- Medical Devices

- Disposable Medical Supplies Market

Disposable Medical Supplies Market Size, Trends, Share, Growth, and Regional Forecast, 2025 to 2032

Disposable Medical Supplies Market by Product (Wound Management Products, Drug Delivery Products, Infection Prevention Products, Diagnostic Supplies), Material (Plastic, Paper, Metal, Glass), End-user (Hospitals and Clinics, Ambulatory Surgery Centers, Home Healthcare, Diagnostic Centers, Others), and Regional Analysis from 2025 to 2032

Disposable Medical Supplies Market Share and Trends Analysis

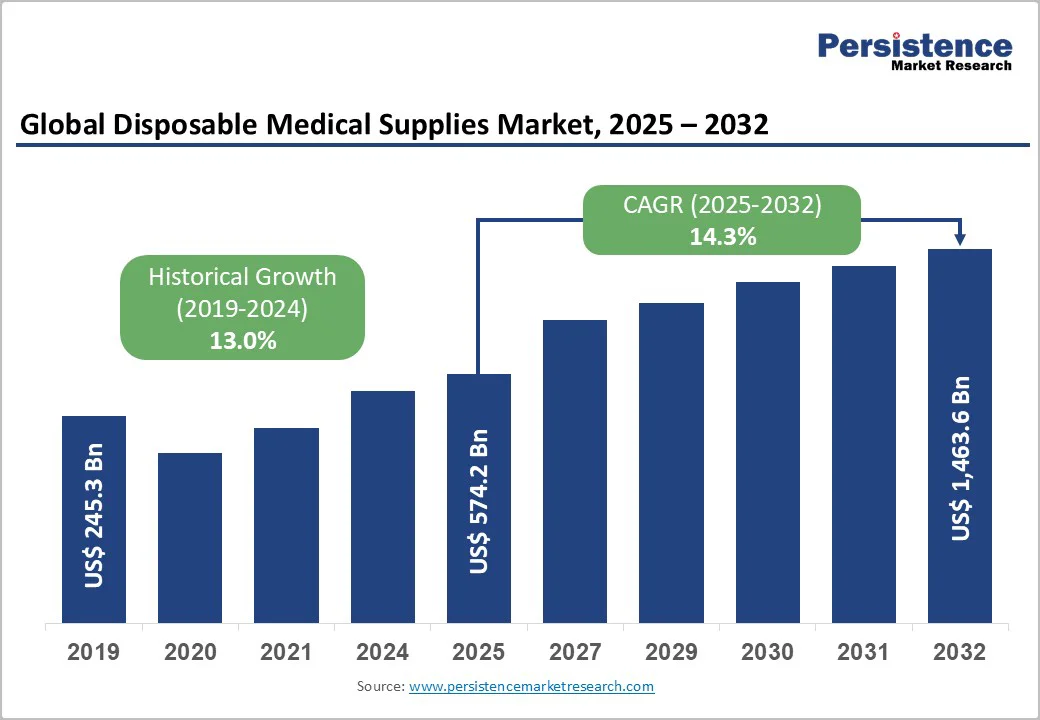

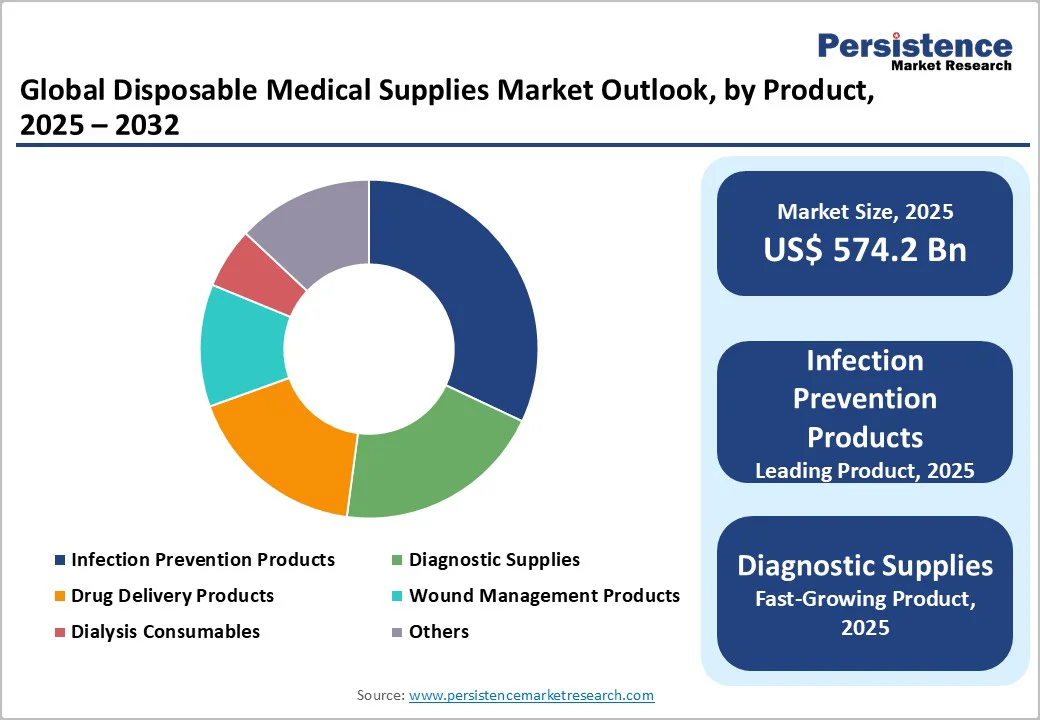

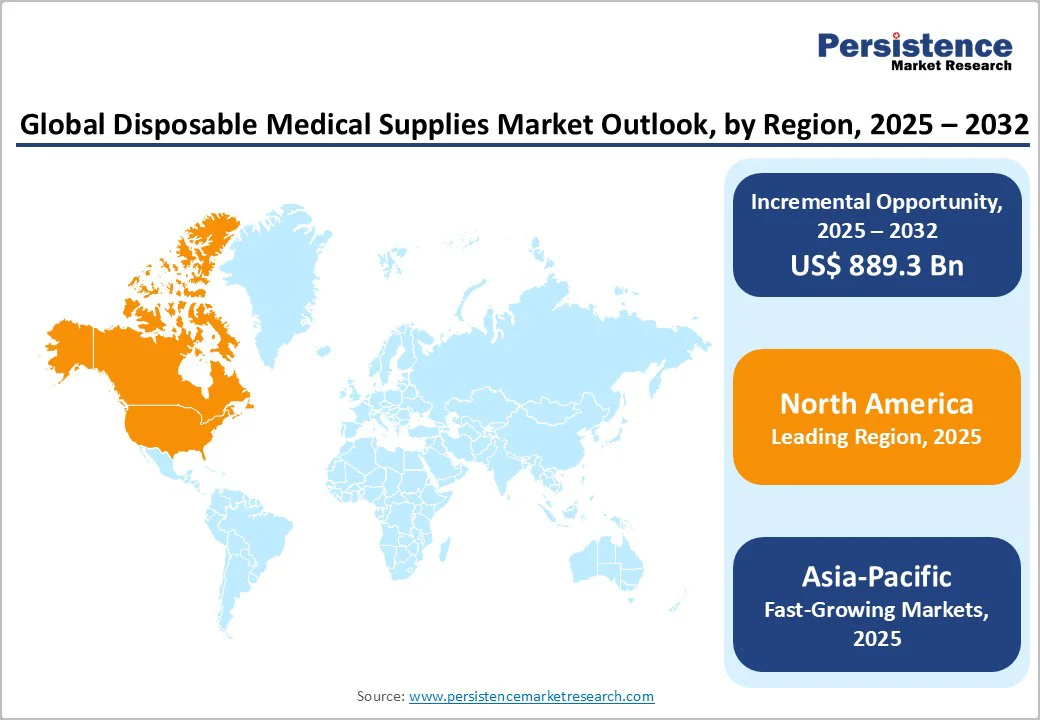

The global disposable medical supplies market size is valued at US$574.2 billion in 2025 and is projected to reach US$1,463.6 billion, growing at a CAGR of 14.3% from 2025 to 2032.

The disposable medical industry is expanding steadily, fueled by rising surgical volumes, infection-control needs, and the shift toward single-use products for safety and efficiency. North America leads due to its advanced healthcare infrastructure and strong regulatory support. At the same time, the Asia-Pacific region is the fastest-growing region driven by increasing hospital capacity, higher patient volumes, and rapid adoption of cost-effective disposable solutions.

Key Industry Highlights:

- Dominant Segment: Infection prevention products hold the largest share with 32.0% in 2025, driven by growing hospital-acquired infection (HAI) risks, rising surgical procedures, and strong adoption of sterile, single-use consumables across hospitals and ambulatory centers.

- Dominant Region: North America leads the market with its advanced healthcare infrastructure, strict infection-control regulations, higher disposable usage per patient, and strong presence of global manufacturers.

- Investment Plans: Asia-Pacific is the fastest-growing region, driven by rapid hospital expansion, rising healthcare budgets, growth in medical tourism, and increasing local production of cost-effective disposables in China, India, and Southeast Asia.

- Growth Indicators: Increasing chronic diseases, rising surgical volumes, emphasis on infection control, expansion of home healthcare, and growing preference for single-use medical supplies to reduce contamination risks.

- Market Opportunity: Development of biodegradable and eco-friendly disposables, automation-ready sterile packaging, smart single-use sensors, localized manufacturing hubs, and penetration into emerging markets with rising outpatient and emergency care demand.

| Key Insights | Details |

|---|---|

| Global Disposable Medical Supplies Market Size (2025E) | US$574.2 Bn |

| Market Value Forecast (2032F) | US$ 1,463.6 Bn |

| Projected Growth (CAGR 2025 to 2032) | 14.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 13.0% |

Market Dynamics

Driver - Rising Burden of Chronic and Infectious Diseases

The rising burden of chronic and infectious diseases is a key driver of the Disposable Medical Supplies Market, as growing patient volumes directly increase the need for sterile, single-use products. According to the World Health Organization (WHO), non-communicable diseases such as cardiovascular disease, diabetes, chronic respiratory illness, and cancer were responsible for around 43 million deaths in 2021, representing about 74% of global non-pandemic deaths.

This growing chronic disease burden results in more hospital visits, longer-term treatments, and frequent use of items such as catheters, syringes, IV sets, and wound-care supplies. Simultaneously, infectious diseases and hospital-acquired infections (HAIs) remain a major concern.

WHO reports that up to 15% of hospitalized patients in low- and middle-income countries acquire an infection during their stay. At the same time, antimicrobial-resistant HAIs contribute to millions of complications each year. These trends reinforce the need for safe, sterile, disposable supplies to reduce cross-contamination, prevent the spread of infection, and support the expanding global healthcare demand.

Restraints - Rising Environmental Concerns

Rising environmental concerns are a significant restraint on the Disposable Medical Supplies Market, as the heavy reliance on single-use plastics creates substantial waste-management challenges. According to the World Health Organization (WHO), healthcare facilities generate millions of tonnes of waste annually, with around 15% classified as hazardous, including infectious or chemically contaminated materials requiring specialized treatment.

High-income countries produce nearly 0.5 kg of hazardous healthcare waste per hospital bed per day, while low-income nations generate approximately 0.2 kg. The COVID-19 pandemic further intensified the issue. WHO reported over 87,000 tonnes of excess PPE waste entering the global waste stream, mostly composed of plastic-based disposable items.

Improper disposal through open burning or uncontrolled incineration can release toxic pollutants such as dioxins, furans, and particulate matter, contributing to environmental degradation and public health risks. These concerns are prompting governments and healthcare systems to push for stricter waste regulations and more sustainable, biodegradable alternatives, increasing compliance pressure on manufacturers.

Opportunity - Eco-Friendly and Biodegradable Disposables

Eco-friendly and biodegradable disposables represent a powerful opportunity for the disposable medical supplies market because they directly address mounting environmental pressures. Hospitals worldwide generate millions of tonnes of plastic waste each year, much of it single-use and persistent in landfills and the oceans. Only about 5% of healthcare plastics are currently recycled, according to recent reports.

Biodegradable materials like polylactic acid (PLA) and polyhydroxyalkanoates (PHAs) derived from plants or microbes offer a greener alternative, degrading into non-toxic byproducts under the right conditions. For example, a research initiative at UNSW is developing PHA-based medical packaging to replace petroleum-based plastics, aligning with circular-economy goals.

By investing in sustainable materials, manufacturers can reduce plastic waste, lower their carbon footprint, and meet growing regulatory and societal demand for greener healthcare solutions.

Category-wise Analysis

By Product, Infection Prevention Products Dominate the Disposable Medical Supplies Market

Infection Prevention Products occupy 32.0% share of the global market in 2025, because they are critical for reducing hospital-acquired infections (HAIs), which remain a major international concern. The World Health Organization reports that HAI prevalence can reach up to 15% of hospitalized patients in low- and middle-income countries, with surgical and ICU wards showing the highest risk.

Basic disposables such as gloves, masks, gowns, drapes, and sterile syringes are frontline tools for preventing cross-contamination. In the U.S., infection-control guidelines strongly emphasize single-use protective gear, with most hospitals relying heavily on disposable PPE to maintain sterility.

These strict infection-control requirements and high consumption rates make infection-prevention items indispensable, driving their leadership within the overall disposable medical supplies market.

By Material, Plastic is gaining traction due to low cost, sterility, durability, mass production, and widespread clinical reliance.

Plastic products dominate the Disposable Medical Supplies Market because they offer low cost, durability, sterility, and flexibility for mass production of essential items like syringes, IV bags, tubing, gloves, and specimen containers. According to the World Health Organization (WHO), nearly 85% of all healthcare waste is non-hazardous, much of it composed of plastic-based single-use items.

U.S. hospitals generate around 14,000 tons of waste per day, with an estimated 20-25% of it plastic, reflecting the scale of plastic disposables use. Plastics such as polypropylene (PP), polyethylene (PE), and PVC are preferred due to their compatibility with sterilization and medical-grade standards. Their reliability, affordability, and widespread clinical acceptance make plastics the dominant material in disposable medical supplies worldwide.

Regional Insights

North America Disposable Medical Supplies Market Trends

North America dominates the disposable medical supplies market with 36.7% share in 2025, due to its high healthcare spending, advanced medical infrastructure, and strong focus on infection control. The U.S. spends about 17% of its GDP on healthcare, one of the highest globally, according to the OECD.

Per-capita spending reached USD 12,555 in 2022, more than double the OECD average, supporting high procedure volumes and widespread adoption of single-use consumables. U.S. hospitals also generate significant medical waste, studies estimate over 6,600 metric tons per day, much of it from disposable plastics used in surgeries, diagnostics, and routine patient care.

Strict CDC and OSHA guidelines further push hospitals toward sterile, single-use items to reduce contamination risks, reinforcing North America’s market leadership.

Europe Disposable Medical Supplies Market Trends

Europe is an important region in the disposable medical supplies market due to its strong healthcare infrastructure, high public investment, and stringent infection-control regulations. According to Eurostat, EU countries spend roughly 10% of their GDP on healthcare, amounting to about €1.6 trillion in 2022, with nearly 18% of this directed toward medical goods, including disposable products.

Hospitals account for more than 36% of total health expenditure, reflecting high utilization of single-use supplies in surgeries, diagnostics, and inpatient care. The region also maintains strict hygiene and sterilization standards under EU medical device regulations, driving consistent demand for sterile disposables. Europe’s ageing population and rising chronic disease burden further support consumption, making it a critical and stable market for disposable medical supplies.

Asia-Pacific Disposable Medical Supplies Market Trends

Asia-Pacific is the fastest-growing region in the disposable medical supplies market due to rapid healthcare expansion, rising incomes, and a growing disease burden. According to the OECD, per-capita health spending in Asia-Pacific increased by 65% in lower-middle-income countries and 76% in upper-middle-income countries between 2010 and 2019, reflecting major investment in hospitals, equipment, and medical consumables.

Many nations are scaling healthcare capacity. WHO reports that lower-middle-income Asian countries have about 2.8 hospital beds per 1,000 people, and this number is rising as governments boost infrastructure. Ageing populations and increasing chronic diseases further accelerate demand for sterile, single-use supplies. Combined with growing local manufacturing capabilities, these factors make the Asia-Pacific region the one with the fastest market growth.

Competitive Landscape

Leading companies in the disposable medical supplies market focus on high-volume production, sterile manufacturing, and material innovation. They invest in improved infection-prevention products, cost-efficient plastics, eco-friendly alternatives, and automated production lines.

Strategic partnerships with hospitals and distributors enhance supply reliability, while R&D efforts target safer, stronger, and more sustainable disposables to meet rising surgical volumes, infection-control needs, and expanding global healthcare demand.

Key Industry Developments:

- In March 2025, Visby Medical™ reported that the FDA granted De Novo authorization for its Women’s Sexual Health Test, a single-use at-home diagnostic kit that provides rapid and accurate detection of sexually transmitted infections, including Gonorrhea, Chlamydia, and Trichomoniasis.

- In February 2025, Rockwell Medical announced a distribution services agreement with a major manufacturer of medical disposable products and equipment, including hemodialysis machines and automated fluid balance systems. Through this partnership, Rockwell Medical will supply its newly launched single-use bicarbonate cartridge to customers across hospital-based outpatient centers, dialysis centers, and nursing facilities.

Companies Covered in Disposable Medical Supplies Market

- Cardinal Health, Inc.

- Covidien plc.

- 3M Health Care Ltd.

- Halyard Health, Inc.

- Molnlycke Health Care AB

- Medline Industries Inc.

- Sempermed USA, Inc.

- Ansell Healthcare LLC

- Nipro Corp.

- McKesson Corp.

- Others

Frequently Asked Questions

The global disposable medical supplies market is projected to be valued at US$ 574.2 Bn in 2025.

Rising surgeries, infection-control needs, chronic diseases, expanding hospitals, aging populations, and increasing preference for sterile, single-use medical products drive market growth.

The global disposable medical supplies market is poised to witness a CAGR of 14.3% between 2025 and 2032.

Eco-friendly disposables, localized manufacturing, smart single-use devices, home-care consumables, and rising healthcare demand in emerging markets create strong growth opportunities.

Cardinal Health, Inc., Covidien plc., 3M Health Care Ltd., Halyard Health, Inc.,Molnlycke Health Care AB, Medline Industries Inc.