- Off-Road Equipment & Machinery

- Pile Driver Market

Pile Driver Market Size, Share, and Growth Forecast, 2026 – 2033

Pile Driver Market by Product Type (Hydraulic, Diesel, Vibratory, Pneumatic, Impact), Capacity (Less than 300 kN, 300 - 500 kN, 500 - 1000 kN, 1000 - 1500 kN, Over 1500 kN), Application (Construction, Infrastructure, Offshore, Mining, Energy), and Regional Analysis for 2026-2033

Pile Driver Market Share and Trends Analysis

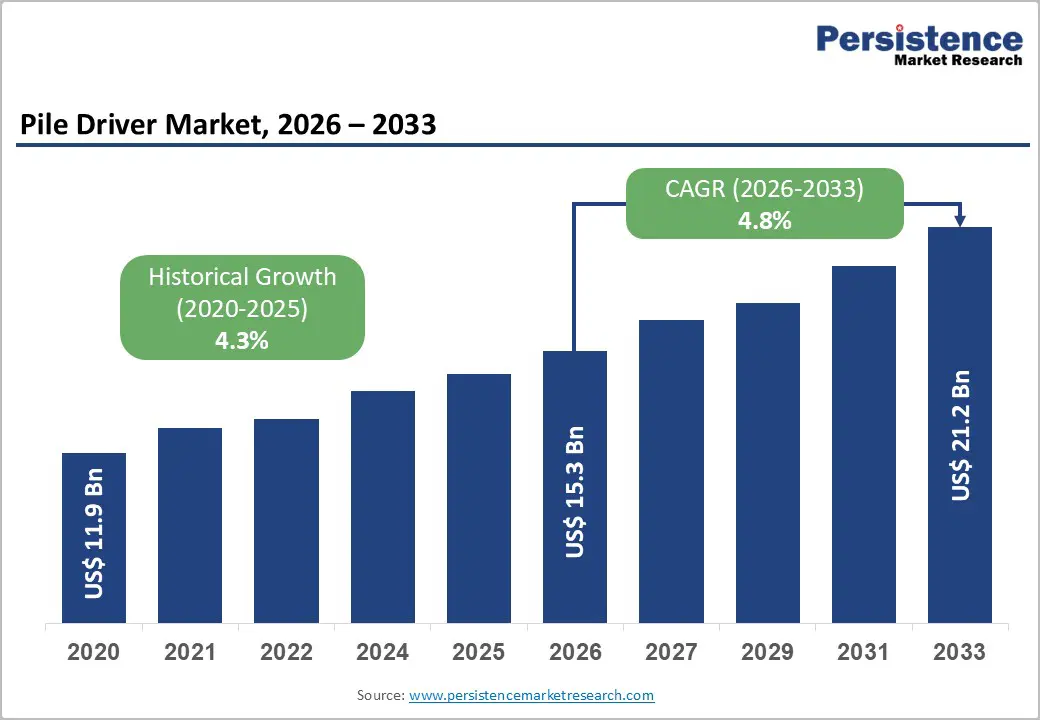

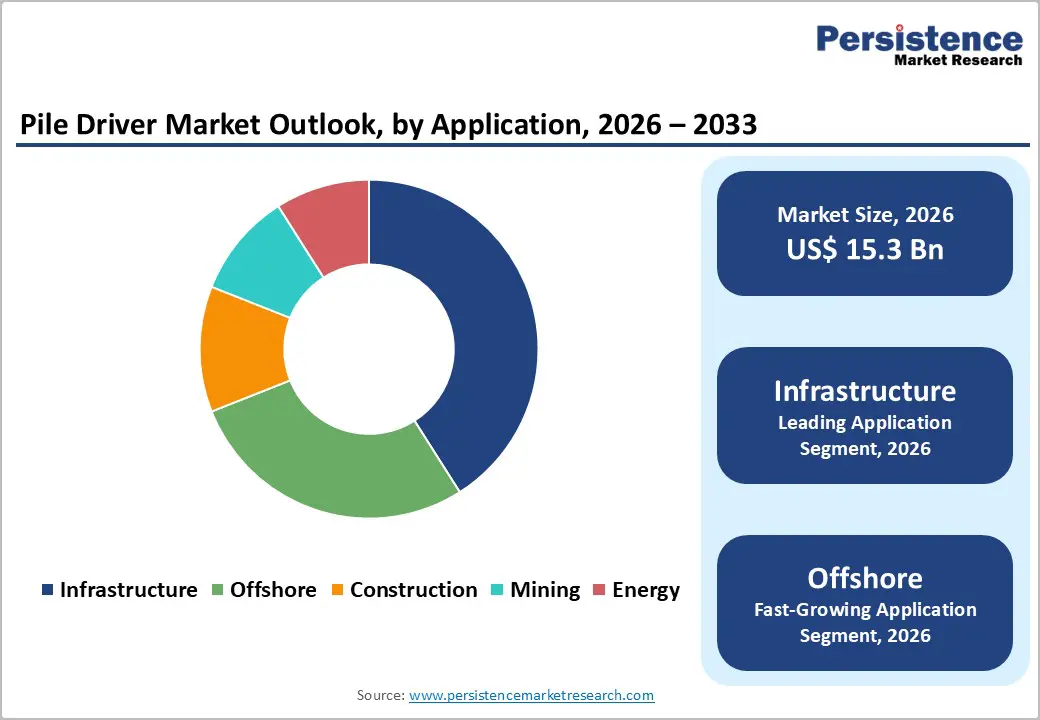

The global pile driver market size is likely to be valued at US$ 15.3 billion in 2026, and is projected to reach US$ 21.2 billion by 2033, growing at a CAGR of 4.8 % during the forecast period 2026−2033. Sustained expansion of large-scale infrastructure development represents the primary growth catalyst, as urban population growth and industrial decentralization increase demand for deep foundation systems across transportation, energy, and industrial assets. Demographic concentration in urban centers creates higher structural load requirements, directly increasing reliance on pile driving equipment capable of handling complex soil and seismic conditions.

Technological integration within construction machinery, including automation, vibration control, and energy-efficient power systems, improves installation accuracy while reducing operational risk, reinforcing adoption across regulated construction environments. Rising awareness of structural safety standards and long-life asset requirements, driven by updated building codes and international engineering guidelines, elevates preference for mechanized piling solutions over manual or semi-mechanical alternatives.

Key Industry Highlights

- Leading Application: The infrastructure segment is likely to lead with about 41% market share in 2026 due to sustained investment in transportation networks, urban transit systems, and durable foundation solutions.

- Fastest-growing Application: The offshore segment is forecasted to grow the fastest through 2033, owing to expanding renewable energy projects, port development, and demand for specialized marine foundation solutions.

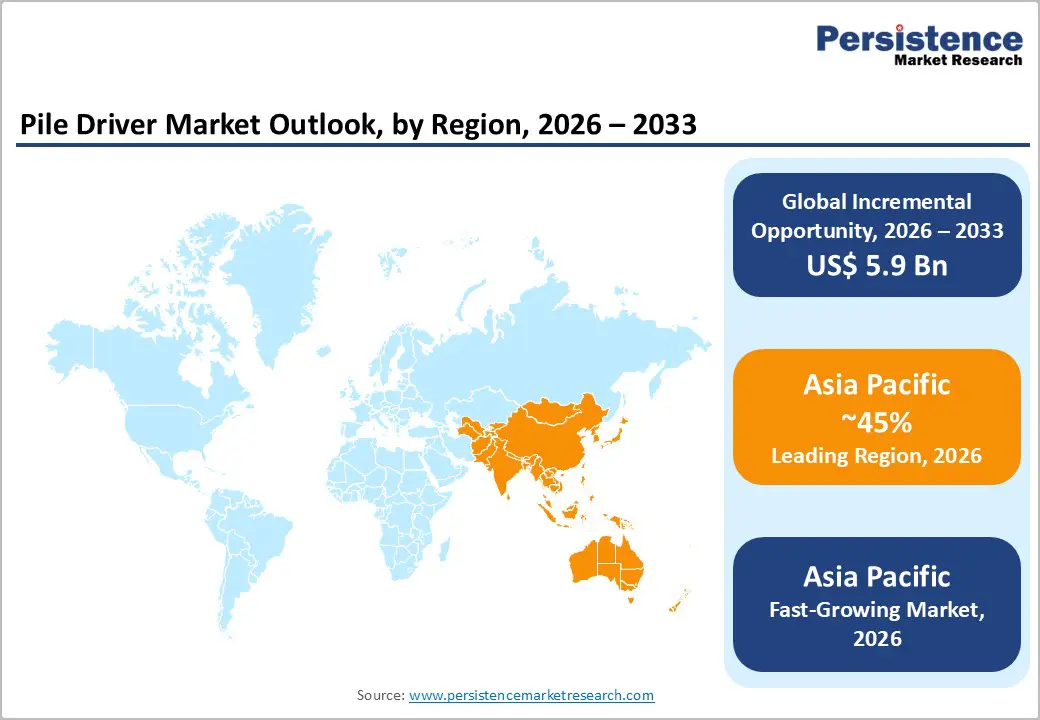

- Dominant Region: Asia Pacific is expected to hold about 40% market share in 2026, driven by extensive investment in core infrastructure development.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market for pile drivers from 2026 to 2033, fueled by offshore energy expansion and renewable power projects.

- September 2025: Blattner Energy signed a 3-year deal with Built Robotics to deploy AI-powered autonomous robots for U.S. solar projects, automating pile driving, surveying, drilling, trenching, and material handling.

| Key Insights | Details |

|---|---|

| Pile Driver Market Size (2026E) | US$ 15.3 Bn |

| Market Value Forecast (2033F) | US$ 21.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.8 % |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Infrastructure Modernization and Urban Development Initiatives

Public infrastructure modernization initiatives form a long-term structural foundation for sustained pile driver demand, particularly as public authorities prioritize durability, safety, and lifecycle efficiency in large-scale construction assets. Transportation corridors, bridges, ports, airports, and urban transit systems increasingly require foundation solutions that can withstand higher traffic loads, climate-induced stress, and extended operational timelines. National infrastructure strategies issued by ministries of transport, public works departments, and multilateral development institutions emphasize stricter engineering standards, including deeper foundation depths and enhanced load-bearing capacity. These standards elevate reliance on pile drivers that deliver consistent penetration performance, precise energy control, and reduced vibration impact to protect adjacent structures. Compliance with such specifications necessitates technologically advanced piling systems, supporting replacement demand alongside new installations.

Urban development and densification further reinforce this demand trajectory by introducing complex site constraints and heterogeneous soil conditions that limit conventional foundation approaches. High-density residential towers, mixed-use commercial complexes, and underground transit networks require deeper, more accurate piling to ensure structural stability within limited construction footprints. Urban construction environments also impose stricter noise, vibration, and emissions controls, accelerating adoption of modern pile drivers with enhanced precision and environmental compliance capabilities. Government-backed infrastructure financing frameworks and public–private partnership models reduce capital exposure for contractors, supporting long-term equipment ownership strategies rather than short-duration leasing.

Skilled Labor Shortage and Project Delays

Limited availability of skilled operators and ongoing project delays exert significant constraints on growth by restricting execution capacity on complex foundation projects that demand specialized expertise. Operating heavy piling equipment requires precision in setup, adjustment, and response to variable subsurface conditions. Shortage of trained personnel forces crews to work at slower paces, compromises quality, and increases safety risks. When workforce supply shrinks amid high demand for expertise, contractors encounter resourcing gaps that extend schedules or require reliance on less efficient teams. Industry reporting indicates about 45% of construction projects report delays directly linked to labor shortages, reflecting a widespread operational constraint on timely project delivery. Reduced availability of skilled personnel limits the number of simultaneous tasks a team can perform, driving inefficiencies and increasing cost per unit of delivered work.

Execution timelines also suffer from delays in foundational activities that postpone subsequent structural operations, lower overall site productivity, and increase idle equipment costs. Shifts in schedule disrupt cash flow planning for contractors and clients, prompting tighter contract terms and heightened scrutiny on future projects. Workforce deficits remain a primary factor behind schedule unreliability on major builds, linking labor shortages with broader operational risk. Extended timelines reduce contractor capacity to undertake additional work, strain client relationships, and encourage conservative bidding to offset potential overruns. Such slowdowns restrict capital recycling across project portfolios and diminish overall productivity, impeding growth and limiting investment in advanced equipment.

Growing Government-Backed Financing

Expansion of public financing programs creates a significant opportunity by reducing capital barriers associated with acquiring heavy equipment. Structured loans, subsidized credit schemes, and targeted funding initiatives improve access to long?term capital for contractors facing high upfront costs for foundation machinery. Wider access to affordable financing allows firms to shift from short-term rentals to ownership of advanced pile drivers that deliver higher performance, precision, and operational reliability. Contractors can dedicate working capital to other operational requirements instead of reserving funds solely for equipment purchases. Alignment of public funding with national infrastructure priorities establishes predictable investment pipelines that support long-term capital planning. Financial support strengthens contractor balance sheets and encourages fleet modernization with technologies that enhance productivity and compliance with evolving engineering standards.

Availability of government-backed capital increases investment in advanced equipment across project portfolios, improving construction quality and operational efficiency. Structured financing arrangements often include performance incentives tied to efficiency gains and environmental standards, promoting adoption of modern pile driving technologies with reduced emissions and minimized onsite disruptions. Public funding enhances investor confidence in project viability, accelerates procurement cycles, and improves contractor cash flows. Predictable funding simplifies budgeting and risk assessment for major infrastructure initiatives, reducing the chance of execution delays due to financing gaps. Firms with access to affordable capital can deploy equipment strategically, optimize utilization rates, and strengthen competitive positioning.

Category-wise Analysis

Product Type Insights

Hydraulic pile drivers are poised to lead with a forecasted 34% share in 2026, owing to superior control accuracy, adaptability across soil conditions, and alignment with regulatory noise and vibration standards. Hydraulic systems provide consistent energy delivery, which minimizes stress on piles and ensures uniform installation depth, critical for long-term structural stability. Their precision supports deployment in complex geotechnical environments, including heterogeneous soil layers and high-density urban zones. Contractors prefer hydraulic configurations due to seamless integration with automated monitoring and diagnostic systems, enabling real-time performance tracking.

Vibratory pile drivers are anticipated to be the fastest-growing segment between 2026 and 2033, fueled by increasing adoption in sheet piling, marine construction, and temporary foundation applications. Vibratory systems reduce soil resistance and allow faster installation, accelerating project timelines for large-scale infrastructure initiatives. Advanced noise suppression technologies and vibration control mechanisms enhance compliance with urban construction regulations and environmental standards. Contractors leverage vibratory equipment for applications requiring minimal disruption to surrounding structures or operational sites.

Capacity Insights

500–1000 kilonewton (kN) units are likely to be the leading segment with a projected 37% of the pile driver market share in 2026, due to their balanced performance across mid- to large-scale construction projects. This capacity range matches the foundation requirements of urban infrastructure, commercial complexes, industrial plants, and bridge construction, offering sufficient energy without excessive operational complexity. Contractors value these units for operational versatility, ease of handling, and cost-efficiency, which support project scheduling and budget control. Availability through rental fleets and dealer networks ensures equipment accessibility, while maintenance support and reliability reinforce trust. Consistent performance under variable soil conditions strengthens adoption across diverse construction environments.

Over 1500 kilonewton units are expected to witness the fastest growth between 2026 and 2033, powered by expansion of offshore energy, heavy industrial, and mega-infrastructure projects. Increasing project scale demands higher energy transfer, deeper pile penetration, and robust machinery capable of handling extreme load requirements. Advancements in hydraulics, automation, and monitoring systems reduce operational risks and improve precision in challenging environments. Capital-intensive projects financed through government programs and private investment favor ownership of high-capacity units.

Application Insights

The infrastructure segment is slated to hold a dominant position, with an anticipated 41% of the pile driver market revenue share in 2026, driven by sustained investment in transportation networks, urban transit systems, and public utilities. Focus on durable foundation solutions ensures longevity and structural safety, aligning with regulatory and engineering standards. Large-scale projects such as bridges, highways, and metro networks require reliable, high-performance pile driving equipment, creating consistent demand. Standardized specifications across public and private contracts simplify equipment selection, while government-backed financing encourages fleet modernization. Contractors prioritize machines with operational versatility, precision, and low emissions to meet project timelines and regulatory requirements, sustaining adoption in this sector.

The offshore segment is forecasted to be the fastest-growing end-user segment between 2026 and 2033, boosted by renewable energy deployment, port expansion, and coastal protection initiatives. Pile drivers are critical for installing marine foundations, including wind turbine platforms, jetties, and seawall structures. Specialized configurations and technological enhancements, such as corrosion-resistant materials and precision monitoring systems, improve operational efficiency in challenging offshore environments. Contractors adopt equipment capable of withstanding tidal forces, high salinity, and remote logistics constraints. Expanding renewable energy projects and maritime infrastructure programs, supported by public and private funding, are expected to drive sustained demand for high-capacity and technologically advanced pile driving solutions.

Regional Insights

North America Pile Driver Market Trends

North America demonstrates steady demand for pile drivers, supported by extensive infrastructure rehabilitation and modernization initiatives. Highway and bridge upgrades, urban transit expansions, and waterfront redevelopment require foundation solutions capable of operating in constrained urban sites and variable soil conditions. Growth in offshore wind energy, particularly along the U.S. East Coast, drives adoption of high-capacity marine piling equipment designed for monopile and jacket foundations. Electrification of industrial zones and expansion of power transmission networks increases foundation needs for substations, data centers, and renewable energy facilities. Contractors increasingly deploy hydraulic and electric pile drivers with low emissions and reduced vibration to comply with strict environmental and community regulations.

Telemetry-enabled machinery and digital maintenance systems enhance uptime, optimize project scheduling, and extend equipment lifecycle, supporting efficient operations across diverse project types. Recent urban and industrial initiatives further strengthen market activity. Large-scale data center corridors, cold-climate hydropower projects in northern states, and coastal flood resilience works demand specialized machines capable of working in rocky, frozen, or tidal conditions. Federal and state-level infrastructure funding programs reduce capital constraints for contractors, encouraging adoption of advanced equipment over short-term rentals. Firms integrate automated monitoring and remote diagnostics to improve precision, safety, and operational efficiency.

Europe Pile Driver Market Trends

Europe remains a strategically significant market for pile driving equipment, driven by extensive urban redevelopment and aging infrastructure replacement programs. Large-scale projects across metro networks, bridges, and ports demand precision foundation solutions capable of minimizing disruption in densely populated cities. Environmental and noise regulations are among the strictest globally, promoting adoption of low-emission, hydraulic, and electric pile drivers with vibration control and automated energy management systems. Contractors increasingly use digital tools, including telematics and real-time monitoring, to optimize installation cycles and maintain compliance with regulatory standards. Investments in flood protection, riverbank stabilization, and coastal reinforcement projects create demand for specialized machines capable of operating on soft soils, reclaimed land, and variable water tables.

Offshore wind farms along the North Sea, Baltic, and Atlantic coasts require high-capacity marine piling equipment for monopile and jacket foundations, while harbor expansion and quay reinforcement projects increase demand for heavy-duty machines with precise depth control. Governments and private developers prioritize advanced systems to reduce environmental impact, enhance operational efficiency, and maintain safety during installation. Expansion of industrial zones, cross-border high-speed rail networks, and sustainable urban infrastructure further increases foundation requirements.

Asia Pacific Pile Driver Market Trends

Asia Pacific is expected to dominate with an estimated 40% of the pile driver market share in 2026, reflecting extensive infrastructure expansion, rapid urbanization, and growing investment in transportation networks, ports, and industrial facilities. Large-scale construction programs demand high-capacity and precise foundation solutions, driving adoption of hydraulic and vibratory pile drivers with advanced energy control, automated monitoring, and vibration suppression capabilities. Government-backed financing initiatives reduce capital barriers for contractors, enabling fleet modernization and acquisition of technologically advanced machines. High-density urban development and industrial facility construction require deep and stable foundations, increasing reliance on equipment capable of consistent performance across heterogeneous soil conditions.

Asia Pacific is forecasted to be the fastest-growing regional market for pile drivers between 2026 and 2033, stimulated by rapid expansion of offshore energy, renewable power installations, port development, and large-scale industrial projects. Challenging soil conditions, deepwater foundations, and remote project locations drive demand for specialized, high-capacity pile driving equipment with precision control and automated performance tracking. Contractors leverage advanced technology to optimize installation cycles, reduce operational risk, and meet aggressive project schedules. Strategic public-private partnerships, favorable regulatory frameworks, and local technical support facilitate rapid equipment deployment.

Competitive Landscape

The global pile driver market structure reflects moderate fragmentation, characterized by the coexistence of influential multinational manufacturers and specialized regional players. BAUER GROUP, Liebherr, Junttan Oy, Soilmec S.p.A., ABI GmbH, and PVE USA represent key global participants, each holding significant market influence through diversified product portfolios and extensive service networks. These companies leverage technological differentiation, offering solutions that integrate automation, vibration control, and energy-efficient systems, enabling contractors to meet increasingly stringent regulatory and environmental standards. Regional specialists complement the competitive landscape by targeting localized construction and infrastructure needs, often providing tailored solutions with flexible financing and maintenance support.

Market competitiveness is further reinforced by aftermarket support, including equipment servicing, operator training, and spare part availability, which strengthens customer loyalty and long-term adoption. Leading players such as BAUER GROUP and Liebherr emphasize advanced hydraulic and vibratory technologies, while Junttan Oy, Soilmec S.p.A., ABI GmbH, and PVE USA focus on high-capacity, modular, and precision-driven systems for infrastructure and offshore applications. Investment in digital monitoring and predictive maintenance solutions has become a critical differentiator, enhancing operational efficiency for end users.

Key Industry Developments

- In September 2025, Trimble’s Groundworks machine control system was integrated with Vermeer’s PD10R and PD25R remote?control pile drivers, enabling a single operator to accurately position and drive piles on solar farm construction sites, which improved productivity and safety.

- In August 2025, U.S. startup Xpanner introduced a robotic automation retrofit kit for existing solar pile drivers that integrates advanced hardware and software to enable automated hammering, precise pile placement, and improved site productivity with minimal downtime.

- In February 2025, China launched the Erhai Changqing, a new pile?driving vessel from Nantong with the world’s tallest derrick and highest piling capacity, capable of installing massive foundation piles with centimeter?level precision for major infrastructure and offshore projects.

Companies Covered in Pile Driver Market

- BAUER GROUP

- Liebherr

- Junttan Oy

- Soilmec S.p.A.

- ABI GmbH.

- PVE USA

- ABI Group

- BSP TEX

- Dieseko Group

Frequently Asked Questions

The global pile driver market is projected to reach US$ 15.3 billion in 2026.

Heavy investments in infrastructure, urban development projects, and adoption of advanced, automated piling technologies drive the market.

The market is poised to witness a CAGR of 4.8 % from 2026 to 2033.

Key market opportunities lie in offshore energy and coastal infrastructure projects, and rapid industrialization-driven transport and urban development in emerging economies.

Some of the key market players include BAUER GROUP, Liebherr, Junttan Oy, Soilmec S.p.A., and ABI GmbH.