- Beverages

- Fermented Beverages Market

Fermented Beverages Market Size, Share, and Growth Forecast, 2026 - 2033

Fermented Beverages Market by Source (Grains, Fruits & Vegetables, Dairy Products, Tea, Others), Packaging Type (Bottles, Cans, Cartons, Kegs, Barrels, Others), Beverage Type (Alcoholic, Non-Alcoholic, Fermented Tea Drinks), and Regional Analysis 2026 - 2033

Fermented Beverages Market Size and Trends Analysis

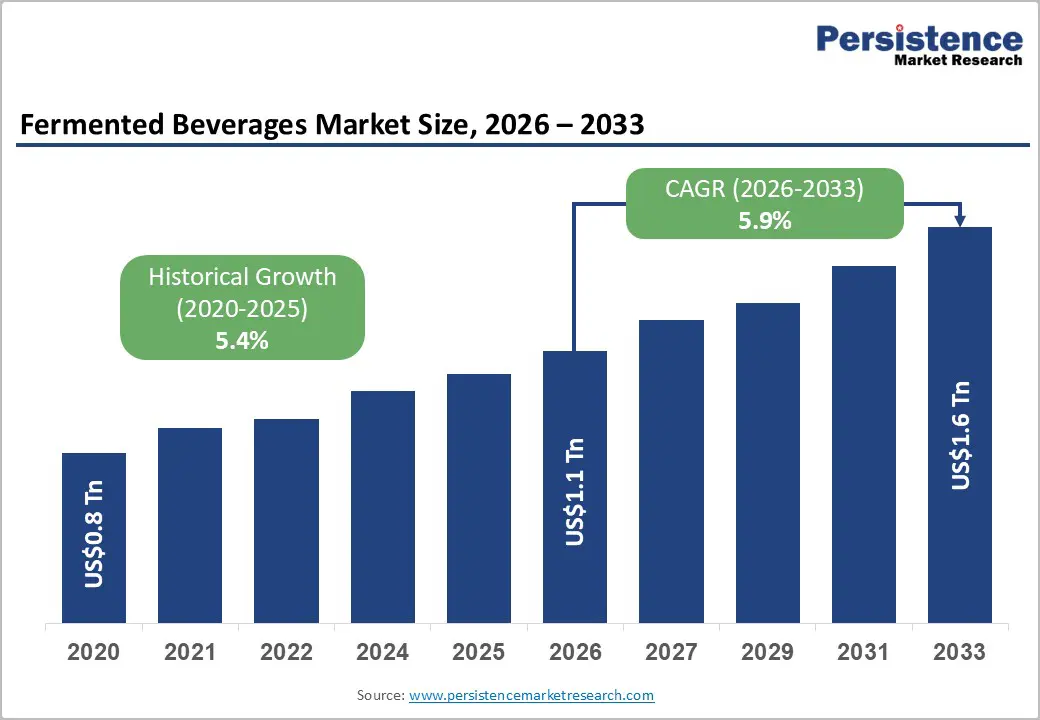

The global fermented beverages market size is likely to be valued at US$1.1 trillion in 2026 and is expected to reach US$1.6 trillion by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033, driven by increasing consumer awareness of gut health, which is boosting demand for functional beverages across multiple sources.

Rapid urbanization is accelerating the adoption of convenient options, particularly non-alcoholic variants, while advancements in fermentation technologies are improving shelf life and flavor. At the same time, regulatory and consumer pressure are pushing manufacturers to develop low-sugar formulations, supporting sustained growth among health-focused consumer segments.

Key Industry Highlights:

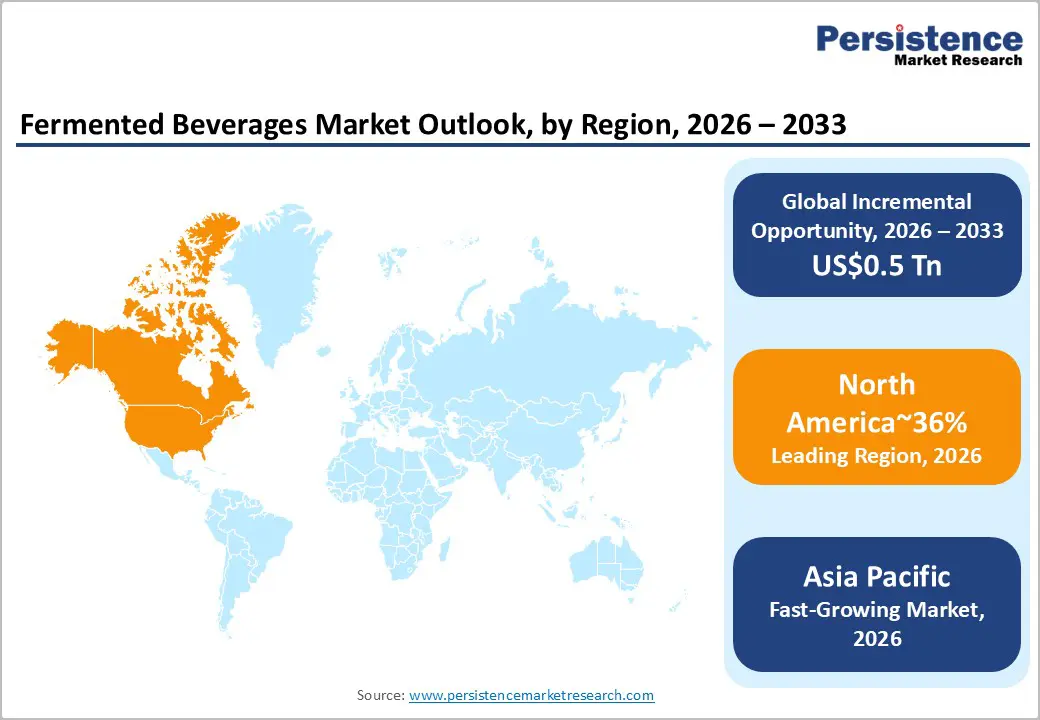

- Leading Region: North America is projected to lead, accounting for approximately 36% share in 2026, supported by established retail infrastructure and premiumization trends.

- Fastest-growing Region: Asia Pacific is anticipated to grow the fastest, driven by expanding middle-class demographics, rising urbanization, and localized production scaling.

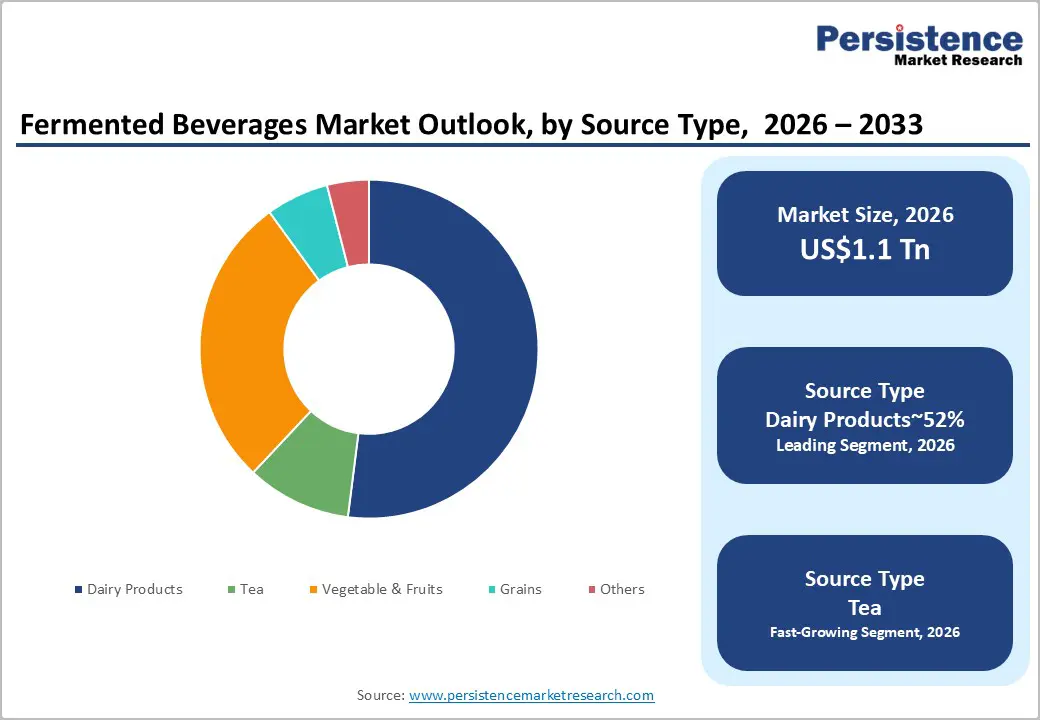

- Leading Source: Dairy products are expected to lead, accounting for approximately 52% share in 2026, anchored by historical consumption habits and extensive agricultural networks.

- Leading Beverage Type: The alcoholic segment is anticipated to dominate, accounting for approximately 69.3% share in 2026, anchored by entrenched cultural consumption patterns and robust brewing infrastructures.

| Key Insights | Details |

|---|---|

| Fermented Beverages Market Size (2026E) | US$1.1 Tn |

| Market Value Forecast (2033F) | US$1.6 Tn |

| Projected Growth (CAGR 2026 to 2033) | 5.9 % |

| Historical Market Growth (CAGR 2020 to 2025) | 5.4% |

DRO Analysis

Driver - Functional Nutrition Prioritization

Shifting consumer behavior increases the demand for proactive dietary solutions and functional nutrition integration. Producers such as Danone S.A. and Yakult Honsha Co., Ltd. incorporate microbial cultures to align products with evolving metabolic health considerations. Urban consumers prioritize wellness-linked formulations, influencing retail procurement toward evidence-based offerings. This transition reshapes category dynamics by emphasizing measurable health outcomes in beverage selections. Consequently, structured product innovation accelerates revenue momentum across functional beverage segments.

Strategic diversification enables brands to capture expanding health-conscious consumer demographics effectively. PepsiCo with KeVita Turmeric-Ginger Kombucha demonstrates targeted functional positioning within competitive retail environments. Ingredient transparency strengthens brand trust while supporting premium shelf allocation decisions. Retailers prioritize verifiable health-oriented hydration products, reinforcing sustained category consumption growth.

Rising Momentum of Non-Alcoholic Fermented Beverages

Evolving dietary preferences accelerate demand for non-alcoholic fermented beverages as substitutes for traditional spirits. Supportive regulations for low-alcohol products enable scalable production using diverse grain and fruit substrates. Hybrid fermentation processes improve cost efficiencies, strengthening supplier margin structures across competitive markets. This shift enhances adoption within hospitality and retail channels seeking alternative beverage offerings. Consequently, non-alcoholic segments gain structural traction across evolving consumer consumption patterns.

GT's Living Foods’ SYNERGY Kombucha strengthens shelf visibility through certified organic product positioning. These strategies validate commercial scalability across expanding sober-curious consumer demographics. Diversified product portfolios reinforce sustained market participation and category growth.

Restraint Analysis - Complex Standardization

Biological fermentation inconsistency creates quality control vulnerabilities across large-scale production environments. Microbial variability disrupts formulation stability during continuous manufacturing cycles, increasing operational complexity. This scientific unpredictability raises spoilage risks throughout extended distribution networks and storage phases. The combined pressures constrain margin expansion and limit efficiency gains across fermentation-based beverage production systems.

Maintaining live culture viability requires costly cold-chain logistics across distribution networks. GT's Living Foods with SYNERGY Raw Kombucha faces constraints from temperature-sensitive product handling requirements. Fluctuations during transit degrade product efficacy before retail availability, impacting quality assurance outcomes. These infrastructure gaps restrict penetration into developing regions lacking reliable refrigeration systems. Elevated logistical costs continue to limit scalability across broader geographic markets.

Supply Chain Volatility

Climate-driven variability disrupts the availability of grains and fruits used in fermentation processes. This instability increases procurement costs across dairy and plant-based input supply chains. Inconsistent agricultural yields compress supplier margins while creating uncertainty in production planning cycles. Value chains experience structural strain as sourcing pressures intensify across upstream and midstream operations. Consequently, manufacturers face constrained output stability and elevated input cost exposure.

Archer Daniels Midland, with grain fermentation platforms, encounters yield variability affecting raw material consistency. Cargill, with dairy culture ingredients, faces supply gaps linked to lactose availability fluctuations. These disruptions heighten commercial risks for downstream beverage producers and formulation specialists. Bottling companies increasingly delay capacity expansions amid uncertain input supply conditions. Such volatility reinforces cautious investment strategies across supply-dependent production segments.

Opportunity Analysis - Opportunity - Precision Fermentation

Engineered microorganisms enable controlled flavor and protein synthesis across precision fermentation systems. This approach removes variability associated with traditional wild culture fermentation processes. Predictable production cycles improve resource utilization and stabilize industrial-scale manufacturing outputs. Synthetic biology tools accelerate the development of customized functional attributes within fermented products. These efficiencies restructure cost dynamics and enhance scalability across fermentation-based supply chains.

Targeted bioactive compounds address niche wellness demands across increasingly segmented global consumer markets. Tata Consumer Products with Tetley Kombucha explores precision-driven nutritional formulations for differentiated positioning. Customized microbial engineering supports premium pricing across specialized retail channels and health-focused segments. Advanced biotechnology reduces dependence on traditional agricultural inputs and seasonal variability constraints. Such innovation-driven platforms expand commercialization potential across evolving functional beverage ecosystems.

Sustainable Packaging Adoption

Eco-conscious procurement accelerates the adoption of recyclable packaging formats amid tightening plastic regulations globally. Advances in material science enable durable alternatives that maintain integrity for fermented beverage distribution. Retail compliance mandates drive format transitions toward sustainable containers across supply chains. These shifts improve logistics efficiency through weight reduction and optimized transportation configurations. Consequently, packaging innovation contributes to cost rationalization and environmental compliance simultaneously.

Owens-Illinois, with Eco-Shape PET Bottles, advances lightweight alternatives to traditional glass packaging formats. Amcor with Rigid-Lite Cans supports carbonated fermentation requirements with improved material efficiency. These strategies align with certification frameworks emphasizing sustainability and reduced environmental impact. Manufacturers increasingly integrate circular economy principles into packaging design and lifecycle management.

Category-wise Analysis

Source Insights

Dairy products are expected to dominate the market, accounting for around 52% share, anchored by historical consumption habits. Widespread agricultural infrastructure guarantees consistent raw material availability globally. This supply reliability mitigates volatile pricing dynamics for enterprise manufacturers. Traditional formulation techniques remain highly trusted among older consumer demographics. Yakult Honsha with Yakult Probiotic Drink dominates this established vertical. Extensive clinical validation reinforces consumer trust in milk-derived functional claims. Global dairy cooperatives continuously optimize sophisticated cold-chain distribution networks entirely.

Tea-based beverages are projected to be the fastest-growing segment, driven by vegan adoption and enzyme tech advancements. Grains and fruits enable scalable non-dairy probiotics that match dairy nutrition profiles. GT's Living Foods with Enlightened Kombucha leads tea infusions with raw variants. Integration of precision fermentation widens appeal in wellness aisles. Remedy Drinks with Remedy Coconut Kefir targets these mindful consumption trends. Plant-derived functional drinks naturally command higher price points at checkout. Consequently, expanding profit margins are forecast to accelerate corporate investments.

Packaging Type Insights

Bottles are projected to lead the packaging, accounting for approximately 49% share, reinforced by superior atmospheric preservation capabilities. Impermeable glass structures effectively prevent oxygen ingress during prolonged storage. This material resilience protects sensitive microbial cultures from environmental degradation. Transparent walls visually communicate product authenticity and natural fermentation cloudiness. Brew Dr. with Strawberry Fields Kombucha utilizes these secure enclosures.

Premium aesthetic qualities simultaneously justify higher retail pricing strategies consistently. Supermarkets favor rigid containers that stack securely on display shelves. These logistical advantages streamline inventory management across large retail environments.

Cans are anticipated to be the fastest-growing segment in the Fermented Beverages Market, driven by increasing demand for portability. Active consumer lifestyles necessitate durable and lightweight transportation solutions daily. This convenience factor strongly influences procurement across urban retail environments. Opaque metal walls completely block ultraviolet light from degrading biotics.

Lipton with Lipton Kombucha leverages aluminum to enhance on-the-go accessibility. Superior recycling rates also align with mounting ecological consumer preferences. Reducing shipping weights proportionally decreases logistics costs for beverage distributors. Such operational savings allow manufacturers to reinvest in marketing campaigns. Consequently, metallic formats are set to capture rapid market share. Continued metallurgical innovations are forecast to expand structural packaging capabilities.

Regional Insights

North America Fermented Beverages Market Trends

North America is expected to remain the leading regional market, accounting for approximately 36% share in 2026, supported by established retail infrastructure. Dense distribution networks ensure rapid product placement across diverse demographics. This logistical maturity facilitates immediate access to premium functional nutrition. High disposable incomes allow consistent expenditure on specialized dietary enhancements. Stringent labeling regulations simultaneously cultivate intense consumer trust in formulations. Retailers dedicate significant floor space to holistic wellness beverage categories. Such structural advantages are set to sustain ongoing category dominance.

The U.S. is projected to anchor regional momentum through sustained investments in retail innovation. Aggressive marketing campaigns continuously educate populations regarding digestive health optimization. This knowledge dissemination drives robust procurement across mainstream grocery channels. GT's Living Foods with SYNERGY Raw Kombucha commands significant shelf space domestically. Domestic venture capital further accelerates technological advancements in precision fermentation. These financial infusions rapidly scale production capabilities for emerging startups. Such aggressive capitalization is anticipated to solidify localized market leadership.

Asia Pacific Fermented Beverages Market Trends

Asia Pacific is anticipated to register the fastest growth trajectory, as expanding middle-class demographics accelerate market expansion across urban centers. Rapid urbanization fundamentally shifts dietary habits toward convenient functional solutions. This demographic transition stimulates unprecedented demand for health-oriented packaged goods. Rising disposable incomes enable broader participation in premium wellness trends. Local manufacturers actively upgrade production lines to meet escalating consumption.

E-commerce platforms simultaneously bypass traditional infrastructural limitations in rural territories. Consequently, modernization forces continue to drive profound structural sector transformation.

India is positioned to spearhead this expansion through rapid retail modernization efforts. Government policies actively promote domestic manufacturing capabilities for functional foods. This industrial support lowers baseline production costs for wellness brands. Tata Consumer Products with Tetley Kombucha captures evolving domestic palates. Increasing awareness of the gut-brain axis heavily influences procurement choices. Urban professionals increasingly seek portable nutrition to combat sedentary lifestyles. Such favorable dynamics are likely to propel massive commercial acceleration.

Europe Fermented Beverages Market Trends

Europe is poised to remain a mature and structurally stable regional market, with demand primarily anchored in premiumization. Deep historical roots heavily influence contemporary consumption of cultured products. This cultural integration guarantees a consistent baseline of recurring revenue. Strict sustainability directives compel ongoing innovation in eco-friendly packaging solutions. Consumers consistently demand verifiable organic certifications across all retail touchpoints. Supermarkets strictly enforce these compliance metrics before authorizing shelf placements. These established preferences remain on track to maintain stable financial trajectories.

Germany is expected to drive consistent volume via ingrained dietary traditions. Robust biological agricultural sectors supply high-quality ingredients for local producers. This reliable sourcing network mitigates exposure to international supply disruptions. MOMO Kombucha with MOMO Organic Kombucha navigates these demanding consumer expectations. Stringent domestic purity laws reinforce exceptional manufacturing standards and quality. Citizens inherently trust specialized apothecary and health food store recommendations. Therefore, strong baseline demand is projected to support continuous profitability.

Competitive Landscape

The global fermented beverages market remains fragmented due to localized taste preferences and regulatory diversity across regions. Leading players exert influence through extensive cold-chain networks and retailer procurement relationships. PepsiCo with KeVita Turmeric-Ginger Kombucha defines functional integration benchmarks within mainstream portfolios. Nestlé with N3 Milk demonstrates precision fermentation capabilities, enhancing protein efficiency. Yakult Honsha with Yakult Probiotic Drink anchors global probiotic consumption standards. Brand equity sustains premium pricing acceptance while capital strength reinforces competitive barriers.

Competitive positioning centers on diversification and supply chain integration to protect margins across segments. GT's Living Foods with SYNERGY Raw Kombucha exemplifies premium dominance through organic certification strategies. Lipton with Lipton Kombucha expands accessibility via cost-efficient scaling approaches. Heineken with Heineken 0.0 sets non-alcoholic beverage benchmarks across global markets. Anheuser-Busch InBev, with Stella Artois Wild, reflects flavor engineering within hybrid fermentation portfolios. Constellation Brands accelerates consolidation through targeted acquisitions in premium kombucha segments.

Key Industry Developments:

- In April 2026, Clean Food Group secured £4.5 million (US$$6.08 million) in funding to complete the scale-up of its high-performance oils and fats fermentation facility. This investment enables the commercialization of sustainable, fermented ingredients for the global food and beverage industry, challenging traditional supply chains.

- In July 2025, PepsiCo launched "Pepsi Prebiotic Cola," the first functional cola in the traditional carbonated category. The product, containing 3 grams of prebiotic fiber and significantly lower sugar, marks a major pivot toward functional fermented-style health benefits within mainstream soda aisles.

Companies Covered in Fermented Beverages Market

- Nestlé S.A.

- Danone S.A.

- PepsiCo, Inc.

- Yakult Honsha Co. Ltd.

- Anheuser-Busch InBev

- Heineken

- Carlsberg Group

- Asahi Group Holdings

- Suntory Holdings

- GT's Living Foods

- Health-Ade LLC

- Brew Dr. Kombucha

- Remedy Drinks

- Tata Consumer Products

- Keurig Dr Pepper

- Lifeway Foods

Frequently Asked Questions

The global fermented beverages market is projected to be valued at US$1.1 trillion in 2026 and is expected to reach US$1.6 trillion by 2033, driven by rising consumer awareness of gut health, urbanization, and advancements in fermentation technology.

Functional nutrition drives the market as consumers increasingly seek proactive health benefits from their diets. Companies like Danone S.A., Yakult Honsha Co., Ltd., and PepsiCo, Inc. are leveraging this shift by offering microbiome-focused and functionally positioned beverages.

The fermented beverages market is forecast to grow at a CAGR of 5.9% from 2026 to 2033, reflecting sustained expansion anchored within specialized dietary consumer demographics and rising demand for non-alcoholic variants.

North America is the leading regional market, accounting for approximately 36% share in 2026, supported by established retail infrastructure and premiumization trends.

The fermented beverages market is fragmented due to localized taste preferences. Key players include Nestlé S.A., Danone S.A., PepsiCo, Inc., Yakult Honsha Co. Ltd., Anheuser-Busch InBev, Heineken, GT's Living Foods, and Tata Consumer Products.