- Automotive

- Driver Monitoring System Market

Driver Monitoring System Market Size, Share, and Growth Forecast 2026 - 2033

Driver Monitoring System Market by Component (Hardware, Software), by Technology (Camera-based DMS, Infrared LED-based DMS), by Functionality (Driver State Monitoring), by Vehicle Type, and Regional Analysis, 2026 - 2033

Driver Monitoring System Market Size and Trends Analysis

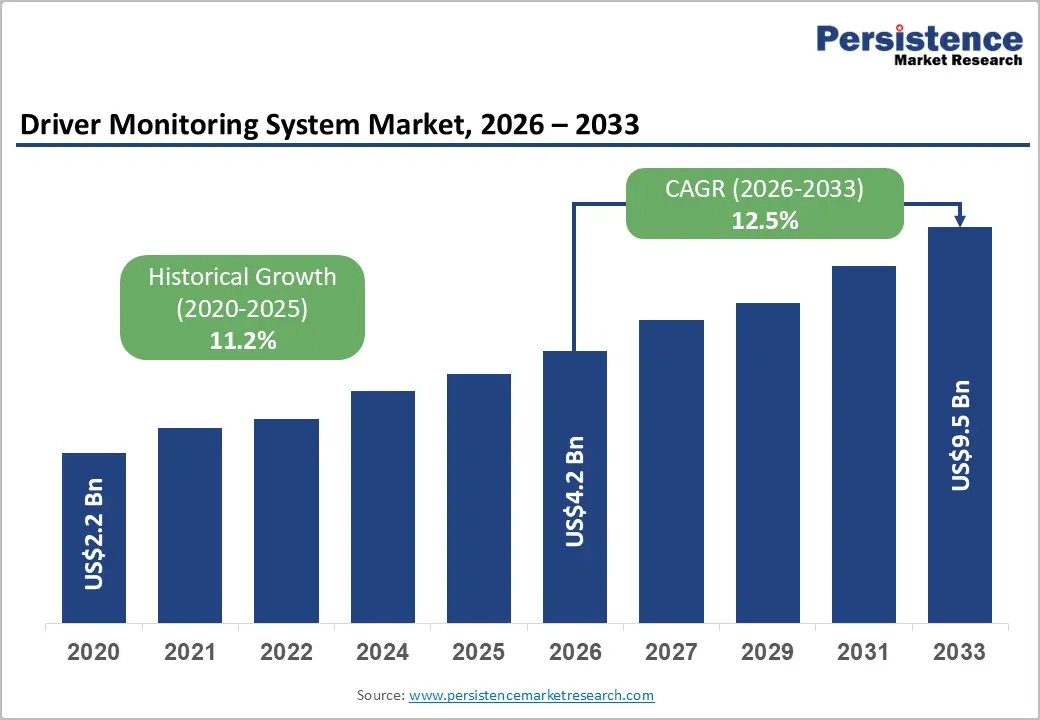

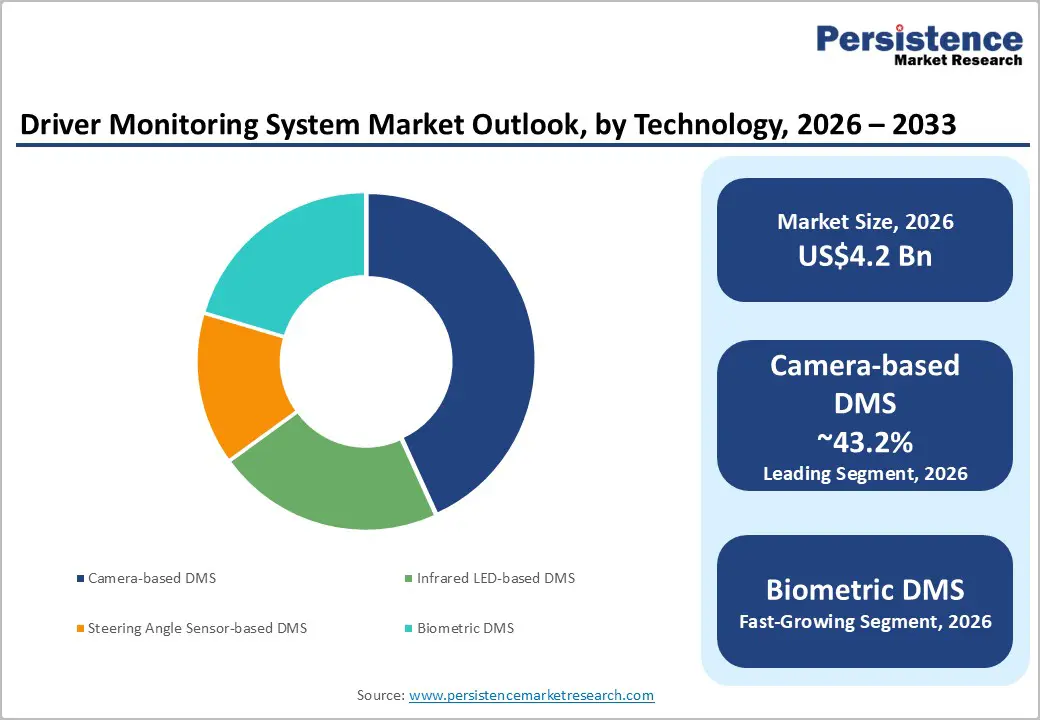

The global driver monitoring system market size is likely to be valued at US$ 4.2 billion in 2026 and is expected to reach US$ 9.5 billion by 2033, growing at a CAGR of 12.5% during the forecast period from 2026 to 2033, driven by the rising implementation of vehicle safety regulations mandating driver attention and drowsiness detection systems across leading automotive markets. Increasing integration of advanced driver monitoring systems with ADAS and autonomous driving technologies is further boosting adoption among OEMs.

Key Industry Highlights:

- Latest Agreement: In March 2025, Mitsubishi Electric Automotive America (MEAA) signed a Referral Agreement with Seeing Machines to promote the Guardian Generation 3 driver monitoring solution across the Americas. Guardian Generation 3 is an aftermarket DMS that tracks signs of distraction and drowsiness in real time and alerts drivers through visible and audible warnings.

- Leading Technology: Camera-based DMS has approximately 43.2% share in 2026, as it provides high-accuracy real-time tracking of eye movement, gaze, and head position.

- Dominant Functionality: Driver state monitoring, nearly 35.1% in 2026, as it directly targets fatigue and distraction, which are key causes of road accidents.

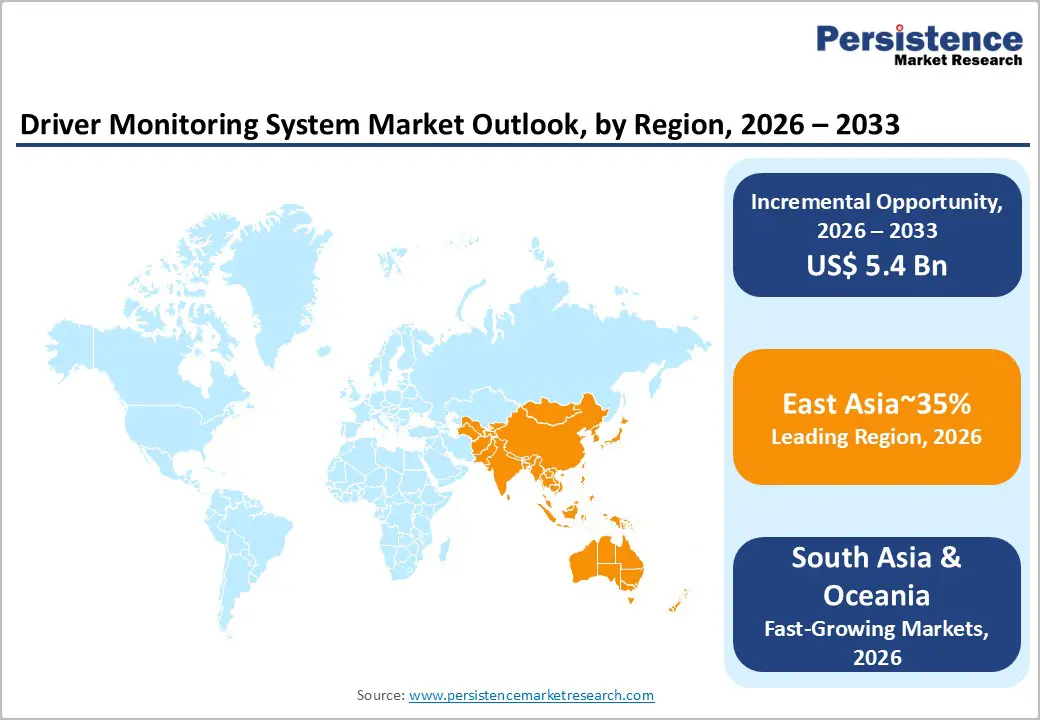

- Leading Region: North America, with about 36.3% share in 2026, backed by early adoption of advanced vehicle safety technologies.

- Fast-growing Region: Asia Pacific, owing to increasing vehicle production and surging investment by automakers in smart cabin technologies.

DRO Analysis

Driver - Strict Government Rules Push DMS into Every New Vehicle

Governments worldwide are making Driver Monitoring Systems (DMS) a legal requirement, not a premium feature. The EU's General Safety Regulation (GSR), established under Regulation (EU) 2019/2144, made Driver Drowsiness and Attention Warning (DDAW) systems compulsory for all new vehicles from July 7, 2024. The Advanced Driver Distraction Warning (ADDW) requirement, which mandates direct eye-tracking of the driver, applies to all new vehicle types from mid-2024. It extends to all newly registered vehicles across categories M and N from July 2026.

Euro New Car Assessment Program (NCAP) has strengthened this by tying DMS performance to its 5-star safety ratings, putting commercial pressure on automakers beyond just legal compliance. Fatigue is estimated to be responsible for 10 to 25% of all road crashes in Europe, which gives regulators a public safety basis for these mandates. China's Ministry of Transport has also issued directives requiring intelligent video surveillance in commercial vehicles, mirroring the EU's approach. This regulatory convergence across leading auto markets means manufacturers have little room to avoid adoption.

Urgent Need to Reduce Insurance Premiums among Fleet Managers

Fleet operators and transportation companies are increasingly implementing DMS solutions not only to enhance safety, but also to reduce operational expenses and improve overall fleet efficiency. Fleet insurance premiums hit a record US$0.102 per mile in 2024, with rates climbing another 8.8% in Q2 2025 alone. DMS-enabled telematics gives insurers verified behavioral data, including hard braking, distraction events, and eye closure frequency, that shifts the premium calculation in the fleet's favor. Telematics-equipped fleets are now securing 15 to 30% premium reductions, while others face double-digit increases.

Beyond insurance, the business case extends to cargo protection and driver behavior correction. Dash camera telematics allow fleet managers to receive data about driver behavior, enabling drivers to improve in the moment through self-coaching based on that data. For example, an 85-truck fleet in Houston saw an 18% premium reduction, saving US$378,000 annually, after sharing telematics data with its insurance carrier for 12 months. This type of measurable ROI is bolstering DMS uptake well beyond passenger vehicles.

Restraint- Driver Discomfort with Constant In-Cabin Surveillance

One of the most persistent barriers to DMS adoption is the unease drivers feel about being continuously monitored inside their own vehicles. Modern DMS setups use infrared cameras, gaze trackers, and facial expression analysis, all of which capture highly personal biometric data. The concern is not hypothetical. The Mozilla Foundation labeled cars the worst product category for privacy in its 2023 review, noting that connected vehicles collect data including biometrics, driving behavior, facial expressions, and video footage. High-profile incidents have deepened distrust.

A 2024 New York Times investigation revealed how General Motors collected detailed driver behavior data through its connected services program without clear driver consent. In commercial settings, this friction is particularly visible. A 2025 survey by the Chartered Management Institute found that while 53% of managers supported workplace monitoring, 42% opposed it, citing concerns that it undermines trust, invades privacy, or could be misused. Drivers often question whether their in-cabin data is being used purely for safety or shared with insurers, employers, or data brokers. It is anticipated to slow the willingness to accept systems that could otherwise reduce road fatalities.

Opportunity - Combination of Multiple Sensors

A key limitation of early DMS was that a single camera could be defeated by sunglasses, poor lighting, or unusual head positions. The shift toward multimodal sensor fusion addresses this issue. IDTechEx's In-Cabin Sensing report identifies near-infrared (NIR) cameras, time-of-flight (ToF) cameras, radar, and capacitive steering sensors as the core components now being combined for in-cabin monitoring. NIR cameras penetrate polarized lenses to track eye closure rates. Millimeter-wave radar adds a redundant layer by picking up micro-movements independent of lighting conditions.

Smart Eye's multimodal approach covers head tracking, eye tracking, facial expression analysis, and multimodal sensor data analysis simultaneously. This layered sensing makes it far harder for a drowsy or distracted driver to go undetected. China's C-NCAP 2024 draft rules have already begun scoring DMS on fatigue and attention monitoring scenarios, pushing automakers toward these superior multi-sensor designs. As the technology matures, systems can now reliably flag micro-sleeps and abnormal eye-closure patterns even under real-world conditions that previously caused false negatives.

Emergence of Health Sensing Features

DMS is expanding beyond alertness monitoring into passive, non-contact health surveillance, which is a significant opportunity for both automotive and healthcare adjacencies. At CES 2024, Bosch demonstrated interior radar running at 60 GHz capable of detecting changes in the breathing patterns of drivers. Its goal is to identify drivers in distress and allow the vehicle to stop safely while notifying emergency contacts. The research foundation for this is surging. A peer-reviewed study published in Scientific Reports (2023) by researchers at TU Braunschweig and Cambridge University demonstrated a multimodal in-vehicle system using ECG, PPG sensors, and a steering-wheel-facing RGB camera.

These can detect heartbeat irregularities during real driving scenarios across city, highway, and rural conditions. Cardiovascular diseases cause around 17.9 million deaths annually globally, and a vehicle that can detect the early signs of a cardiac event represents a genuine lifesaving use case. This positions DMS vendors to move up the value chain from safety compliance into connected health, potentially partnering with emergency response networks and health insurers.

Category-wise Analysis

Technology Insights

The camera-based DMS segment is predicted to lead with a share of approximately 43.2% in 2026, as it tracks eye closure, gaze direction, and head pose in real time. It is considered the most reliable indicator of distraction and drowsiness. Regulators have also validated this approach. For example, the European Commission mandates driver drowsiness and attention warning systems under the General Safety Regulation, and most approved solutions rely on camera sensors. This has pushed automakers to adopt camera-based DMS as a default.

The biometric DMS segment is estimated to be the fastest-growing in the forecast period, as it goes beyond behavior tracking. It measures physiological signals such as heart rate, stress levels, and fatigue patterns. This allows early detection of medical emergencies, which traditional camera systems cannot fully capture. For instance, the National Highway Traffic Safety Administration has emphasized the need for advanced driver state detection, including health-related risks, in its research on next-generation vehicle safety systems.

Functionality Insights

The driver state monitoring segment is anticipated to dominate with a share of nearly 35.1% in 2026, as it addresses the most prominent cause of accidents, i.e., human error. Driver distraction and fatigue remain the key contributors to road accidents globally. According to the World Health Organization (WHO), human factors account for the majority of road crashes. Driver state monitoring systems target these risks by detecting drowsiness, microsleep, and cognitive distraction. This functionality is also the first to be mandated by regulators. The EU safety rules, for instance, require attention warning systems, not identity recognition or comfort features.

The driver identification and authentication segment is expected to remain in the second position in 2026, as vehicles are becoming software-defined and personalized. Modern vehicles store user profiles, payment systems, and connected services. This creates a demand for secure and smooth driver identification. Biometric authentication, including face recognition or iris scanning, allows instant profile loading without keys or passwords. Tesla already uses cabin cameras to identify drivers and adjust seat position and settings. In China, NIO integrates facial recognition for driver login and vehicle access.

Regional Insights

North America Driver Monitoring System Market Trends

North America is anticipated to lead with a share of approximately 36.3% in 2026. The U.S. leads the regional market. This is due to the implementation of driver monitoring systems in Level 2+ and Level 3 autonomous driving packages delivered by companies such as General Motors (Super Cruise), Tesla (Autopilot), and Ford (BlueCruise). These systems require continuous driver attention monitoring by design, making DMS a functional necessity rather than an add-on. Regulatory momentum is also accelerating with the National Highway Traffic Safety Administration (NHTSA) endorsing DMS as a key safety feature in its updated New Car Assessment Program (NCAP).

U.S. Driver Monitoring System Market Trends

The U.S. market is accelerating rapidly as regulatory enforcement and commercial competition increasingly reinforce one another. In May 2026, the National Highway Traffic Safety Administration (NHTSA) announced that the 2026 Tesla Model Y became the first vehicle to successfully pass the agency’s newly updated Advanced Driver Assistance Systems (ADAS) evaluations under the New Car Assessment Program (NCAP), which now incorporates pass/fail criteria for driver assistance technologies. This development signals that Driver Monitoring Systems (DMS) are becoming a competitive necessity rather than an optional feature in modern vehicles.

Additionally, NHTSA’s 2024 amendment to FMVSS No. 208 introduced mandatory rear seat belt reminders by 2027, while the 2023 Advance Notice of Proposed Rulemaking (ANPRM) could pave the way for future DMS requirements aimed at preventing or restricting vehicle operation under driver impairment.

Asia Pacific Driver Monitoring System Market Trends

Asia Pacific is predicted to be the fastest-growing region in the forecast period, as it is being pulled forward by a mix of regulation, expansion, and EV adoption. Beyond China, the region's total vehicle production volumes are enormous, giving every incremental regulation an outsized market effect. India's surging focus on NCAP ratings, South Korea's ongoing ADAS deployment by Hyundai, Kia, and Genesis, and Japan's established OEM safety culture compound the regional momentum.

In 2024, Asia Pacific region generated almost a quarter of global DMS revenues, with China, Japan, and India leading the way. China's fast-growing electric vehicle market and increasing applications for smart cabins have fostered an acceleration in adoption across all segments.

China Driver Monitoring System Market Trends

The China market has shifted from voluntary to mandatory. Its latest C-NCAP management rules, effective from July 2024, include DMS in the active safety evaluation framework for the first time, assigning it a score of 2 points. This is significant as C-NCAP scores influence purchasing decisions across the country's massive car market. Following a fatal Xiaomi SU7 crash in early 2025 involving an automated driving feature, China's Ministry of Industry and Information Technology (MIIT) announced sweeping new regulations requiring SAE-level labeling of all ADAS functions and subjecting over-the-air updates to safety features to the same scrutiny as hardware recalls.

Japan Driver Monitoring System Market Trends

Japan's growth is steady rather than explosive, reflecting how deeply safety is already embedded in the country's automotive culture. Its prominent OEMs, such as Toyota, Honda, and Subaru have been deploying driver attention monitoring in their vehicles for years, predating regulatory mandates elsewhere. The Mitsubishi Electric Mobility and Seeing Machines capital partnership, announced in December 2024, signals Japan's intent to expand DMS commercially. Mitsubishi Electric Mobility stated that DMS will be mandatory in new European vehicles starting in 2026.

Europe Driver Monitoring System Market Trends

Europe is the most regulation-driven market in the world, and enforcement is tightening year on year. GSR mandates DDAW for all new vehicles from July 2024, with ADDW requiring eye-gaze tracking by July 2026 for all registrations, while Euro NCAP 2026 protocols eliminate compensatory scoring. It makes DMS performance non-negotiable for five-star ratings. This means automakers can no longer offset a weak DMS score with strong performance in other areas.

Germany Driver Monitoring System Market Trends

Germany is the technological engine of Europe's market. It houses the continent's largest OEMs and the world's most capable Tier 1 automotive suppliers. Germany's strong research and development and supplier base, led by Bosch, Continental, and Faurecia, focuses on advanced sensors and data analytics to detect fatigue or medical distress through vital sign and posture monitoring. Government initiatives and EU safety regulations are pushing in-car wellness adoption, with Germany leading due to the inclusion of DDAW systems in the EU General Safety Regulation.

U.K. Driver Monitoring System Market Trends

The U.K.'s growth is being influenced by compliance with EU safety standards and an independent legislative push on autonomous vehicles. Even after Brexit, the country continues to comply its vehicle safety requirements with Euro NCAP protocols, which now score DMS performance directly. The government passed the Automated Vehicles Act 2024, acknowledging that human error is a factor in 80% of collisions that result in personal injury. It has hence established a legal framework for authorizing self-driving vehicles on public roads. Autonomous vehicles require superior driver monitoring by design, mainly for systems with a user in charge who must be capable of retaking control.

Competitive Landscape

The global driver monitoring system market is moderately consolidated, with the presence of a small group of automotive Tier-1 suppliers and AI-based vision companies. Robert Bosch GmbH, Continental AG, Valeo SA, Denso Corporation, Magna International, Seeing Machines, and Smart Eye AB dominate due to long-standing OEM partnerships, integrated ADAS capabilities, and superior AI software portfolios. These leading players collectively account for over half of the global market. It shows that automakers prefer established suppliers with proven automotive-grade safety validation and large-scale manufacturing capability.

A key competitive divide exists between hardware integrators and pure-play AI software specialists. Companies such as Smart Eye AB, Seeing Machines, and Tobii AB specialize in eye-tracking algorithms, gaze estimation, and behavioral analytics, often licensing their software to large automotive suppliers. Another prominent trend is the entry of semiconductor and compute-platform companies into the value chain. NVIDIA Corporation, Arm Holdings, and advanced imaging firms are now influencing DMS architecture through AI compute platforms and edge-processing capabilities.

Key Industry Developments:

- In January 2026, Gentex presented an all-new driver and in-cabin monitoring demonstrator at CES 2026. It included 2D and structured-light-based 3D cabin monitoring for detecting passengers, behavior, objects, and the presence of life.

- In January 2026, Valeo and Seeing Machines announced that their joint In-Cabin Monitoring Solutions (ICMS) for driver and occupant applications would be featured across several Valeo demonstrations at CES 2026. The demonstrations included Valeo's Panovision head-up display, the Safe InSight demonstration vehicle presenting a multi-layer approach to driver and interior monitoring, and SmartCluster Helmet Detection for two-wheelers.

- In January 2025, Gentex Corporation unveiled its next-generation mirror-integrated driver and in-cabin monitoring system at CES 2025. It tracks driver head pose, eye gaze, and other metrics to determine distraction, drowsiness, sudden sickness, and return of manual control in semi-autonomous vehicles.

Companies Covered in Driver Monitoring System Market

- Valeo S.A.

- Denso Corporation

- Bosch Mobility Solutions

- Seeing Machines Limited

- Continental AG

- Smart Eye AB

- Aptiv PLC

- Magna International Inc.

- Visteon Corporation

- Lytx Inc.

Frequently Asked Questions

The global driver monitoring system market is projected to be valued at US$4.2 billion in 2026.

The driver monitoring system market is expected to reach US$9.5 billion by 2033.

Key market trends include the shift toward AI-based in-cabin sensing and integration of DMS with occupant monitoring systems.

Camera-based DMS is expected to be the leading technology with a share of nearly 43.2% in 2026, as it enables multi-functional in-cabin sensing using a single hardware unit.

The driver monitoring system market is expected to grow at a CAGR of 12.5% from 2026 to 2033.

Valeo S.A., Denso Corporation, Bosch Mobility Solutions, and Seeing Machines Limited are a few key market players.