- Industrial Machinery

- U.S. Fire Sprinklers Market

U.S. Fire Sprinklers Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

U.S. Fire Sprinklers Market by Product Type (Wet Pipe Fire Sprinkler, Dry Pipe Fire Sprinkler, Pre-action Sprinkler System, Deluge Sprinkler System, Others) and Application (Commercial Buildings, Industrial Facilities, Residential, Institutional.), and Regional Analysis for 2026 - 2033

U.S. Fire Sprinklers Market Trends & Analysis

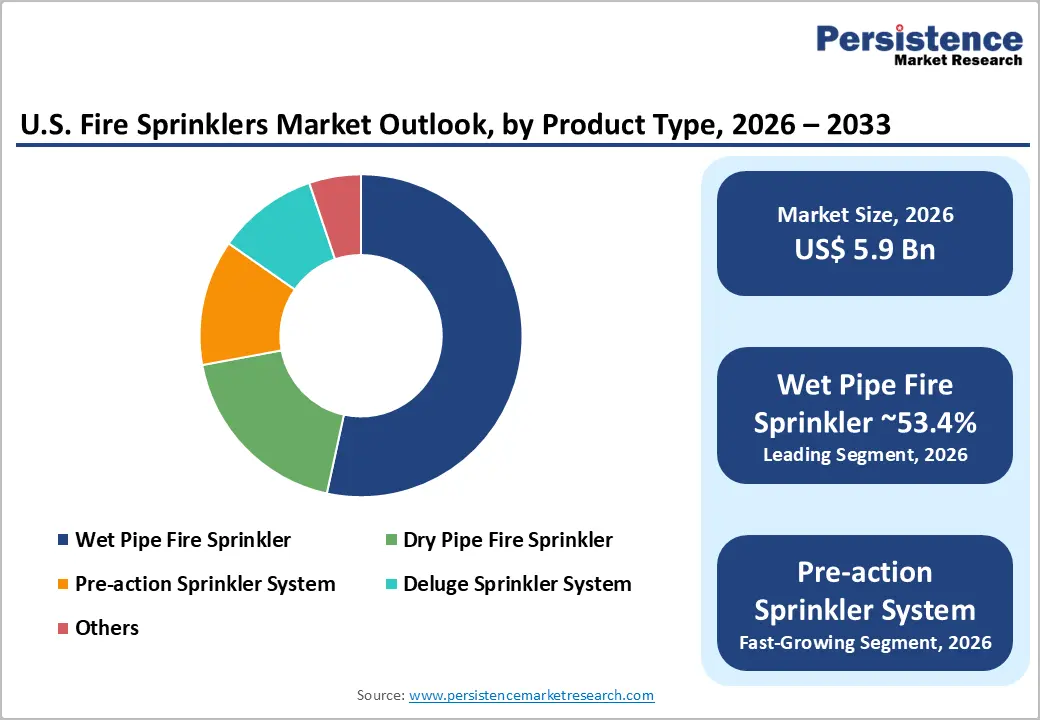

The U.S. fire sprinklers market size is projected at US$ 5.9 billion in 2026 and is projected to reach US$ 9.7 billion by 2033, growing at a CAGR of 7.4% between 2026 and 2033.

Strong regulatory enforcement of NFPA 13 and International Building Code (IBC) across all 50 states continues to drive mandatory installation in new commercial, institutional, and multi-family projects. Rise in construction activity, urban densification and retrofit requirements in older stock are expanding the installed base and associated inspection and maintenance revenues. Digital monitoring, predictive maintenance and insurance incentives are accelerating adoption while shifting value toward integrated, data-rich service models.

Key Industry Highlights:

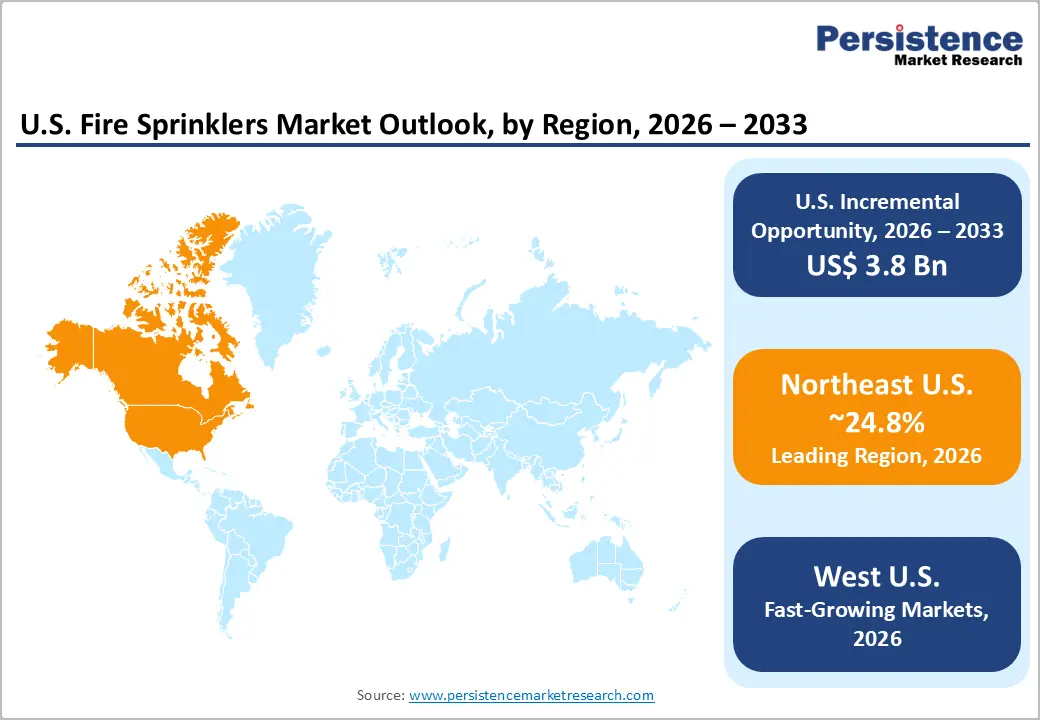

- Incremental Value: Incremental opportunity of US$ 3.8 Bn emerges over 2026 - 2033, driven by new construction, retrofits and expanded service offerings across commercial, industrial and residential segments.

- Dominant Application: Commercial buildings hold about 41.8% share, supported by stringent NFPA 13/IBC requirements in offices, retail, hospitality, and public facilities nationwide.

- Fastest-Growing Application: Residential applications are likely to witness a positive growth, as more states adopt home sprinkler provisions and multifamily high-rise construction and senior living developments expand.

- Dominant Product: Wet pipe systems are likely to command roughly 53.4% revenue share in 2026, reflecting superior reliability and broad suitability in conditioned spaces.

- Fastest-Growing Product: Pre-action systems are poised to grow at 8.5% CAGR, supported by data centers, labs and mission-critical applications requiring additional water-damage safeguards.

- Regional Dynamics: Northeast U.S. leads with about 24.8% share, while West U.S. posts the fastest growth at roughly 8.1% CAGR and Southeast U.S. combines 22.3% share with 7.7% CAGR, reflecting strong Sun Belt and coastal development trends.

- Strategic Activity: Post-2023 M&A and portfolio reshaping by Pye-Barker, EMCOR-affiliated entities, Carrier and APi Group signal ongoing consolidation, geographic expansion and refocusing around higher-growth, service-intensive life-safety offerings.

Market Dynamics Analysis

Drivers - Stringent codes, standards and enforcement

NFPA 13, referenced by the IBC and adopted as the basis for state building codes, effectively makes automatic sprinklers mandatory in most new commercial, institutional and multifamily buildings over defined occupancy thresholds across the U.S. NFPA data for 2017-2021 show that when sprinklers are present, civilian fire death and injury rates per fire are roughly 90% and 32% lower, respectively, than in buildings without automatic extinguishing systems, underlining the public-safety rationale for strict enforcement. This provides long-term visibility for manufacturers, contractors and service providers.

The local authorities increasingly require NFPA-compliant design, hydraulic calculations and third-party review before granting occupancy certificates, tightening compliance in both new build and major renovation projects. Insurers often condition favorable premiums on the presence of well-maintained systems, reinforcing adoption in high-value commercial, industrial and healthcare facilities. Together, these regulatory and insurance mechanisms systematically expand installed sprinkler density and support steady growth in recurring testing, inspection and retrofit work.

Proven life-safety and loss-mitigation performance

Evidence from multiple NFPA studies shows sprinklers confine fire spread to the room of origin in about 94% of reported structure fires where systems are present, versus roughly 73% in buildings without automatic extinguishing systems. Overall, sprinklers are judged to operate and be effective in approximately 89% of fires large enough to activate them, with wet-pipe systems performing at the upper end of this range. These outcome improvements translate into materially lower life, property and business-interruption losses for asset owners and insurers.

Quantified benefits underpin growing acceptance of sprinklers in residential occupancies, especially high-rise multi-family and assisted living where evacuation is complex. As awareness spreads among city officials, developers and the public, jurisdictions are extending requirements for home fire sprinkler systems in new one- and two-family dwellings, while healthcare, education and warehouse occupancies face continued tightening of performance-based codes. This broadening risk-based rationale supports above-GDP growth across both new installations and upgrades from older, less reliable systems.

Restraints - Installation complexity, labor constraints and permitting delays

Although sprinklers are mandated in many occupancies, system design must be stamped by fire protection engineers and installed by licensed contractors, and AHJ review cycles can be lengthy. Shortages of experienced NICET-certified technicians and fitters in some regions slow project execution and can delay occupancy certificates, impacting near-term system revenue realization even when demand is structurally strong. These capacity bottlenecks particularly affect complex pre-action and deluge projects.

Building owner hesitancy around retrofits and shutdowns

For existing facilities, owners often defer voluntary retrofits because of perceived disruption to operations, especially where work requires ceiling access, temporary system impairments and coordination with other trades. Concerns about water damage from accidental discharges, especially in high-value IT, archival or hospitality environments, can lead some stakeholders to favor detection-only solutions despite evidence of better outcomes with sprinklers. This hesitancy moderates retrofit penetration outside mandated categories, leaving segments of the legacy building stock under-protected.

Opportunities - Smart, connected and performance-based service models

The shift toward connected life-safety systems, including remote supervision of valves, pumps and flow switches, creates an opportunity to monetize data-driven service contracts beyond standard quarterly or annual inspections. Condition-based maintenance, automated impairment tracking and digital record-keeping help owners demonstrate compliance, support insurance negotiations and reduce nuisance outages. As more new installations incorporate IoT-enabled components, the installed base suitable for these services will expand rapidly alongside overall market growth.

For vendors, this trend supports recurring revenue with higher margins and stickier customer relationships, particularly in mission-critical sectors such as healthcare, logistics and data centers. Over 2026 - 2033, even modest penetration of enhanced monitoring contracts across the installed base could translate into hundreds of millions of dollars in incremental service revenue, while also differentiating suppliers in an otherwise hardware-intensive market. Partnerships between sprinkler OEMs, monitoring platforms and integrators are likely to accelerate this transition.

Consolidation and regional roll-up strategies

The U.S. installer and service landscape remains highly fragmented, with numerous regional sprinkler contractors alongside large national players. Recent activity shows aggressive consolidation, with Pye-Barker Fire & Safety alone acquiring dozens of fire alarm, sprinkler and security companies in 2024-2025, creating a national platform for life-safety services. Similar roll-up strategies from APi Group and EMCOR-affiliated businesses are expanding geographic coverage and multi-trade capabilities.

This consolidation offers opportunities for smaller contractors to join larger networks, gaining access to capital, design resources and national accounts. For investors and strategics, continued roll-ups can unlock synergies across procurement, fabrication, design centers and back-office functions while enabling cross-selling of sprinklers with alarms, suppression and security. As the total market grows by nearly US$ 3.8 Bn between 2026 and 2033, consolidation will be a key route to capturing outsized share of incremental demand.

Category-wise Analysis

Product Type Insights

Wet pipe fire sprinklers are the leading product type, accounting for about 53.4% of market revenue, supported by their simplicity, reliability and favorable performance profile in most non-freezing indoor environments. NFPA analyses show wet-pipe systems operate and are effective in roughly 89% of relevant fires, outperforming dry-pipe alternatives, which reinforces their specification in offices, retail, schools and healthcare facilities. Dry-pipe, deluge and specialty systems remain essential in cold storage, process and high-hazard applications, but their aggregate share is structurally smaller, and current trends suggest wet systems will retain leadership barring a major technology disruption.

Pre-action sprinkler systems are the fast-growing product segment expanding at a positive CAGR, driven by data centers, laboratories, museums and high-end commercial spaces where owners seek to minimize accidental discharge risk while meeting stringent fire protection requirements. Growth is supported by rising IT load densities, digital infrastructure investment and broader adoption of performance-based design, which favors configurable, intelligent pre-action solutions in sensitive environments.

Application Insights

By application, commercial buildings (offices, retail, hospitality) hold the leading share at around 41.8%, reflecting mandatory sprinkler requirements in most new non-residential construction and frequent upgrades in hospitality, office and large retail formats. These sites typically combine wet-pipe systems in occupied spaces with specialized solutions in back-of-house or parking areas, generating significant design and service revenue. Industrial facilities and institutional buildings together contribute a substantial secondary share, particularly in logistics, manufacturing, healthcare and education, where risk management and business-continuity considerations are prominent.

Residential (apartments, single-family homes, high-rises) is the fast-growing application, with an estimated 8.6% CAGR as authorities are incentivizing home sprinkler requirements and multifamily construction remains elevated. Aging population, demand for senior living communities and high-rise urban housing intensify focus on life-safety performance, while insurers and advocacy campaigns highlight the significant reduction in residential fire fatalities when sprinklers are installed.

Regional Insights

Northeast U.S. Fire Sprinklers Market Trends

By 2026, the Northeast is expected to represent around one-quarter of U.S. fire sprinkler revenues, supported by retrofit activity in older multifamily and commercial buildings in New York City, Boston and Philadelphia, and a steady pipeline of institutional projects. This translates into a market worth well over US$ 1 Bn annually, concentrated in wet-pipe and increasingly smart, monitored systems.

Beyond the leading states, Connecticut, Pennsylvania and regional university towns contribute meaningfully through campus expansions, lab construction and healthcare upgrades. Competitive dynamics feature a mix of national contractors and strong regional specialists, with AHJs and union labor structures shaping bidding, execution models and service opportunities across the corridor.

West U.S. Fire Sprinklers Market Trends

California alone, with comprehensive requirements in hotels, motels and residential care facilities, anchors a large share of western demand, driving strong new-build and retrofit volume. Data centers, logistics hubs and semiconductor facilities across the broader West increasingly specify pre-action and deluge systems, boosting value per project and favoring sophisticated design-build contractors.

Other western states, including Colorado, Utah and Oregon, add momentum through population growth, infrastructure projects and warehousing linked to e-commerce corridors. National players and regional firms headquartered in the West, such as Western States Fire Protection, leverage multi-state footprints and fabrication capabilities to capture scale efficiencies and recurring service contracts across this high-growth market.

Southeast U.S. Fire Sprinklers Market Trends

High levels of housing permits and multifamily approvals in Texas and Florida, alongside rapid expansion of logistics and manufacturing corridors, underpin strong demand for wet-pipe systems in apartments, big-box retail and distribution centers. Religious, education and healthcare facilities also contribute, often requiring more complex design and tighter compliance documentation.

Beyond the largest states, emerging metros in Tennessee, Alabama and the Carolinas are upgrading codes and investing in industrial parks, driving adoption of both standard wet systems and specialized pre-action solutions. The region’s market is characterized by active consolidation, with large platforms such as Pye-Barker and APi Group acquiring local sprinkler contractors to build scale, broaden service offerings and improve coverage across fast-growing metropolitan clusters.

Competitive Landscape

The U.S. fire sprinklers market remains moderately fragmented but rapidly consolidating, as national life-safety platforms acquire regional contractors to build scale across design, fabrication, installation, and service. Key differentiators include NFPA-compliant engineering expertise, multi-regional execution capability, 24/7 service coverage, and integration of sprinklers with alarms, suppression, and digital monitoring.

Strategic themes center on innovation in smart, connected systems, selective cost leadership in commoditized wet-pipe offerings, and aggressive market expansion via roll-up acquisitions and geographic diversification into high-growth Sun Belt and western states.

Strategic Developments:

- In March 2026, FSS Technologies acquired The Fire Group, Inc., expanding its fire sprinkler installation and service capabilities in the U.S. Midwest and strengthening its position as a comprehensive life-safety solutions provider across commercial and industrial facilities.

- In March 2026, Pye-Barker Fire & Safety announced it had completed 57 acquisitions in 2025, adding fire alarm, sprinkler and security companies across the United States to scale its integrated life-safety platform and deepen local coverage in high-growth metropolitan areas.

- In July 2025, Pye-Barker reported 12 additional acquisitions in the first half of 2025, including multiple sprinkler and fire equipment providers, enhancing its design, installation and service capabilities and expanding its presence in key states such as Texas, Florida, Illinois and Ohio.

- In April 2026, APi Group announced a definitive agreement to acquire Onyx-Fire Protection Services Inc., an inspection-first fire and life-safety services provider in Canada, expanding APi’s recurring revenue base and strengthening its North American service platform relevant to sprinkler inspection and maintenance.

U.S. Fire Sprinklers Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 4.0 Bn |

| Current Market Value (2026) | US$ 5.9 Bn |

| Projected Market Value (2033) | US$ 9.7 Bn |

| CAGR (2026 - 2033) | 7.4% |

| Leading Region | Northeast U.S. |

| Dominant Application | Commercial Buildings - 41.8% |

| Top-ranking Product | Wet Pipe Fire Sprinkler - 53.4% |

| Incremental Opportunity | US$ 3.8 Bn |

Companies Covered in U.S. Fire Sprinklers Market

- Johnson Controls International plc (Tyco Fire Products)

- APi Group Corporation

- EMCOR Group, Inc.

- S.A. Comunale

- Pye-Barker Fire & Safety

- Viking Fire Protection Group

- The Viking Corporation

- Reliable Automatic Sprinkler Co., Inc.

- Victaulic Company

- Potter Electric Signal Company LLC

- Western States Fire Protection Company

- Globe Fire Sprinkler Corporation

- APi-affiliated regional contractors and VFPG companies

- EMCOR-affiliated S.A. Comunale

- FSS Technologies

Frequently Asked Questions

The U.S. Fire Sprinklers Market is expected to reach about US$ 5.9 Bn in 2026, expanding toward US$ 9.7 Bn by 2033 on the back of code-driven demand and service growth.

Market growth is driven primarily by NFPA 13 and IBC-based mandates, proven life-safety and loss-reduction performance, robust construction and retrofit activity, and increasing integration of sprinklers into connected, smart-building life-safety ecosystems.

Between 2026 and 2033, the U.S. Fire Sprinklers Market is projected to grow at approximately 7.4% CAGR, reflecting sustained regulatory enforcement and expansion of higher-value engineered and service offerings.

Key opportunities include under-penetrated residential and mixed-use buildings, smart and data-driven service models, and consolidation of regional contractors, which together can unlock significant incremental revenue and margin expansion over the forecast period.

Key players span global OEMs and national service platforms, including Johnson Controls (Tyco), APi Group, EMCOR-affiliated entities, Pye-Barker, Viking Fire Protection Group, Reliable Automatic Sprinkler, Victaulic, Potter Electric Signal, Western States Fire Protection, Globe Fire Sprinkler and FSS Technologies, alongside numerous regional specialists.