- Power Generation, Transmission, & Distribution

- Distributed Energy Resource Management System Market

Distributed Energy Resource Management System Market Size, Share, and Growth Forecast, 2026 - 2033

Distributed Energy Resource Management System Market by Component (Software, Service), Application Type (Solar PV Units, Energy Storage Systems, Wind Generation Units, EV Charging Stations), and Regional Analysis for 2026 - 2033

Distributed Energy Resource Management System Market Size and Trends Analysis

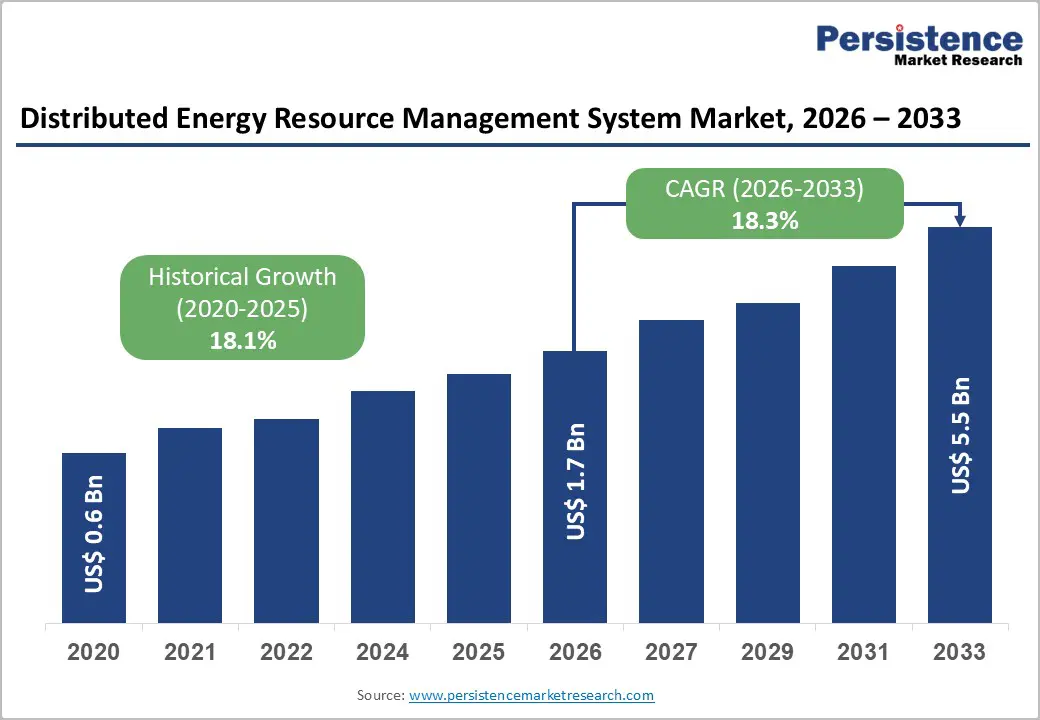

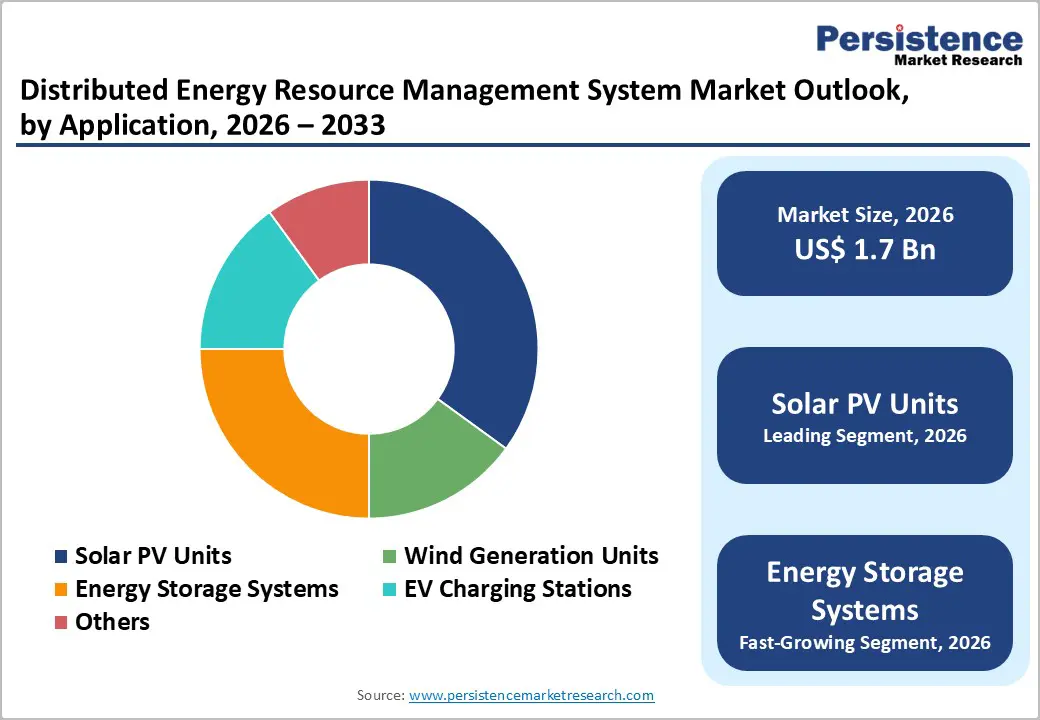

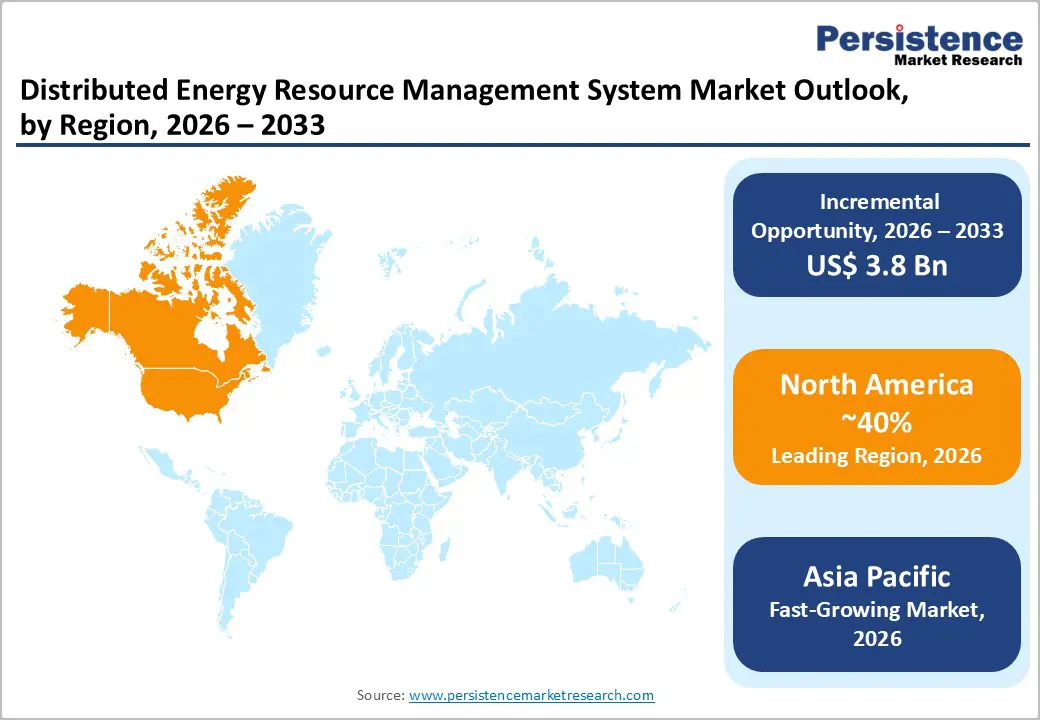

The global distributed energy resource management system market size is likely to be valued at US$1.7 billion in 2026 and is expected to reach US$5.5 billion by 2033, growing at a CAGR of 18.3% during the forecast period from 2026 to 2033, driven by an increase in distributed generation capacity across residential, commercial, and utility-scale applications.

The growing penetration of renewable energy sources such as solar PV, wind power, energy storage systems, and electric vehicle (EV) charging infrastructure has intensified the need for advanced grid coordination and real-time energy optimization solutions. Key growth drivers include government policy incentives for renewable energy deployment, ambitious decarbonization targets, and large-scale grid modernization initiatives to improve reliability, flexibility, and resilience.

Key Industry Highlights:

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by high penetration of distributed energy resources (DERs), supportive regulatory frameworks, and continued utility investments in grid resilience and digital energy platforms.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, driven by rapid urbanization, strong policy support, expanding renewable installations, and rising energy security initiatives across China, Japan, India, and ASEAN countries.

- Leading Component Type: The software segment is projected to represent the leading component in 2026, accounting for 58% of the revenue share, driven by its critical role in real-time analytics, control, and optimization of distributed energy resources.

- Leading Application: Solar PV units are anticipated to be the leading application type, accounting for over 50% of the revenue share in 2026, supported by widespread rooftop and utility-scale solar installations worldwide.

| Key Insights | Details |

|---|---|

|

Distributed Energy Resource Management System Market Size (2026E) |

US$1.7 Bn |

|

Market Value Forecast (2033F) |

US$5.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

18.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

18.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Adoption of Renewable Energy Sources

Power grids worldwide transition from centralized fossil-fuel-based generation to decentralized renewable energy models. Rapid deployment of solar photovoltaic systems, wind power installations, and distributed energy storage has significantly increased the complexity of grid operations. Unlike conventional generation, renewable energy sources are variable and intermittent, requiring advanced digital platforms to monitor, forecast, and balance supply and demand in real time.

Distributed energy resource management system (DERMS) enables utilities and grid operators to maintain grid stability, optimize energy flows, and improve visibility across geographically dispersed assets, making it essential for large-scale renewable integration. Government policies and decarbonization targets are accelerating renewable adoption across residential, commercial, and utility-scale applications. Incentives such as feed-in tariffs, net metering, renewable portfolio standards, and carbon reduction mandates are driving investments in distributed generation assets.

Renewable penetration rises, utilities increasingly rely on distributed energy resource management systems to coordinate distributed resources, support bidirectional power flows, and enable advanced use cases such as virtual power plants and demand response. The growing renewable energy footprint directly strengthens the demand for DERMS solutions to ensure efficient, resilient, and sustainable power system operations.

Regulatory Uncertainties and Interoperability Issues

Energy policies, grid codes, and interconnection standards differ between countries and sometimes even within states or provinces, creating a complex regulatory landscape for utilities and DERMS providers. These uncertainties can delay deployment timelines, increase compliance costs, and create ambiguity around the revenue models for distributed energy resources (DERs). Frequent changes or updates to renewable energy regulations, grid modernization incentives, and cybersecurity compliance requirements can disrupt project execution and create operational risks.

Utilities and technology providers often need to invest in legal consultations, policy monitoring, and adaptive strategies to align DERMS implementation with evolving regulatory frameworks. Modern grids combine legacy systems with advanced digital technologies, requiring DERMS platforms to communicate seamlessly with various hardware components, communication protocols, and vendor-specific solutions. Differences in data formats, control protocols, and software standards can limit real-time coordination, reduce operational efficiency, and increase integration costs.

For example, integrating solar PV systems, battery storage, wind turbines, and EV chargers from multiple vendors often necessitates custom interfaces or middleware solutions, adding complexity and risk. Lack of standardized protocols also affects scalability, as utilities face challenges when expanding DERMS deployments across multiple regions or DER types.

Integration of AI and Advanced Analytics

The penetration of distributed energy resources (DERs) such as solar PV, wind, battery storage, and EV charging stations continues to rise, and utilities face increasing complexity in balancing supply and demand, predicting load fluctuations, and optimizing energy flows. AI-driven DERMS platforms leverage machine learning algorithms, predictive analytics, and big data processing to provide real-time insights into grid operations. These technologies enable utilities to forecast renewable generation variability, detect potential system failures, and optimize the dispatch of distributed resources, enhancing both efficiency and reliability.

AI and advanced analytics unlock opportunities for innovative grid services such as virtual power plants (VPPs), automated demand response, and energy arbitrage. Through aggregation and intelligent orchestration of DERs, DERMS can optimize energy production and consumption at both local and regional levels, enabling utilities to participate more effectively in electricity markets. Advanced predictive models also support scenario analysis, risk management, and investment planning for new distributed assets. Cloud-based analytics and AI-driven platforms enhance scalability and interoperability, allowing utilities to integrate multiple DER types and vendors seamlessly.

Category-wise Analysis

Component Insights

The software segment is expected to lead the distributed energy resource management system market, accounting for approximately 58% of revenue in 2026, due to its critical role in analytics, monitoring, control, and optimization of distributed energy resources (DERs). Software platforms enable utilities to process real-time data, forecast load and generation variability, and integrate diverse DERs such as solar PV, wind, and energy storage into the grid efficiently.

Advanced features, including predictive analytics, automated dispatch, and real-time alerts, allow grid operators to maintain stability and improve operational efficiency. For example, Siemens’ Spectrum Power DERMS platform provides utilities with centralized control and visibility across thousands of DER assets, allowing efficient management of energy flows while optimizing grid performance.

The services segment is likely to represent the fastest-growing segment in 2026, driven by rising demand for consulting, integration, implementation, and ongoing maintenance. As DER penetration increases, utilities require professional services to address system complexity, ensure interoperability, and guarantee compliance with grid codes and evolving regulations. Services also support training, customization, and deployment of advanced DERMS platforms across residential, commercial, and utility-scale applications.

For example, Schneider Electric offers DERMS integration and consulting services that assist utilities in connecting diverse DER assets, optimizing operations, and maintaining system reliability. With utilities increasingly investing in distributed generation, energy storage, and EV infrastructure, professional services are essential to scale DERMS solutions effectively.

Application Insights

Solar PV units are projected to lead, capturing around 50% of the revenue share in 2026, due to the widespread adoption of rooftop and utility-scale solar installations. The variable and intermittent nature of solar generation necessitates real-time monitoring, predictive analytics, and optimization, all of which are provided by DERMS platforms. Utilities leverage DERMS to balance supply, forecast generation, and integrate solar power efficiently into the grid.

For example, GE Digital’s DERMS platform enables utilities to manage distributed solar farms, forecast PV output, and coordinate with other grid resources for enhanced stability.

Energy storage systems (ESS) are likely to be the fastest-growing application, driven by declining battery costs, increasing renewable adoption, and supportive policy incentives. ESS, including lithium-ion batteries and other storage technologies, provides critical functions such as peak shaving, load leveling, and grid stabilization. DERMS platforms optimize storage dispatch, integrate energy from solar or wind assets, and enable bidirectional flows to support virtual power plants and demand response programs.

For example, Tesla’s Autobidder software allows utilities to aggregate battery storage assets and optimize their real-time operation within the grid. As solar-plus-storage and wind-plus-storage projects expand, the energy storage systems segment grows rapidly, supporting grid flexibility, reliability, and renewable integration.

Regional Insights

North America Distributed Energy Resource Management System Market Trends

North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by the region’s high adoption of distributed energy resources (DERs), advanced grid infrastructure, and strong regulatory support. Utilities are increasingly deploying DERMS platforms to manage distributed solar PV, energy storage, wind, and EV charging assets efficiently. Key trends include the integration of renewable energy into the grid, expansion of microgrids, and adoption of virtual power plants (VPPs) to optimize energy flows and enhance grid resilience. The region also benefits from significant government incentives and funding for smart grid modernization, which accelerates DERMS adoption.

Leading technology providers are capitalizing on these trends by offering advanced DERMS solutions tailored for North American grids. For example, Siemens’s Spectrum Power DERMS platform allows utilities to monitor and control thousands of distributed energy assets in real time, optimize renewable integration, and enhance system reliability. Companies are also investing in AI-driven analytics, cybersecurity, and interoperability improvements, ensuring scalable and resilient DERMS deployments. North American utilities are increasingly leveraging predictive maintenance and real-time forecasting tools to minimize outages and improve operational efficiency.

Europe Distributed Energy Resource Management System Market Trends

Europe is expected to be a key market for distributed energy resource management systems (DERMS) in 2026, driven by the region’s ambitious renewable energy targets, grid modernization efforts, and increasing deployment of distributed energy resources (DERs). The European Union’s commitment to achieving net-zero carbon emissions, along with national renewable energy mandates, has accelerated the adoption of solar PV, wind, and energy storage systems.

Utilities are increasingly using DERMS platforms to integrate these variable energy sources efficiently, maintain grid stability, and optimize energy flows. European companies are developing DERMS solutions tailored to the region’s unique regulatory and operational requirements.

For instance, ABB’s Ability DERMS platform helps utilities integrate diverse renewable resources, manage energy storage, and optimize distributed generation across multiple areas. Firms are focusing on modular and scalable solutions, enabling utilities to implement DERMS gradually while maintaining compatibility with existing grid infrastructure. AI-based forecasting and predictive maintenance tools are being widely adopted to manage variability in renewable generation and reduce operational costs. Investments are also being made in cybersecurity and cloud-based analytics to ensure the secure and efficient integration of distributed energy resources.

Asia Pacific Distributed Energy Resource Management System Market Trends

The Asia Pacific region is expected to be the fastest-growing market for distributed energy resource management systems (DERMS), driven by rapid urbanization, industrialization, and strong government support for renewable energy integration. Countries such as China, Japan, India, and the ASEAN nations are increasingly deploying distributed energy resources (DERs), including solar PV, wind, energy storage systems, and EV charging infrastructure. Investments in smart grids, microgrids, and virtual power plants (VPPs) are rising to efficiently manage variable renewable energy generation. Policy measures, subsidies, and incentives for renewable adoption, combined with the need for energy security and reduced reliance on fossil fuels, are further accelerating DERMS deployment.

Leading technology providers are capitalizing on these trends by offering region-specific DERMS solutions designed to address local grid challenges. For example, Mitsubishi Electric Power Products’ DERMS platform enables utilities in Asia Pacific to monitor and control diverse distributed assets, optimize renewable integration, and support energy storage deployment. Companies are increasingly incorporating AI-driven analytics, cloud computing, and cybersecurity measures to ensure scalability, reliability, and real-time operational decision-making. With large-scale renewable projects expanding rapidly, DERMS adoption in Asia Pacific is expected to accelerate, creating opportunities for innovation, operational efficiency, and sustainable energy management across the region.

Competitive Landscape

The global distributed energy resource management system market is moderately fragmented, with established energy management companies, specialized DERMS vendors, and innovative startups competing for market share. Large technology and industrial firms leverage expertise in grid operations, digital transformation, and energy automation to develop DERMS platforms offering real-time monitoring, predictive analytics, and integration with diverse distributed energy resources. Strategic partnerships, acquisitions, and ecosystem collaborations help companies expand geographically and enhance solution portfolios.

Key players include Siemens AG, Schneider Electric SE, General Electric Company, ABB Ltd., and Oracle Corporation. Competition is driven by product innovation, improved interoperability, and comprehensive DERMS solutions for utilities, commercial enterprises, and distributed energy aggregators. Companies also differentiate through strategic alliances with utilities, R&D investment, and entry into emerging markets to capture growth opportunities.

Key Industry Developments:

- In November 2025, Husk launched its AI-driven distributed energy resources (DER) platform, “Powering Prosperity,” targeting the delivery of renewable electricity to 30 million households, businesses, and communities across Africa, South Asia, and Southeast Asia by 2030. The platform uses predictive and agent-based AI to optimize solar and battery storage operations in real time, maximizing renewable energy utilization while reducing costs. Husk aims to deploy at least 2 GW of DER assets over the next five years, supported by US$400 million in Series E funding.

- In March 2025, Itron, Inc. launched its IntelliFLEX grid-edge Distributed Energy Resource Management System (DERMS) solution to help utilities optimize the integration of distributed energy resources (DERs) and improve grid flexibility. The modular, scalable platform provided real-time visibility, control, and optimization of behind-the-meter DERs, including solar, batteries, and EVs, enabling utilities to unlock up to 20% more capacity in the distribution grid and defer costly infrastructure upgrades.

Companies Covered in Distributed Energy Resource Management System Market

- ABB

- GE DIGITAL

- Siemens

- Schneider Electric

- ENGIE Group

- Mitsubishi Electric Power Products, Inc.

- Itron Inc.

- Emerson Electric Co.

- Oracle

- Spirae, LLC

Frequently Asked Questions

The global distributed energy resource management system market is projected to reach US$1.7 billion in 2026.

The distributed energy resource management system market is driven by the growing adoption of renewable energy and the demand for real-time monitoring, control, and optimization of distributed energy resources.

The distributed energy resource management system market is expected to grow at a CAGR of 18.3% from 2026 to 2033.

Key market opportunities include AI and advanced analytics integration, virtual power plant (VPP) deployment, growth in energy storage solutions, microgrid development, and rising adoption of EV infrastructure.

ABB, GE Digital, Siemens, Schneider Electric, ENGIE Group, and Mitsubishi Electric Power Products, Inc. are the leading players.