- Medical Devices

- Endoscopic Closure Systems Market

Endoscopic Closure Systems Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Endoscopic Closure Systems Market by Product Type (Endoscopic Clips, Endoscopic Suturing Systems, Endoscopic Vacuum-Assisted Closure, Cardiac Septal Defect Occluders, Stapling Devices, and Others), by Application (Gastrointestinal (GI) Bleeding Management, Post-Endoscopic Mucosal Resection (EMR) Closure, Perforation & Fistula Closure, Anastomotic Leak Repair, Bariatric Surgery, and Others) End User, and Regional Analysis from 2026 - 2033

Endoscopic Closure Systems Market Share and Trend Analysis

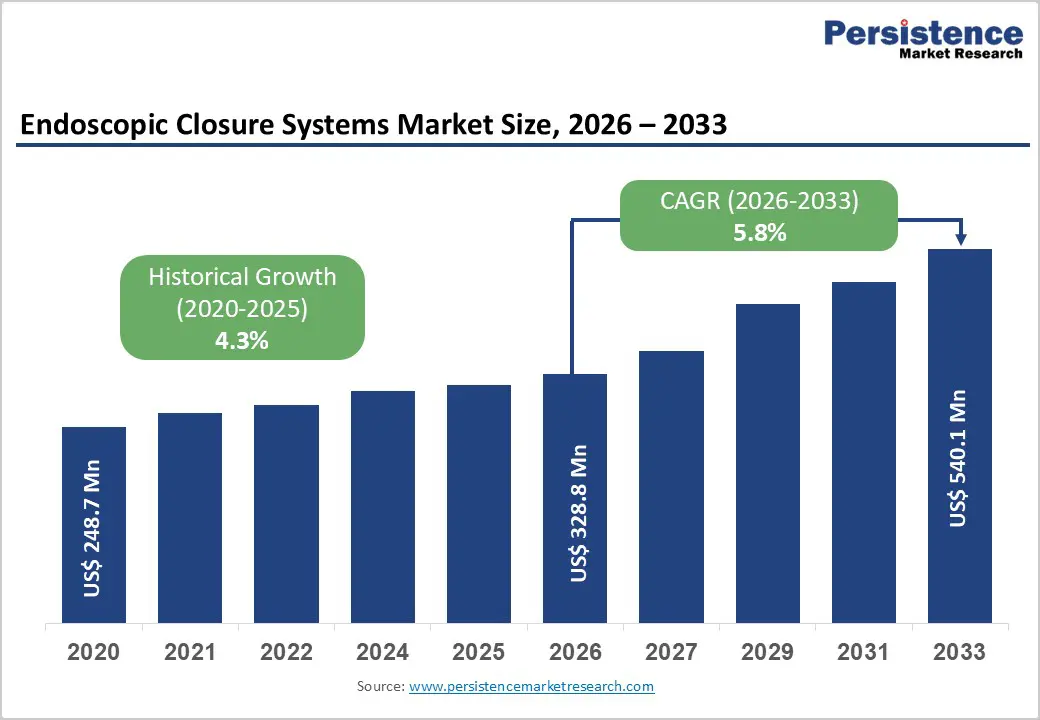

The global endoscopic closure systems market size is estimated to grow from US$ 328.8 million in 2026 to US$ 540.1 million by 2033. The market is projected to grow at a CAGR of 5.8% from 2026 to 2033. The increasing shift toward minimally invasive gastrointestinal procedures and the rising burden of digestive disorders are significantly accelerating the adoption of endoscopic closure systems worldwide. Hospitals, specialty clinics, and ambulatory surgical centers are performing a growing number of therapeutic endoscopic interventions that require effective defect closure, bleeding control, and tissue approximation.

Devices such as clips, suturing systems, and vacuum-assisted solutions enable clinicians to achieve precise closure, reduce complication rates, and improve patient recovery outcomes. These systems are particularly valuable in high-volume settings where consistency, speed, and procedural safety are critical. Simultaneously, continuous advancements in endoscopic technologies are supporting market expansion. Modern closure systems are designed with improved deployment mechanisms, enhanced visualization compatibility, and greater tissue grip strength, allowing for more efficient and reliable performance during complex procedures. As clinical practices evolve toward advanced interventions such as EMR, ESD, and bariatric endoscopy, the need for dependable closure solutions continues to grow. Increasing healthcare investments, expanding endoscopy infrastructure, and rising awareness of minimally invasive treatment benefits are further strengthening global demand.

Key Industry Highlights:

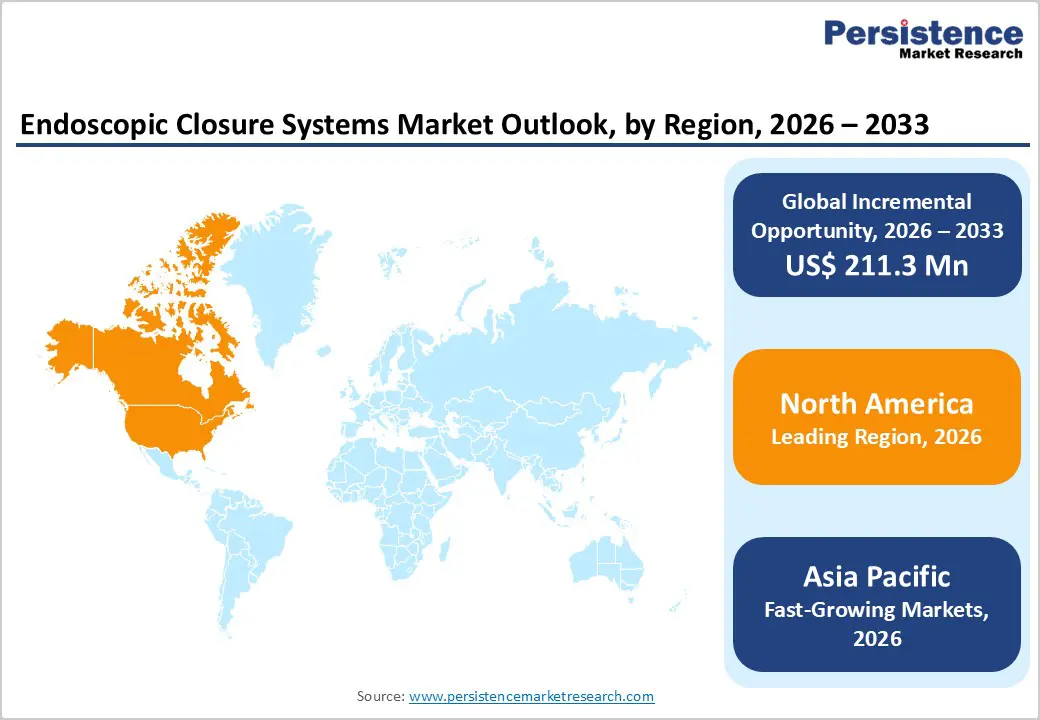

- Leading Region: North America holds 46.7% of the global market, supported by advanced healthcare infrastructure, high procedural volumes, strong reimbursement frameworks, and continuous innovation in endoscopic technologies.

- Fastest-Growing Region: Asia Pacific is witnessing the fastest expansion due to improving healthcare access, rising gastrointestinal disease prevalence, increasing investments in hospital infrastructure, and growing adoption of minimally invasive procedures.

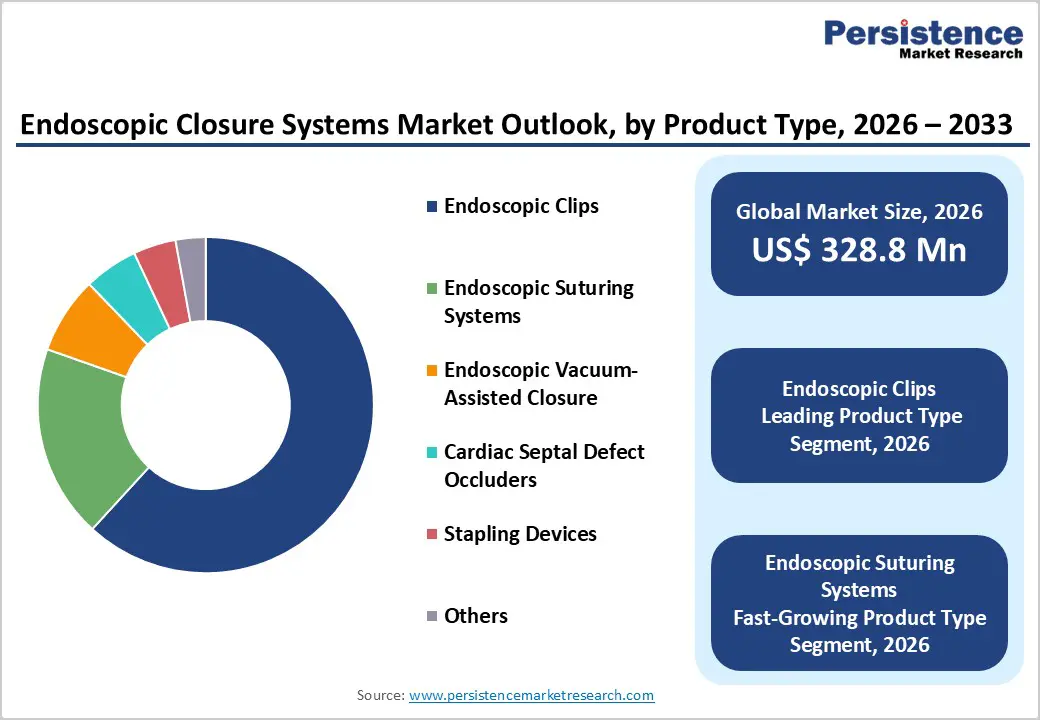

- Leading Product Type Segment: Endoscopic clips account for 42.6% of the market, driven by their widespread clinical use, ease of application, rapid hemostasis capability, and effectiveness in routine endoscopic closure procedures.

- Fastest-Growing Product Type Segment: Endoscopic suturing systems are gaining strong traction as healthcare providers increasingly adopt advanced solutions capable of handling complex closures with greater precision and durability.

- Leading Application Segment: Gastrointestinal (GI) bleeding management represents 36.4% of the market, supported by the high incidence of GI disorders and the need for immediate and effective endoscopic intervention.

- Fastest-Growing Application Segment: Post-endoscopic mucosal resection (EMR) closure is expanding rapidly due to increasing adoption of advanced therapeutic endoscopy and the need for reliable closure following large lesion resections.

| Key Insights | Details |

|---|---|

|

Endoscopic Closure Systems Market Size (2026E) |

US$ 328.8 Mn |

|

Market Value Forecast (2033F) |

US$ 540.1 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

5.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.3% |

Market Dynamics

Driver - Rising Adoption of Minimally Invasive Endoscopic Procedures and Increasing Gastrointestinal Disease Burden

The growing preference for minimally invasive procedures is a key factor accelerating demand for advanced endoscopic closure solutions. Endoscopy has become a standard approach for diagnosing and treating gastrointestinal conditions due to reduced recovery time, lower complication rates, and shorter hospital stays compared to open surgeries. As a result, procedures such as endoscopic mucosal resection (EMR), endoscopic submucosal dissection (ESD), and bariatric endoscopy are increasing globally, all of which require reliable closure techniques to manage defects, bleeding, and perforations. Closure systems such as clips and suturing devices enable precise tissue approximation, improving procedural safety and clinical outcomes.

Additionally, the global rise in gastrointestinal disorders, including colorectal cancer, peptic ulcers, and obesity-related complications, is significantly increasing procedure volumes. Emergency cases such as GI bleeding further necessitate immediate and effective closure solutions. Healthcare providers are increasingly adopting technologically advanced devices that enhance procedural efficiency and reduce reintervention rates. Additionally, improvements in endoscopic training and expanding access to specialized care are supporting wider adoption. These combined factors are driving sustained demand for endoscopic closure systems across both developed and emerging healthcare markets.

Restraints - High Device Costs and Technical Complexity Associated with Advanced Closure Systems

The market faces constraints related to the cost and complexity of advanced endoscopic closure technologies. Devices such as endoscopic suturing systems and over-the-scope clips often involve significant upfront investment, which can limit accessibility for smaller hospitals and healthcare facilities in cost-sensitive regions. In addition to procurement costs, ongoing expenses related to device maintenance, accessory components, and staff training must also be considered, adding to the overall financial burden. Another challenge lies in the technical expertise required to effectively use these systems. Advanced closure procedures demand a high level of endoscopic skill, and inadequate training can lead to suboptimal outcomes or increased procedure time. This creates variability in adoption rates across institutions with differing levels of clinical expertise.

Furthermore, alternative treatment approaches, including surgical interventions or conventional clipping methods, may still be preferred in certain cases due to familiarity and lower cost. Limited reimbursement coverage for some advanced endoscopic procedures in specific regions also acts as a barrier. Collectively, these economic and operational challenges may slow the widespread penetration of premium closure technologies.

Opportunity - Technological Advancements and Expansion of Therapeutic Endoscopy Across Emerging Markets

Continuous innovation in endoscopic technologies is creating substantial growth opportunities for manufacturers of closure systems. The development of next-generation devices, including advanced suturing platforms, enhanced clipping mechanisms, and vacuum-assisted closure systems, is enabling clinicians to perform increasingly complex procedures with improved precision and safety. These innovations are expanding the scope of therapeutic endoscopy beyond traditional applications, allowing for effective management of conditions such as fistulas, leaks, and large mucosal defects without the need for invasive surgery.

Emerging markets are also presenting significant untapped potential as healthcare infrastructure continues to improve. Countries across Asia-Pacific, Latin America, and parts of the Middle East are investing in modernizing hospitals and expanding access to endoscopic services. This is accompanied by a growing patient population, rising healthcare awareness, and increasing demand for cost-effective minimally invasive treatments. Additionally, training programs and international collaborations are enhancing the capabilities of healthcare professionals in these regions. Manufacturers are also focusing on developing user-friendly and cost-efficient devices to cater to diverse market needs. As therapeutic endoscopy gains broader acceptance globally, the demand for innovative and accessible closure solutions is expected to rise steadily.

Category-wise Analysis

By Product Type Insights

Endoscopic clips are projected to account for 61.8% of the global endoscopic closure systems market in 2026, establishing them as the dominant product category. Their leadership stems from widespread clinical use in gastrointestinal procedures where rapid and reliable tissue approximation is required. These devices offer ease of deployment, reduced procedure time, and strong hemostatic capability, making them a preferred first-line solution among endoscopists. Continuous improvements in clip design, including enhanced rotational control, reopening capability, and better tissue grip, are further strengthening their adoption. In addition, compatibility with standard endoscopes and cost-effectiveness compared to advanced suturing systems contribute to their high utilization across hospitals and ambulatory settings. As procedure volumes for GI bleeding and mucosal resections continue to rise globally, endoscopic clips remain the most practical and scalable closure solution.

By Application Insights

Gastrointestinal (GI) bleeding management is expected to hold 28.5% of the global endoscopic closure systems market in 2026, making it the largest application segment. The high prevalence of peptic ulcers, colorectal disorders, and other GI conditions necessitates frequent endoscopic interventions for bleeding control. Closure systems, particularly clips and advanced devices, play a critical role in achieving immediate hemostasis and preventing re-bleeding complications. Increasing adoption of minimally invasive endoscopic therapies, combined with rising emergency admissions related to GI bleeding, is driving consistent demand for these solutions. Moreover, clinical guidelines increasingly recommend endoscopic closure techniques as a standard of care in bleeding management. The growing availability of skilled gastroenterologists and improved access to endoscopy units across healthcare systems further support segment expansion, reinforcing its leading position in the market.

By End-user Insights

Hospitals are anticipated to capture 58.7% of the global endoscopic closure systems market in 2026, making them the leading end-user segment. Their dominance is attributed to the high volume of complex endoscopic procedures performed in hospital settings, including emergency interventions, therapeutic endoscopy, and advanced gastrointestinal surgeries. Hospitals are equipped with specialized endoscopy units, skilled professionals, and access to a broad range of closure devices, enabling them to handle diverse clinical scenarios. Additionally, the presence of reimbursement frameworks and greater capital investment capacity allows hospitals to adopt technologically advanced systems such as suturing platforms and over-the-scope clips. The increasing burden of gastrointestinal diseases and the growing preference for minimally invasive treatments are further driving patient inflow into hospitals. As a result, hospitals continue to serve as the primary hub for endoscopic closure procedures globally.

Regional Insights

North America Endoscopic Closure Systems Market Trends

North America is projected to account for 46.7% of the global endoscopic closure systems market in 2026, maintaining its leadership position. The region benefits from a highly developed healthcare ecosystem, characterized by widespread adoption of advanced endoscopic technologies and strong clinical expertise. The United States, in particular, performs a high volume of gastrointestinal procedures, supported by well-established reimbursement structures that encourage the use of innovative closure devices. Hospitals and specialized endoscopy centers across the region are early adopters of technologies such as endoscopic suturing systems and over-the-scope clips, which enhance procedural outcomes and reduce complication rates.

Additionally, the presence of major medical device manufacturers and continuous product innovation contribute to rapid technology penetration. Training programs and clinical workshops further improve physician proficiency in advanced closure techniques. The rising prevalence of colorectal cancer, obesity-related conditions, and gastrointestinal disorders is increasing the demand for therapeutic endoscopy. Moreover, strong investment in healthcare infrastructure and ongoing research in minimally invasive procedures continue to support market expansion. These factors collectively reinforce North America’s dominance in the global landscape.

Europe Endoscopic Closure Systems Market Trends

Europe represents a well-established market for endoscopic closure systems, supported by advanced healthcare infrastructure and a strong emphasis on clinical quality standards. Countries such as Germany, the United Kingdom, France, and Italy are key contributors, with high adoption of minimally invasive gastrointestinal procedures. The region benefits from a robust network of public healthcare systems, which ensures broad patient access to endoscopic treatments and associated closure technologies.

Clinical practice across Europe is guided by stringent regulatory frameworks and evidence-based guidelines, encouraging the use of reliable and standardized closure devices to improve patient outcomes. Hospitals and specialized centers are increasingly integrating advanced solutions such as endoscopic suturing and vacuum-assisted systems, particularly for complex cases like perforations and fistula management. Additionally, ongoing collaborations between academic institutions and medical device companies are fostering innovation and clinical research in therapeutic endoscopy. The growing aging population and rising incidence of chronic gastrointestinal diseases are further contributing to steady demand. Overall, Europe continues to demonstrate stable growth driven by technological adoption and strong clinical infrastructure.

Asia Pacific Endoscopic Closure Systems Market Trends

Asia Pacific is expected to be the fastest-growing regional market, expanding at a CAGR of approximately 7.9% between 2026 and 2033. Rapid advancements in healthcare infrastructure, combined with increasing awareness of minimally invasive procedures, are significantly driving demand for endoscopic closure systems across countries such as China, India, Japan, and South Korea. Governments in the region are investing heavily in healthcare modernization, leading to the expansion of endoscopy units and improved access to advanced medical technologies.

The region is witnessing a sharp rise in gastrointestinal disorders, including gastric cancer and ulcer-related complications, which is increasing the need for effective endoscopic interventions. In parallel, the growing presence of private healthcare providers and multi-specialty hospitals is accelerating the adoption of advanced closure devices. Training initiatives and international collaborations are enhancing the skill sets of healthcare professionals, enabling wider use of complex procedures such as endoscopic suturing. Furthermore, the expansion of medical tourism and cost-effective treatment options are attracting patients globally. These factors collectively position Asia Pacific as a high-growth market with significant long-term potential.

Competitive Landscape

The global endoscopic closure systems market is highly competitive, with strong participation from CooperSurgical, Inc., STERIS, Life Partners Europe (LPE), Ovesco Endoscopy AG, Boston Scientific Corporation, and Abbott Laboratories. These companies leverage strong distribution networks, physician training programs, and continuous innovation in clips, suturing systems, and advanced closure technologies to strengthen market presence.

Rising demand for minimally invasive procedures and increasing gastrointestinal interventions are encouraging manufacturers to develop advanced closure systems with improved precision, ease of deployment, and enhanced patient outcomes, supporting efficient defect closure and procedural success.

Key Developments:

- In March 2026, Seger Surgical Solutions Ltd., a leader in minimally invasive surgical innovation, announced the successful completion of three first-in-human procedures as part of a clinical trial evaluating its proprietary SEGER IDEA™ laparoscopic bowel closure device. The surgeries were performed at Zacamil Hospital in El Salvador and mark a significant milestone in advancing fully intracorporeal anastomosis (IA), a technique that enables bowel closure to be performed entirely within the body.

- In March 2026, the Green Healthcare Scotland programme, led by the Centre for Sustainable Delivery (CfSD) and hosted by NHS Golden Jubilee, was expanded to include renal and endoscopy services. These areas are among the most resource-intensive in healthcare delivery. The initiative builds on the National Green Theatres Programme, which aimed to reduce waste and energy consumption in hospitals while maintaining high standards of patient care.

- In June 2025, Intrinsic Therapeutics, a medical technology company focused on improving outcomes for lumbar discectomy patients with large annular defects, announced the first implantation of its Barricaid Annular Closure Device using an endoscopic approach. The procedure was performed by Daniel E. Choi, MD, FAAOS, a Harvard-trained, board-certified orthopedic spine surgeon, at Gramercy Surgery Center in New York.

Companies Covered in Endoscopic Closure Systems Market

- CooperSurgical, Inc.

- STERIS

- Life Partners Europe (LPE)

- Ovesco Endoscopy AG

- Boston Scientific Corporation

- Abbott Laboratories

- Olympus Corporation

- Medtronic

- Teleflex Incorporated

- B. Braun SE

- Johnson & Johnson Services, Inc. (Ethicon)

- Cook

- CONMED Corporation

- ERBE Elektromedizin GmbH

- Micro-Tech (Nanjing) Co., Ltd.

- Others

Frequently Asked Questions

The global endoscopic closure systems market is projected to be valued at US$ 328.8 Mn in 2026.

Rising gastrointestinal disease burden, increasing minimally invasive endoscopic procedures, aging population, and continuous technological advancements in closure devices are driving market growth.

The global endoscopic closure systems market is poised to witness a CAGR of 5.8% between 2026 and 2033.

Expansion of therapeutic endoscopy, growing screening volumes, guideline-supported defect closure, and innovation in AI-enabled and advanced suturing technologies are creating significant market opportunities.

CooperSurgical, Inc., STERIS, Life Partners Europe (LPE), Ovesco Endoscopy AG, Boston Scientific Corporation, and Abbott Laboratories are some of the key players in the endoscopic closure systems market.