- Medical Devices

- Functional Endoscopic Sinus Surgery Market

Functional Endoscopic Sinus Surgery Market Size, Share, and Growth Forecast, 2025 - 2032

Functional Endoscopic Sinus Surgery Market By Product Type (Endoscopes, Powered Surgical Instruments), Procedure Type (Traditional, Image-Guided FESS), Indication (Allergic Fungal Sinusitis, Others), End-user (Hospitals, Others), and Regional Analysis for 2025 - 2032

Functional Endoscopic Sinus Surgery Market Size and Trends Analysis

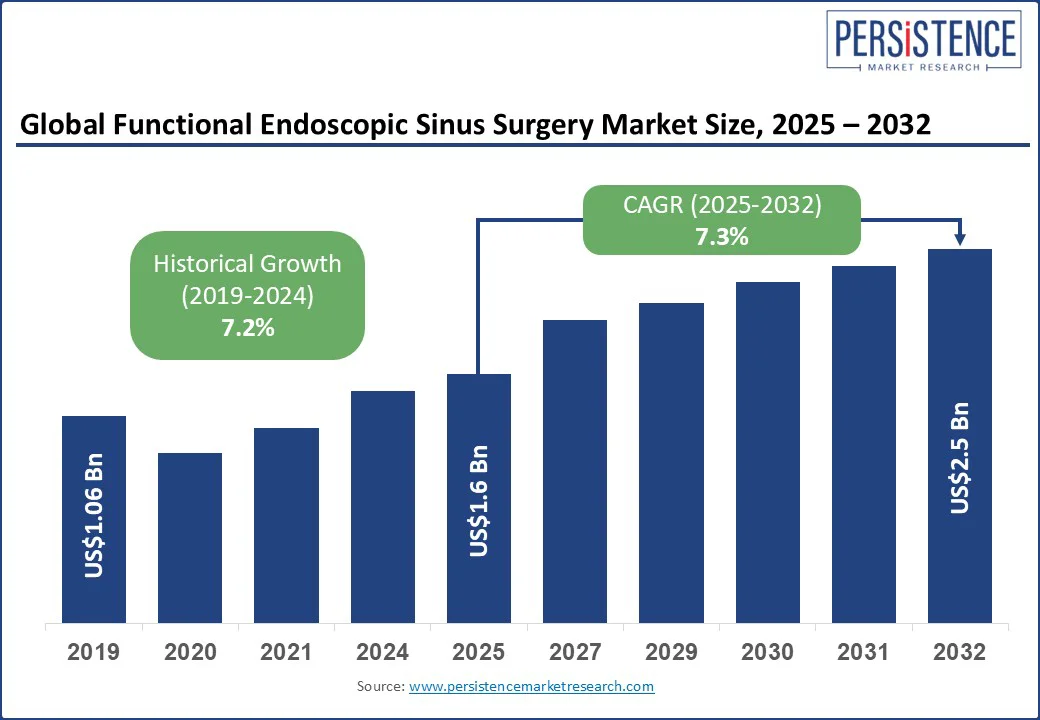

The global functional endoscopic sinus surgery market size is likely to value at US$ 1.6 Bn in 2025 to US$ 2.5 Bn by 2032, growing at a CAGR of 7.3% during the forecast period from 2025 to 2032. The Functional Endoscopic Sinus Surgery (FESS) market is experiencing steady growth, driven by increasing incidence of chronic sinusitis and a global shift toward minimally invasive surgical procedures.

Technological advancements such as high-definition imaging, navigation systems, and robotic assistance are enhancing surgical precision and outcomes. The demand for outpatient ENT procedures is rising, driven by shorter recovery times and lower healthcare costs. The growing awareness of sinus-related disorders and improved access to ENT care are expanding the patient pool. Emerging markets are also contributing to growth through improved healthcare infrastructure and specialist availability.

Key Industry Highlights:

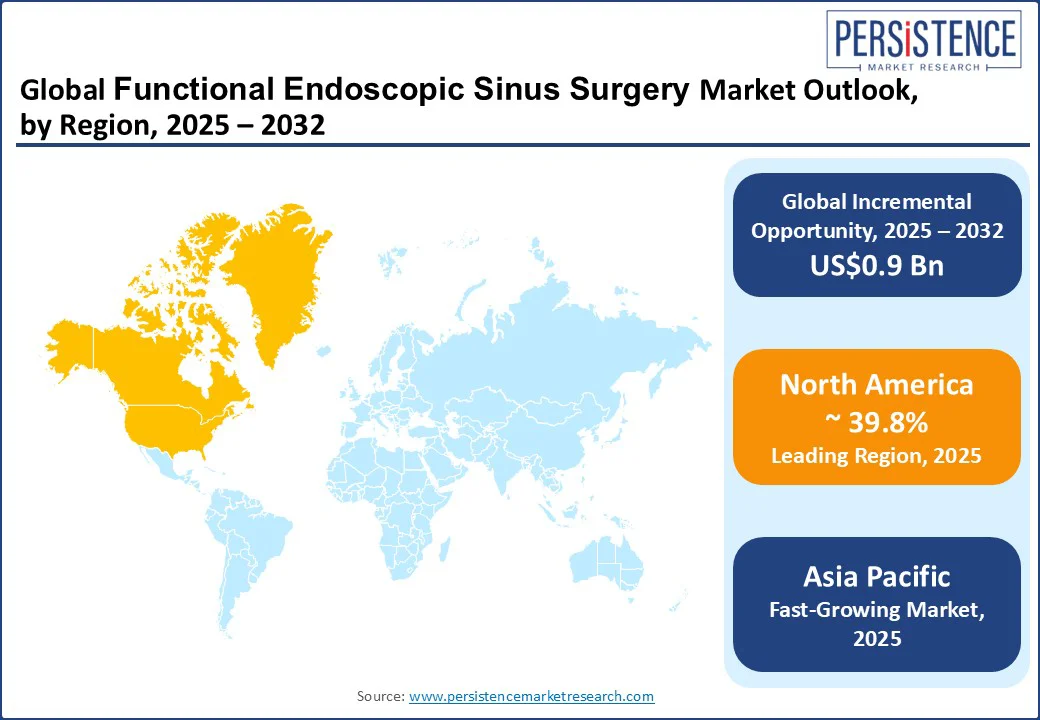

- Leading Region: North America leads the global FESS market with a market share of 39.8%, driven by advanced ENT infrastructure, high outpatient volumes, and growing adoption of image-guided surgery, particularly in the U.S. and Canada.

- Fast-Growing Region: The rising prevalence of chronic rhinosinusitis and expanding ENT specialty clinics in Asia Pacific are accelerating procedure volumes, particularly in India and China.

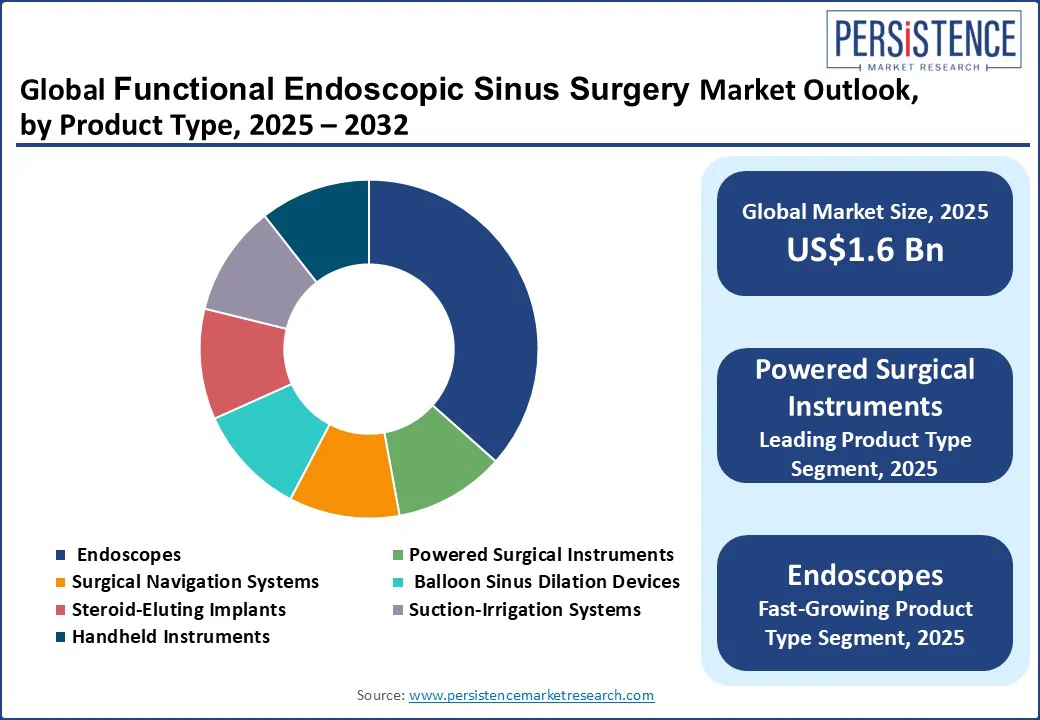

- Leading Product: Powered surgical instruments are the leading product segment with a share of 38% in 2025, valued for their precision in tissue removal during complex procedures such as ethmoid and sphenoid surgeries.

- Industry Trend: Balloon-assisted FESS is gaining rapid momentum, especially in office-based settings. It offers shorter recovery times, minimal bleeding, and a viable option for patients seeking to avoid general anesthesia.

- Role of Artificial Intelligence: Technological innovations such as AI-driven navigation systems and 3D endoscopy are transforming surgical accuracy and efficiency, particularly in revision and frontal sinus surgeries.

- Strategic Aspect: Strategic collaborations and acquisitions, including Medtronic’s acquisition of Intersect ENT, are driving competition and portfolio diversification across sinus implants and navigation-enabled devices.

|

Global Market Attribute |

Key Insights |

|

Functional Endoscopic Sinus Surgery Market Size (2025E) |

US$ 1.6 Bn |

|

Market Value Forecast (2032F) |

US$ 2.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.2% |

Market Dynamics

Driver - Improved Outcomes from Sinus Implants are Driving Repeat FESS Adoption

The uptick in image-guided navigation systems for sinus surgery is spurring precision and adoption among ENT specialists. Real-time navigation and 4K UHD endoscopes reduce surgical complications and enhance precision in sinus surgery. This trend is strengthened by innovations in specialized sinus instruments, powered microdebriders, and ultra-slim sinus forceps that enable efficient tissue removal and minimize trauma in complex ethmoid and maxillary procedures. Office-based balloon sinuplasty is expanding access to younger and older patients, who avoid hospital surgeries. Growth in AI-enhanced cone-beam CT diagnostics for fungal sinusitis detection is improving candidate selection, delivering higher diagnostic confidence before FESS.

The rising use of ambulatory ENT specialty clinics, which offer powered FESS workflows, is also shifting volume away from traditional hospitals. The recurrence of chronic sinusitis and incomplete primary interventions drive the demand for revision FESS. Surgeons increasingly rely on 3D endoscopic visualization systems to navigate scarred and altered anatomy during secondary procedures. The emergence of post-FESS drug-eluting sinus implants is enhancing long-term surgical outcomes, reducing the need for systemic steroids, and encouraging repeat adoption of advanced FESS protocols.

Restraint - Shortage of Proficiency in Advanced AI-Assisted FESS Tools Slows Clinician Adoption Rates

The lack of rural ENT specialist outreach clinics restricts access to FESS in underserved regions, causing delays in diagnosis and intervention. In areas with sparse healthcare infrastructure, patients seldom receive referrals for image-guided sinus surgery, perpetuating untreated chronic sinusitis cases. This uneven distribution of trained professionals directly limits the procedural volume in remote communities.

Surgeons face a steep learning curve with 3D endoscopic navigation systems, which impacts early adoption in mid-sized hospitals. The dependency on high-frequency powered microdebrider systems requires specialized training that many facilities lack. Limited clinician proficiency with advanced, AI-assisted FESS tools constrains adoption.

Opportunity - Expanded Adoption of Ambulatory Specialty ENT Clinics Offering Hybrid Balloon-FESS Protocols

Increased use of AI-guided cone-beam CT diagnostic solutions for fungal sinusitis discrimination improves candidate selection and effective procedure triage. This boosts referral rates for FESS among complex cases and supports integration of advanced navigation tech into standard pathways. The development of intraoperative 3D model updating via endoscopic video fusion (a digital-twin approach) enables real-time anatomical mapping during surgery, unlocking higher accuracy in revision procedures and challenging anatomy.

Expanded adoption of ambulatory specialty ENT clinics offering hybrid balloon-FESS protocols is enabling minimally invasive outpatient care for chronic rhinosinusitis and nasal polyposis, particularly in urban markets. Simultaneously, companies can leverage rising demand for steroid-eluting bioabsorbable sinus implants post-FESS to improve patient outcomes and reduce revision rates, creating bundled procedure opportunities and longer-term device pipelines.

Category-wise Analysis

Product Type Insights

Powered surgical instruments are anticipated to hold the largest market share of 38% in 2025. These tools, such as microdebriders, powered forceps, and shavers, are widely used for their precision, speed, and tissue-handling efficiency, especially in complex ethmoid and sphenoid sinus surgeries. Surgeons prefer them due to their reliability, ease of use, and ability to improve intraoperative control, particularly in high-volume hospital settings. Their integration into standard ENT surgical kits makes them the most indispensable component in procedural setups.

Endoscopes, particularly 4K and 3D sinuscopes, are the fastest-growing product category. With rising demand for enhanced visualization and minimal invasiveness, high-definition endoscopic systems are becoming essential tools in advanced FESS centers. These devices reduce surgeon fatigue and improve clarity during delicate procedures, especially in anatomically distorted sinus cavities. The transition to digital, compact, and ergonomic designs is also expanding their utility across both hospitals and ambulatory surgical centers.

Procedure Type Insights

Traditional FESS is projected to dominate overall market share in 2025. This technique is well-established, widely taught in ENT residency programs, and forms the clinical backbone of sinus surgeries globally. It remains the preferred approach for moderate to severe chronic rhinosinusitis, particularly in cases requiring comprehensive access to multiple sinuses. Its extensive use in hospitals ensures high procedural volume despite emerging technologies.

Powered FESS is emerging as the fastest-growing procedure type, largely due to the adoption of advanced powered instrumentation. The ability to perform precise, controlled tissue removal with powered tools allows for quicker procedures, minimal bleeding, and faster recovery. Hospitals and ambulatory centers increasingly favor powered techniques to reduce operative time and enhance patient throughput, particularly for patients requiring bilateral or multi-sinus intervention.

Regional Insights

North America Functional Endoscopic Sinus Surgery Market Trends - High Prevalence of Chronic Rhinosinusitis and Well-Established Network of ENT Specialists

North America is expected to hold the largest share in the global FESS market, accounting for approximately 39.8% of total revenue in 2025. The region benefits from a high prevalence of chronic rhinosinusitis, strong clinical adoption of advanced navigation technologies, and a well-established network of ENT specialists. The U.S. leads with over 250,000 FESS procedures annually, driven by early access to 3D-enabled sinuscopes and widespread reimbursement for minimally invasive sinus interventions. Nearly 73% of surgical centers in the U.S. now use 3D endoscopy and powered instrumentation, particularly for complex ethmoid or sphenoid cases.

Canada continues to see an uptick in image-guided FESS adoption across tertiary hospitals, backed by favorable regulatory approvals and ENT training expansion through provincial funding. Recent developments such as Medtronic’s acquisition of Intersect ENT and Integra LifeSciences’ takeover of Acclarent have strengthened the competitive landscape, particularly in post-FESS drug-eluting implants and balloon dilation systems.

Asia Pacific Functional Endoscopic Sinus Surgery Market Trends - Rising Surgical Volumes and Expanding ENT Infrastructure

Asia Pacific is the fastest-growing region in the global FESS market, propelled by rapid healthcare modernization, increasing sinusitis incidence, and a growing ENT workforce. The region is witnessing a significant rise in outpatient balloon-assisted procedures and hybrid surgical setups. China is leading this growth, driven by investments in hospital infrastructure and rising cases of fungal and bacterial sinusitis in urban areas. Major city hospitals are integrating AI-based diagnostic tools and adopting intraoperative navigation systems to improve procedural safety.

In India, the rise of private ENT specialty clinics and minimally invasive platforms has led to a 65% increase in FESS procedure volume over recent years. Expansion of medical tourism and ENT-focused fellowships is further accelerating the market. Balloon dilation remains the most popular method across urban centers, while advanced FESS tools are seeing high growth, especially in Japan and South Korea. Regulatory relaxation and device affordability are additional enablers across the region.

Europe Functional Endoscopic Sinus Surgery Market Trends - Advancements in Endoscopic Technology and Rising Adoption of Office-Based Procedures Fuel Growth

Europe represents a mature and steadily expanding market, with a projected CAGR of around 7%. The region’s growth is supported by universal healthcare access, institutional ENT training, and consistent reimbursement policies. Germany leads with a high density of ENT hospitals and strong clinical integration of image-guided FESS systems. German institutions are also among the first to pilot new navigation software and 4K sinuscopes, helping improve precision and outcomes in revision procedures.

In the U.K., FESS procedure volumes have increased by more than 20% over the past decade, supported by the NHS's efforts to reduce wait times for sinus surgeries and incorporate new surgical training programs. Cost-effective adoption is encouraged through centralized procurement and outcome-based technology assessment. Recent product introductions, such as Olympus' 4K UHD endoscopy system and Medtronic’s ENT navigation platform, have gained early traction in both Germany and the U.K., reinforcing Europe’s position as a key innovation hub in sinus surgery.

Competitive Landscape

The global functional endoscopic sinus surgery market is moderately consolidated, with a mix of global medtech giants and specialized ENT device companies competing across product lines. Medtronic, Stryker, and Olympus Corporation are market leaders, offering comprehensive portfolios that span powered instrumentation, 3D/4K endoscopy systems, and image-guided navigation platforms. Medtronic’s acquisition of Intersect ENT expanded its dominance in post-operative sinus care through drug-eluting implants such as PROPEL. Stryker has leveraged its strength in powered tools and endoscopic visualization to cater to both hospitals and ambulatory surgical centers.

Strategic collaborations, technology licensing, and surgeon training programs are common tactics used to strengthen market presence. With increasing demand for hybrid FESS techniques and office-based interventions, competition is shifting from mere product availability to integrated procedural solutions, driving R&D and partnerships across the value chain.

Key Industry Developments

- In June 2025, multiple AI-integrated FESS navigation platforms received CE mark clearance, allowing commercial distribution in Europe. These systems assist surgeons in identifying critical anatomical landmarks in distorted sinus cavities, especially during revision surgeries.

- In May 2024, clinical trials for the next generation of SINUVA steroid-releasing implants by Intersect ENT (now part of Medtronic) entered their final phase. Early data show improved drug elution profiles and extended post-op efficacy, with FDA review expected in early 2025.

Companies Covered in Functional Endoscopic Sinus Surgery Market

- Medtronic plc

- Stryker Corporation

- Olympus Corporation

- Johnson & Johnson

- Karl Storz SE & Co. KG

- Smith & Nephew plc

- B. Braun Melsungen AG

- Richard Wolf GmbH

- Intersect ENT, Inc.

- Xoran Technologies, LLC

- Fiagon GmbH

- Scopis GmbH

- ClaroNav Kolahi Inc.

- Spiggle & Theis Medizintechnik GmbH

- Lumenis Ltd.

- Sino-Lion Medical

- ENTOD International

- Trivitron Healthcare

Frequently Asked Questions

The functional endoscopic sinus surgery market is projected to be valued at US$ 1.6 Bn in 2025.

The functional endoscopic sinus surgery market is expected to reach approximately US$ 2.5 Bn, by 2032.

Key trends include the shift toward office-based balloon sinus dilation, adoption of AI-powered navigation platforms, integration of 4K/3D endoscopy systems, and the rise in revision FESS procedures.

Powered surgical instruments lead the market, accounting for over 38% of global revenue in 2025, due to their precision and adaptability in complex sinus procedures.

The market is expected to grow at a CAGR of 7.3% from 2025 to 2032, supported by technological advancements and growing ENT outpatient volumes.

Leading companies include Medtronic plc, Stryker Corporation, Olympus Corporation, Johnson & Johnson, and Karl Storz SE & Co. KG.