- HVAC

- Dust Control Market

Dust Control Market Size, Share, and Growth Forecast 2026–2033

Dust Control Market by Product Type (Wet Scrubbers, Wet Electrostatic Precipitators (WESP/WEPS), Water Spray Systems, Fogging & Mist Systems, Bag Dust Collectors, Cyclone Dust Collectors, Electrostatic Dust Collectors, Vacuum Dust Collectors, Cartridge Dust Collectors, Others), Technology (Filtration Systems, Electrostatic Systems, Vacuum-based Systems, Water-based Dust Suppression Systems, Hybrid Systems), Mobility Type, Application, End-user, and Regional Analysis for 2026–2033

Dust Control Market Size and Trend Analysis

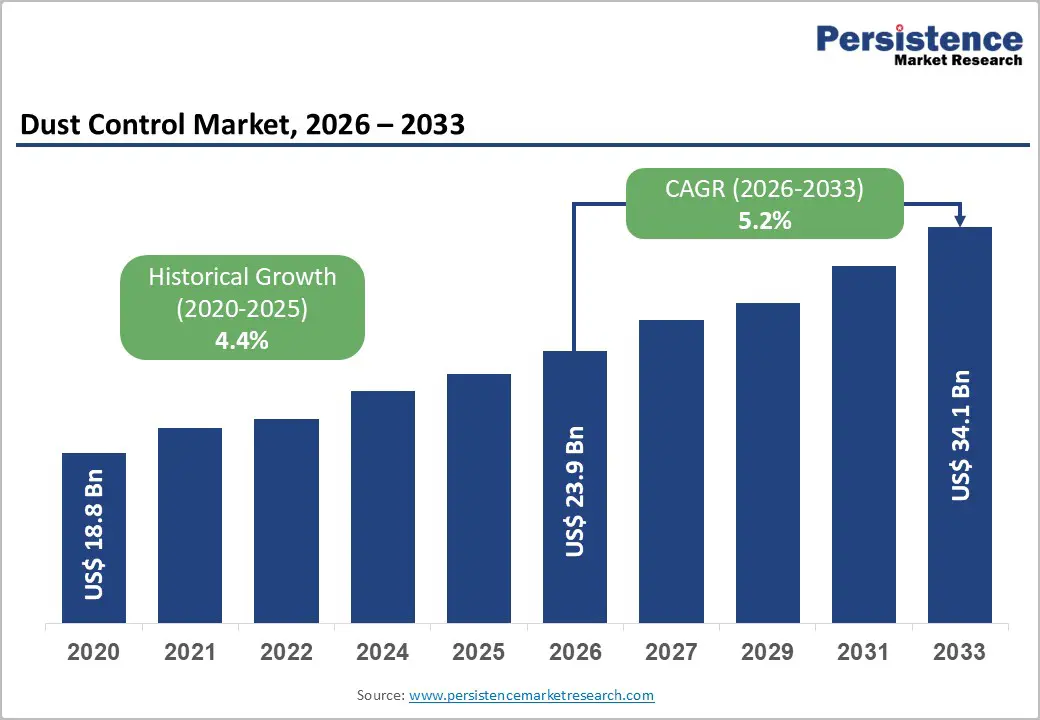

The global Dust Control market size is valued at US$ 23.9 billion in 2026 and is projected to reach US$ 34.1 billion, growing at a CAGR of 5.2% between 2026 and 2033.

Dust control involves the use of specialized technologies, equipment, and operational practices to minimize or suppress airborne dust particles such as silica, soil, ash, and industrial particulates. It plays a critical role in maintaining air quality, protecting worker and public health, ensuring regulatory compliance, and improving operational safety and visibility across construction sites, mining operations, industrial facilities, and transportation corridors.

According to the United Nations, nearly 2 billion tons of dust are released into the atmosphere annually, equivalent to the weight of approximately 307 Great Pyramids of Giza. More than 80% of global dust emissions originate from North African and Middle Eastern deserts; however, dust pollution has become a global environmental challenge affecting over 150 countries and nearly 330 million people worldwide.

The market is being propelled by tightening occupational health and environmental regulations globally, rapid industrialization across emerging economies, and expanding construction and mining activity. Regulatory frameworks such as the U.S. Occupational Safety and Health Administration (OSHA) silica dust standard and the European Union Industrial Emissions Directive (IED) are compelling industries to adopt advanced dust suppression technologies. Simultaneously, infrastructure investments under programs such as India's National Infrastructure Pipeline (NIP) and the U.S. Infrastructure Investment and Jobs Act are generating sustained demand for mobile and fixed dust control solutions across construction and municipal applications.

Market Dynamics

Drivers - Stringent Regulatory Standards for Industrial Air Quality and Worker Safety

Regulatory mandates are the most powerful catalyst driving investment in dust control equipment worldwide. In the United States, OSHA's Respirable Crystalline Silica Standard (29 CFR 1910.1053), effective since 2018, reduced the permissible exposure limit (PEL) for silica dust to 50 µg/m³, half the previous limit, obligating construction contractors, foundries, and cement plants to install engineering controls such as wet suppression systems, local exhaust ventilation, and high-efficiency bag filters.

The European Union's IED (Directive 2010/75/EU) and associated Best Available Techniques Reference Documents (BREFs) impose binding emission limit values on particulate matter for large combustion plants, cement kilns, and metal-processing facilities. Similarly, China's Ministry of Ecology and Environment (MEE) introduced ultra-low emission standards for the steel and cement sectors in 2019, mandating total suspended particulate (TSP) concentrations below 10 mg/Nm³. These overlapping national and supranational frameworks create a persistent baseline of demand for Bag Dust Collectors, Wet Electrostatic Precipitators (WESPs), and advanced fogging systems, locking in multi-year capex cycles across heavy industry.

Accelerating Construction, Mining, and Infrastructure Activity in Emerging Economies

Construction and mining activities are the two largest end-use applications for dust control, collectively accounting for over 40% of global equipment demand. The United Nations Environment Programme (UNEP) estimates that construction activity alone generates approximately 40% of global particulate matter emissions in urban areas.

Infrastructure programs in Asia Pacific are particularly impactful: India's National Infrastructure Pipeline targets US$ 1.4 trillion in capital expenditure through 2025, while the Asian Development Bank (ADB) projects ASEAN infrastructure investment needs at US$ 210 billion annually through 2030. Mining sector growth, particularly iron ore, coal, and non-ferrous metals in Australia, South Africa, and Chile is driving high adoption of mobile and portable dust suppression rigs equipped with water spray and fogging systems. These structural trends ensure that demand for dust control solutions remains robust across forecast years, especially in fast-developing geographies where regulatory enforcement is also intensifying.

Restraints -High Capital and Maintenance Costs of Industrial Dust Control Systems

Advanced dust control equipment, particularly Bag Dust Collectors and Wet Electrostatic Precipitators demands significant upfront capital outlay and ongoing maintenance expenditures. Industrial-grade bag filter systems for cement or steel plants can cost between US$ 250,000 and US$ 2 million. Filter bag replacement alone for large installations often runs US$ 50,000–US$ 200,000 per cycle. Small and medium-sized enterprises (SMEs), which constitute the majority of manufacturers in developing economies, frequently defer investments or opt for lower-efficacy, non-compliant methods. According to the International Finance Corporation (IFC), access to affordable green industrial finance remains a key bottleneck in Sub-Saharan Africa and Southeast Asia, constraining market penetration.

Water Availability Constraints Limiting Wet Dust Suppression Adoption

Wet dust suppression systems, including fogging, misting, and water spray systems, depend on a continuous water supply that may be unavailable or prohibitively expensive in arid regions. The United Nations World Water Development Report 2023 notes that over 2 billion people live in water-stressed countries, many of which overlap with regions of high mining and construction activity, such as the Middle East, North Africa, and parts of Southern Africa. Mining sites in these geographies must either transport water at significant cost or rely entirely on dry filtration alternatives, restricting the addressable market for water-based systems and inflating total project costs.

Opportunities - Rising Adoption of Smart and IoT-integrated Dust Monitoring and Control Systems

The convergence of Industry 4.0 and environmental compliance is creating substantial demand for intelligent, sensor-driven dust control systems. IoT-enabled dust monitors can provide real-time particulate concentration data, triggering automated suppression responses and reducing water or energy consumption by up to 30–40% compared to fixed-schedule systems. The U.S. Environmental Protection Agency (EPA)'s ongoing development of low-cost sensor networks for ambient air quality monitoring is encouraging site operators to integrate digital monitoring with suppression equipment. In 2024, the International Labour Organization (ILO) published updated guidance on real-time occupational dust monitoring, further accelerating enterprise adoption. Manufacturers offering connected, data-driven systems, particularly for mining and cement applications, can command premium margins and long-term service contracts. The rapid proliferation of 5G industrial networks and edge computing platforms is expected to further lower the cost barrier for smart dust control integration, making it accessible even to mid-market operators across the Asia Pacific and Latin America.

Growth of Pharmaceutical and Food & Beverage Industries Driving Demand for High-purity Filtration

The pharmaceutical and food and beverage (F&B) sectors are among the fastest-growing end-users of specialized dust control systems, requiring solutions that comply with Good Manufacturing Practice (GMP) and food safety regulations. The U.S. Food and Drug Administration (FDA)'s 21 CFR Part 211 and the European Medicines Agency (EMA) guidelines require pharmaceutical manufacturers to maintain stringent airborne particulate limits in cleanroom environments. Similarly, the FDA Food Safety Modernization Act (FSMA) mandates controls against cross-contamination from airborne particulates in food processing.

The global pharmaceutical manufacturing market is projected to grow at a CAGR of approximately 7% through 2030 (World Health Organization data), creating compounding demand for high-efficiency Cartridge Dust Collectors and HEPA-grade vacuum systems. Companies that tailor offerings to these regulated verticals, including hygienic design, rapid filter changeout, and validation documentation support are well-positioned to capture above-market growth in these high-value application segments.

Category-wise Analysis

Product Type Insights

Dry dust control systems dominate the product type segment, accounting for approximately 62% of the global dust control market in 2026. Within this category, bag dust collectors represent the largest sub-segment, driven by their high collection efficiency (typically 99–99.9% for fine particulates), versatility across industries, and ability to operate without water, a critical advantage in water-scarce regions.

According to the U.S. EPA, fabric filter (baghouse) technology is the most widely specified air pollution control device for industrial point sources in North America. Cement, steel, and power generation sectors are the primary adopters, owing to regulatory requirements for PM10 and PM2.5 compliance. The maturity of the technology, the wide availability of replacement filter bags, and compatibility with industrial automation systems further cement its leading position. Cyclone Dust Collectors hold a secondary share, used as pre-separators to extend bag filter life in high-dust-load environments such as woodworking and grain handling.

Fogging & mist systems represent the fastest-growing sub-segment within Wet Dust Control Systems, projected to expand at a CAGR of approximately 6.8% through 2033. This growth is fueled by the rising adoption of high-pressure atomization technology in construction demolition, quarrying, and transfer point dust suppression. Fogging systems offer low water consumption typically 60–80% less than conventional sprays while achieving effective suppression of sub-micron particles, making them particularly attractive in water-stressed regions.

Technology Insights

Filtration systems represent the leading technology segment, holding approximately 45% share of the dust control market. This dominance reflects the widespread deployment of bag filters, cartridge collectors, and panel filters across industrial processes where dry capture of fine and ultrafine dust particles is required. Filtration technology is integral to regulatory compliance across a broad spectrum of sectors.

The American Conference of Governmental Industrial Hygienists (ACGIH) recommends filtration as the primary engineering control for respirable dust exposures, reinforcing its position as the default technology choice. Advances in membrane filter media, nanofiber coatings, and pulse-jet cleaning automation have improved filtration efficiency while reducing operating costs. The integration of filter condition monitoring sensors, enabling predictive maintenance is extending the appeal of filtration systems into smart factory contexts. Electrostatic Systems (including Dry and Wet ESPs) hold the second-largest share, particularly in power generation and chemical industries where high gas volumes and continuous operation favor electrostatic precipitation.

Hybrid systems combining filtration with electrostatic or water-based suppression represent the fastest-growing technology segment, projected to grow at a CAGR of approximately 7.1% through 2033. Their ability to handle variable dust loads and meet multiple regulatory thresholds simultaneously is driving adoption in complex industrial environments such as steel recycling, hazardous waste incineration, and pharmaceutical API manufacturing.

Mobility Type Insights

Fixed dust control systems dominate the mobility type segment, representing approximately 68% of the market. Fixed systems integrated into plant infrastructure at design or retrofit stages are preferred in large-scale, continuous-process industries such as cement manufacturing, power generation, and metal smelting. Their higher throughput capacity, lower operating cost per unit of cleaned air, and integration with existing process control systems make them the default choice for stationary industrial sources. Permanence of installation also aligns with multi-year permit compliance cycles, making fixed systems a lower-risk procurement decision for plant operators. The U.S. EPA National Emission Standards for Hazardous Air Pollutants (NESHAP) explicitly mandates continuous emission monitoring on fixed sources, reinforcing the dominance of permanently installed systems.

Mobile/portable dust control systems are the fast-growing segment in this category, with an estimated CAGR of 6.5% through 2033. The growth is underpinned by expanding construction, demolition, and road maintenance activity globally, where project-based deployments require flexible, relocatable suppression units. Portable fogging cannons and wheeled vacuum dust collectors are witnessing strong uptake across quarrying and event remediation applications.

Application Insights

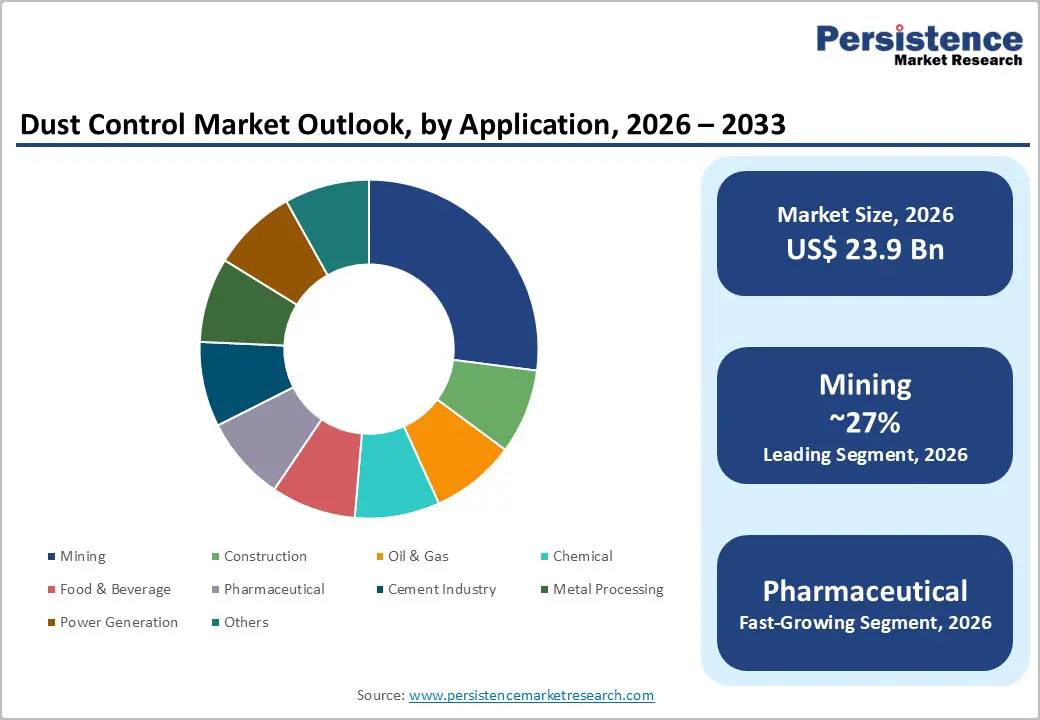

Mining is the leading application segment in the dust control market, commanding approximately 27% share in 2026. Mining operations generate substantial volumes of respirable and nuisance dust at every stage blasting, crushing, conveying, and stockpiling requiring comprehensive, multi-point suppression strategies. The Mine Safety and Health Administration (MSHA) in the U.S. enforces a 1.5 mg/m³ PEL for coal dust and 0.1 mg/m³ for respirable crystalline silica at metal/non-metal mines, driving mandatory equipment investment.

The International Council on Mining and Metals (ICMM) has committed member companies to real-time dust monitoring and suppression as part of its health and safety performance standards. Major producers in Australia, Chile, and South Africa are upgrading legacy spray systems to precision fogging and enclosed conveyor belt vacuum systems, generating significant replacement demand.

The pharmaceutical sector is the fast-growing application segment, projected at a CAGR of 7.5% through 2033. The expansion of API manufacturing capacity in India and China, combined with tightening GMP enforcement by the U.S. FDA and EMA, is driving procurement of contained cartridge filtration and HEPA-grade vacuum systems tailored to cleanroom dust management.

End-user Insights

Industrial is the dominant end-use segment, accounting for approximately 52% of the total dust control market. Industrial facilities including steel mills, cement plants, chemical processing units, pharmaceutical factories, food processing plants, and power generation stations operate under the most stringent ambient air quality and occupational exposure standards, necessitating continuous, high-capacity dust management systems.

The International Energy Agency (IEA) reported that global industrial energy consumption rose 3.4% in 2023, reflecting recovery and expansion of manufacturing activity, which directly translates into growing point-source dust generation. Industrial operators are also subject to permit renewal cycles and third-party environmental audits that drive periodic system upgrades. The sheer scale and diversity of industrial dust generation sources from kiln exhaust to grinding operations ensures that industrial end-user remains the market's dominant value pool throughout the forecast period.

Municipal is among the fastest-growing end-use segments, with a projected CAGR of 6.3%. Rapid urbanization, road dust management programs, and growing awareness of PM2.5-related health burdens are motivating city governments to deploy mobile fogging vehicles and road wetting systems, particularly in South Asia and the Middle East where ambient dust levels frequently exceed WHO air quality guidelines.

Regional Insights

North America Dust Control Market Trends

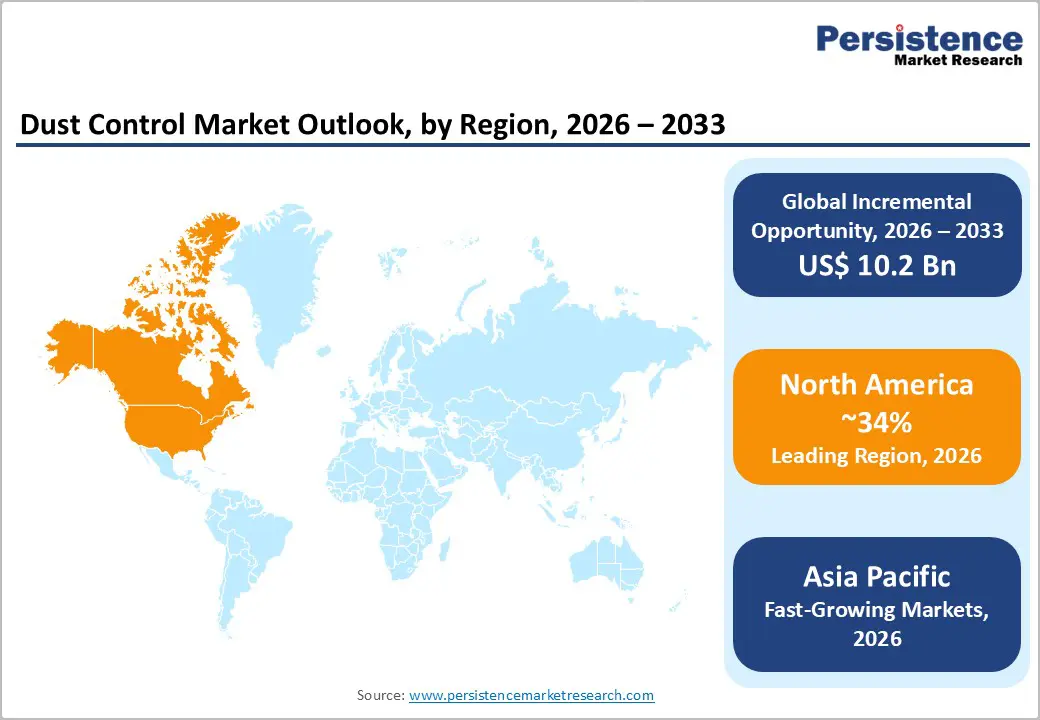

North America holds the largest share of the global dust control market at approximately 34% in 2026, underpinned by mature regulatory infrastructure, high industrial activity, and widespread adoption of advanced emission control technologies. The region benefits from one of the most comprehensive air quality regulatory frameworks globally, including OSHA's silica and coal dust standards, the EPA's National Ambient Air Quality Standards (NAAQS), and the MSHA dust PEL requirements. These mandates continuously stimulate replacement and upgrade cycles for installed dust control equipment.

The U.S. Infrastructure Investment and Jobs Act (2021), with its US$ 1.2 trillion allocation for roads, bridges, ports, and broadband, has generated substantial downstream demand for mobile dust suppression systems at construction sites. Canada's active mining sector particularly oil sands in Alberta and metallic mineral mining in Ontario and Quebec supports strong demand for wet scrubbers and water spray systems. Mexico's expanding manufacturing base, particularly in automotive and chemical processing, is also contributing to regional growth.

U.S. Dust Control Market: The Largest and Most Regulated Market in North America

The United States accounts for approximately 78% of the North America dust control market and is expected to reach a CAGR of 4.8%. The country's dominance is driven by the breadth and enforcement rigor of its occupational and environmental regulations. The U.S. EPA has set binding PM2.5 NAAQS of 9 µg/m³ (revised 2024), among the tightest globally, compelling industrial operators to retrofit older particulate control systems. The American Lung Association's 'State of the Air 2024' report identified over 119 million Americans living in counties with unhealthy particle pollution, creating policy and reputational pressure on industry to invest in best-in-class dust suppression. The construction, mining, and cement sectors collectively represent the majority of procurement activity. The mature equipment market also supports a large installed base requiring regular maintenance, filter replacement, and technology upgrades sustaining a significant aftermarket revenue pool.

Europe Dust Control Market Trends

Europe represents the second-largest regional market, accounting for approximately 26% share globally in 2026. The region is characterized by a high level of regulatory harmonization through the EU Industrial Emissions Directive (IED), the Ambient Air Quality Directives (2008/50/EC), and the European Green Deal's zero-pollution action plan, which targets a 55% reduction in premature deaths from air pollution by 2030. These regulatory imperatives are accelerating the replacement of legacy dust control infrastructure with high-efficiency systems.

Germany leads European adoption of electrostatic and hybrid filtration systems, particularly in automotive manufacturing and chemical processing. The U.K. Health and Safety Executive (HSE) continues to enforce strict Workplace Exposure Limits (WELs) for wood dust (3 mg/m³), silica (0.1 mg/m³), and flour dust (1 mg/m³), sustaining demand across the woodworking, food, and construction sectors. France and Spain are investing in cement plant modernization and decarbonization, creating co-investment opportunities for Bag Dust Collector and WESP retrofits.

Germany: Europe's Industrial Dust Control Powerhouse Driven by Advanced Manufacturing

Germany accounts for approximately 22% of the European dust control market and is projected to grow at a CAGR of 4.5% through 2033. As Europe's largest industrial economy, Germany's extensive automotive manufacturing (Volkswagen, BMW, Mercedes-Benz), chemical processing (BASF, Covestro), and steel production (ThyssenKrupp) generate significant and sustained dust control equipment demand. Germany's Bundes-Immissionsschutzgesetz (BImSchG), its Federal Immission Control Act imposes plant-level emission limits more stringent than EU minimums, driving adoption of advanced dry electrostatic precipitators and hybrid filtration systems. The country's Energiewende transition away from coal power is simultaneously reducing some legacy ESP demand while creating retrofit opportunities at remaining thermal plants.

U.K.: Regulatory-driven Demand for Dust Control Across Construction and Agri-food Sectors

The United Kingdom holds approximately 15% of the European dust control market, projected to grow at a CAGR of 4.2% through 2033. The U.K. HSE's strict enforcement of WELs and the Control of Substances Hazardous to Health (COSHH) regulations are the primary demand drivers. The ongoing HS2 high-speed rail project and residential housing expansion under the Levelling Up agenda are sustaining demand for mobile dust suppression equipment at construction sites. The food manufacturing sector a major U.K. industrial employer represents a growing market for Cartridge Dust Collectors and HEPA vacuum systems under Food Standards Agency (FSA) compliance requirements.

France: Cement and Chemical Industry Modernization Fueling Dust Control Investments

France represents approximately 13% of the European dust control market, with a forecast CAGR of 4.3%. The country's cement industry, led by Lafarge (Holcim) and Vicat, is undergoing significant emission control upgrades under IED-aligned National Action Plans, driving procurement of Bag Dust Collectors and WESPs. France's Plan de rénovation énergétique de l'industrie (industrial energy renovation plan) is channeling funds into clean production technologies, of which advanced dust control is a key component. Chemical industry clusters in the Rhône Valley and Normandy represent additional demand centers for enclosed filtration systems.

Italy: Strong Demand from Ceramic, Stone Processing, and Metal Manufacturing Sectors

Italy accounts for approximately 11% of the European dust control market, with an estimated CAGR of 4.0% through 2033. Italy's distinctive industrial profile including world-renowned ceramic tile manufacturing (Sassuolo district), marble and stone processing (Carrara), and precision metal engineering (Northern Industrial Triangle) generates specialized requirements for Cartridge Dust Collectors, vacuum systems, and water suppression units tailored to abrasive dust environments.

The Italian National Institute for Insurance against Accidents at Work (INAIL) has issued sector-specific guidance on silica and ceramic dust, promoting investment in engineering controls. Italy's National Recovery and Resilience Plan (NRRP/PNRR), funded by EU NextGenerationEU, includes environmental compliance investments for SME manufacturers.

Asia Pacific Dust Control Market Trends

Asia Pacific is the fastest-growing regional market, anticipated to expand at a CAGR of 6.1% through 2033, and holds approximately 29% of the global market in 2026. The region's growth is powered by large-scale industrialization, rapidly expanding construction activity, tightening national air quality standards, and government-led smart city and clean air programs. China, India, Japan, and ASEAN nations collectively represent the dominant demand centers.

China's Ministry of Ecology and Environment's Action Plan on Air Pollution Prevention and Control has driven mandatory retrofitting of dust control systems across steel, cement, and coking coal sectors. India's National Clean Air Programme (NCAP), targeting a 40% reduction in PM concentrations across 131 non-attainment cities by 2026, is catalyzing procurement of both fixed and mobile dust suppression equipment. In ASEAN, rapid construction of industrial parks in Vietnam, Indonesia, and Thailand is generating strong first-time installation demand.

China: Mega-scale Industrial Emission Controls Transforming Dust Suppression Technology Adoption

China is the single largest country market in Asia Pacific for dust control, representing approximately 38% of regional demand, growing at a CAGR of 5.9% through 2033. China's steel sector, producing over 1 billion tonnes annually (World Steel Association) is the world's largest single point-source dust generator, mandating WESPs, bag filters, and enclosed conveyor systems. The Ministry of Housing and Urban-Rural Development (MOHURD) requires mandatory dust suppression at all active construction sites in 339 prefecture-level cities. China's domestic manufacturers of dust control equipment including CECO Environmental Corp. local subsidiaries and Jiangsu Hengrui, are rapidly gaining competitiveness, particularly at the mid-market price point.

India: National Clean Air Mission Catalyzing Unprecedented Dust Control Infrastructure Growth

India represents approximately 18% of Asia Pacific dust control market share, with a forecast CAGR of 7.2% among the highest globally. The Central Pollution Control Board (CPCB) and state pollution control boards have significantly increased enforcement activity under the Environment Protection Act, 1986, particularly targeting cement plants, brick kilns, thermal power stations, and construction sites. India's rapid cement capacity expansion the country is the world's second-largest cement producer, is a key driver of Bag Dust Collector demand. Urban municipal procurement of dust suppression vehicles (fog cannons, water tankers) for PM2.5 management is an emerging demand stream in the NCAP-designated non-attainment cities.

South Korea: Precision Manufacturing and Semiconductor Industry Driving High-purity Dust Control Demand

South Korea accounts for approximately 10% of the Asia Pacific dust control demand, growing at a CAGR of 5.4%. The country's advanced manufacturing base, including semiconductor fabrication (Samsung Electronics, SK Hynix), display manufacturing (LG Display), and shipbuilding (HD Hyundai, Hanwha Ocean) requires ultra-clean air environments. Cleanroom dust control and vacuum filtration systems are in high demand across the semiconductor and pharmaceutical sectors. South Korea's Ministry of Environment-led voluntary agreements with conglomerates on PM2.5 reduction further reinforce industrial dust control investment. The steel industry (POSCO) is also upgrading to advanced WESPs to meet upgraded emission standards under Korea's Clean Air Conservation Act.

Competitive Landscape

The global dust control market exhibits a moderately fragmented competitive structure, with a mix of global conglomerates, specialized environmental technology firms, and regional manufacturers. The top 10 companies collectively account for approximately 40–45% of global market revenue, while the remainder is distributed among hundreds of local and regional players. Market leaders differentiate through technology portfolio breadth (covering both wet and dry systems), aftermarket service capabilities, compliance expertise, and digital integration.

Key competitive strategies include geographic expansion into high-growth emerging markets, vertical integration with filter media or water treatment, and R&D investment in IoT-connected and energy-efficient systems. Emerging business model trends include outcome-based service contracts (dust-as-a-service), equipment leasing for project-based applications, and bundled monitoring and suppression offerings targeting smart manufacturing and smart city clients.

Key Developments:

- In May 2026, DustSentinel Environmental Systems Limited launched DustSentinel-LX, an advanced lunar dust ingress monitoring and containment subsystem designed for lunar habitats, airlocks, suitports, and pressurized rovers to improve astronaut safety and respirable dust event management.

- In March 2025, Emerson introduced a new Dust Collector Monitoring and Control solution designed to automate filtration management, improve environmental compliance, reduce maintenance costs, and minimize operational downtime across multiple industrial sectors handling particulate emissions.

- February 2025: Nederman Holding AB announced the acquisition of a leading ASEAN-based industrial filtration distributor, strengthening its Asia Pacific service network and expanding its Bag Dust Collector installed base in the region.

- September 2024: CECO Environmental Corp. launched its next-generation Peerless Faber cartridge dust collector line with integrated IoT dust monitoring, targeting the pharmaceutical and food processing verticals with GMP-compliant documentation capabilities.

- March 2023: Camfil introduced its Farr Gold Series high-efficiency cartridge collector designed for metal processing and battery manufacturing dust, offering 99.9%+ filtration efficiency for sub-micron particles addressing the rapidly growing EV battery plant dust management segment.

Companies Covered in Dust Control Market

- Donaldson Company, Inc.

- Camfil AB

- Nederman Holding AB

- AAF International

- Parker Hannifin Corporation

- MANN+HUMMEL Group

- CECO Environmental Corp.

- Atlas Copco AB

- FLSmidth & Co. A/S

- Dustcontrol AB

- Imperial Systems, Inc.

- Keller Lufttechnik GmbH + Co. KG

- Sly Inc.

- Amano Corporation

- Babcock & Wilcox Enterprises, Inc.

Frequently Asked Questions

The global dust control market is valued at US$ 23.9 Bn in 2026 and is projected to reach US$ 34.1 Bn by 2033, growing at a CAGR of 5.2%.

The primary growth drivers are stringent occupational and environmental regulations including OSHA's silica PEL of 50 µg/m³, the EU IED, and China's MEE ultra-low emission standards combined with rapid industrialization and large-scale infrastructure investment across Asia Pacific and Latin America. The rise of smart, IoT-integrated suppression systems and growing demand from pharmaceutical and F&B sectors are additional accelerators.

Dry dust control systems, specifically bag dust collectors are the dominant product type, holding approximately 38% share of the overall market. Their dominance is attributed to high filtration efficiency (99–99.9%), independence from water supply, broad regulatory endorsement by OSHA and EPA, and applicability across cement, steel, power generation, and pharmaceutical sectors.

North America is the leading region with approximately 34% of global share in 2026. The United States accounts for ~78% of North America demand, driven by comprehensive regulatory enforcement under OSHA, EPA, and MSHA, a large installed industrial base with active replacement cycles, and infrastructure spending under the U.S. Infrastructure Investment and Jobs Act.

The integration of IoT and smart sensor technologies into dust monitoring and suppression systems represents the most significant market opportunity. Connected systems reduce water and energy consumption by up to 30–40%, while generating recurring revenue through service contracts. Additionally, the pharmaceutical and food & beverage sectors growing at CAGRs of 7.5% and ~6% respectively through 2033 offer above-market growth potential for high-purity, GMP-compliant dust control solutions.

Leading companies in the dust control market include Nederman Holding AB (Sweden), CECO Environmental Corp. (USA), Camfil AB (Sweden), Donaldson Company, Inc. (USA), Parker Hannifin Corporation (USA), Bühler AG (Switzerland), Schenck Process Holding GmbH (Germany), BossTek (USA), and Spraying Systems Co. (USA), among others. These companies compete on technology breadth, compliance expertise, global service networks, and digital integration capabilities.