- Medical Devices

- Endoscopic Balloon Dilators Market

Endoscopic Balloon Dilators Market Size, Share, and Growth Forecast, 2025 - 2032

Endoscopic Balloon Dilators Market by Product (Biliary Balloon Dilator, Esophageal Balloon Dilator, Pyloric Balloon Dilator, Colonic Balloon Dilator, Duodenal Balloon Dilator), Modality Type (Single Lumen, Double Lumen), End-use (Hospitals, Ambulatory Surgical Centers, Specialty Centers), and Regional Analysis for 2025 - 2032

Endoscopic Balloon Dilators Market Size and Trend Analysis

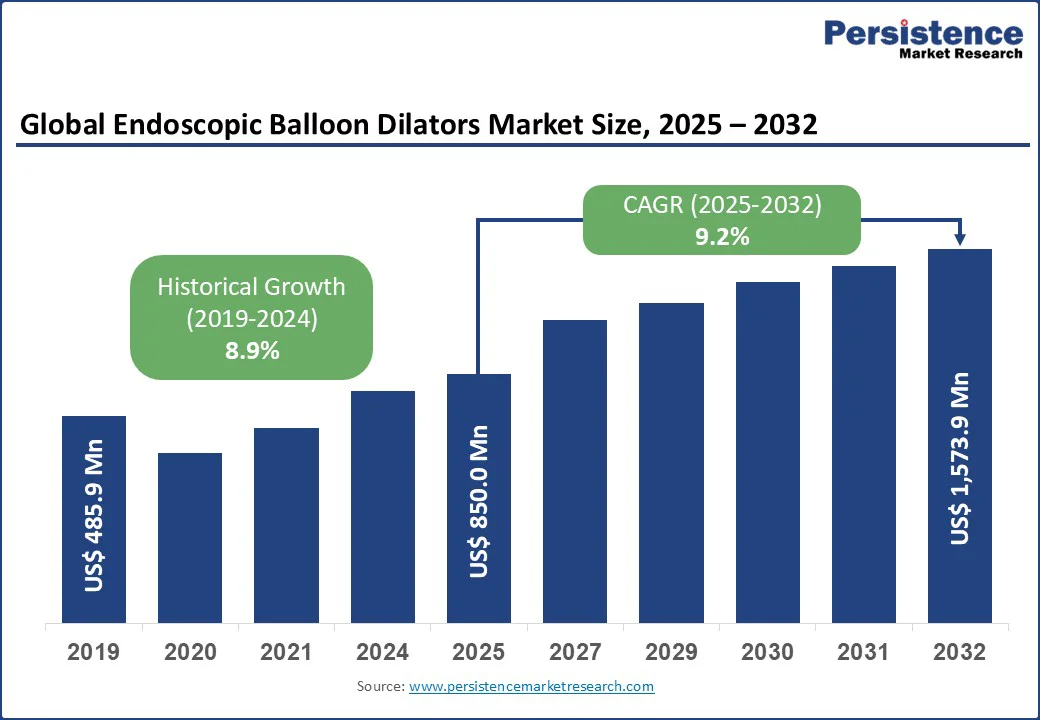

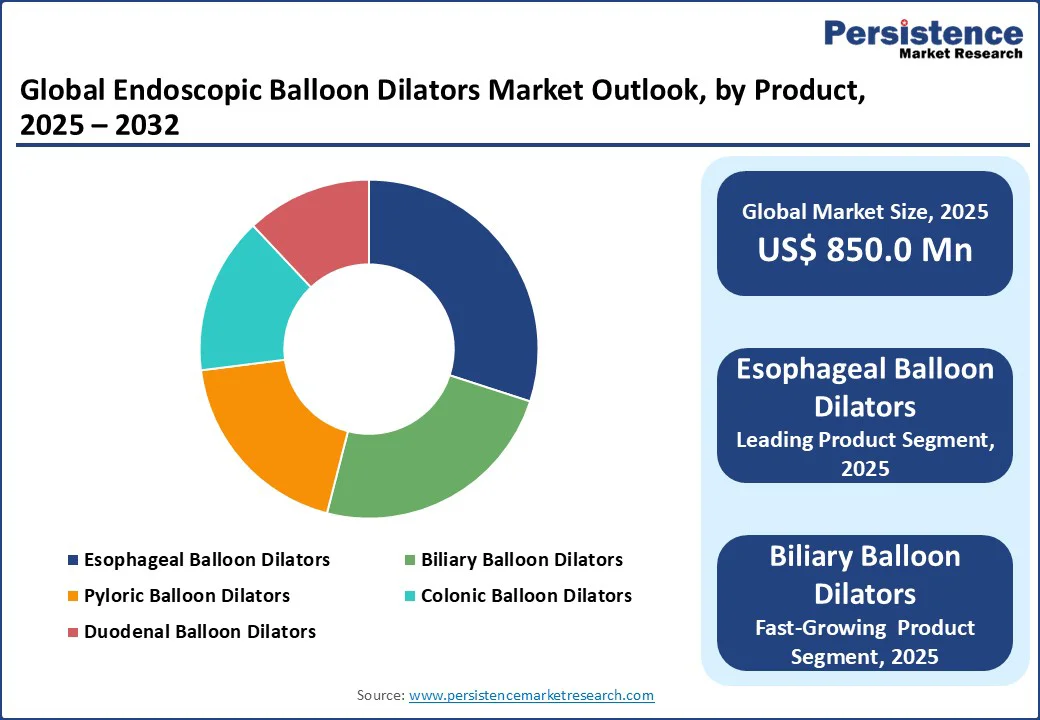

The global endoscopic balloon dilators market is likely to be valued at US$850.0 million in 2025. It is estimated to reach US$1,573.9 million by 2032, growing at a CAGR of 9.2% during the forecast period from 2025 to 2032.

Rising prevalence of gastrointestinal disorders such as achalasia, esophageal strictures, and bile duct obstructions are increasing the need for effective treatment solutions.

Key Industry Highlights:

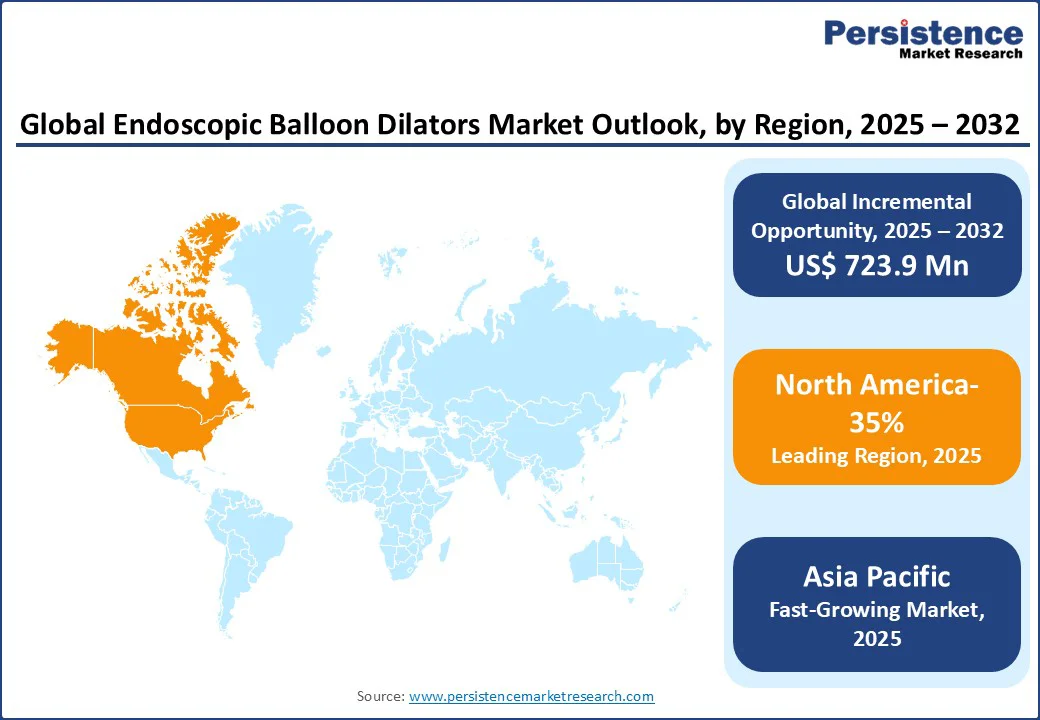

- Leading Region: North America dominates 35% of the global endoscopic balloon dilators market share in 2025, supported by advanced healthcare systems and strong adoption of minimally invasive endoscopic procedures.

- Fastest-Growing Region: Asia Pacific shows the fastest growth, fueled by rising gastrointestinal disorder cases and expanding healthcare access in China and India.

- Dominant Product: Esophageal balloon dilators lead with a 30% share in 2025, driven by their effectiveness in treating achalasia and esophageal strictures.

- Leading Modality Type: Single lumen dilators hold 60% market share, preferred for cost-efficiency and ease of use in standard gastrointestinal interventions.

- Leading End-use: Hospitals dominate with a 65% share, reflecting high patient volumes and advanced clinical infrastructure.

- Key Developments: In December 2023, Medtronic deepened its AI partnership with Cosmo Pharmaceuticals to enhance endoscopy precision, while Boston Scientific’s Hurricane RX biliary dilator with radiopaque markers continues to support safer, more accurate procedures.

|

Global Market Attribute |

Key Insights |

|

Endoscopic Balloon Dilators Market Size (2025E) |

US$850.0 Mn |

|

Market Value Forecast (2032F) |

US$1,573.9 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

9.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

8.9% |

The growing preference for minimally invasive endoscopic procedures further accelerates the adoption of balloon dilators, which offer reduced recovery time and lower complication rates. In addition, continuous technological advancements in balloon dilator design and expanding hospital infrastructure are enhancing procedural precision and accessibility, collectively supporting strong market expansion and wider clinical adoption worldwide.

Market Dynamics

Driver: Rising Prevalence of Gastrointestinal Disorders and Minimally Invasive Procedures

The increasing prevalence of gastrointestinal disorders such as inflammatory bowel disease, gastroesophageal reflux disease, and functional gastrointestinal disorders is a key driver of the endoscopic balloon dilators market. These conditions represent a major healthcare burden worldwide, with growing cases of strictures and motility disorders requiring therapeutic intervention.

For instance, the National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK) reports that digestive diseases account for more than 20 million hospitalizations annually in the United States, underlining the scale of clinical demand for effective treatment options.

In parallel, the healthcare industry is witnessing a steady shift toward minimally invasive procedures, driven by the need for safer treatments, shorter recovery times, and reduced costs. Endoscopic balloon dilation provides a reliable, non-surgical alternative for managing digestive tract narrowing, with high success rates and improved patient comfort.

Hospitals and clinics are increasingly adopting this approach, reinforcing its role in modern gastroenterology. Together, the rise in gastrointestinal disorders and the growing adoption of minimally invasive techniques are expected to accelerate market expansion for endoscopic balloon dilators over the coming years.

Restraint: High Costs and Alternative Treatment Options

One of the major restraints limiting the growth of the endoscopic balloon dilators market is the high cost of procedures and devices. Endoscopic interventions often require specialized equipment, skilled professionals, and hospital infrastructure, leading to higher treatment expenses compared to conventional therapies. In regions with limited healthcare budgets and low reimbursement coverage, these costs can restrict patient access and slow adoption, particularly in developing economies.

In addition to cost concerns, the presence of alternative treatment options such as stent placement, surgical resection, and pharmacological therapies poses a significant challenge to market growth. These options are often perceived as more accessible or cost-effective by patients and healthcare providers, which can reduce reliance on balloon dilation procedures and limit overall market expansion.

Opportunity: Technological Advancements and Emerging Markets

The endoscopic balloon dilators market is expected to benefit significantly from ongoing technological advancements. Innovations in balloon materials, catheter design, and precision inflation systems are improving procedural safety, reducing complications, and enhancing treatment outcomes.

Integration of advanced imaging and real-time monitoring technologies further supports accurate diagnosis and targeted dilation, making these devices more reliable and user-friendly for healthcare providers. Continuous product development by leading manufacturers is likely to drive wider clinical adoption in the coming years.

At the same time, emerging markets in the Asia Pacific, Latin America, and the Middle East are creating lucrative opportunities due to rising healthcare investments, expanding hospital infrastructure, and increasing awareness of minimally invasive treatments. Growing patient populations and government initiatives to strengthen gastroenterology care are expected to accelerate demand.

Category-wise Insights

Product Insights

In 2025, esophageal balloon dilators hold the dominant position with a 30% market share, supported by their extensive use in managing achalasia and esophageal strictures. Their adoption remains strong as esophageal dilation is one of the most common gastrointestinal procedures, accounting for nearly 60% of GI endoscopies in 2024. The rising burden of inflammatory bowel disease, which increased by more than 47% between 1990 and 2019, continues to drive clinical demand for effective esophageal dilation therapies.

Biliary balloon dilators represent the fastest-growing segment, driven by rising cases of bile duct obstruction and related strictures. In 2024 alone, the prevalence of bile duct obstructions rose by around 25%, highlighting the need for minimally invasive treatment options. Their proven effectiveness under fluoroscopic guidance is encouraging broader adoption among gastroenterologists, positioning biliary dilators as a key growth area.

Modality Type Insights

In 2025, single lumen dilators account for the largest market share at 60%, maintaining their leadership due to cost-effectiveness and ease of use in routine gastrointestinal procedures. Their simple design and reliability make them the preferred choice in clinical practice, with nearly 70% of hospitals adopting single lumen dilators for standard GI interventions in 2024. This strong hospital preference continues to reinforce their dominance across global healthcare settings.

On the other hand, double lumen dilators represent the fastest-growing segment, gaining traction in advanced and complex procedures. Their adoption increased by nearly 20% in 2024, supported by advantages such as enhanced precision, better maneuverability, and compatibility with advanced imaging technologies. These benefits position double lumen dilators as an increasingly valuable tool for gastroenterologists handling more challenging therapeutic interventions, driving steady expansion.

End-use Insights

In 2025, hospitals lead the endoscopic balloon dilators market with a dominant 65% share, supported by high patient volumes and advanced infrastructure. Hospitals remain the primary setting for gastrointestinal interventions, with nearly 80% of endoscopic procedures performed in these facilities in 2024. Significant investments in healthcare infrastructure worldwide have further strengthened hospitals’ capacity to adopt advanced endoscopic technologies, reinforcing their leadership position in this segment.

Meanwhile, ambulatory surgical centers (ASCs) are emerging as the fastest-growing end-use segment. A 15% rise in outpatient procedures in 2024 reflects the growing preference for cost-effective care and faster recovery times. ASCs are increasingly equipped with modern endoscopic tools, enabling them to perform a wide range of gastrointestinal interventions. This shift toward outpatient care is driving higher adoption of balloon dilators in ASCs, positioning them as a key growth contributor to the overall market.

Regional Insights

North America Endoscopic Balloon Dilators Market Trends

In 2025, North America holds a leading 35% share of the endoscopic balloon dilators market, driven by high disease prevalence, advanced healthcare infrastructure, and strong adoption of minimally invasive procedures. The region records a significant burden of gastrointestinal disorders, including inflammatory bowel disease and esophageal strictures, creating consistent demand for endoscopic dilation therapies.

Well-established hospitals and specialized endoscopy centers, coupled with favorable reimbursement frameworks, further support the uptake of advanced devices. In addition, ongoing investments in healthcare technology and the presence of key medical device manufacturers strengthen North America’s dominance. Growing awareness of early diagnosis and the shift toward outpatient endoscopic procedures continue to reinforce the region’s position as the largest contributor to global market revenue.

Europe Endoscopic Balloon Dilators Market Trends

Europe accounts for a significant share of the endoscopic balloon dilators market, supported by the rising prevalence of gastrointestinal disorders and the widespread adoption of minimally invasive treatments across the region. The growing incidence of esophageal strictures, achalasia, and bile duct obstructions is driving consistent demand for effective dilation therapies.

Europe also benefits from a strong network of hospitals, specialized gastroenterology clinics, and advanced healthcare infrastructure that facilitate the adoption of innovative endoscopic devices. Favorable regulatory approvals and government initiatives to improve digestive health further strengthen the regional market outlook. Additionally, the presence of leading medical device companies and ongoing clinical research in countries such as Germany, the U.K., and France reinforces Europe’s role as a key contributor to global market growth.

Asia Pacific Endoscopic Balloon Dilators Market Trends

Asia Pacific is the fastest-growing region in the endoscopic balloon dilators market, driven by a rapidly expanding patient population, rising prevalence of gastrointestinal disorders, and increasing adoption of minimally invasive procedures. Countries such as China, India, and Japan are witnessing significant growth in hospital infrastructure and healthcare investments, creating a strong platform for advanced endoscopic technologies.

Rising awareness of early diagnosis, coupled with improving access to specialized gastroenterology care, is further accelerating demand. Additionally, the growing burden of inflammatory bowel disease and biliary disorders across the region is fueling procedure volumes. With supportive government initiatives and expanding medical tourism, the Asia Pacific is positioned as the most dynamic regional market, offering substantial opportunities for manufacturers and healthcare providers alike.

Competitive Landscape

The global endoscopic balloon dilators market shows a competitive environment shaped by continuous product innovation and strategic expansion. Companies are focusing on developing safer, more efficient devices that support minimally invasive procedures and improve patient outcomes.

Growing demand for gastrointestinal treatments is also encouraging investment in research, regulatory approvals, and wider distribution networks. As healthcare systems expand and the need for advanced endoscopic solutions rises, market players are prioritizing technology upgrades and broader accessibility, ensuring steady competition and long-term growth opportunities.

Key Developments

- December 2023: Medtronic strengthened its partnership with Cosmo Pharmaceuticals to advance AI-driven endoscopy solutions, integrating the GI Genius™ intelligent module to improve diagnostic accuracy and procedural outcomes.

- Ongoing: Boston Scientific continues to offer its Hurricane RX biliary balloon dilator, designed with radiopaque markers for enhanced visibility and positioning during procedures, supporting safer and more precise dilation.

Companies Covered in Endoscopic Balloon Dilators Market

- Medi-Globe GmbH

- PanMed US

- Hobbs-Medical Inc

- Olympus Medical Corporation

- Boston Scientific Corporation

- Merit Medical Endotek

- ConMed Corporation

- Cook Medical

- Rockwell Medical

- Fresenius Medical Care AG

- Asahi Kasei Medical Co. Ltd

- B. Braun Melsungen AG

- Envaste Medical Instruments

- Stening SRL

- MicroPort Scientific

- Others

Frequently Asked Questions

The endoscopic balloon dilators market is projected to reach US$850.0 mn in 2025, driven by GI disorder prevalence and minimally invasive procedure adoption.

Rising GI disorders, minimally invasive surgery demand, and technological advancements fuel market growth.

The endoscopic balloon dilators market will grow from US$850.0 mn in 2025 to US$1,573.9 mn by 2032, with a CAGR of 9.2%.

Drug-coated balloons and emerging market expansion drive growth in endoscopic applications.

Leading players include Boston Scientific Corporation, Olympus Medical Corporation, Cook Medical, Medi-Globe GmbH, and Merit Medical Endotek.