- Telecommunications

- Fiber Optic Connectors Market

Fiber Optic Connectors Market Size, Share, and Growth Forecast 2026 - 2033

Fiber Optic Connectors Market by Connector Type (Lucent Connectors, Mechanical Transfer Registered Jacks, Subscriber Connectors, MPO Connectors, Straight Tip Connectors, Ferrule Connectors, Others), Application (Telecommunication, Data Centers, Military, Television and Broadcasting, Aerospace and Avionics, Test and Measurement, Others), and Regional Analysis, 2026 - 2033

Fiber Optic Connectors Market Size and Trend Analysis

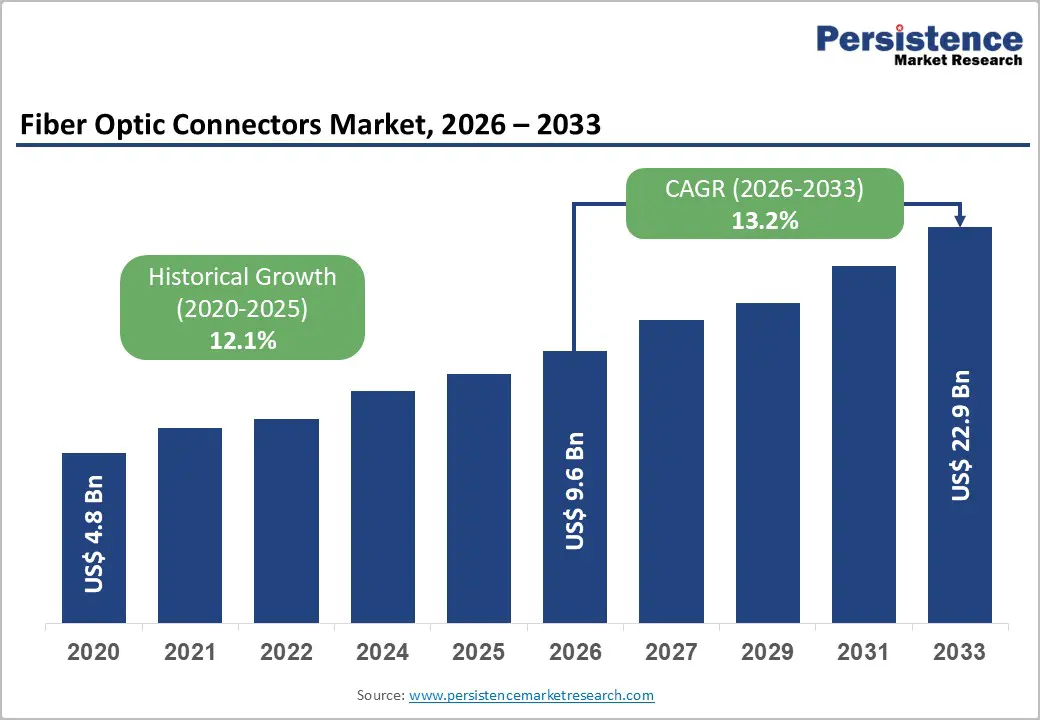

The global fiber optic connectors market size is projected to be valued at approximately US$ 9.6 billion in 2026 and is expected to reach US$ 22.9 billion by 2033, expanding at a CAGR of 13.2% during the forecast period from 2026 to 2033. Market growth is primarily driven by the rapid deployment of 5G infrastructure and the expansion of AI-driven data centers.

According to the ITU, global active mobile broadband subscriptions reached nearly 7 billion connections in 2023, driven by expanding smartphone adoption and growing mobile data consumption worldwide. Furthermore, large-scale investments in cloud computing, IoT integration, and edge computing continue to accelerate the adoption of high-performance fiber optic connectors across telecom and enterprise networks.

Key Market Highlights

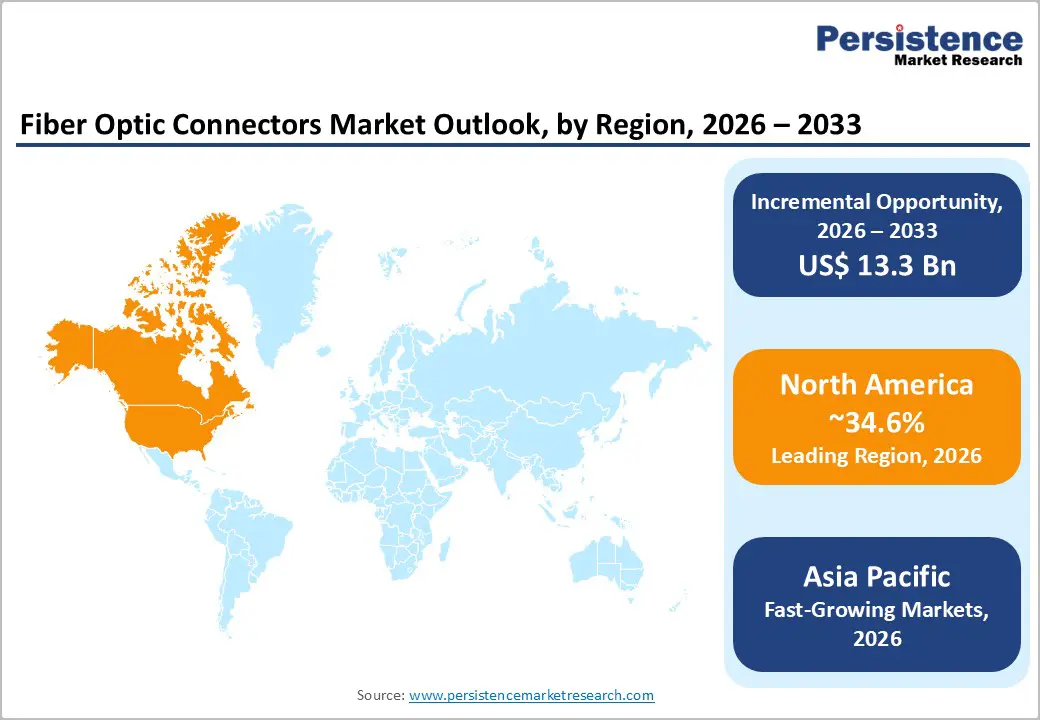

- Leading Region: North America holds about 34.6% market share, driven by strong U.S. broadband funding, large-scale 5G investments, and dense hyperscale data center presence.

- Fastest-Growing Region: Asia Pacific accounts for roughly 38.4% share and is the fastest-growing market, supported by China’s FTTH scale, India’s BharatNet rollout, and Japan’s mature fiber ecosystem.

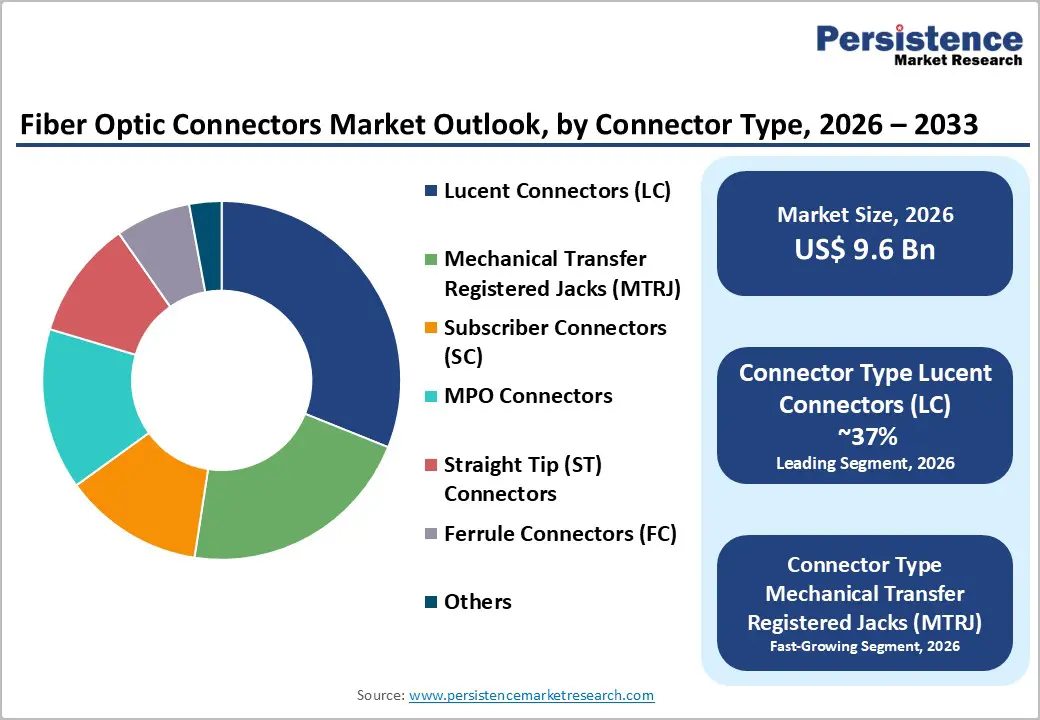

- Leading Category: LC connectors dominate with nearly 37% share, supported by compact design, high-density networking capability, and broad adoption across telecom, data centers, and FTTH.

- Fastest-Growing Category: Telecommunications contributes around 22.3% share, while data centers are the fastest-growing application due to AI-driven hyperscale expansion and 400G–800G Ethernet adoption.

- Key Market Opportunity: Expanding edge computing and industrial IoT deployments are driving demand for fiber optic connectors, supported by a projected 28.4% CAGR in the edge computing market through 2032.

| Key Insights | Details |

|---|---|

|

Fiber Optic Connectors Market Size (2026E) |

US$ 9.6 Billion |

|

Market Value Forecast (2033F) |

US$ 22.9 Billion |

|

Projected Growth CAGR(2026-2033) |

13.2% |

|

Historical Market Growth (2020-2025) |

12.1% |

Market Dynamics

Drivers - Accelerated 5G Network Deployment and Digital Infrastructure Investment

The rapid global rollout of 5G networks is creating strong demand for fiber optic connectors, as next-generation mobile architecture depends on dense fiber-based fronthaul, midhaul, and backhaul networks. With over 2.25 billion 5G connections worldwide by early 2025, telecom operators are upgrading network infrastructure to support higher data speeds, ultra-low latency, and massive device connectivity. Fiber has become a core enabler of this transition, accounting for a growing share of fixed broadband connections across developed economies.

Government-led and operator-driven investments in fiber infrastructure are further amplifying market growth. Large-scale initiatives focused on fiber-to-the-home (FTTH) and fiber-to-the-building (FTTB) deployments are expanding rapidly across both urban and rural areas. Programs such as India’s BharatNet, designed to extend broadband connectivity to hundreds of thousands of villages, are generating sustained demand for standardized, durable, and high-performance fiber optic connectors across access and aggregation network layers.

Exponential Growth in AI-Powered Data Centers and Hyperscale Computing

The accelerating adoption of artificial intelligence and machine learning is transforming data center architecture, driving a sharp rise in demand for high-speed fiber optic interconnects. Hyperscale data centers increasingly rely on optical transceivers capable of supporting ultra-high bandwidths, including 800G and emerging 1.6T technologies. These performance requirements place critical importance on low-loss, high-density fiber optic connectors to ensure signal integrity and scalability.

In parallel, innovations such as co-packaged optics and next-generation Ethernet switching are reshaping connectivity design within AI-focused data centers. As AI clusters scale to hundreds of thousands of GPUs and rack-level power densities increase significantly, efficient optical connectivity becomes essential. Fiber-optic connectors enable compact cabling, improved thermal management, and reliable, high-bandwidth data transmission, making them a foundational component of hyperscale and AI-driven computing environments.

Restraints - Rising Manufacturing Costs and Supply Chain Disruptions

The fiber optic connector manufacturing ecosystem is facing mounting cost pressures across materials, labor, and infrastructure deployment. Volatility in raw material pricing, combined with elevated costs for skilled labor in developed markets, is increasing overall production expenses. In parallel, shortages of specialized technicians and construction labor are constraining installation capacity, while regulatory and permitting processes for underground fiber deployment continue to extend project timelines. These factors are placing pressure on capital budgets and slowing the pace of network rollouts, particularly in dense urban environments.

Supply chain disruptions are further compounding these challenges. Constraints in critical inputs, including helium and specialized optical components, have introduced production uncertainties and limited scalability. Lengthy right-of-way approvals, environmental compliance requirements, and rising interim financing costs are adding to project risk. Additionally, evolving trade policies and tariffs on optical connector imports, especially in the United States, are creating pricing instability, complicating procurement strategies, and dampening near-term investment confidence across the fiber connectivity value chain.

Intense Price Competition from Chinese OEM Manufacturers

The global fiber optic connectors market is experiencing heightened price competition driven by the aggressive expansion of Chinese original equipment manufacturers (OEMs). Large-scale production capacity, cost-efficient manufacturing, and growing export volumes have enabled these suppliers to offer connectors at significantly lower prices, particularly in standardized product categories. This dynamic is intensifying competition across price-sensitive markets, especially in the Asia Pacific, where procurement decisions are often driven by cost rather than brand differentiation.

Margin pressure is most pronounced in high-volume connector segments such as LC and MPO connectors, where product standardization limits opportunities for premium pricing. Established global manufacturers are facing challenges in balancing competitive pricing with sustained investment in quality assurance and research and development. Smaller and mid-tier suppliers, lacking comparable economies of scale, are particularly vulnerable, accelerating market consolidation and constraining profitability across multiple tiers of the fiber optic connector supply chain.

Opportunity - Growing Adoption of Edge Computing and Industrial IoT Applications

The accelerating adoption of edge computing and industrial Internet of Things (IIoT) solutions presents a strong growth opportunity for fiber optic connector manufacturers. As data processing shifts closer to the source, ultra-low latency and high-reliability connectivity become critical for real-time applications in manufacturing automation, healthcare systems, and autonomous operations. Edge computing architectures rely on dense optical interconnects for intra-rack communication, localized data processing nodes, and distributed sensor networks, directly increasing demand for high-performance fiber optic connectors.

This opportunity is further amplified by the rapid expansion of industrial automation and smart infrastructure projects. Manufacturing facilities increasingly require fiber-to-the-machine connectivity to enable predictive maintenance, real-time quality control, and production optimization. In response, leading connector suppliers are developing ruggedized, high-density fiber solutions tailored for harsh industrial environments, positioning fiber optic connectors as essential components in the evolving edge computing and IIoT ecosystem.

Expansion of Fiber Infrastructure in Latin America and Southeast Asia

Latin America represents a rapidly expanding market for fiber optic connectors, supported by accelerated fiber broadband adoption and infrastructure modernization. Several countries in the region are witnessing sharp increases in fiber penetration as telecommunications providers transition away from legacy copper networks. This shift is generating sustained demand for standardized, cost-efficient fiber optic connectors across access, aggregation, and core network deployments.

At the same time, Southeast Asia is emerging as both a high-growth consumption market and a strategic manufacturing hub for fiber infrastructure. Countries such as Vietnam, Thailand, and Indonesia are advancing fiber deployments through smart city initiatives, industrial zone expansion, and government-led digital transformation programs. These developments create opportunities for connector manufacturers to establish localized production, strengthen regional distribution networks, and capture early-market advantages as next-generation fiber connectivity becomes foundational to regional economic growth.

Category-wise Analysis

Connector Type Insights

Lucent Connectors (LC) lead the global fiber optic connectors market with an estimated 37% market share, supported by their compact 1.25 mm ferrule design that enables high-density cabling in data centers and telecom networks. Their push-pull latch mechanism simplifies installation while ensuring secure connections. Broad compatibility with SFP-based transceivers, suitability for FTTH deployments, and strong manufacturing standardization have reinforced LC connectors as the preferred industry standard across enterprise and carrier networks.

The fastest-growing connector type segment is MPO/MTP multi-fiber connectors, driven by rising demand for parallel optics and ultra-high-bandwidth transmission. Hyperscale data centers are increasingly adopting these connectors to support 400G, 800G, and next-generation Ethernet architectures. Growth is further accelerated by spine-leaf network designs, co-packaged optics, and the need for high-density fiber harnesses that reduce cabling complexity while improving scalability.

Application Insights

Telecommunications remain the leading application segment, accounting for approximately 22.3% of the global fiber optic connectors market. This dominance reflects the essential role connectors play in backbone networks, mobile base station interconnections, and last-mile broadband deployments. The global expansion of 5G infrastructure continues to drive demand for ultra-reliable, low-latency fiber connectivity across fronthaul, midhaul, and backhaul network layers.

Data centers represent the fastest-growing application segment, supported by rapid expansion of cloud computing, artificial intelligence workloads, and hyperscale facility construction. Operators require high-density, low-loss connectors to optimize rack space and enable ultra-high-speed Ethernet standards. Emerging technologies such as co-packaged optics and silicon photonics are further increasing demand for advanced fiber connector solutions.

Regional Insights

North America Fiber Optic Connectors Trends

North America holds a leading position in the global fiber optic connectors market, accounting for an estimated 34.6% market share, driven primarily by the United States. Aggressive 5G deployment, federally supported broadband expansion programs, and dense hyperscale data center concentration continue to fuel demand for high-performance fiber connectivity. Strong investments by cloud service providers and telecom operators are accelerating the adoption of advanced connector technologies across both urban and rural infrastructures.

The region also benefits from mature telecommunications networks, rapid technology adoption, and favorable regulatory frameworks. Canada and Mexico contribute meaningfully to regional growth, with Mexico showing particularly strong momentum in fiber broadband adoption. Demand is increasingly shifting toward premium, specialized connectors, including military-grade, aerospace-certified, and high-density data center solutions, reinforcing North America’s position as a high-value market.

Europe Fiber Optic Connectors Trends

Europe represents a significant and steadily expanding market for fiber optic connectors, supported by large-scale digital infrastructure initiatives and EU-wide broadband targets. The region is projected to grow at a CAGR of around 12% during the forecast period, driven by strong fiber rollout programs in major economies such as Germany, France, and Italy. Public funding and regulatory mandates are accelerating FTTH and FTTB deployments across both urban and rural regions.

Western and Central Europe dominate regional demand, with countries such as France, Germany, and the Nordics leading multi-gigabit fiber adoption. The region’s emphasis on quality standards, energy efficiency, and long-term network resilience is encouraging adoption of high-specification fiber connectors. Growing Wi-Fi 7 readiness and next-generation broadband services are further strengthening demand for advanced, low-loss connector solutions.

Asia Pacific Fiber Optic Connectors Trends

Asia Pacific is the fastest-growing regional market, accounting for an estimated 38.4% share of the global fiber optic connectors market, led by China, India, and Japan. China remains the world’s largest FTTH market, supported by large-scale 5G investment and national data center initiatives. High export volumes of fiber cable and components reflect the region’s manufacturing dominance and rising internal demand.

India and Southeast Asia are emerging as key growth engines, driven by nationwide fiber expansion programs, smart city projects, and industrial digitization. Japan continues to lead in FTTH penetration and technology maturity. Rapid urbanization, expanding cloud infrastructure, and cost-effective manufacturing capabilities position the Asia Pacific as both the largest demand center and the most influential production hub for fiber optic connectors globally.

Competitive Landscape

The global fiber optic connectors market exhibits a moderately consolidated competitive structure, characterized by the presence of large multinational manufacturers alongside specialized niche players. Competition is particularly intense in high-volume, standardized connector categories such as LC and SC, where pricing pressure limits margins. Leading players collectively account for a significant portion of total market share, supported by scale advantages, global distribution networks, and strong manufacturing capabilities, with strategic focus centered on 5G infrastructure and hyperscale data center connectivity.

Market participants are increasingly differentiating through technology innovation, partnerships, and operational strategies rather than pricing alone. Emphasis is placed on improving optical performance, developing high-density connector designs, and enhancing durability for harsh environments. Emerging trends include vertical integration, regionalized manufacturing to reduce supply chain risk, and value-added services such as deployment support and network optimization to strengthen long-term customer relationships.

Key Market Developments

- In May 2025, Corning Incorporated announced a deepened collaboration with Broadcom to supply optical components, including fiber harnesses and high-density connectors for Broadcom's Bailly CPO system and next-generation 200G per lane CPO solutions. This partnership focuses on delivering unprecedented speeds and bandwidth concentrations with lower power consumption for AI-powered data centers.

- In March 2025, Sumitomo Electric Industries and 3M announced an assembler agreement enabling Sumitomo Electric to offer expanded beam optical interconnect solutions featuring 3M Expanded Beam Optical (EBO) Ferrule technology. Sumitomo Electric is expanding production capacity 7 times the previously announced target due to surging customer demand, planning to debut 12- and 16-fiber EBO cable assemblies at OFC 2025.

- In March 2025, Molex introduced its VersaBeam EBO interconnect solutions offering 12, 16, or 144-fiber connector options for hyperscale data centers. These high-density connectors leverage 3M EBO ferrule technology, reducing inspection and cleaning time by 6 times and deployment time by 85% based on field testing with Ciena and hyperscale data center customers.

Companies Covered in Fiber Optic Connectors Market

- Siemens AG

- Hitachi Information and Telecommunication Engineering Ltd.

- 3M

- Sumitomo Electric Industries Ltd.

- Broadcom Inc.

- TE Connectivity

- Corning Incorporated

- Furukawa Electric Co. Ltd

- OFS Fitel LLC

- Amphenol Corporation

- Fujikura Ltd., Belden Inc.

- Hirose Electric Co. Ltd.

- Optical Cable Corporation

- Molex LLC

Frequently Asked Questions

The global fiber optic connectors market is valued at about US$ 9.6 billion in 2026 and is projected to reach US$ 22.9 billion by 2033, growing at a 13.2% CAGR driven by 5G, AI data centers, and broadband digitalization.

Growth is fueled by 5G deployment (2.25+ billion connections), AI data centers supporting up to 1.6 Tbps, cloud computing, IoT proliferation, and large government broadband programs such as BharatNet and France Relance.

LC connectors lead with ~37% market share, supported by compact design, high-density compatibility, and widespread use across telecom, data centers, and FTTH networks.

North America holds ~34.6% share, driven by strong U.S. broadband funding, US$ 275 billion 5G investment, and hyperscale data center concentration, while Asia Pacific is the fastest-growing region.

Edge computing growth at 28.4% CAGR, AI-driven hyperscale data centers, Latin American fiber expansion, and Southeast Asian manufacturing hubs present major long-term opportunities.