- Medical Devices

- Digital Orthodontics Market

Digital Orthodontics Market Size, Share, and Growth Forecast, 2026 – 2033

Digital Orthodontics Market by Product Type (X-rays, Lasers, White Light, Others), Technology (Printing, Imaging, Digital Photography, Others), End-user (Hospitals, Ambulatory Care Centers, Others), and Regional Analysis for 2026 – 2033

Digital Orthodontics Market Size and Trends Analysis

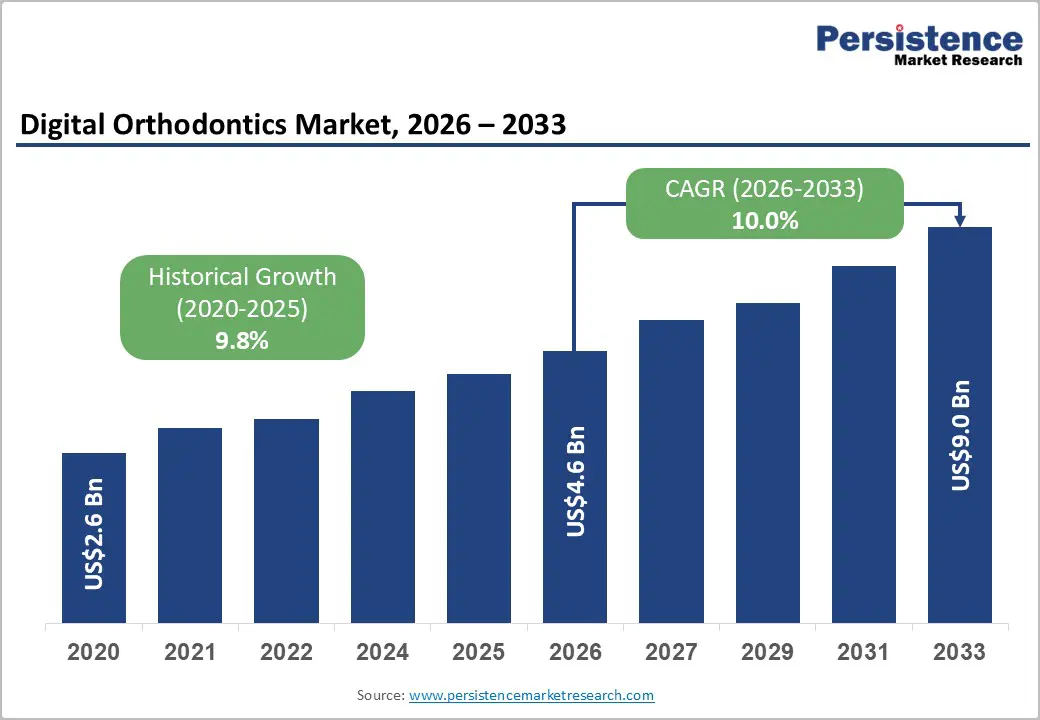

The global digital orthodontics market size is likely to be valued at US$4.6 billion in 2026 and is expected to reach US$9.0 billion by 2033, growing at a CAGR of 10.0% during the forecast period from 2026 to 2033, driven by the rising prevalence of malocclusion, creating strong demand for precise, efficient, and patient-friendly orthodontic solutions.

Advanced technologies such as 3D imaging, intraoral scanners, and computer-aided design/manufacturing (CAD/CAM) are accelerating treatment timelines, enhancing accuracy, and enabling fully customized clear aligners, retainers, and braces.

The integration of tele-dentistry platforms, accelerated in the post-pandemic era, enables remote monitoring, enhances patient compliance, and supports personalized treatment adjustments. Growing aesthetic awareness, particularly among adult orthodontic patients, combined with an increasing preference for minimally invasive procedures, reinforces market adoption. Innovations in software analytics, cloud-based treatment planning, and 3D printing are enabling dental professionals to streamline workflows, reduce chair time, and enhance patient experience. These technological, clinical, and demographic trends position digital orthodontics as a key driver of modern, patient-centric orthodontic care.

Key Industry Highlights:

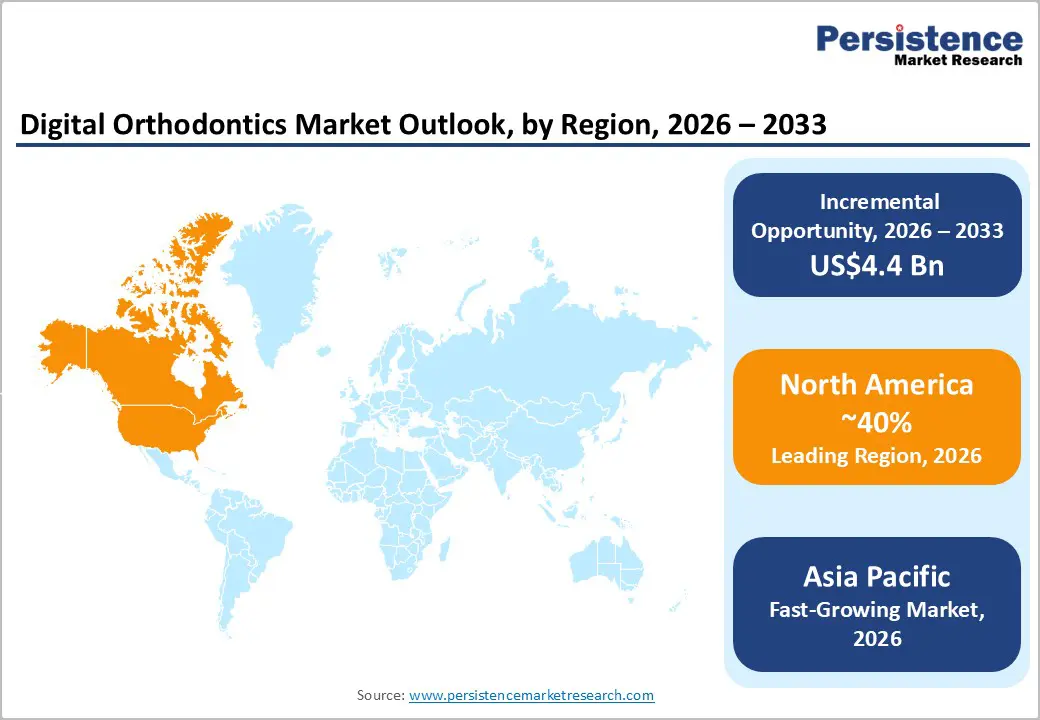

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by high adoption of digital tools, strong aesthetic demand, advanced infrastructure, and a mature tele-dentistry ecosystem.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by the expansion of healthcare infrastructure, rising dental awareness, and local manufacturing advantages.

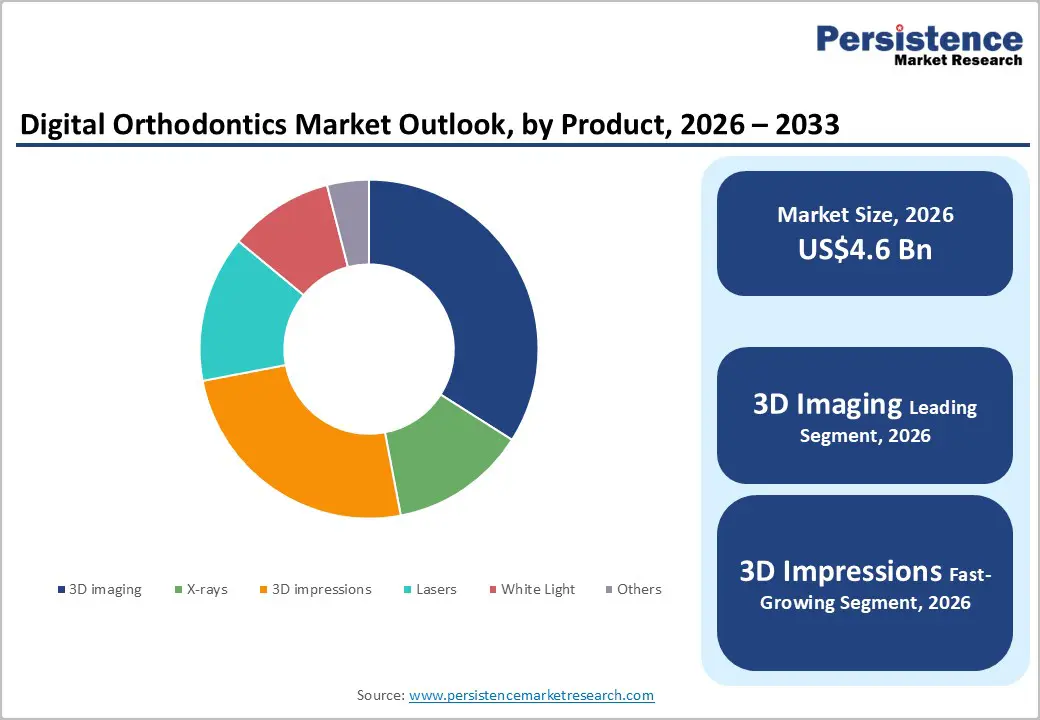

- Leading Product Type: 3D imaging is projected to represent the leading product type in 2026, accounting for 45% of the revenue share, driven by its role in precise diagnosis, treatment planning, and seamless CAD/CAM integration.

- Leading Technology Type: Computer-aided design/computer-aided manufacturing (CAD/CAM) is anticipated to be the leading technology type, accounting for over 40% of the revenue share in 2026, supported by its precision in appliance fabrication, workflow automation, and integration with 3D imaging for accurate orthodontic treatments.

| Key Insights | Details |

|---|---|

|

Digital Orthodontics Market Size (2026E) |

US$4.6 Bn |

|

Market Value Forecast (2033F) |

US$9.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

10.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

9.8% |

DRO Analysis

Driver Analysis- Rising Prevalence of Malocclusion and Orthodontic Demand

The increasing prevalence of malocclusion, affecting a significant portion of the population, has intensified the demand for orthodontic interventions. As awareness of dental aesthetics and oral health grows, patients are seeking precise and efficient solutions, prompting clinics to adopt digital orthodontic technologies. These technologies facilitate accurate diagnosis, treatment simulation, and monitoring, addressing complex dental alignment challenges while enhancing patient satisfaction. Demographic shifts toward adult orthodontic treatment, where aesthetic considerations are more critical, reinforce the need for advanced digital workflows, positioning digital orthodontics as a vital component in modern dental practice.

The sustained growth in orthodontic procedures drives investment in high-precision tools such as 3D imaging, intraoral scanners, and CAD/CAM systems. Dental professionals are increasingly integrating these solutions to reduce chair time, improve treatment accuracy, and streamline appliance fabrication. Tele-dentistry platforms complement this trend, enabling remote monitoring and better patient adherence to treatment plans. As populations urbanize and middle-class spending rises, clinics are responding to the higher demand with scalable digital solutions, ensuring consistent treatment quality.

Technological Advancements in 3D Imaging and CAD/CAM Systems

Innovations in 3D imaging, including CBCT and digital volumetric scanning, have transformed orthodontic workflows by enabling highly accurate visualization of dental structures. These advancements allow practitioners to plan treatments with precision, simulate outcomes, and fabricate appliances with minimal manual intervention. CAD/CAM systems enhance efficiency, facilitating the design and rapid production of custom aligners, retainers, and braces. The integration of these technologies reduces errors, shortens treatment timelines, and improves patient comfort, driving widespread adoption in both private clinics and large dental centers.

Enhanced software algorithms and cloud-based platforms complement imaging and CAD/CAM systems, allowing seamless data transfer between clinics, laboratories, and patients. Real-time analytics, predictive modeling, and automated appliance generation have lowered barriers for complex treatments and increased workflow efficiency. These improvements also enable tele-dentistry integration, supporting remote consultations and follow-ups. The technological evolution in digital orthodontics provides a competitive edge, helping dental practices deliver personalized, high-quality care while reducing costs and optimizing resource utilization.

Restraint Analysis - Lack of Standardized Protocols and Interoperability Issues

The absence of standardized protocols across digital orthodontic platforms limits seamless data sharing between devices, software, and laboratories. Diverse file formats, proprietary systems, and inconsistent workflow practices create operational inefficiencies and increase the potential for errors. Dental professionals often face challenges integrating intraoral scanners, imaging devices, and CAD/CAM systems from different vendors, slowing adoption in smaller clinics. Regulatory and technical inconsistencies across regions exacerbate interoperability concerns, preventing uniform implementation of digital workflows.

Interoperability challenges also impact collaboration with dental laboratories and multi-clinic networks, reducing operational efficiency and prolonging treatment timelines. The need for cross-platform data translation or manual adjustments increases cost and labor, limiting the scalability of digital orthodontics. Software updates and hardware compatibility issues can result in additional training requirements and maintenance overheads. Addressing these challenges through standardized communication protocols, open-source data formats, and unified software ecosystems is critical for encouraging wider adoption, facilitating seamless integration, and unlocking the full potential of digital orthodontic technologies across markets.

Shortage of Skilled Professionals and Training Gaps

A critical challenge in the digital orthodontics landscape is the shortage of trained professionals capable of operating advanced imaging, scanning, and CAD/CAM systems. Many dental practitioners remain accustomed to traditional analog workflows, requiring extensive training to adopt digital tools effectively. The learning curve for precise digital treatment planning, intraoral scanning, and 3D appliance design can be steep, especially in regions with limited continuing education resources. This skill gap slows adoption rates, limits the utilization of high-end equipment, and constrains smaller clinics from transitioning fully to digital workflows, despite the evident benefits for accuracy and efficiency.

Training gaps also impact patient outcomes and operational efficiency, as improper use of devices can lead to errors in impressions, appliance fabrication, and treatment simulation. Dental schools and professional programs are increasingly incorporating digital orthodontics modules, but inconsistent curriculum adoption across regions delays workforce readiness. Manufacturers and distributors often provide in-house training, yet widespread access remains limited. Bridging these gaps through structured education, workshops, and certification programs is essential to expand the skilled workforce, improve confidence in digital solutions, and accelerate the adoption of advanced orthodontic technologies.

Opportunity Analysis - Technological Convergence with AI and Smart Devices

The integration of artificial intelligence (AI) and smart devices with digital orthodontic systems presents a significant growth opportunity. AI-driven treatment planning tools can predict optimal tooth movement, automate appliance design, and provide personalized treatment recommendations. Coupled with smart devices such as intraoral sensors, wearable trackers, and mobile monitoring apps, these technologies enable real-time patient feedback, improved compliance, and predictive analytics. Such convergence enhances workflow efficiency, reduces treatment errors, and delivers superior clinical outcomes, positioning dental practices at the forefront of precision orthodontics and opening new avenues for innovation in digital solutions.

AI-enabled automation also supports remote monitoring and tele-dentistry, allowing practitioners to track progress, adjust treatment plans, and communicate with patients virtually. Predictive models can identify potential complications early, reducing the need for corrective procedures. Smart devices can collect behavioral and oral hygiene data, contributing to personalized care plans and higher patient engagement. Investment in AI and connected device ecosystems creates opportunities for partnerships, software as a service platform, and advanced appliance manufacturing, reinforcing the market’s shift toward intelligent, data-driven orthodontic practices.

Expansion of Clear Aligner Manufacturing to General Dental Practitioners (GDPs)

Expanding clear aligner manufacturing access to general dental practitioners represents a key opportunity to increase market penetration. By enabling GDPs to offer orthodontic treatments, practices can meet rising patient demand without referring to specialized orthodontists. Digital workflows, including intraoral scanning, CAD/CAM appliance design, and 3D printing, simplify aligner production, reducing barriers for non-specialist clinics. This democratization of treatment provision allows for faster service delivery, improved patient convenience, and broader adoption of aesthetic orthodontics across urban and semi-urban regions, ultimately expanding the overall market for digital orthodontic solutions.

Partnerships between aligner manufacturers and GDPs provide training, software access, and workflow support, enabling high-quality treatment without extensive orthodontic expertise. Clinics can leverage digital platforms for treatment simulation, monitoring, and appliance adjustments, maintaining outcome precision while scaling operations. The approach also opens opportunities in emerging markets, where specialized orthodontic services are limited, by offering affordable, locally produced aligners. This expansion strategy enhances revenue streams for both manufacturers and dental practices while accelerating patient access to minimally invasive, digitally enabled orthodontic care.

Category-wise Analysis

Product Type Insights

3D imaging is expected to lead the digital orthodontics market, accounting for approximately 45% of revenue in 2026, driven by its critical role in accurate diagnosis, treatment planning, and simulation across modern orthodontic practices. By combining cone-beam computed tomography (CBCT) with multi-dimensional visualization tools, 3D imaging allows practitioners to precisely evaluate malocclusion, jaw structure, and tooth movement trajectories. For example, the integration of Carestream Health’s CS 9600 CBCT system has been widely adopted in clinics for orthodontic diagnostics, providing high-resolution imaging that supports precise treatment simulations.

3D impressions are likely to represent the fastest-growing segment, supported by the adoption of intraoral scanners and the elimination of traditional impression materials. These digital impressions reduce procedural discomfort, shorten chair time, and increase accuracy, directly benefiting patient experience and clinic efficiency. For example, 3Shape’s TRIOS intraoral scanner enables clinicians to capture highly detailed digital impressions quickly, automatically integrating with CAD/CAM systems to fabricate clear aligners, retainers, and orthodontic appliances.

Technology Type Insights

Computer-aided design/Computer-aided manufacturing (CAD/CAM) is projected to lead the market, capturing around 40% of the revenue share in 2026. Its dominance arises from its ability to automate appliance design and production with high precision, ensuring custom-fit aligners, retainers, and braces for orthodontic patients. CAD/CAM systems reduce manual labor, lower error rates, and accelerate treatment timelines, enhancing clinic efficiency and patient satisfaction. For example, Align Technology’s Invisalign CAD/CAM workflow utilizes sophisticated software to design patient-specific clear aligners, which are then manufactured using automated milling and printing processes.

Intraoral scanners are likely to be the fastest-growing technology type, driven by the convenience of chairside digital impressions and integration with 3D printing workflows. These scanners enhance clinical efficiency by eliminating traditional molds, reducing patient discomfort, and enabling faster appliance fabrication. For example, 3M’s True Definition Scanner offers high-resolution digital captures that can be directly transmitted to CAD/CAM systems for appliance production. The segment’s growth is supported by rising adoption in both private practices and hospital settings, as clinicians leverage wireless scanning and cloud-based storage to improve workflow and tele-dentistry capabilities.

Regional Insights

North America Digital Orthodontics Market Trends

North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by high demand for technologically advanced treatment solutions and a strong focus on patient-centric care. Key trends include widespread adoption of digital imaging and intraoral scanning technologies that enhance diagnostic accuracy and streamline workflows. This shift is supported by a mature healthcare infrastructure, regulatory clarity around digital devices, and relatively high per-capita spending on dental care.

For example, Align Technology’s Invisalign ecosystem exemplifies this trend by combining digital scans, predictive modeling, and CAD/CAM-produced clear aligners, enabling precise, patient-friendly orthodontic treatments while improving operational efficiency for providers.

Digital platforms that integrate intraoral scans with cloud-based monitoring tools allow practitioners to assess progress remotely, reducing unnecessary office visits and improving treatment adherence. Partnerships between technology developers and dental service organizations are accelerating the deployment of advanced devices across broader networks. With ongoing innovation, especially in AI and data analytics, North America’s market is poised for continued growth, driven by enhanced digital experiences, operational efficiencies, and improved clinical outcomes.

Europe Digital Orthodontics Market Trends

Europe is likely to be a significant market for digital orthodontics, due to well-established healthcare systems and patient demand for high-quality care. A significant trend is the integration of digital impressions and imaging into routine orthodontic workflows, with intraoral scanners and 3D visualization becoming standard tools across clinics in Germany, the UK, France, and Italy. For example, Dentsply Sirona’s CEREC Primescan, widely adopted across European practices, enables rapid, precise intraoral scans that seamlessly integrate with CAD/CAM workflows for designing orthodontic appliances.

Tele dentistry and cloud-based platforms are increasingly integrated with scanning and imaging systems, enabling remote treatment planning and monitoring, which expands service reach and enhances patient convenience. Clinics are also leveraging digital data exchange with laboratories to accelerate appliance fabrication and reduce turnaround times. Regulatory emphasis on data standards, quality, and patient safety ensures that technologies such as CBCT imaging and digital impressions meet stringent performance thresholds, building clinician confidence.

Asia Pacific Digital Orthodontics Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by the rising disposable incomes, growing aesthetic awareness, and improving healthcare infrastructure, which are driving increased adoption of advanced orthodontic solutions across the region. Urban centers in China, Japan, India, and ASEAN nations are witnessing heightened demand for digital workflows such as intraoral scanning, 3D imaging, and CAD/CAM integration, which enable more accurate diagnostics and personalized treatment plans.

Younger populations, influenced by cosmetic trends and social media, are seeking minimally invasive treatments such as clear aligners, while technology adoption is supported by government initiatives that promote digital health and oral care awareness.

Core clinical adoption, collaborations between companies and regional partners are fueling innovation and local market penetration. For example, Align Technology’s expansion of its Invisalign clear aligners and digital treatment platforms in Asia Pacific has accelerated the integration of digital orthodontic workflows in major cities, offering tailored solutions that enhance clinical outcomes and patient experience. The company’s partnerships with local dental networks enable better access to digital scanning and treatment planning tools, addressing both urban and semi-urban demand.

Competitive Landscape

The global digital orthodontics market exhibits a moderately fragmented structure, driven by strong innovation, rapid adoption of integrated digital workflows, and the presence of established and emerging competitors focused on varied technology offerings and geographic expansion. Market players span a spectrum from large multinationals to niche specialists, all investing in product development to meet clinician demands for precision, efficiency, and improved patient experience.

With key leaders including Align Technology, Inc., 3Shape A/S, Dentsply Sirona Inc., 3M Company, Planmeca Oy, and Ormco Corporation, competition remains intense around proprietary scanning, imaging, CAD/CAM systems, and AI-enabled treatment planning platforms, as well as clear aligner solutions that are core to digital orthodontic adoption. These players compete through continuous technological innovation, strategic collaborations, and expansion of product portfolios tailored to orthodontic practices and dental clinics worldwide.

Key Industry Developments:

- In February 2026, Smile White launched what it claims to be the first fully online dentist-prescribed clear aligner platform, enabling patients to begin their orthodontic treatment journey entirely online by uploading photos that are automatically analysed using a machine-learning model to assess case complexity. After the initial digital assessment, patients are connected with Smile White-accredited dentists who perform clinical evaluations using 3D scanning to finalise treatment planning, blending digital convenience with professional oversight.

- In February 2025, Henry Schein UK launched Smilers and Smilers Expert, advanced clear aligner systems designed for general dental practitioners and orthodontists, aimed at correcting malocclusions and enhancing smile aesthetics. These systems are powered by the NemoCast software suite from Nemotec, a cloud-based digital orthodontics platform that supports treatment visualization, diagnosis, and planning, improving precision and clinical efficiency for aligner therapy.

- In May 2025, Align Technology, Inc. launched a marketing campaign, “20M smiles, 20M stories,” highlighting doctors using digital orthodontic tools such as Invisalign® aligners, iTero™ scanners, and exocad™ CAD/CAM software, celebrating the milestone of 20 million smiles transformed and showcasing the impact of digital workflows on patient outcomes.

Companies Covered in Digital Orthodontics Market

- 3M

- Dentsply Sirona

- Stratasys Ltd.

- 3Shape

- Altem Technologies (P) Ltd

- Align Technology, Inc

- Carestream Health

- Planmeca Oy

- Angelalign Technology

- Dentaurum

- Ormco

- Deltaface

- CADdent

- Boss Orthodontics

- FN Orthodontics

Frequently Asked Questions

The global digital orthodontics market is projected to reach US$4.6 billion in 2026.

The digital orthodontics market is driven by the rising prevalence of malocclusion and increasing adoption of advanced technologies such as 3D imaging, intraoral scanners, and CAD/CAM systems for precise, efficient, and patient-centric orthodontic treatments.

The digital orthodontics market is expected to grow at a CAGR of 10.0% from 2026 to 2033.

Key market opportunities lie in the integration of AI and smart devices, the expansion of clear aligner solutions to general dental practitioners, and the growth of tele‑orthodontics for remote treatment and monitoring.

3M, Dentsply Sirona, Stratasys Ltd., 3Shape, Altem Technologies (P) Ltd, Align Technology, and Carestream Health are the leading players.