- Plastics, Polymers & Resins

- Inflammatory Bowel Disease Market

Inflammatory Bowel Disease Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Inflammatory Bowel Disease Market Size by Disease Type (Crohn's Disease, Ulcerative Colitis), Drug Class (Aminosalicylates, Corticosteroids, Others), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Others), and Regional Analysis for 2025 - 2032

Inflammatory Bowel Disease Market Share and Trends Analysis

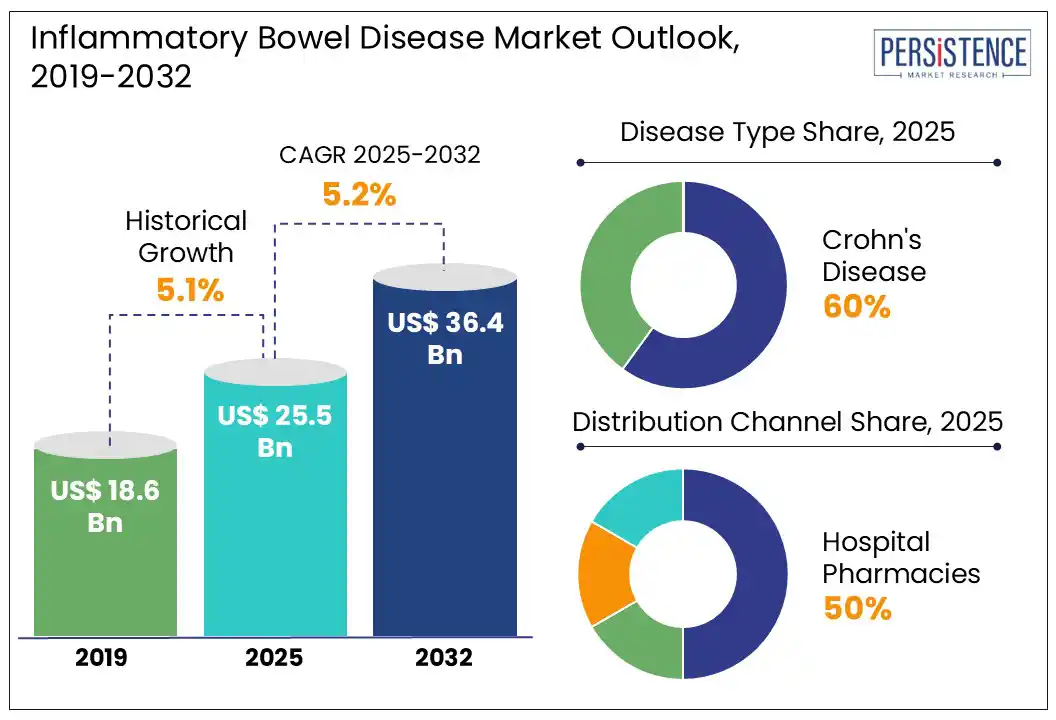

The global inflammatory bowel disease market size is likely to be valued at US$ 25.5 Bn in 2025 and is estimated to reach US$ 36.4 Bn by 2032, growing at a CAGR of 5.2% during the forecast period 2025−2032. The inflammatory bowel disease market is making steady headway, fueled by the rise in global prevalence of Crohn's disease and ulcerative colitis. A study published in The Lancet revealed that in 2023, ulcerative colitis affected around 5 million individuals around the world, and the incidence of the condition is growing.

The Global Burden of Disease Study 2019 estimated that nearly 5 million people suffered from Crohn’s disease in 2019. This surge in cases is driving the demand for advanced inflammatory bowel disease (IBD) therapies that improve symptom management and patient outcomes. A major trend shaping the inflammatory bowel disease therapeutics market is the growing inclination toward personalized medicine. This trend is being increasingly supported by innovations in genetic testing, biomarker analysis, and pharmacogenomics. These advancements have enabled tailored treatment strategies that enhance efficacy and minimize side effects. The future of IBD treatment is anticipated to involve biologics, immunomodulators, smart drug delivery systems, and digital health platforms.

Key Industry Highlights:

- The inflammatory bowel disease market is increasingly focusing on patient-centric care, mental health support, and holistic management strategies.

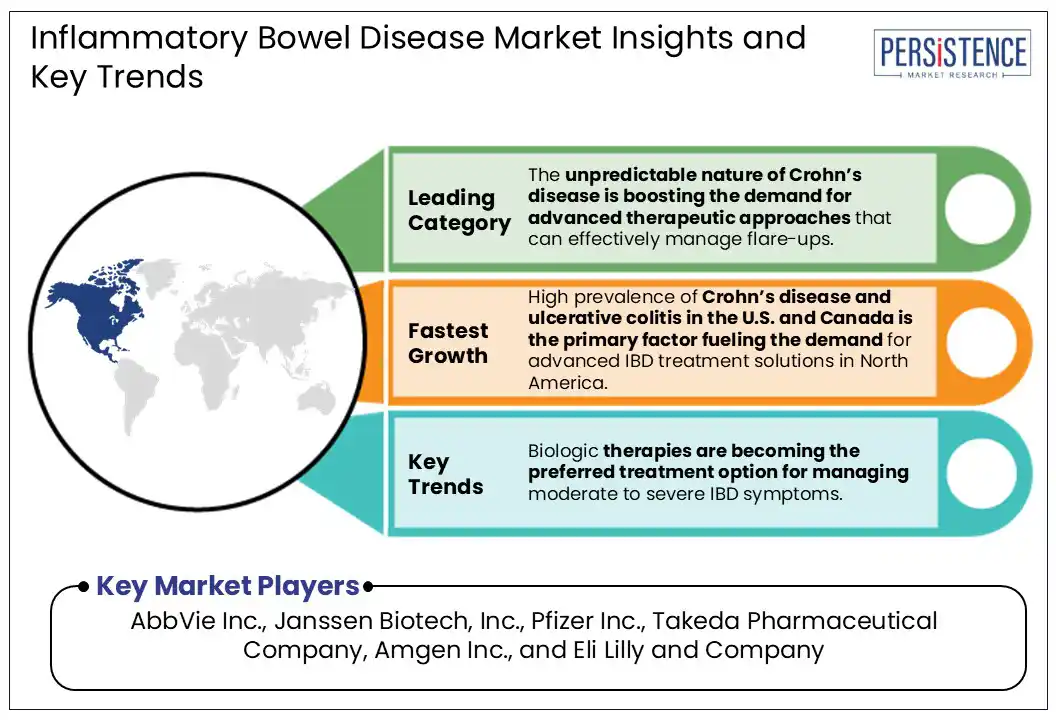

- The Crohn’s disease segment holds a significant share of the IBD therapeutics market.

- North America is anticipated to lead the inflammatory bowel disease market in 2025, with approximately 49.6% market share.

- There is a growing trend toward early diagnosis and timely intervention in inflammatory bowel disease cases.

- Hospital pharmacies are projected to play an increasingly vital role in the market, accounting for nearly 50% of the revenue share in 2025.

- Biologic therapies are becoming the preferred treatment option for managing moderate to severe IBD symptoms.

- Leading companies driving innovation in the market include AbbVie Inc., Janssen Biotech, Inc., Pfizer, Inc., and Takeda Pharmaceutical Company.

|

Global Market Attribute |

Key Insights |

|

Inflammatory Bowel Disease Market Size (2025E) |

US$ 25.5 Bn |

|

Market Value Forecast (2032F) |

US$ 36.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.1% |

Market Dynamics

Driver - Increasing Incidence of IBD to Stoke Market Growth

The inflammatory bowel disease market is transforming as a result of the rising prevalence of IBD across the globe and the urgent need for effective long-term treatment strategies. The Global Burden of Disease Study 2019 found that between 1990 and 2019, individuals suffering from IBD rose from 3.3 million to 4.9 million. Healthcare providers are actively adopting comprehensive care models that combine pharmacological therapies, lifestyle changes, and surgical interventions to manage conditions such as ulcerative colitis. This growing demand is encouraging pharmaceutical companies to intensify their R&D efforts, which is creating exciting opportunities for developing innovative IBD treatment options and harnessing the market potential.

A discernible trend in the IBD therapeutics market is the shift toward early detection and preventive care. Routine screenings, low-FODMAP diets, and personalized medicine, including genetic screening and microbiome analysis, are gaining traction, as they are tangibly improving patient outcomes. With healthcare systems prioritizing proactive management of IBD, this market is slated to enter a rapid expansion phase.

Restraint - Adverse Effects of Known IBD Treatments to Stifle the Market

The inflammatory bowel disease market growth, while catching speed, faces grave challenges due to the adverse side effects and complications caused by existing treatment options. For example, corticosteroids, commonly used for acute flare management in Crohn’s disease and ulcerative colitis, are known to have risk factors associated with them, such as osteoporosis, weight gain, and immune suppression. Immunomodulators such as thiopurines present risks of a different kind, including hepatotoxicity and increased vulnerability to infections, posing questions on their long-term viability in treating inflammatory bowel disease. Biologic therapies, though effective, are associated with infusion reactions and a notably high susceptibility to infection, with their high cost becoming another significant barrier, especially in emerging markets. These limitations highlight the urgent need for innovation in the inflammatory bowel disease therapeutics market.

Opportunity - Introduction of Low-cost IBD Therapies to Accelerate Market Expansion

The above-mentioned hurdles present excellent opportunities for innovation for players in the IBD market. These can be seen through the development of cost-effective therapies aimed at improving treatment accessibility globally. While biologics remain central to IBD treatment, their high costs have narrowed their uptake. However, the advent of biosimilars offers a promising solution by maintaining efficacy while reducing costs of biologic drugs, thereby enhancing affordability for patients and easing the financial burden on healthcare systems.

In addition to biosimilars, the expansion of generic formulations of established drugs such as mesalazine further bolsters cost-effective treatment strategies. The integration of digital health technologies, including remote monitoring and telemedicine, has also led to enhanced patient outcomes and reduced healthcare expenditures, driving the inflammatory bowel disease market.

Category-wise Insights

Disease Type Insights

Based on disease type, the IBD market is segmented into Crohn’s disease and ulcerative colitis. Crohn’s is poised to account for a significant share of 60% in 2025 in the inflammatory bowel disease market. The disease is known for its complex and variable clinical manifestations causing symptoms such as abdominal pain, diarrhea, fatigue, and weight loss, necessitating robust and adaptable treatment strategies. The unpredictable nature of Crohn’s disease is also boosting the demand for advanced therapeutic approaches that can effectively manage flare-ups and sustain remission.

Key growth drivers in the Crohn’s disease treatment market include the increasing adoption of biologic therapies that target specific immune pathways and the rising preference for personalized medicine. Innovations in genetic profiling and biomarker-based treatment plans are further elevating therapeutic precision, improving patient outcomes, and expanding the inflammatory bowel disease market scope.

Distribution Channel Insights

Hospital pharmacies, retail pharmacies, e-commerce platforms, and others are the main segments, based on distribution channel, for this market. Hospital pharmacies are projected to play an increasingly vital role in the market, accounting for nearly 50% of the revenue share in 2025. Their importance stems from the complexities involved in IBD management, which requires coordinated care from acute diagnosis to long-term treatment. Hospitals offer access to advanced therapies such as biologics, immunomodulators, and intravenous treatments, which are typically administered under professional supervision, making them central to effective IBD care delivery.

Hospitals also enable effective collaboration among gastroenterologists, surgeons, and nutritionists, enabling personalized treatment plans for inflammatory bowel disease. Healthcare systems are prioritizing specialized services for chronic illnesses, and hospitals will remain the nucleus in this process as they ensure an uninterrupted access to high-quality care and drive improved patient outcomes across diverse population.

Regional Insights

North America Inflammatory Bowel Disease Market Trends

At 49.6%, North America is anticipated to lead the inflammatory bowel disease market share in 2025. High prevalence of Crohn’s disease and ulcerative colitis in the region, particularly in the U.S. and Canada, is the primary factor fueling the demand for advanced IBD treatment solutions. Early diagnosis, widespread awareness, and a robust healthcare infrastructure contribute to North America's dominance in the management of inflammatory bowel disease.

Additionally, massive investments in biologic therapies, immunomodulators, and personalized medicine, supported by access to clinical trials and innovative treatment options, are the other factors contributing to the dominance of North America in the IBD market. Supporting these are the comprehensive healthcare reimbursement systems and insurance coverage that ensure affordability and accessibility to high-cost therapies in the region.

Asia Pacific Inflammatory Bowel Disease Market Trends

Asia Pacific is poised to exhibit significant growth in 2025, driven by improvements in healthcare infrastructure, rising awareness about IBD, and widening access to world-class treatments. Large economies, mainly China, Japan, India, and South Korea, are witnessing a surge in Crohn’s disease and ulcerative colitis cases attributed to rampant urbanization, changing dietary patterns, and an increasing recognition of IBD among healthcare professionals. This growing demand for effective IBD therapeutics is prompting pharmaceutical companies to tap into these markets by investing in regional expansion and conducting clinical research. The adoption of biologic therapies and personalized treatment approaches is also increasing in the region, attracting strong support from evolving policy frameworks. As a result, the Asia Pacific region is emerging as a key growth hub in the inflammatory bowel disease market.

Competitive Landscape

The competitive landscape of the global inflammatory bowel disease market is recalibrated by strategic acquisitions, partnerships, and continuous innovation. Leading pharmaceutical companies, such as Pfizer and AbbVie, are actively collaborating with other competitors to strengthen their research capabilities and diversify their product portfolios, particularly in the areas of biologic therapies and personalized medicine for Crohn’s disease and ulcerative colitis. These alliances are accelerating the development and commercialization of advanced inflammatory bowel disease treatment options.

Moreover, companies are aggressively enhancing their production capacities to meet the growing demand for IBD therapeutics. This includes scaling up manufacturing for biologics, biosimilars, and immunomodulators, as well as integrating digital health solutions for remote monitoring and patient engagement.

Key Industry Developments

- In April 2025, Parvus Therapeutics Inc. and AbbVie Inc. announced that their investigational drug candidate, PVT-401, a novel peptide-major histocompatibility complex (pMHC) nanomedicine known as a Navacim, successfully met predefined nonclinical pharmacology and manufacturing benchmarks.

- In May 2025, the UK’s Medicines and Healthcare Products Regulatory Agency (MHRA) approved guselkumab (Tremfya) as the first IL-23 inhibitor for moderate-to-severe Crohn’s disease and ulcerative colitis, in both intravenous and subcutaneous formulations.

Companies Covered in Inflammatory Bowel Disease Market

- AbbVie Inc.

- Janssen Biotech, Inc.

- Pfizer Inc.

- Takeda Pharmaceutical Company Limited

- Ferring Pharmaceuticals

- Amgen Inc.

- Eli Lilly and Company

- Novartis AG

- Bristol-Myers Squibb

- Johnson & Johnson

- Merck & Co., Inc.

- GlaxoSmithKline plc

Frequently Asked Questions

The inflammatory bowel disease market is projected to reach US$ 25.5 Bn in 2025.

The rising prevalence of IBD across the globe and the urgent need for effective long-term treatment strategies are driving the market.

The inflammatory bowel disease market is poised to witness a CAGR of 5.2% from 2025 to 2032.

The introduction of low-cost IBD therapies and the expansion of generic formulations of established drugs are key market opportunities.

AbbVie Inc., Janssen Biotech, Inc., and Pfizer Inc. are some of the key players in the market.