- Industrial Machinery

- Drilling Machines Market

Drilling Machines Market Size, Share, and Growth Forecast, 2025 - 2032

Drilling Machines Market By Product Type (Radial Drilling Machines, Upright/Column/Pillar Drilling Machines, Others), Operation (Manual, Others), End-user Industry (Automotive, Aerospace & Defense, Fabrication & Industrial Machinery, Others), and Regional Analysis for 2025 - 2032

Drilling Machines Market Share and Trends Analysis

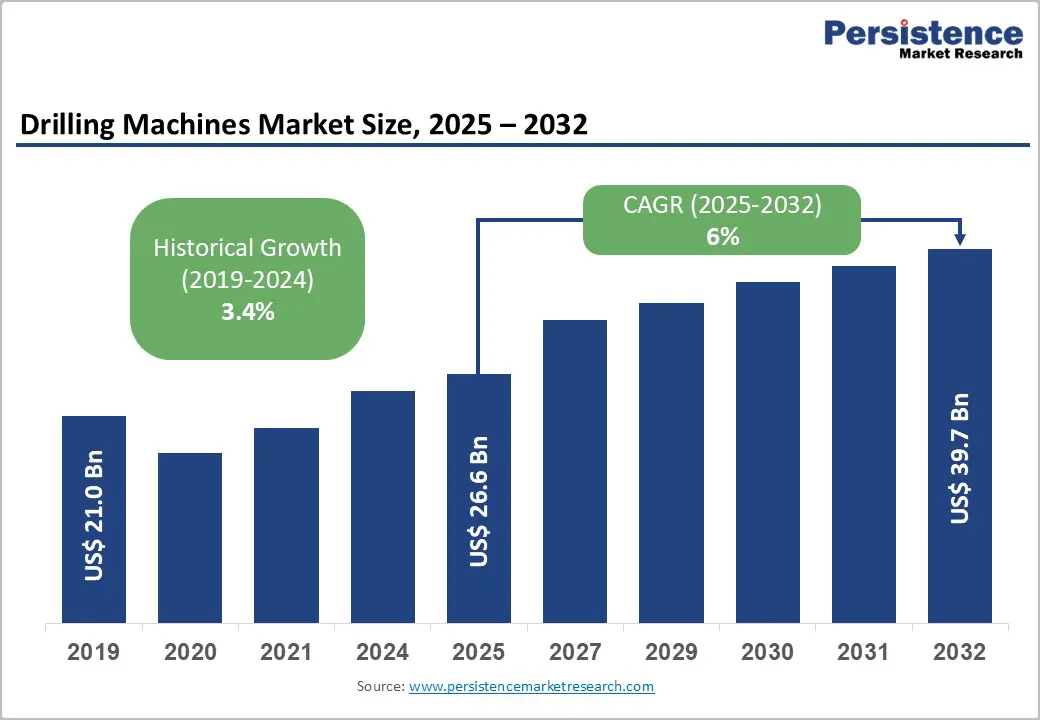

The global drilling machines market size is likely to be valued at US$26.6 Billion in 2025, and is estimated to reach US$39.7 Billion by 2032, growing at a CAGR of 6% during the forecast period 2025 - 2032, driven by ramping up of aerospace production, proliferation of electric vehicle (EV) battery assembly lines, and growing adoption of modular steel-frame construction.

Industrial automation, driven by CNC for predictive maintenance and quality control, shapes equipment priorities. Growth is fueled by Asia Pacific manufacturing and North American aerospace. Semi-automated drilling aids SMEs, while radial machines remain vital for engines and wind turbine gearboxes.

Key Industry Highlights

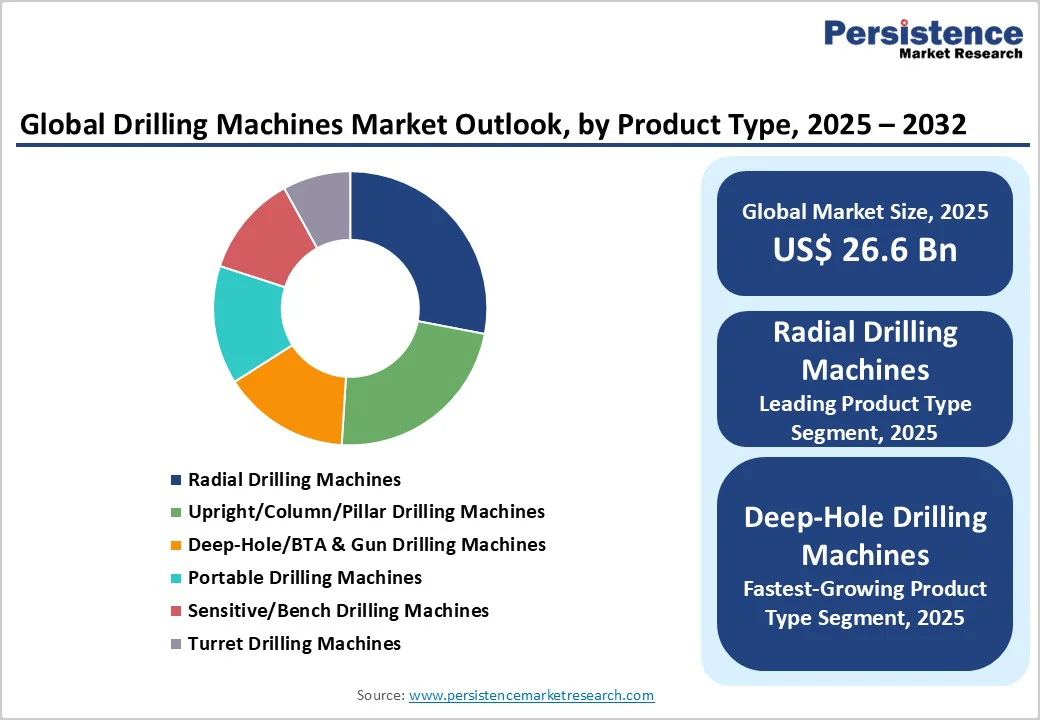

- Leading Product Type: Radial drilling machines lead with 28% of market revenue in 2025, while deep-hole drilling is set to grow the fastest during 2025 - 2032, backed by specialized aerospace and energy applications.

- Leading Operation: Semi-automatic machines dominate with 36.4% market share, balancing automation benefits and capital costs for SMEs, while CNC systems accelerate the fastest, driven by Industry 4.0 adoption.

- Dominant End-user: Automotive holds the largest revenue share at 25.7% in 2025, where aerospace & defense grows fastest through 2032, fueled by military modernization and commercial aircraft production ramp-ups.

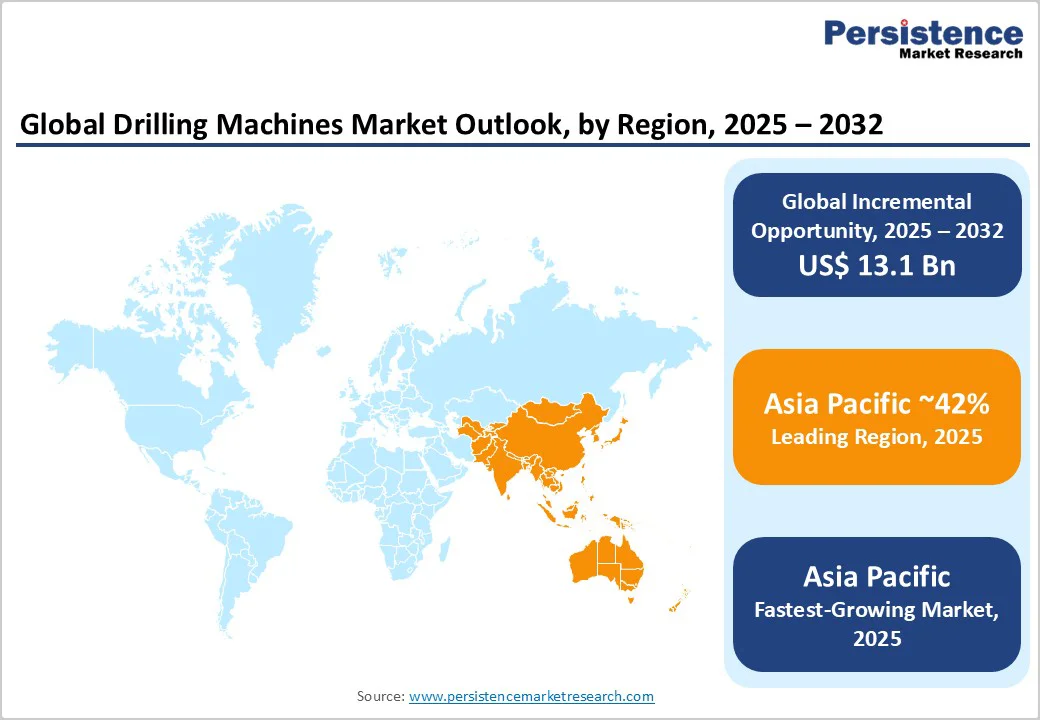

- Regional Dominance: Asia Pacific dominates with 42% of the market share in 2025, and grows at the highest CAGR, driven by China's manufacturing capacity expansion, India's defense localization initiatives, and ASEAN supply chain diversification.

- Player Strategies: Launch of drill bit technologies to deliver step-change tool life improvements, productivity enhancement through intelligent drill development, and platform expansions for creating a contractor ecosystem.

- April 2025: Borr Drilling secured new contracts for its jack-up rigs Thor, Gerd, and Norve, totaling approximately US$120 Million in revenue and extending operations through 2025 and 2026 across Vietnam, the Ivory Coast, and West Africa.

| Key Insights | Details |

|---|---|

| Drilling Machines Market Size (2025E) | US$26.6 Bn |

| Market Value Forecast (2032F) | US$39.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Aerospace Production Acceleration Driving Specialized Drilling Equipment Demand

Global aerospace manufacturers are ramping single-aisle aircraft production following pandemic-driven capacity cuts, reshaping drilling machine procurement patterns within airframe supply chains. This surge is stimulating the demand for large radial drilling machines capable of cutting titanium frame members with 25-micrometer positional repeatability in single-setup operations.

Fuselage section manufacturers require five-axis automation and pallet pool configurations to maintain throughput while meeting aerospace tolerance specifications. Military modernization programs are promoting market growth, with Navy contracts stipulating in-country machining for hull penetrations and missile launch tube installations, generating incremental orders for angle-head and deep-hole drilling rigs.

The shift toward composite materials in aerospace applications is further driving equipment specialization. Carbon fiber-reinforced polymers and ceramic matrix composites demand drilling parameters fundamentally different from aluminum alloys, creating replacement cycles even among recently purchased conventional metal drilling systems.

Suppliers offering multi-material drilling capability with automated tool changers and AI-driven monitoring to prevent delamination during composite drilling are capturing premium pricing. Drilling machine manufacturers with aerospace-certified equipment portfolios are expected to experience order visibility for a prolonged time period, enabling capacity expansion investments.

High Capital Investment and Skilled Operator Shortage Constraining Adoption

The drilling machine market growth faces headwinds from escalating equipment costs and persistent skilled labor shortages that disproportionately impact small and medium-sized manufacturers. Top-tier CNC drilling systems with multi-axis capability, integrated robotics, and digital twin connectivity now command prices between US$300,000 and US$800,000 per unit, placing advanced equipment beyond the financial reach of contractors operating on thin margins.

As a result, enterprises must simultaneously finance equipment purchases and allocate resources for extended operator training programs for complex CNC systems. This constraint intensified after the pandemic, as experienced machinists retired without proportional younger workforce entry, widening knowledge transfer gaps in specialized applications such as deep-hole drilling.

Regulatory compliance adds layers of operational complexity, with different ISO standards requiring specialized expertise and documentation systems. Smaller firms struggle to maintain compliance personnel while simultaneously investing in equipment maintenance capabilities for increasingly sophisticated machinery.

Equipment downtime from inadequate preventive maintenance disproportionately affects operations lacking in-house technical expertise, with unplanned failures potentially delaying projects by weeks while awaiting specialized technicians.

The fragmented regulatory landscape across jurisdictions further complicates multi-site operations, as drilling contractors must navigate varying permitting requirements, environmental restrictions, and noise ordinances that can extend project timelines and inflate costs.

EV Battery Manufacturing to Open New Opportunities

The accelerating global transition to EVs is generating exceptional growth opportunities in precision drilling equipment designed specifically for battery assembly line applications. The EV battery supply chain requires drilling operations radically different from traditional automotive manufacturing.

For example, battery tray assemblies, e-axle housings, and thermal management plates require micron-level precision and contamination-free operations to ensure electrical safety and thermal performance. Further, battery gigafactory construction is proliferating globally, and these facilities require multi-spindle gang drilling stations capable of processing aluminum battery enclosures at high throughput while maintaining dimensional tolerances.

Portable magnetic drilling machines are experiencing parallel growth in battery factory construction, driven by structural steel assembly requirements in rapidly deployed modular factory construction. The technical requirements of such cutting-edge drilling solutions create premium pricing opportunities.

Manufacturers offering complete drilling cells with robotic loading, multi-station drilling heads, and Industry 4.0 connectivity are positioned to capture disproportionate value in this emerging segment.

Category-wise Analysis

Product Type Insights

Radial drilling machines hold the largest revenue share at 28% in 2025, driven by their versatility in heavy fabrication, large component machining, and general industrial applications. Their adjustable radial arms allow drilling, reaming, and tapping on workpieces too large or complex for conventional column drills.

Automotive manufacturers extensively use radial drills for engine block, water jacket, and suspension bracket operations, where multi-position access without repositioning reduces cycle times. Similarly, wind turbine gearbox producers leverage long-reach radial capabilities for precise drilling of large-diameter ring gears and planetary carrier assemblies.

Deep-hole drilling machines are the fastest-growing segment through 2032, driven by aerospace, oil and gas, and medical applications. They deliver holes with length-to-diameter ratios over 10:1 while maintaining tight straightness tolerances. Aerospace adoption rises with increased titanium alloy usage in structural components requiring cooling channels and weight reduction.

Oil and gas recovery fuels demand for valve bodies and manifold drilling, while medical device manufacturers depend on deep-hole drilling for orthopedic implant cannulations and surgical instrument production, supporting robust market growth for this specialized segment.

Operation Insights

Semi-automatic drilling machines lead the market with roughly 36.4% of the market share in 2025. These systems automate feed control, depth limiting, and multi-position indexing while retaining manual workpiece loading, tool changes, and program selection. This hybrid setup boosts productivity without the extensive programming, fixture complexity, or capital required for full CNC automation.

Semi-automated machines are especially suited for job shops and contract manufacturers handling varied part geometries and moderate production volumes, where full automation is not cost-effective. The segment also benefits from simple operator training, with skilled manual drill operators typically reaching proficiency within weeks.

CNC and fully automated drilling systems are projected to grow fastest between 2025 and 2032, driven by Industry 4.0 adoption, rising labor costs, and demand for consistent quality in high-value manufacturing. These systems feature automated tool changers, pallet systems, and advanced sensor packages for real-time process monitoring and adaptive machining.

Automotive Tier 1 suppliers lead CNC adoption, particularly for engine block and transmission lines, with IoT integration enabling predictive maintenance and reduced downtime.

End-user Industry Insights

The automotive industry leads the drilling machine market, accounting for roughly 25.7% of revenue in 2025. Traditional internal combustion engine (ICE) production continues to drive demand for engine blocks, cylinder heads, transmission housings, and chassis components. However, growth through 2032 will reflect the shift toward EVs, which require distinct drilling approaches.

Battery tray assemblies demand precise hole patterns for cell modules and thermal management, while e-axle housings require tight-tolerance bearing bore drilling. CNC drilling adoption is rising as precision requirements tighten, with manufacturers integrating Industry 4.0 solutions such as automatic tool life management, statistical process control, and coordinate measurement systems.

The aerospace and defense sector is expected to grow fastest between 2025 and 2032, fueled by military modernization, commercial aircraft backlogs, and increased composite material usage.

Rising single-aisle aircraft production and domestic defense programs, such as India’s Make in India and European strategic autonomy initiatives, drive localized drilling machine demand. Manufacturers increasingly offer integrated equipment, tooling, and process optimization for complex aerospace materials.

Regional Insights

North America Drilling Machines Market Trends

North America accounts for about 24% of the global demand for drilling machines in 2025, driven by aerospace manufacturing resurgence, infrastructure modernization programs, and advanced manufacturing reshoring initiatives.

The U.S. dominates regional activity, with its diversified industrial base spanning aerospace, automotive, oil and gas equipment, and medical device manufacturing. The region's regulatory framework significantly influences equipment specifications.

For instance, OSHA workplace safety standards mandate machine guarding, emergency stop systems, and noise level compliance that often exceed international baseline requirements. These have effectively set in place a regional equipment standard that suppliers must address through design modifications or model variants.

The innovation ecosystem of North America positions it as a testing ground for advanced drilling technologies before broader commercialization. Industry 4.0 initiatives are particularly advanced in U.S. manufacturing, with automotive and aerospace suppliers implementing digital twin technologies, predictive maintenance algorithms, and automated quality verification systems that drive premium equipment specifications.

Infrastructure investment, catalyzed by the U.S. Infrastructure Investment and Jobs Act allocating US$1.2 Trillion over five years, is driving construction equipment demand, including portable magnetic drills for structural steel assembly and concrete core drilling systems for utility installations.

Europe Drilling Machines Market Trends

Europe commands roughly 26% of the drilling machines market share in 2025, backed by the region's mature industrial base, stringent regulatory environment, and emphasis on advanced manufacturing technologies. Germany maintains regional leadership, aided by its automotive industry concentration, aerospace component manufacturing, and machine tool production ecosystem.

The country's engineering excellence and Industry 4.0 leadership position positions German manufacturers as both primary drilling equipment consumers and technology developers.

BMW, Mercedes-Benz, and Volkswagen Group's extensive powertrain component production networks require continuous drilling equipment investments to maintain competitive productivity while transitioning toward EV architectures. France is home to automotive and aerospace giants, with Airbus headquarters and final assembly lines driving regional equipment procurement.

Europe’s regulatory environment strongly influences drilling machine design and adoption. Strict EU directives on safety, electromagnetic compatibility, and environmental impact require detailed compliance and advanced features beyond ISO standards. Energy-efficiency rules drive the use of variable-frequency drives and optimized spindles, while sustainability goals push operators toward water-based fluids, chip recycling, and lower compressed-air consumption.

Asia Pacific Drilling Machines Market Trends

Asia Pacific dominates the drilling machines market landscape with a 42% share in 2025, and leads growth momentum through 2032, on account of manufacturing capacity expansion, infrastructure investment, and increasing localization of precision component production. China commands the largest country market share, leveraging its vast manufacturing ecosystem to sustain drilling machine deployment across multiple end-use sectors.

The country's Made in China 2025 industrial policy explicitly targets high-end machine tool capabilities, incentivizing domestic drilling machine manufacturers while driving quality improvements to displace imported equipment in mid-tier applications.

China's large-scale infrastructure projects, including urban rail systems, bridge construction, and industrial park development, are sustaining the demand for portable drilling equipment and specialized foundation drilling systems.

India represents the fastest-growing major market within Asia Pacific, propelled by the Make in India initiative, defense industry localization requirements, and automotive sector expansion serving domestic and export markets.

The country's drilling machine market benefits from government infrastructure commitments, including highway construction, metro rail expansion, and industrial corridor development, creating equipment demand across construction and manufacturing applications.

Asia Pacific's price sensitivity drives regional equipment specifications emphasizing cost-effectiveness and operational simplicity, with many manufacturers offering simplified machine variants specifically designed for emerging market requirements.

Competitive Landscape

The global drilling machines market is moderately fragmented, with the top 10 manufacturers holding about 48% of the market share. Leaders such as Epiroc, Sandvik, Atlas Copco, and Kennametal leverage broad product portfolios, global distribution, and strong customer ties, emphasizing technological innovation to secure premium contracts in aerospace and automotive sectors.

Mid-tier players such as Bauer Maschinen, Boart Longyear, and Hitachi focus on niche markets and regional support. Competitive advantage increasingly relies on digital solutions, including remote monitoring, predictive maintenance, and consumables management, driving recurring revenues and enhancing customer retention through integrated service offerings.

Key Industry Developments

- In November 2025, Speedcast integrated Starlink HTS into COSL Drilling Europe’s semi-submersible rigs, boosting connectivity for safe, efficient, and low-carbon offshore operations. The hybrid dual-LEO and VSAT solution ensures 100% uptime, while Starlink PNI provides secure, low-latency data transmission, supporting COSL’s remote operations and operational efficiency goals.

- In September 2025, Herrenknecht opened a facility in India to tap into the growing infrastructure sector, offering localized sales, service, and support. This move aims to enhance competitiveness through faster delivery, better customization, and closer engagement with urban projects.

- In September 2025, Epiroc AB started building a global distribution center in Sweden to streamline spare parts supply, optimize logistics, enhance safety, and reduce environmental impact with solar panels, supporting growth and efficient aftermarket operations, opening in late 2027.

Companies Covered in Drilling Machines Market

- Epiroc AB

- Sandvik Mining and Rock Solutions

- Atlas Copco AB

- Kennametal Inc.

- Hilti Corporation

- DMG MORI Co., Ltd.

- Bauer Maschinen GmbH

- Boart Longyear

- Hitachi Construction Machinery Co., Ltd.

- DATRON AG

- Makino Milling Machine Co., Ltd.

- Fehlmann AG

- China National Petroleum Corporation (CNPC)

- Entrust Manufacturing Technologies, Inc.

- TIBO Tiefbohrtechnik GmbH

Frequently Asked Questions

The global drilling machines market size is projected to reach US$26.6 Billion in 2025.

Ramping up of aerospace production and proliferation of EV battery assembly lines are driving the market.

The drilling machines market is poised to witness a CAGR of 6% from 2025 to 2032.

Key market opportunities lie in modular steel-frame construction and industrial automation, especially CNC integration for predictive maintenance and real-time quality monitoring.

Epiroc AB, Sandvik Mining and Rock Solutions, Atlas Copco AB, and Kennametal Inc. are some of the key players in the drilling machines market.