- Automotive

- Driver Training Simulator Market

Driver Training Simulator Market Size, Share, and Growth Forecast 2026 - 2033

Driver Training Simulator Market by Simulator Type (Fixed-Base Simulators, Motion-Based Simulators, VR/AR Headset-Based Simulators, Full-Cab / Retrofit Cab Simulators, Cloud / SaaS Simulators (Virtual Simulators)), by Application (Research & Testing, Training, Motor Sports & Gaming), by Vehicle Type (Passenger, Motorcycles, Specialized Vehicles, Truck & Bus, Others), by Regional Analysis, 2026 - 2033

Driver Training Simulator Market Size and Trend Analysis

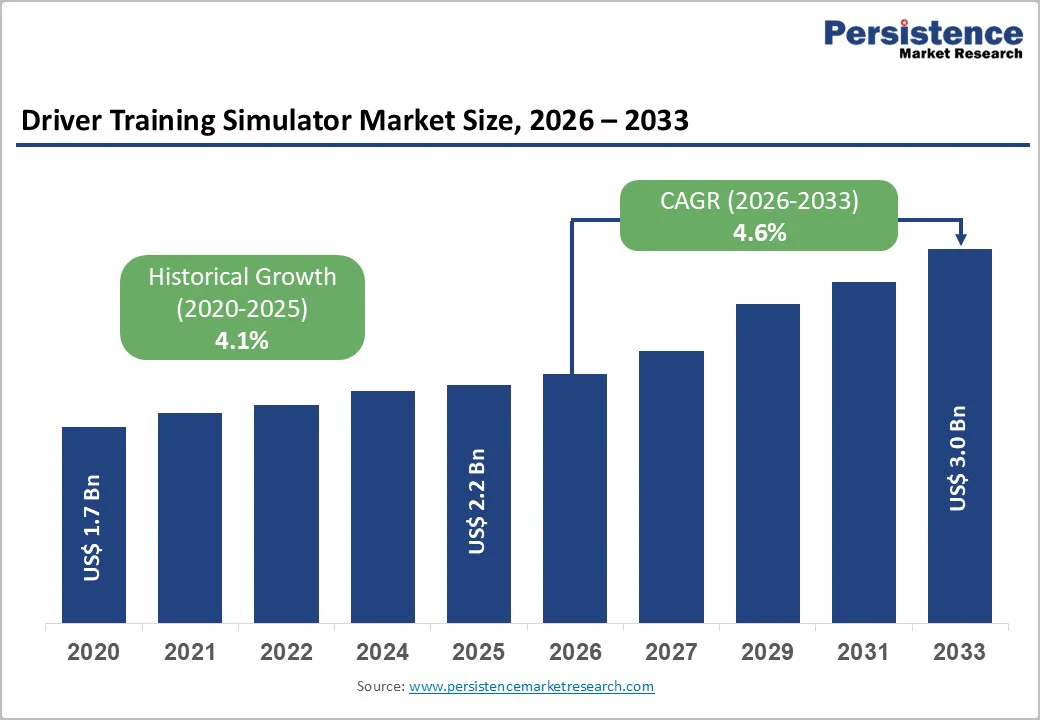

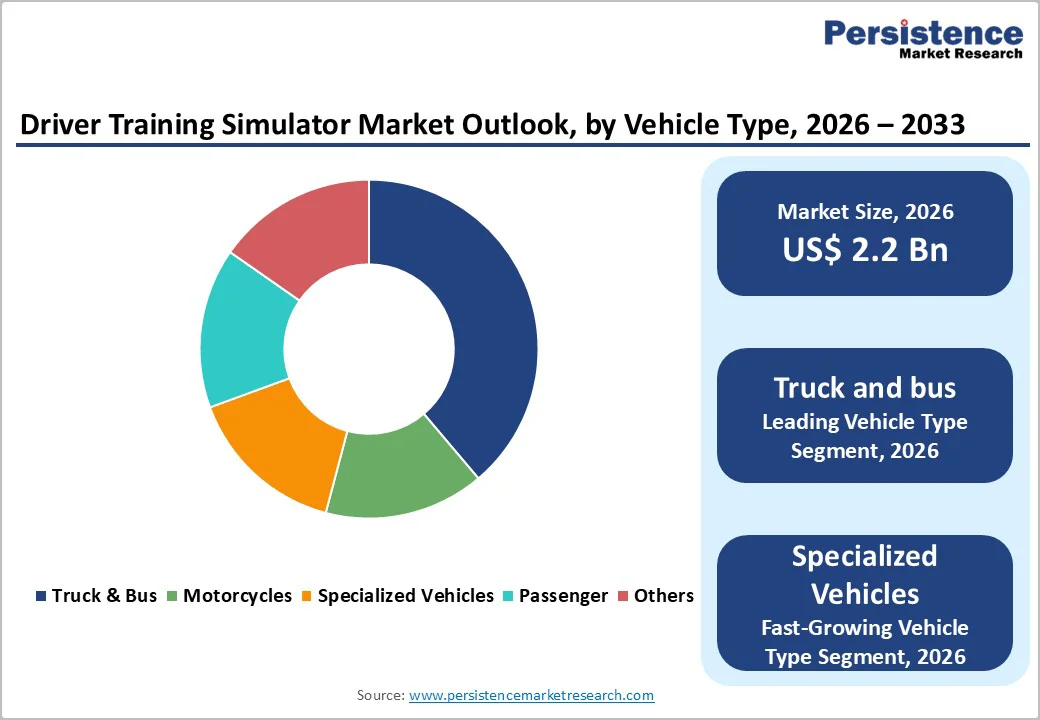

The global driver training simulator market is projected to be valued at US$ 2.2 Bn in 2026 and is projected to reach US$ 3.0 Bn by 2033, growing at a CAGR of 4.6% between 2026 and 2033.

This steady expansion reflects the growing emphasis on road safety regulations worldwide and the increasing adoption of advanced simulation technologies for driver education and professional training. Regulatory frameworks such as European Directive 2003/59/EC mandate professional driver training and periodic recertification, creating sustained demand for cost-effective, scalable training solutions. Additionally, automotive manufacturers and research institutions are leveraging simulator technology to accelerate the development and validation of Advanced Driver Assistance Systems (ADAS) Calibration Equipment and autonomous vehicle functions, further driving market growth across multiple end-user segments.

Key Industry Highlights:

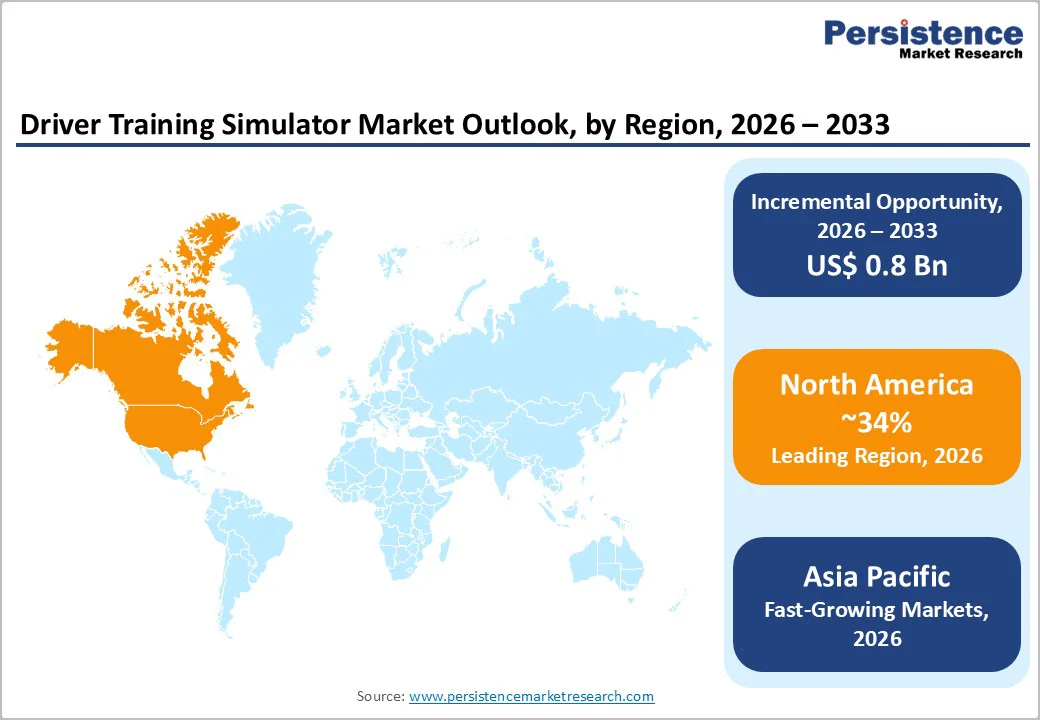

- Leading Region: North America leads the driver training simulator market with a 34% share in 2025, supported by strong simulation technology capabilities, advanced research ecosystems, and progressive ADAS and autonomous vehicle regulations.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with a projected 6.8% CAGR from 2026 - 2033, propelled by urbanization, rising vehicle ownership, infrastructure expansion, and government-backed road safety initiatives.

- Dominant Segment: Fixed-Base Simulators dominate the market, with a 45% share in 2025, due to their cost efficiency, low maintenance requirements, and effectiveness in meeting procedural training and compliance requirements.

- Fastest Growing Segment: VR/AR Headset-Based Simulators are the fastest-growing segment with an expected 8.2% CAGR through 2033, driven by rapid technology improvements, declining device costs, and suitability for distributed training setups.

- Key Market Opportunity: Expanding deployment for ADAS and autonomous vehicle development testing presents substantial growth potential, enabling simulator manufacturers to diversify into higher-value engineering applications alongside traditional training markets.

| Key Insights | Details |

|---|---|

| Driver Training Simulator Market Size (2026E) | US$ 2.2 Bn |

| Market Value Forecast (2033F) | US$ 3.0 Bn |

| Projected Growth CAGR (2026 - 2033) | 4.6% |

| Historical Market Growth (2020 - 2025) | 4.1% |

Market Dynamics

Drivers - Stringent Road Safety Regulations and Professional Driver Training Requirements

Global road safety initiatives and regulatory mandates are significantly driving the expansion of the driver training simulator market. Directive 2003/59/EC of the European Parliament requires professional drivers of goods and passenger vehicles to complete 35 hours of periodic training every five years to maintain their Certificate of Professional Competence (CPC). According to the World Health Organization (WHO), traffic accidents remain among the leading causes of death globally, with road traffic injuries accounting for substantial annual fatalities.

European Union member nations have embraced simulator-based training, with countries including France, the Netherlands, Denmark, and Norway allowing up to 8 hours of the mandatory training to be completed on simulators. The American Trucking Associations and similar regulatory bodies worldwide are advocating for enhanced driver training curricula that incorporate simulation technology to address the critical shortage of skilled professional drivers and improve road safety outcomes. These regulatory frameworks create recurring revenue opportunities for simulator manufacturers and training center operators.

Technological Advancements in Virtual Reality and Motion Simulation Platforms

Rapid technological innovation in Virtual Reality (VR), Augmented Reality (AR), and motion cueing systems is transforming the capabilities and market attractiveness of driver training simulators. Studies from Michigan State University’s Spartan Motorsport Lab have validated that full motion simulators significantly increase predictive steering accuracy and visual load response among trainees. Companies such as Moog Inc. have developed advanced 6-Degree-of-Freedom (6DOF) electric motion platforms capable of supporting payloads ranging from 1,000 kg to 16,000 kg, delivering acceleration forces up to 1g and velocities of 9 m/s, thereby creating highly realistic driving sensations.

The integration of NVIDIA autonomous vehicle simulation platforms and AI-driven training analytics is enabling personalized learning pathways and real-time performance assessment. VR-based driving simulators can replicate over 1,000 distinct driving scenarios, including tire blowouts, brake failures, and adverse weather conditions, providing risk-free exposure to dangerous situations. These technological capabilities are making simulators increasingly attractive to driving schools, fleet operators, and automotive research facilities seeking cost-effective alternatives to traditional on-road training.

Restraints - High Initial Capital Investment and Infrastructure Requirements

The substantial upfront costs of acquiring and deploying advanced driving simulators pose significant barriers to market adoption, particularly in developing economies and smaller training institutions. Professional-grade motion-based simulators incorporating Williams Advanced Engineering platforms and high-fidelity visual systems can represent capital expenditures exceeding several hundred thousand dollars per unit. Bosch Rexroth high-performance driving simulators featuring X-Y table motion systems measuring 18 m x 15 m with hexapod and rotating yaw table configurations require specialized facility infrastructure, climate control, and power distribution systems. Installation timelines can extend beyond 12 months for complex integrated systems, creating opportunity costs for training organizations. The recurring maintenance costs for automotive actuators, servo motors, and visual projection systems, combined with software licensing fees, further strain operational budgets.

Complexity of Replicating Real-World Driving Dynamics and Validation Challenges

Despite significant technological progress, accurately simulating complex road environments, vehicle dynamics, and human factors interactions remains technically challenging and impacts user acceptance. Automotive engineers at Kempten University of Applied Sciences, working with AB Dynamics advanced vehicle driving simulators, have identified that achieving correlation between simulated and real-world vehicle behavior requires extensive calibration and validation against proving ground data. The Netherlands and other European countries have noted the absence of standardized regulations defining simulator specifications and training syllabi, creating inconsistencies across training providers and hindering quality assurance. Research institutions emphasize that simulator validation requires comparing driver performance metrics between virtual and real-world environments, a resource-intensive process. These technical and regulatory uncertainties can slow adoption rates among conservative training organizations and regulatory authorities.

Opportunity - Expanding Deployment for ADAS and Autonomous Vehicle Development Testing

The rapid advancement of autonomous driving technologies and ADAS features is creating substantial opportunities for driving simulator applications beyond traditional driver training. Waymo’s autonomous vehicles have logged over 20 million miles on public roads but tens of billions of miles in virtual test drives, demonstrating the critical role of simulation in validating safety-critical systems. BMW Group, in partnership with Bosch Rexroth and AV Simulation, has deployed high-fidelity and high-dynamic simulators specifically designed to evaluate autonomous vehicle performance across highway and urban driving scenarios. The European Commission and automotive manufacturers are investing heavily in driver-in-the-loop (DIL) simulation to accelerate development cycles and reduce dependence on costly physical prototypes. Companies like IPG Automotive report that their CarMaker simulation software enables comprehensive ADAS testing through flexible scenario generation and sensor simulation, supporting development from concept through validation.

Growth in Commercial Fleet Training and Logistics Sector Demand

The expanding global logistics industry and the growth of commercial vehicle fleets present significant market opportunities for truck and bus driving simulators. The international truck driving simulator market is experiencing robust growth, driven by rising demand for skilled drivers amid growing road safety concerns and regulatory requirements. Daimler Truck announced a strategic partnership with NVIDIA in May 2025 to co-develop autonomous trucking software and a high-fidelity simulation platform for driver training across its brands. Fleet operators including Linde have implemented TecknoSIM Truck Driving Simulators to improve training quality and safety, reporting fuel efficiency improvements of 20% and accident reduction of 27% within short implementation periods.

The European Directive 2003/59/EC framework creates recurring demand as professional drivers must complete periodic training to maintain certifications, with millions of active commercial driver licenses across European Union member states requiring ongoing education. Logistics companies and transportation operators are increasingly adopting eco-driving, defensive driving, and hazardous goods transportation training modules enabled by simulation technology, positioning this application segment for sustained expansion throughout the forecast period.

Category-wise Analysis

Simulator Type Insights

Fixed-base simulators hold the leading position in the driver training simulator market with an estimated 45% share in 2025, supported by their affordability, reduced maintenance, and strong suitability for procedural training. By eliminating motion platforms, these systems cut operational complexity and power requirements while still offering high-quality visual environments and steering-force feedback essential for cognitive and rules-based learning. Their widespread use in aviation and automotive training proves their capability to deliver effective instrument, basic driving, and regulatory training at significantly lower total cost of ownership. For driving schools and municipal training centers focused on foundational skills, fixed-base simulators provide the best balance of cost, utility, and training effectiveness.

Application Insights

The Training application segment dominates the driver training simulator market with an estimated 52% market share in 2025, reflecting its central role in driver education and professional skills development. Driving schools globally adopt simulators to teach vehicle control, hazard perception, and emergency responses in controlled environments before progressing to road training. Growth in young driver populations and mandatory certification requirements further strengthens this segment. Institutions such as the IRU Academy and leading commercial training centers rely on simulation to deliver standardized, repeatable instructional modules. With regulatory mandates, periodic skill refresh requirements, and clear pedagogical advantages, the Training segment remains the primary revenue engine for simulator manufacturers and service providers.

Vehicle Type Insights

Truck and bus simulators account for the largest share of the driver training simulator market with an estimated 38% market share in 2025, driven by stringent regulatory requirements and the complexity of heavy vehicle operation. These simulators replicate real-world cab layouts, transmission behaviors, and dynamics, enabling trainees to practice maneuvering, braking, and hazardous condition responses safely. European Directive 2003/59/EC mandates structured qualification for professional drivers, sustaining strong demand across training centers and fleet operators. Organizations increasingly invest in heavy-vehicle simulators to enhance safety performance, reduce fuel consumption, and address persistent driver shortages. This combination of regulatory pressure and operational need ensures continued leadership of the truck and bus segment.

Regional Insights

North America Driver Training Simulator Market Trends

North America retains a leading position in the global driver training simulator market with an estimated 34% share in 2025, supported by advanced simulation engineering capabilities, strong regulatory influence, and a mature ecosystem of technology providers. The United States drives regional adoption through established suppliers such as L3Harris Technologies, CXC Simulations, and Tecknotrove, which serve driving schools, commercial fleets, and automotive manufacturers. Canada-based CAE Inc., with its global network of aviation training centers and deep expertise in full-flight simulators, continues to influence automotive simulation standards.

FAA certification frameworks further strengthen regional quality benchmarks by providing rigorous technical guidelines applicable to simulator design. Research universities across the region use high-fidelity simulators for human factors and driver behavior studies, while the National Safety Council’s emphasis on young driver safety expands demand for structured training solutions. Corporate fleets increasingly adopt eco-driving and defensive driving programs to reduce accidents, insurance costs, and emissions, reinforcing regional leadership.

Europe Driver Training Simulator Market Trends

Europe represents a critical market for driver training simulators with an estimated 32% share in 2025, shaped by harmonized regulations, strong automotive engineering capabilities, and national road safety commitments. Regional adoption is driven by Directive 2003/59/EC, which mandates initial and periodic training for professional drivers, allowing approved simulators to fulfill key learning requirements. Major markets including Germany, France, the U.K., and Spain consistently invest in high-fidelity simulation systems to meet evolving training needs.

Germany’s FKFS and University of Stuttgart collaborate with Bosch Rexroth on advanced simulators used for ADAS and autonomous driving research, while BMW’s Munich simulation campus strengthens technical innovation. France’s Exail (formerly ECA Group) remains a prominent European supplier with extensive deployment across driver, truck, and emergency vehicle training programs. Advocacy groups like the European Cycling Federation influence training curricula to improve cyclist and pedestrian safety. Europe's combination of strong regulation, research intensity, and engineering expertise positions it as an innovation hub for next-generation simulation technologies.

Asia Pacific Driver Training Simulator Market Trends

Asia Pacific stands as the fastest-growing driver training simulator market, projected to expand at a 6.8% CAGR from 2026 to 2033, backed by rapid urbanization, rising mobility, and heightened government focus on road safety. Increasing vehicle ownership across China, India, Japan, and ASEAN nations is accelerating demand for scalable, high-quality training solutions. India offers significant potential, driven by a young population and expanding transportation needs, highlighted by CAE Simulation Training Private Limited’s 112% utilization of its 16-simulator pilot training center in FY2025.

China and Japan lead autonomous vehicle development efforts requiring robust simulation frameworks for validation and human-machine interaction research. Manufacturing competitiveness and improving technical expertise are encouraging simulator production within the region, further lowering costs for training institutions. Driving schools, logistics companies, and research organizations are rapidly integrating simulators into training programs, while Southeast Asian governments modernize licensing systems and safety initiatives. These demographic, economic, and regulatory factors ensure sustained growth across Asia Pacific.

Competitive Landscape

The global driver training simulator market remains moderately fragmented, comprising specialized simulation technology developers, diversified automotive testing solution providers, and strong regional players. Market competition is shaped by technological capability, product breadth across fidelity levels, and established relationships with regulatory authorities and large fleet operators.

Companies increasingly differentiate by advancing motion systems, enhancing graphics and physics engines, and offering multi-vehicle simulation platforms that address both commercial driver training and automotive engineering requirements.

Business strategies emphasize collaboration with automotive OEMs, co-development of ADAS and autonomous driving validation tools, and the creation of modular and scalable simulator architectures suited to varied customer budgets. Many providers are moving toward vertically integrated, turnkey ecosystems combining hardware, software, training content, and analytics. Regional specialists strengthen position through local curriculum customization and robust after-sales support.

Emerging trends include simulator-as-a-service, subscription-based licensing, and shared training centers that reduce capital costs. The market is gradually consolidating as larger firms acquire niche technology developers to expand capabilities and global reach.

Key Market Developments:

- December 2025: NVIDIA released Alpamayo-R1 which is the first open-source vision-language-action model for autonomous driving to accelerate AV research and improve decision-making transparency.

- March 2025: Torc Robotics (a subsidiary of Daimler Truck) announced a collaboration with NVIDIA and Flex to build a scalable “physical-AI” compute platform for autonomous long-haul trucks aimed at production-ready deployment by 2027.

Companies Covered in Driver Training Simulator Market

- Adacel Technologies Limited

- Anthony Best Dynamics Limited

- Bosch Rexroth AG

- CAE Inc.

- Cruden BV

- ECA Group (Exail)

- L3Harris Technologies, Inc.

- Tecknotrove

- Thales Group

- VI-grade GmbH

- Moog Inc.

- NVIDIA Corporation

- IPG Automotive GmbH

- MTS Systems Corporation

- CXC Simulations

- AV Simulation

- SimCraft

- AB Dynamics

- Realtime Technologies (FAAC)

- SIEMENS AG

Frequently Asked Questions

The market is expected to reach US$ 3.0 billion by 2033, growing from US$ 2.2 billion in 2026 at a 4.6% CAGR.

Demand is driven by stricter road safety regulations, advances in VR and motion simulation, and growing use in ADAS and autonomous vehicle development.

Fixed-Base Simulators lead the market with about 45% share due to their cost efficiency, flexibility, and strong training effectiveness.

North America leads with roughly 34% share, supported by strong technology providers, research capabilities, and regulatory readiness.

Expanding deployment for ADAS and autonomous vehicle development testing represents the most significant market opportunity.

The market includes several prominent global simulation and engineering technology providers offering advanced training and vehicle development solutions.