- LED & Lighting (Optoelectronics)

- LED Driver Market

LED Driver Market Size, Share, and Growth Forecast 2026 - 2033

LED Driver Market by Component (Driver IC, Discrete Component, Others), Luminaire Type (Decorative Lamps, Reflectors, Type A Lamp, Others), Application (Consumer Electronics, Lighting, Automotive, Outdoor Displays), and Regional Analysis for 2026 - 2033

LED Driver Market Size and Trend Analysis

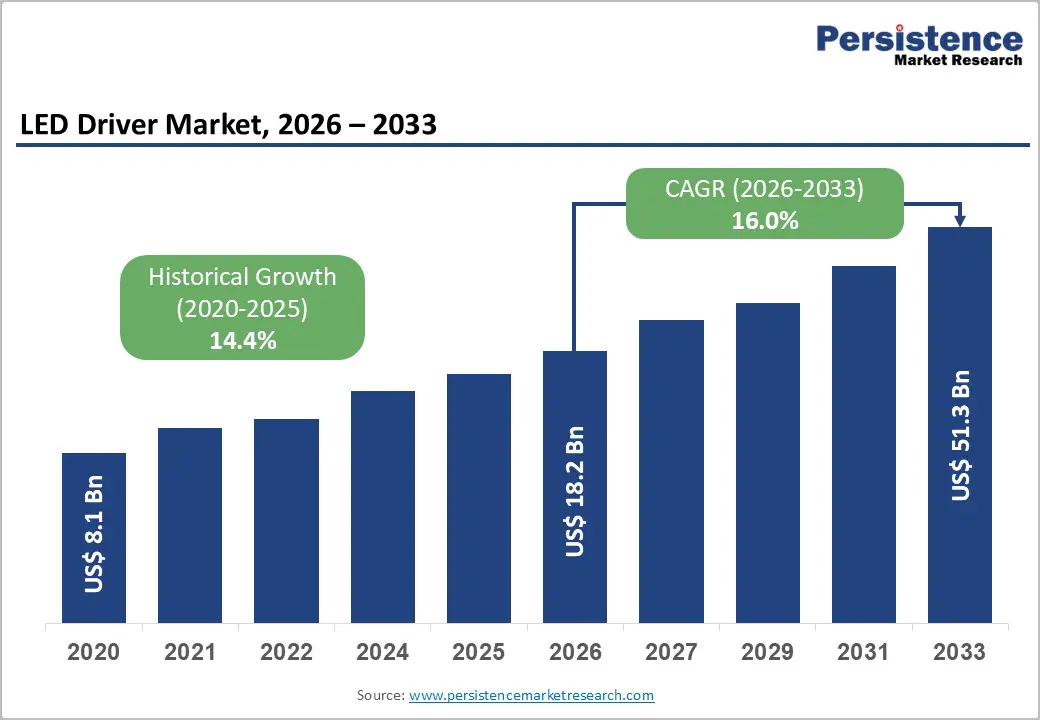

The global led driver Market size is valued at US$ 18.2 billion in 2026 and is projected to reach US$ 51.3 billion by 2033, growing at a CAGR of 16.0% between 2026 and 2033.

The market is experiencing robust expansion driven by accelerating global adoption of energy-efficient lighting technologies and the widespread phase-out of traditional incandescent and fluorescent lamps. According to the International Energy Agency (IEA), all lighting sales must transition to LED technology by 2025 to meet the Net Zero Emissions by 2050 Scenario (NZE Scenario), creating sustained demand for LED drivers across residential, commercial, and industrial applications.

Key Industry Highlights:

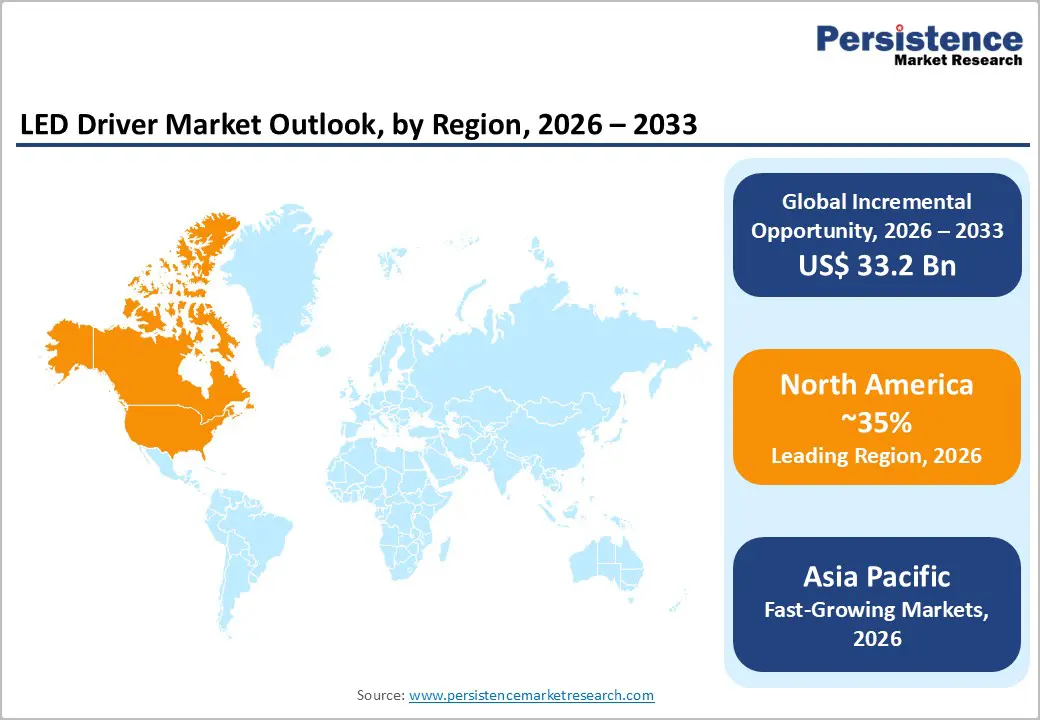

- Leading Region: North America leads the global LED Driver Market, driven by U.S. DOE regulations, ENERGY STAR mandates, and large-scale smart city deployments, accounting for a significant share of global revenues through the forecast period.

- Fastest Growing Region: Asia Pacific is the fastest growing region, propelled by China's smart city initiatives, India's UJALA Scheme, and ASEAN urbanization, with the region expected to command approximately 40% of global market revenue by 2033.

- Dominant Segment: The Driver IC segment under the Component category holds the largest market share (~55%) due to superior current regulation, compact integration, and widespread compatibility across lighting, automotive, and consumer electronics applications.

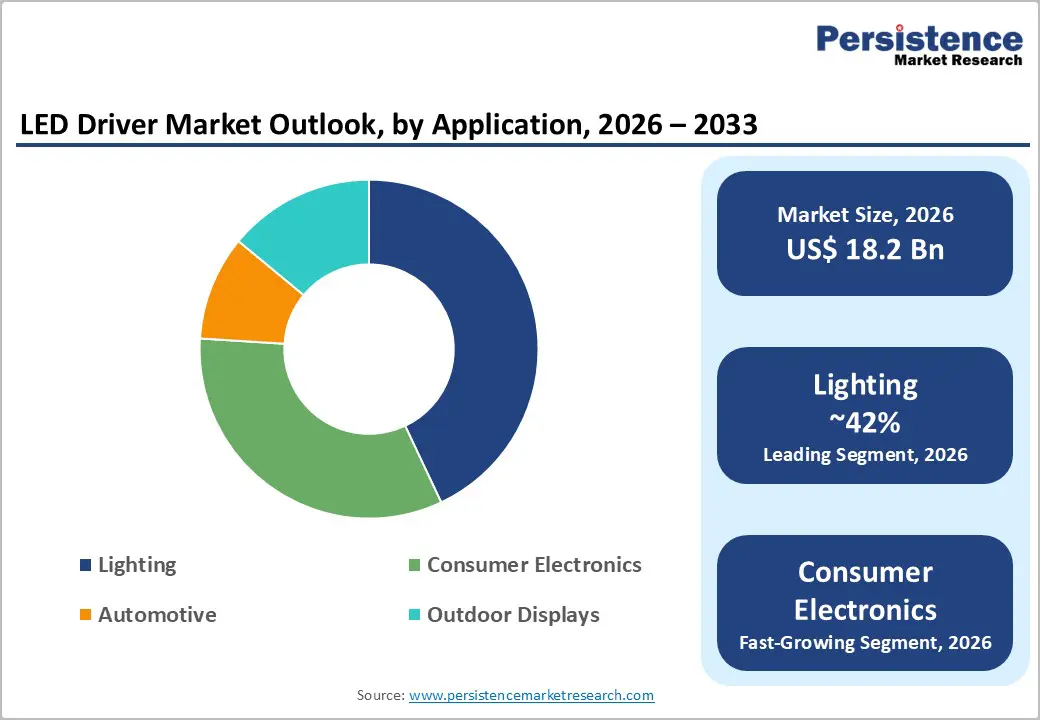

- Fastest Growing Segment: The Consumer Electronics application segment particularly LED backlighting for TVs, monitors, and displays the fastest growing application, driven by the expanding LED & OLED Lighting Products and Displays Market globally.

- Key Market Opportunity: Smart city outdoor LED lighting programs and electric vehicle LED systems represent transformative opportunities, with EV sales surpassing 17 million units in 2024 and government smart city programs mandating large-scale IoT-enabled LED infrastructure upgrades globally.

| Key Insights | Details |

|---|---|

| LED Driver Market Size (2026E) | US$ 18.2 Bn |

| Market Value Forecast (2033F) | US$ 51.3 Bn |

| Projected Growth CAGR (2026 - 2033) | 16.0% |

| Historical Market Growth (2020 - 2025) | 14.4% |

Market Dynamics

Drivers - Stringent Global Energy Efficiency Regulations and Government Mandates

Government policies and regulatory frameworks are among the most powerful catalysts propelling the LED Driver Market. The IEA has identified a global transition requiring 100% LED lighting sales by 2025 under its Net Zero Emissions roadmap, compelling nations to enact minimum energy performance standards (MEPS) and phase-out programs. The U.S. Department of Energy (DOE) continues to tighten efficacy thresholds under its ENERGY STAR certification program, while the European Union's Ecodesign Regulation has mandated progressive elimination of inefficient light sources since 2009. India's UJALA Scheme has distributed over 36 crore LED bulbs, catalysing mass-market adoption. These regulatory pressures create a structural demand floor for LED drivers, as every LED luminaire requires a compatible driver to regulate current and voltage.

Rapid Proliferation of Smart Lighting and IoT-Enabled Ecosystems

The integration of LED drivers into smart home, smart city, and industrial IoT ecosystems represents a transformative growth engine. Intelligent LED drivers now support digital communication protocols such as DALI-2, Zigbee, Thread, and PoE (Power over Ethernet), enabling seamless connectivity with building automation platforms. Cities such as Los Angeles and San Diego have deployed IoT-enabled LED streetlight networks that reduce energy consumption by up to 80% versus traditional luminaires while enabling real-time monitoring and adaptive brightness control. The Smart Street Lighting NY program under Governor Kathy Hochul achieved a milestone of 500,000 LED streetlight replacements nearly three years ahead of its 2025 target, exemplifying the pace of deployment. As the LED & OLED Lighting Products and Displays Market continues to evolve with advanced display technologies, the demand for high-precision, programmable LED drivers capable of supporting colour tuning, dimming, and wireless control is escalating rapidly.

Restraints - High Initial Investment and Thermal Management Challenges

Despite strong long-term economics, the upfront cost of advanced LED driver systems particularly those with embedded digital controls, power factor correction, and surge protection remains a significant barrier for price-sensitive markets. Commercial and industrial retrofit projects require not only the cost of LED luminaires but also compatible driver hardware and installation. Additionally, thermal management continues to be a critical technical restraint; LED drivers generate heat that, if inadequately dissipated, leads to premature failure and performance degradation. Operating temperatures can reduce driver lifespan by as much as 50% per every 10°C rise above rated conditions. This necessitates additional engineering investment in heat sinks, enclosures, and thermal interface materials, increasing total system cost and limiting adoption in retrofit scenarios where existing fixtures were not designed for active thermal management.

Lack of Standardization and Interoperability Issues

The absence of universal standards for LED driver protocols, communication interfaces, and form factors creates significant compatibility challenges across the supply chain. Luminaire manufacturers, system integrators, and end users frequently encounter interoperability issues when combining drivers, controllers, and sensors from different vendors. While standards bodies such as the DALI Alliance and Zhaga Consortium have advanced interoperability frameworks, adoption remains fragmented across geographies. In developing economies where standardization infrastructure is less mature, these incompatibilities lead to inefficiencies, increased project costs, and reduced consumer confidence. Varying national electrical safety standards further complicate the cross-border commercialization of driver products, adding certification costs and prolonging time-to-market cycles for global manufacturers.

Opportunity - Electric Vehicle Lighting Systems as a High-Growth Application Frontier

The accelerating global transition toward electric vehicles (EVs) is creating a substantial and structurally differentiated opportunity for advanced LED driver technologies. Modern EVs extensively utilize LED lighting for adaptive headlights, matrix beam systems, tail lamps, interior ambient lighting, and Advanced Driver-Assistance System (ADAS) indicators. Each vehicle requires multiple compact, high-temperature-tolerant driver ICs qualified to AEC-Q100 automotive standards. Global EV sales surpassed 17 million units in 2024, per the International Energy Agency (IEA), with projections pointing to over 40% of new car sales being electric by 2030. In April 2024, Texas Instruments introduced next-generation AEC-Q100-qualified LED driver ICs supporting adaptive front lighting and matrix beam control for EV and autonomous vehicle platforms.

Smart City Infrastructure Programs Driving Large-Scale Outdoor LED Driver Demand

Government-led smart city programs across Asia, North America, and Europe are emerging as a pivotal demand driver for the LED Driver Market. National programs are funding the mass replacement of legacy street and outdoor lighting infrastructure with intelligent, IoT-connected LED systems. In March 2024, Inventronics launched the industry's first DALI + wireless LED driver certified for Thread-based networking, enabling hybrid wired/wireless smart city deployments. China's 14th Five-Year Plan prioritizes urban LED infrastructure upgrades across tier-1 and tier-2 cities, while the European Green Deal allocates significant capital to sustainable urban lighting. The LED & OLED Lighting Products and Displays Market further magnifies outdoor display demand, where high-brightness LED driver modules are critical for digital signage and public information boards. Market participants developing DALI-2-compliant, wireless-enabled, and IP67-rated driver solutions are well-positioned to capitalize on this structural opportunity.

Category-wise Analysis

Component Insights

The Driver IC segment commands the leading share in the Component category of the LED Driver Market, accounting for approximately 55% of total market revenue. Driver ICs are preferred across applications due to their ability to deliver precise constant-current regulation, ensuring consistent LED brightness and longevity irrespective of input voltage fluctuations or ambient temperature variations. Unlike discrete component assemblies, Driver ICs consolidate multiple circuit functions rectification, regulation, dimming control, and thermal protection into a compact, cost-effective package, reducing PCB footprint and bill-of-materials complexity. The growing adoption of dimming techniques including analogy, digital PWM, and wireless control further reinforces demand for advanced ICs. Companies such as Texas Instruments, Analog Devices, Inc., and STMicroelectronics continue to invest in high-efficiency Driver IC platforms for industrial, automotive, and smart lighting applications, strengthening the segment's dominant position.

Luminaire Type Insights

The Type A Lamp segment holds the leading share within the Luminaire Type category, representing approximately 38% of total LED driver demand. Type A lamps the standard screw-base bulb format familiar to consumers globally are the most widely deployed LED luminaire form factor, benefiting from direct drop-in replaceability with legacy incandescent and halogen bulbs. Their ubiquity across residential, hospitality, and commercial environments ensures continuous replacement-cycle demand. The U.S. DOE has documented that Type A LED lamps achieve payback periods as short as a few weeks compared to tungsten-filament equivalents, accelerating adoption. Simplified internal driver designs compatible with standard dimmers and low-cost AC-to-DC conversion requirements make this segment attractive for high-volume production. The Decorative Lamps segment is gaining traction in premium residential and hospitality settings, but Type A Lamp retains its lead driven by sheer volume and widespread retrofit demand.

Application Insights

The Lighting application segment dominates the LED Driver Market, holding approximately 42% market share. This leadership is underpinned by the global transition from conventional to LED-based general lighting across residential, commercial, industrial, and municipal sectors. According to the IEA, LED technology is projected to account for over 70% of the total global lighting market by 2030, and countries from India to South Africa are actively mandating luminous efficacy standards that Favor LED adoption. The commercial sub-segment alone accounts for over 51% of lighting application revenue, driven by retrofit programs and green building certifications. The Consumer Electronics segment, particularly TV backlighting and display applications, is the fastest growing application category, with demand supported by the expanding LED & OLED Lighting Products and Displays Market globally.

Regional Insights

North America LED Driver Market Trends

North America holds the dominant position in the global LED Driver Market, with the United States serving as the primary engine of regional demand. The market's leadership is anchored in a mature regulatory environment, advanced infrastructure, and early adoption of smart lighting technologies. The U.S. DOE's ENERGY STAR program and successive efficiency standard updates have systematically elevated LED penetration across all building types. New York State's Smart Street Lighting NY program completed 500,000 smart LED streetlight installations ahead of schedule, demonstrating the scale of public investment driving driver demand.

On the innovation front, leading semiconductor companies including Texas Instruments, Analog Devices, and Microchip Technology are headquartered in the region and drive continuous R&D in driver IC platforms. The U.S. market is additionally benefitting from the Inflation Reduction Act (IRA), which allocates significant incentives for energy-efficient building retrofits, further stimulating commercial LED driver adoption.

Europe LED Driver Market Trends

Europe represents a technologically advanced and regulation-driven LED driver market, with Germany, the United Kingdom, France, and Spain leading regional adoption. The EU Ecodesign Regulation 2019/2020 phased out inefficient light sources and set minimum luminous efficacy thresholds, compelling large-scale replacement of fluorescent and halogen-based systems with LED alternatives. The European Green Deal and Renovation Wave Initiative are channelling investment into building energy efficiency upgrades, directly supporting demand for LED driver solutions in commercial and residential retrofit projects.

Germany leads in industrial and automotive LED driver adoption, with AMS-OSRAM AG and ROHM CO., LTD. maintaining strong regional manufacturing and R&D footprints. The United Kingdom is advancing smart lighting mandates for new commercial buildings under updated Building Regulations. Signify Holding (headquartered in the Netherlands) continues to drive connected lighting deployments across European cities.

Asia Pacific LED Driver Market Trends

Asia Pacific is both the largest and fastest-growing region in the global LED Driver Market, driven by a powerful combination of manufacturing scale, urbanization momentum, and government-mandated LED adoption programs. China dominates regional and global production, accounting for a substantial share of global LED driver manufacturing volume. China's 14th Five-Year Plan (2021-2025) prioritizes smart city development and green energy infrastructure, including widespread LED street lighting upgrades across hundreds of cities.

India's UJALA Scheme and Street Light National Programme (SLNP) have driven mass-market LED adoption, with the country targeting full conversion of public lighting infrastructure to LED. ASEAN nations, including Vietnam, Thailand, and Indonesia, are witnessing accelerated urbanization and infrastructure investment that is creating greenfield demand for LED-based street lighting, commercial buildings, and industrial facilities.

Competitive Landscape

The global LED Driver Market exhibits moderate consolidation, with the top five suppliers accounting for approximately 45% of combined market revenue. The competitive landscape balances global semiconductor incumbents such as Texas Instruments, STMicroelectronics, and NXP Semiconductors against specialized lighting-focused players including Signify Holding, AMS-OSRAM AG, and Macroblock, Inc. Market leaders differentiate through platform playsbundling driver hardware with cloud analytics, IoT connectivity, and service layers. Key strategies include acquisitions to expand regional footprints and accelerate R&D (e.g., Inventronics' acquisition of OSRAM Digital Systems), development of GaN and SiC-based high-efficiency drivers, and compliance with evolving automotive and smart building standards.

Key Developments:

- In August 2025, San’an Optoelectronics and Inari Amertron Berhad announced a joint plan to acquire full ownership of Lumileds Holding B.V. and its subsidiaries in Europe and Asia in a deal worth around USD 239 million. This acquisition is intended to expand San’an’s global footprint in LED technology by using Lumileds’ established product range and international presence to strengthen competitiveness in the global LED and lighting market.

- In April 2025, Analog Devices, Inc. unveiled the LT3755EMSE-2, a versatile LED driver IC supporting buck, boost, and SEPIC topologies with up to 3000:1 PWM dimming control for applications requiring flexible voltage regulation.

Companies Covered in LED Driver Market

- ACE LEDs

- Microchip Technology Inc.

- Cree LED

- HLI SOLUTIONS, INC.

- Signify Holding

- SAMSUNG

- Lutron Electronics Co., Inc.

- Macroblock, Inc.

- Analog Devices, Inc.

- NXP Semiconductors

- Semiconductor Components Industries, LLC

- AMS-OSRAM AG

- ROHM CO., LTD.

- STMicroelectronics

- Texas Instruments Incorporated

Frequently Asked Questions

The global LED Driver Market is valued at US$ 18.2 Bn in 2026 and is projected to reach US$ 51.3 Bn by 2033, expanding at a CAGR of 16.0% over the forecast period.

The key demand drivers include stringent global energy efficiency regulations such as the IEA's Net Zero Emissions lighting roadmap and the U.S. DOE's ENERGY STAR program, the rapid proliferation of smart lighting and IoT-enabled ecosystems, large-scale smart city infrastructure programs, and the accelerating adoption of LED lighting in electric vehicles.

The Driver IC segment leads the Component category with approximately 55% market share. Driver ICs dominate due to their ability to deliver precise constant-current regulation, compact form factor integration of multiple circuit functions, and support for advanced dimming and wireless control protocols.

North America is the leading region in the global LED Driver Market. The United States' strong regulatory framework encompassing the DOE's ENERGY STAR program and state-level efficiency mandates alongside early smart technology adoption, a robust innovation ecosystem anchored by leading semiconductor companies, and significant public investment in smart city LED deployments collectively underpin the region's leadership position.

The global LED Driver Market is served by a mix of semiconductor leaders and lighting specialists. Key players include Texas Instruments Incorporated, Signify Holding, STMicroelectronics, AMS-OSRAM AG, NXP Semiconductors, Analog Devices, Inc., ROHM CO., LTD., Semiconductor Components Industries, LLC (onsemi), Macroblock, Inc., Cree LED, Microchip Technology Inc., Lutron Electronics Co., Inc., SAMSUNG, ACE LEDs, and HLI SOLUTIONS, INC., among others.