- Technology

- Distributed Acoustic Sensing Market

Distributed Acoustic Sensing Market Size, Share, and Growth Forecast 2026 - 2033

Distributed Acoustic Sensing Market by Component (Hardware, Software, Service), by Fiber (Single‑mode Fiber, Multi‑mode Fiber), by Application (Pipeline Monitoring, Power Cable Monitoring, Subsea Cable Monitoring, Perimeter Monitoring, Fire Detection, Rail Monitoring, Transportation, Others), and Regional Analysis, 2026 - 2033

Distributed Acoustic Sensing Market Size and Trend Analysis

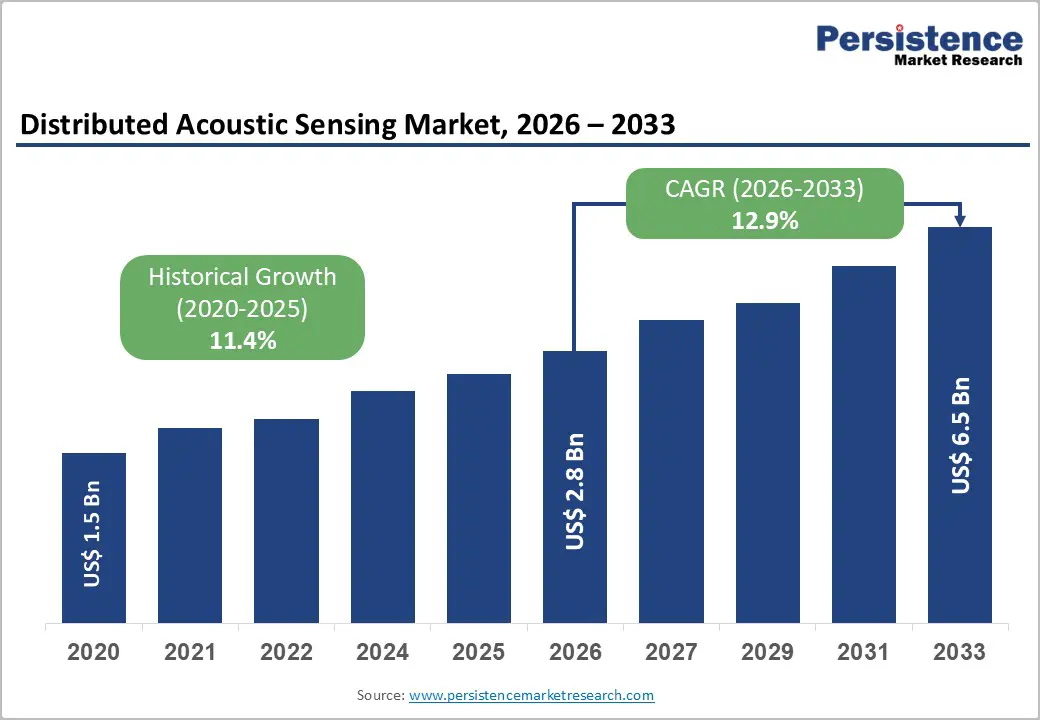

The global distributed acoustic sensing market is projected to reach US$ 2.8 billion in 2026 and US$ 6.5 billion by 2033, growing at a CAGR of 12.9% over the forecast period. This expansion is underpinned by rising demand for continuous, real-time monitoring across oil & gas, power transmission, transportation, and critical infrastructure sectors, where distributed acoustic sensing (DAS) converts existing optical fiber into thousands of virtual sensors.

Key Industry Highlights:

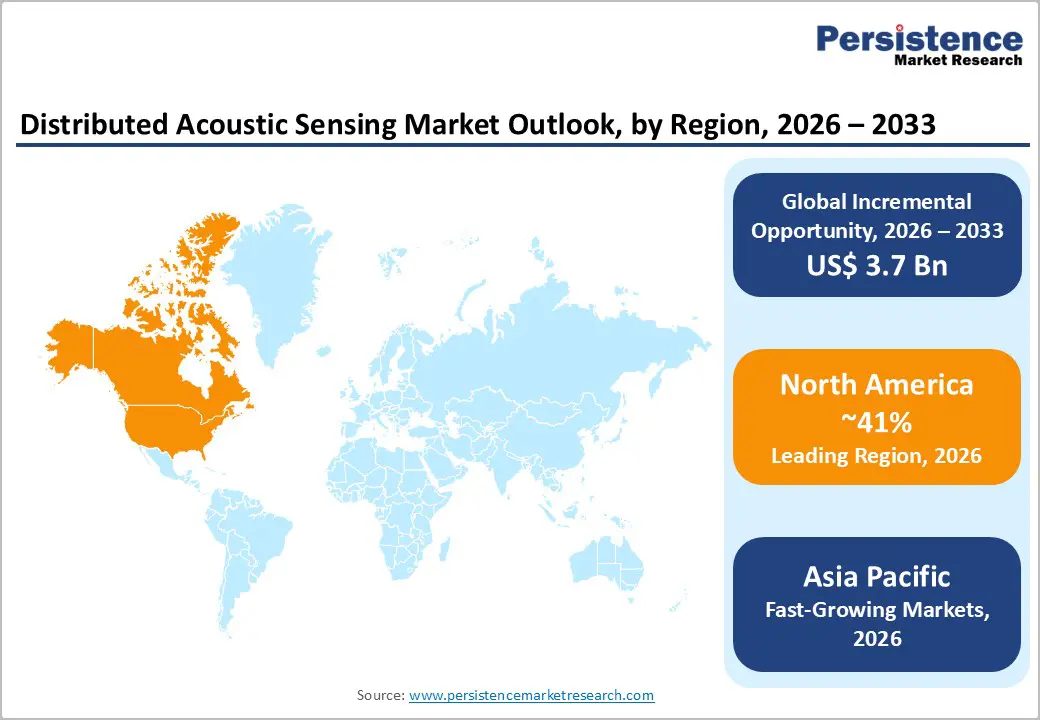

- Leading region: North America dominates the Distributed Acoustic Sensing Market, accounting for 41% of total revenue, owing to stringent pipeline-safety regulations, extensive oil & gas infrastructure, and a mature innovation ecosystem in fiber-optic sensing and IoT.

- Fastest Growing Region: Asia-Pacific is the fastest-growing region with a rising CAGR of 13.7%, driven by rapid infrastructure expansion, government-backed broadband programs, and rising demand for smart city and industrial monitoring solutions.

- Dominant Segment: Pipeline monitoring is the dominant application segment, accounting for about 35% of the Distributed Acoustic Sensing Market, supported by global safety regulations and large-scale oil & gas networks.

- Fastest Growing Segment: Perimeter Monitoring is the fastest-growing segment, with double-digit growth projected, fueled by border-security, airport, and industrial-facility deployments across North America and Europe.

- Key Market Opportunity: Integration of DAS with IoT, AI, and predictive maintenance platforms for oil & gas, utilities, and transportation offers a significant revenue opportunity, enabling digital twins and real-world applications.time asset-health insights.

| Key Insights | Details |

|---|---|

|

Distributed Acoustic Sensing Market Size (2026E) |

US$ 2.8 Billion |

|

Market Value Forecast (2033F) |

US$ 6.5 Billion |

|

Projected Growth CAGR (2026–2033) |

12.9% |

|

Historical Market Growth (2020–2025) |

11.4% |

Market Dynamics

Drivers - Real-Time Pipeline and Infrastructure Monitoring Regulations Are Accelerating Global Adoption of Distributed Acoustic Sensing Systems

The growing need for continuous and high-accuracy monitoring of pipelines, power cables, and transport corridors is a major driver of the Distributed Acoustic Sensing Market. Regulatory authorities such as the U.S. Pipeline and Hazardous Materials Safety Administration (PHMSA) and similar European agencies now require advanced leak detection and intrusion monitoring systems to improve infrastructure safety. DAS technology enables operators to monitor hundreds of kilometres using a single fibre line while detecting leaks, unauthorised activity, and ground movement with high spatial resolution.

This capability significantly enhances operational safety while reducing maintenance costs and downtime. As global pipeline networks continue to expand and ageing infrastructure requires upgrades, operators are increasingly choosing DAS as a cost-effective alternative to traditional point-sensor systems. The ability to deliver real-time insights across large areas makes DAS a critical tool for modern infrastructure management worldwide.

Rapid Expansion of Fibre-Optic and 5G Networks Is Unlocking New Cost-Effective DAS Applications Worldwide

The rapid expansion of fibre-optic communication networks and 5G infrastructure worldwide is strongly supporting growth in the Distributed Acoustic Sensing Market. Telecom companies and utilities are increasingly viewing unused or dark fibre as a valuable asset that can be repurposed for monitoring, security, and environmental sensing without installing new cables. Government broadband programs and telecom industry studies show that fibre deployment has increased significantly in fast-growing regions such as China, India, and Southeast Asia.

This widespread availability of fibre lowers installation costs and improves the economic feasibility of DAS solutions. As cities modernise and invest in smart infrastructure, DAS is finding new applications in railways, urban security, traffic monitoring, and utility management. The combination of expanding fibre networks and digital transformation continues to create strong long-term growth opportunities.

Restraints - High Capital Investment and Complex System Integration Continue to Limit Faster DAS Adoption across Industries

Although DAS offers strong long-term benefits, its high upfront investment remains a key challenge for many organizations. The cost of interrogator units, specialized software, fiber deployment, and system customization can be high, especially for smaller operators. In addition, integrating DAS with existing SCADA systems and legacy monitoring platforms often requires technical adjustments, cybersecurity upgrades, and employee training.

The large-scale DAS deployments in the oil & gas and power sectors can take several years to complete, increasing total project costs. Many companies also struggle to clearly measure return on investment during early implementation phases. Without standardized integration frameworks and simplified deployment models, some infrastructure owners remain hesitant to adopt DAS solutions. These financial and technical barriers continue to slow market penetration in cost-sensitive regions.

Lack of Technical Awareness and Skilled Workforce Slows DAS Deployment in Emerging Infrastructure Markets

In many developing regions, awareness of distributed acoustic sensing technology and its full potential remains relatively low. Engineers, regulators, and infrastructure planners often rely on traditional monitoring methods because they lack familiarity with fiber-optic sensing solutions. Training programs and local certification systems for DAS deployment remain underdeveloped, forcing companies to rely on international vendors and consultants.

Skill shortages and technology-transfer delays increase project risk and operational complexity. This lack of local expertise can lead to longer implementation timelines and higher maintenance costs, discouraging investment. As a result, even though infrastructure spending is rising in Latin America and parts of Africa, DAS adoption remains slower than expected. Strengthening technical education and regional partnerships will be essential to unlock future market growth.

Opportunity - Integration of DAS with AI, IoT, and Predictive Maintenance Platforms Is Transforming Smart Infrastructure Management

A significant growth opportunity lies in combining DAS technology with IoT platforms and AI-driven predictive maintenance systems. By integrating acoustic sensing data with pressure, temperature, and flow measurements, companies can create advanced digital models of infrastructure assets. These systems allow operators to predict equipment failures, detect corrosion, and identify structural stress before serious damage occurs. Research from technical journals shows that machine-learning algorithms trained on DAS data can recognize complex patterns with high accuracy, improving operational decision-making.

As Industry 4.0 initiatives continue to expand across manufacturing, energy, and transportation sectors, demand for intelligent monitoring solutions is rising rapidly. DAS is increasingly becoming a core component of smart infrastructure strategies. Its ability to deliver continuous, real-time data positions it as a key enabler of efficient and predictive asset management.

Rising Renewable Energy Projects and Subsea Monitoring Needs Are Creating High-Growth Opportunities for DAS Solutions

The renewable-energy sector is creating strong new opportunities for the distributed acoustic sensing market, particularly in offshore and subsea environments. DAS is increasingly used to monitor subsea power cables, wind-farm infrastructure, marine traffic, and anchor movement, helping reduce the risk of outages and costly repairs.

Regulatory bodies and grid operators are placing greater emphasis on real-time monitoring to improve system reliability and environmental protection. Large offshore wind projects in Europe, China, and the United States are investing in advanced fiber-optic sensing solutions as part of long-term asset protection strategies. Beyond renewables, DAS is gaining traction in geothermal energy and carbon capture projects for reservoir monitoring and well integrity management. These expanding applications are significantly increasing the addressable market and long-term growth potential for DAS providers.

Category-wise Analysis

Component-wise Insights

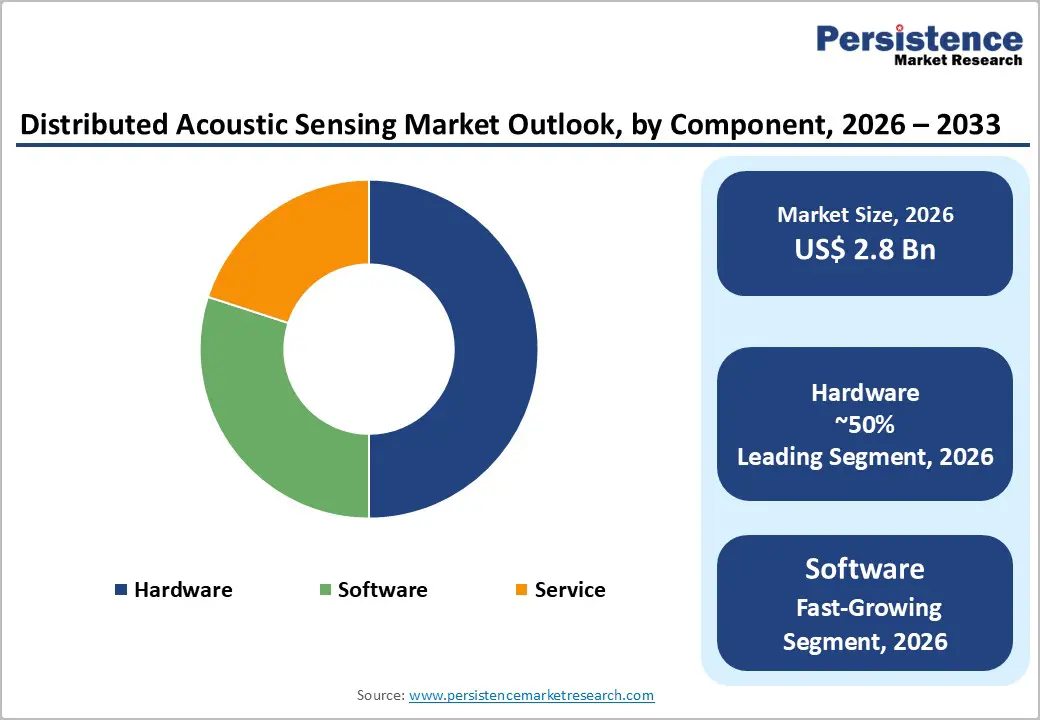

Hardware represents the largest share of the distributed acoustic sensing market, contributing nearly 50% of total market value. This dominance is mainly driven by the critical role of DAS interrogator units, which generate and analyze acoustic signals across fiber-optic cables. These devices are designed to deliver long-range monitoring, high sensitivity, and accurate signal processing, making them high-value components within DAS systems.

Leading vendors such as Halliburton, Schlumberger, and Optasense continuously invest in improving interrogator performance to support broader applications. The quality of hardware directly impacts system accuracy, detection range, and data reliability. As customers demand higher resolution and longer sensing distances, advanced interrogator systems continue to command premium pricing. This strong reliance on sophisticated hardware ensures its continued leadership within the overall market structure.

Fiber-wise Insights

Single-mode fiber dominates the fiber segment, accounting for approximately 85% of total usage. Its ability to support long-distance sensing with minimal signal loss makes it well-suited for monitoring large-scale infrastructure networks, such as pipelines, power grids, and transportation corridors. Government-backed broadband projects and smart-grid investments across China, India, Europe, and North America have significantly expanded single-mode fiber deployment.

This growing installed base provides a cost-efficient foundation for DAS retrofitting without major additional infrastructure investment. Technical research confirms that single-mode fiber offers superior signal stability and lower attenuation than multimode alternatives. These performance advantages enable precise acoustic detection over hundreds of kilometers. As long-range monitoring becomes increasingly important, single-mode fiber will remain the preferred choice across most DAS applications.

Application-wise Analysis

Pipeline monitoring remains the largest application segment, accounting for approximately 35% of total demand. Oil and gas operators use DAS to continuously monitor pipelines for leaks, unauthorized digging, ground movement, and mechanical stress. This aligns closely with safety regulations and environmental protection standards in major energy-producing regions. Regulatory frameworks in the U.S. and Europe increasingly require real-time surveillance of high-risk pipeline areas, accelerating DAS adoption.

Case studies from leading service providers indicate that DAS significantly reduces false alarms and improves emergency response times. The ability to cover long pipeline stretches using a single fiber system makes it highly cost-effective. As energy transportation networks expand globally and aging pipelines require enhanced safety measures, pipeline monitoring will remain a key revenue driver for the market.

Regional Insights

North America Distributed Acoustic Sensing Market Trends

North America leads the distributed acoustic sensing market due to strong regulatory frameworks, advanced infrastructure, and early technology adoption. The United States holds the largest share, supported by strict pipeline safety regulations and extensive oil and gas networks. Agencies such as the Department of Transportation and PHMSA promote real-time monitoring to reduce environmental risks and operational failures.

Major technology providers have established strong R&D and deployment hubs across Texas, California, and other energy-focused regions. In addition, telecom companies and utilities are increasingly using existing fiber networks for infrastructure monitoring and security applications. Smart-city initiatives in major urban areas are also testing DAS for traffic management and perimeter security. This combination of regulation, innovation, and infrastructure density makes North America a mature and high-value market for DAS solutions.

Europe Distributed Acoustic Sensing Market Trends

Europe shows strong regulatory-driven growth in the Distributed Acoustic Sensing Market, supported by harmonized safety and infrastructure policies across the region. Countries such as Germany, the U.K., France, and Spain are leading adoption in energy, transportation, and security sectors. European pipeline safety directives and renewable energy targets are pushing operators to invest in real-time monitoring technologies. Research institutions collaborate closely with DAS vendors to improve sensing range and accuracy. Cross-border infrastructure projects, including offshore wind connections and gas transmission networks, are major deployment areas for DAS systems. Rail monitoring pilots are also expanding across high-speed rail corridors. With strong policy support, technical expertise, and sustainability goals, Europe continues to be a stable and innovation-focused market driving long-term DAS adoption.

Asia Pacific Distributed Acoustic Sensing Market Trends

Asia-Pacific is the fastest-growing region, driven by substantial infrastructure development and rapid urbanization. China and India are investing heavily in pipelines, power transmission, smart cities, and high-speed rail systems, creating strong demand for real-time monitoring solutions. Government programs promoting fiber-optic expansion provide ideal conditions for DAS deployment. Utilities and rail authorities across the region are piloting DAS for asset protection and predictive maintenance. Southeast Asian countries are also adopting DAS for pipeline security and border monitoring with support from regional development programs. Manufacturing hubs in Japan and South Korea are employing DAS for industrial monitoring. The combination of infrastructure investment, digital transformation, and cost-efficient fiber deployment makes Asia Pacific the main growth engine of the global DAS market.

Competitive Landscape

The distributed acoustic sensing market is moderately concentrated, featuring a mix of large energy service companies and specialized fiber-optic sensing providers. Major players such as Halliburton, Schlumberger, and Baker Hughes dominate oil and gas applications, while firms like Optasense, Silixa, and Omnisens focus on infrastructure and security markets. Companies compete by leveraging advanced signal-processing algorithms, extended sensing ranges, and integration with analytics platforms.

Subscription-based DAS-as-a-service models are gaining popularity as they reduce upfront investment for customers. Continuous R&D efforts are driving innovations in multi-parameter sensing, combining acoustic, temperature, and strain monitoring in a single platform. The increasing use of AI-driven data analytics is further enhancing system value. This evolving competitive landscape is fostering rapid technological advancement and expanding application opportunities.

Key Developments:

- In February 2025, Halliburton Co. introduced an advanced DAS interrogator featuring enhanced spatial resolution and real-time analytics, designed for offshore oil & gas pipelines and subsea cables, with cloud-based monitoring enabling remote diagnostics and predictive maintenance for global operators.

- In October, 2024: Schlumberger Limited expanded its DAS footprint with a strategic deployment along high-voltage European transmission lines to monitor tower stability, conductor vibration, and external risk factors, aiming to reduce outages and support grid modernization under EU energy transition objectives.

- In March, 2024, Optasense broadened its DAS security portfolio with perimeter intrusion solutions for critical airports and major facilities in North America and Europe, offering real-time detection of intrusions, vehicle approaches, and threats, enhancing operational efficiency and perimeter protection.

Companies Covered in Distributed Acoustic Sensing Market

- Halliburton Co.

- Schlumberger Limited

- Optasense

- Future Fibre Technologies

- Fotech Solutions Ltd.

- Silixa Ltd

- Bandweaver

- Omnisens SA

- HiFi Engineering Inc.

- Baker Hughes Incorporated

- Solifos

- Aragon Photonics

- Febus Optics

- Senstar

- Yokogawa Electric

- Corning Incorporated

- Nokia Corporation

- Huawei Technologies Co., Ltd

Frequently Asked Questions

The Distributed Acoustic Sensing Market is projected to reach US$ 6.5 Billion by 2033, growing at a CAGR of 12.9% from 2026, driven by pipeline, power, and infrastructure monitoring demand.

Key demand drivers include stringent pipeline‑safety regulations, expansion of fiber‑optic networks, growth in renewable‑energy projects, and increasing adoption of IoT and AI for predictive maintenance.

Pipeline Monitoring is the dominant application segment, accounting for about 35% of the market, due to global oil & gas infrastructure and safety‑regulation requirements.

North America leads the Distributed Acoustic Sensing Market, supported by U.S. pipeline‑safety regulations, mature oil & gas sector, and advanced fiber‑optic and IoT ecosystems.

A key opportunity is integration with IoT and AI platforms for predictive maintenance in oil & gas, utilities, and transportation, enabling digital twins and real‑time asset‑health monitoring.