- Testing, Inspection, & Certification

- Distributed Denial-of-Service (DDoS) Protection Market

Distributed Denial-of-Service (DDoS) Protection Market Size, Share, and Growth Forecast, 2025 - 2032

Distributed Denial-of-Service (DDoS) Protection Market By Component Type (Hardware, Software, Services), Application (Network Security, Others), End-user (BFSI, IT and Telecommunications, Others), and Regional Analysis for 2025 – 2032

Distributed Denial-of-Service (DDoS) Protection Market Size and Trends Analysis

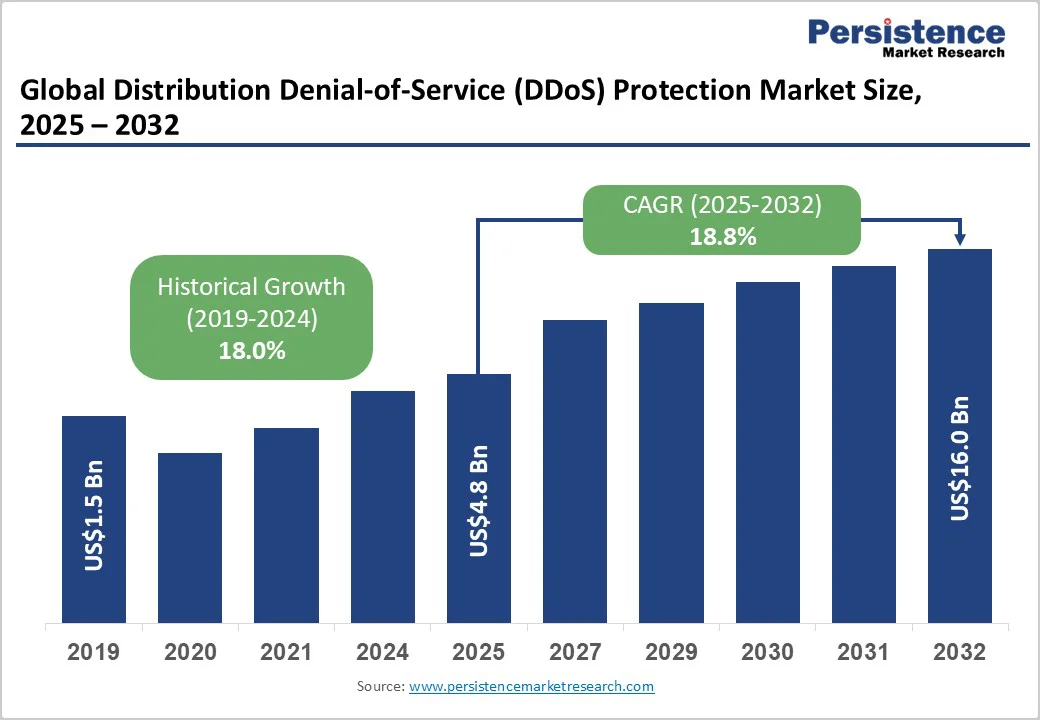

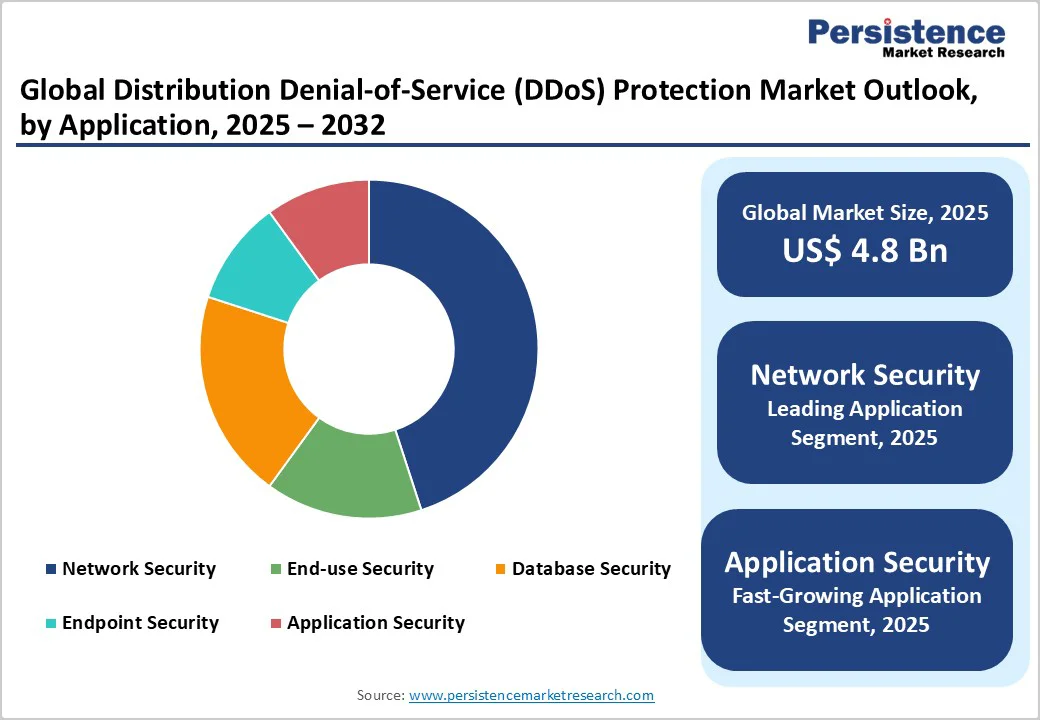

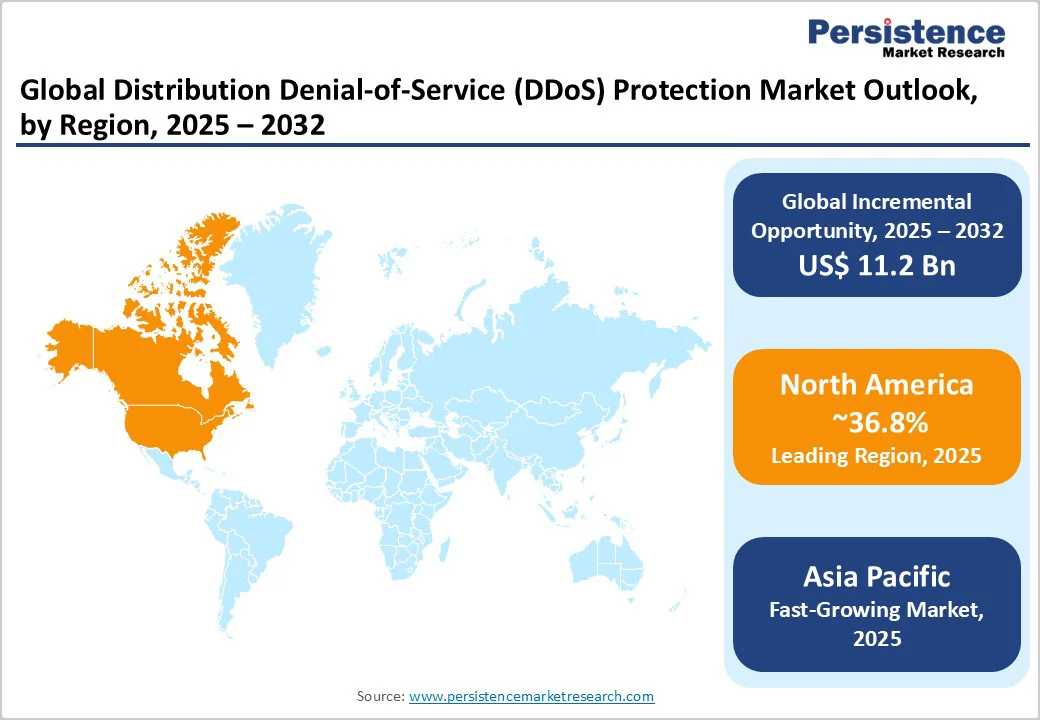

The global distributed denial-of-service (DDoS) protection market size is likely to be valued at US$4.8 Billion in 2025 and is expected to reach US$16.0 Billion by 2032, growing at a CAGR of 18.8% during the forecast period from 2025 to 2032, driven by the increasing prevalence of volumetric attacks, rising demand for cloud-based mitigation, and advancements in AI-driven detection. The need for always-on availability, especially in e-commerce, has significantly increased the adoption of distributed denial-of-service (DDoS) protection across industries. Innovations in software and network security, along with rising reliance on DDoS protection for business continuity in BFSI, continue to drive market growth.

Key Industry Highlights:

- Leading Region: North America, commanding a 36.8% market share in 2025, driven by a high cyber threat landscape, advanced cloud adoption, and strong R&D activities in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by digital economy boom, rising awareness of DDoS risks, and growing investments in cybersecurity in countries China and India.

- Dominant Component Type: Services, holding approximately 40% of the market share, due to rising adoption of managed security and cloud-based mitigation services.

- Leading Application: Network security, accounting for over 45% of the market revenue, driven by perimeter defense.

- Leading End-user: BFSI, contributing nearly 25% of market revenue, due to financial data sensitivity.

- Key Market Driver: Rising integration of zero-trust security frameworks across industries strengthens network resilience against evolving multi-vector DDoS attacks.

- Market Opportunity: Increasing cybersecurity investments in emerging economies present significant growth prospects for service providers and vendors.

|

Key Insights |

Details |

|

Distribution Denial-of-Service (DDoS) Protection Market Size (2025E) |

US$4.8 Bn |

|

Market Value Forecast (2032F) |

US$16.0 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

18.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

18.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Volumetric Attacks and Demand for Cloud-Based Mitigation

The growing occurrence of volumetric attacks, which are massive distributed denial-of-service (DDoS) attacks that flood networks with excessive traffic, has significantly increased the adoption of cloud-based mitigation solutions. These attacks, often surpassing terabits per second, can overwhelm enterprise servers, disrupt digital services, and damage brand reputation. For example, in 2023, Google Cloud mitigated a record-breaking DDoS attack of over 398 million requests per second, illustrating the rising scale and complexity of such threats.

As businesses increasingly migrate to digital and IoT-based ecosystems, the attack surface has expanded, making traditional on-premise security tools insufficient. Cloud-based mitigation solutions leverage AI-driven threat intelligence, scalable infrastructure, and real-time traffic analysis to detect and neutralize attacks before they affect service availability. They provide elasticity, enabling enterprises to efficiently handle sudden traffic spikes. Industries such as banking, e-commerce, and telecommunications are adopting these solutions to safeguard mission-critical applications. The combination of rising attack frequency and the demand for uninterrupted online services is pushing organizations toward cloud-native DDoS protection, positioning it as a key growth driver in the cybersecurity landscape.

High Implementation and False Positive Management Costs

The high costs associated with implementation and false positive management in distributed denial-of-service (DDoS) protection pose a significant restraint on market growth. Implementing these solutions often requires significant financial investment in hardware, software, and skilled personnel to ensure seamless integration with the existing IT infrastructure. Small and medium-sized enterprises (SMEs) particularly struggle, as enterprise-grade systems can demand substantial setup and maintenance expenses, including subscription fees for real-time monitoring and threat intelligence services.

False positive management adds another layer of complexity. Legitimate network traffic or user actions can be incorrectly identified as malicious, disrupting operations and user experience. Handling these incidents requires continuous monitoring, manual verification, and system adjustments, increasing costs and resource use. As a result, security teams often spend substantial time addressing false alarms instead of focusing on actual threats.

Advancements in AI-driven Detection and Zero-trust Architectures

Advancements in AI-driven detection and zero-trust architectures are transforming the modern cybersecurity landscape, enabling organizations to combat increasingly complex and stealthy cyber threats. AI-driven detection systems leverage machine learning and behavioral analytics to identify anomalies, detect potential intrusions, and respond to threats in real time. According to IBM’s 2024 Cybersecurity Report, AI-based systems can reduce threat detection times by up to 40% compared to traditional methods, significantly improving response efficiency. These systems continuously learn from vast datasets, allowing them to predict and counter new attack patterns such as ransomware, phishing, and DDoS attacks.

Zero-Trust Architecture (ZTA) has emerged as a foundational security model, operating on the principle of “never trust, always verify.” It eliminates implicit trust within networks, ensuring continuous verification of users, devices, and applications regardless of their location. Companies such as Google (BeyondCorp) and Microsoft have successfully implemented zero-trust frameworks to protect distributed workforces and cloud environments.

Category-wise Analysis

Component Type Insights

The services segment leads the DDoS protection market with a 40% share in 2025, due to the rising adoption of managed security and cloud-based mitigation services. Organizations increasingly outsource threat monitoring and incident response to specialized providers for 24/7 protection. Growing attack sophistication and lack of in-house expertise further drive reliance on service-based DDoS defense solutions.

Software is the fastest-growing segment, driven by the rapid adoption of AI-driven analytics, automation, and cloud-native solutions. Businesses prefer scalable, cost-effective software for real-time detection and mitigation of evolving cyber threats. Increasing integration with machine learning and zero-trust architectures further accelerates the demand for intelligent, adaptive security platforms.

Application Insights

Network security leads the market, holding a 45% share in 2025, driven by the need to defend against large-scale volumetric and infrastructure attacks. Its dominance stems from traffic scrubbing centers and perimeter-based defense solutions that ensure uptime and reliability. Growing digital connectivity and IoT expansion further fuel demand for robust network-layer protection.

Application security is the fastest-growing segment, driven by the surge in application-layer (Layer 7) attacks targeting web apps, APIs, and cloud platforms. Organizations increasingly adopt AI-driven and behavior-based tools to safeguard digital services. The rapid shift toward cloud-native and SaaS applications further accelerates application-level DDoS protection demand.

End-user Insights

BFSI dominates the market, contributing nearly 25% of revenue in 2025, driven by stringent regulatory compliance and the need to protect high-value, real-time transactions. Financial institutions rely on always-on DDoS defense to ensure uninterrupted banking operations, safeguard customer data, and maintain trust amid rising cyber threats targeting digital payment platforms.

The IT and telecommunication segment is the fastest-growing, due to increasing cloud adoption, 5G rollout, and high data traffic across networks. Service providers face frequent large-scale attacks targeting bandwidth and connectivity. Growing reliance on digital infrastructure and real-time communication services drives demand for scalable, AI-powered DDoS defense solutions.

Regional Insights

North America Distributed Denial-of-Service (DDoS) Protection Market Trends

North America is projected to account for nearly 40% of the global Distributed Denial-of-Service (DDoS) Protection Market in 2025, driven by extensive internet penetration, rapid cloud adoption, and the growing number of connected devices through IoT and 5G networks. The region’s strong digital infrastructure and the presence of major enterprises across the BFSI, government, IT, and telecommunications sectors fuel demand for robust DDoS mitigation solutions.

Increasing regulatory pressures and compliance mandates in the U.S. and Canada compel organizations to invest in advanced, managed, and cloud-based protection services to ensure data integrity and operational continuity. Leading providers such as Akamai Technologies, NetScout Systems, and Fortinet are focusing on AI-driven, scalable DDoS defense solutions tailored for North American enterprises. The region’s high frequency of volumetric and application-layer attacks has accelerated the adoption of real-time monitoring and automated mitigation tools.

Europe Distributed Denial-of-Service (DDoS) Protection Market Trends

Europe is driven by the rising frequency of large-scale and sophisticated cyberattacks targeting critical infrastructure, financial institutions, and government networks. The implementation of stringent cybersecurity regulations such as the EU NIS2 Directive and the Digital Operational Resilience Act (DORA) has accelerated the adoption of advanced DDoS mitigation solutions across industries. Increasing deployment of cloud services, IoT networks, and 5G infrastructure has further expanded the regional attack surface, creating a higher demand for scalable and intelligent protection systems.

Leading providers are focusing on AI- and ML-based traffic analysis, hybrid cloud mitigation, and managed DDoS services to strengthen resilience against evolving threats. The presence of established players such as Akamai Technologies, Orange Cyberdefense, and Deutsche Telekom contributes to innovation in security frameworks.

Asia Pacific Distributed Denial-of-Service (DDoS) Protection Market Trends

Asia Pacific is the fastest-growing market for distributed denial-of-service (DDoS) protection, driven by accelerating digital transformation, cloud adoption, and the surge in cyberattacks across industries. Enterprises and governments are increasingly investing in cloud-based, scalable, and AI-powered mitigation solutions to strengthen defense capabilities and ensure business continuity. Countries such as India, China, Japan, and South Korea are leading this growth, supported by strong regulatory initiatives and expanding digital infrastructure.

Advancements in machine learning-based detection, automated traffic filtering, and hybrid on-premise-cloud models are enhancing real-time protection. The Asia Pacific region is positioned as a key growth engine for the global DDoS protection market, fueled by rising threat complexity and rapid cybersecurity modernization.

Competitive Landscape

The global distributed denial-of-service (DDoS) protection market is highly competitive, comprising a diverse mix of cybersecurity giants and specialized solution providers. In developed regions such as North America and Europe, companies such as Akamai Technologies and Cloudflare, Inc. dominate through extensive research and development, advanced threat intelligence networks, and robust global infrastructure. These players offer scalable, cloud-based mitigation services capable of countering complex multi-vector attacks. In the Asia Pacific region, A10 Networks, Inc. and other regional firms are gaining traction by delivering localized, cost-effective, and high-performance solutions tailored to the needs of emerging economies.

The market is witnessing rapid transformation with a strong focus on AI-driven analytics, automation, and zero-trust architectures that enhance real-time detection and adaptive response capabilities. Strategic partnerships, mergers, and acquisitions are reshaping the competitive landscape, enabling vendors to expand their service portfolios and global reach. The increasing integration of machine learning, behavior-based threat detection, and cloud-native platforms provides a significant competitive edge.

Key Industry Developments

- In November 2025, Hitachi Solutions and Radware jointly announced the launch of a new cloud-based service in Japan to protect organizations from the surge in web-based DDoS attacks. The service uses artificial intelligence to rapidly detect and mitigate sophisticated attacks, generating defense signatures in seconds.

- In June 2025, researchers disclosed the ShadowV2 botnet, which exploits misconfigured Docker containers on AWS cloud servers to launch DDoS-for-hire services. This highlights the ongoing challenge of securing cloud infrastructure.

Companies Covered in Distributed Denial-of-Service (DDoS) Protection Market

- A10 Networks, Inc.

- Akamai Technologies

- Cloudflare, Inc.

- Corero Network Security

- F5, Inc.

- Fortinet, Inc.

- Imperva

- NETSCOUT System Inc.

- Radware

- TransUnion LLC

Frequently Asked Questions

The global distributed denial-of-service (DDoS) protection market is projected to reach US$4.8 Billion in 2025

The rising prevalence of volumetric attacks and demand for cloud-based mitigation are key drivers.

The distributed denial-of-service (DDoS) protection market is poised to witness a CAGR of 18.8% from 2025 to 2032.

Advancements in AI-driven detection and zero-trust architectures are key opportunities.g

A10 Networks, Inc., Akamai Technologies, Cloudflare, Inc., Fortinet, Inc., and Imperva are key players.