, and geographic reach. Players in the market are increasingly investing in R&D to develop lightweight, durable, and efficient gear box housings tailored to evolving applications such as electric vehicles, industrial machinery, and aerospace, while also expanding manufacturing capacities in high-growth regions such as Asia Pacific to capitalize on rising demand.

With key leaders including Roop Automotives, Premier, Hindustan Auto Equipment, IG Watteeuw, Avtec, KOMET, CIE Automotive, IDC Industries, Birken Manufacturing, and Lancereal, the competitive landscape reflects a mix of established players and niche participants focused on specialized applications. These players compete through innovation in materials and manufacturing processes, expanding their product portfolios, strengthening distribution networks, and forming strategic collaborations that enhance their ability to serve diverse end markets.

Key Industry Developments:

- In March 2025, Stagnoli launched the Spinyx worm gear box, a high-performance technopolymer solution that offers a lightweight, low-maintenance alternative to traditional gear boxes. It features a one-piece composite body, FDA and EU food-contact certification, 40% weight reduction, P69 protection, and noiseless operation, making it ideal for industrial applications.

- In October 2025, ZF unveiled a new rail gear box at IREE 2025, designed for Indian railways. The single-stage spur gear drive features a sphero cast housing, compact design, and delivers high efficiency and durability. It’s engineered for axle loads up to 17 tons and speeds of up to 180 km/h, deployed in high-speed trains like the Vande Bharat Express.

- In February 2024, NGC launched two advanced wind energy gear boxes for onshore and offshore turbines. The 10MW and 20MW gear boxes feature high torque density, reduced vibration, and innovations to minimize oil leakage, improving maintenance efficiency for large-scale clean energy projects.

Companies Covered in Gear Box Housing Market

- Roop Automotives

- Premier

- Hindustan Auto Equipment

- IG Watteeuw

- Avtec

- KOMET

- CIE Automotive

- IDC Industries

- Birken Manufacturing

- Lancereal

Frequently Asked Questions

The global gear box housing market is projected to reach US$9.0 billion in 2026.

The gear box housing market is driven by increasing vehicle production, rising adoption of electric and hybrid vehicles, and demand for advanced, lightweight, and durable transmission components.

The gear box housing market is expected to grow at a CAGR of 5.3% from 2026 to 2033.

Key market opportunities lie in the growing adoption of electric and hybrid vehicle gear boxes, technological innovations in lightweight and high-performance housings, and expansion in industrial and renewable energy applications.

Roop Automotives, Premier, Hindustan Auto Equipment, IG Watteeuw, Avtec, and KOMET are the leading players.